Last week, the U.S. Food and Drug Administration (FDA) and the Federal Trade Commission (FTC) sent out warning letters to six different companies for selling copycat food products that contain Delta-8 THC. In a press release published on July 5, the FDA and FTC said they sent out letters to the following companies:

Delta Munchies

Smoke LLC (also known as Dr. S LLC)

Exclusive Hemp Farms/Oshipt

Nikte’s Wholesale LLC

North Carolina Hemp Exchange LLC

The Haunted Vapor Room

The Haunted Vapor Room, Dope Rope Bites

The products in question look exactly like common name brand foods like chips, candy and other snack foods. The FDA says they are concerned they might be mistaken for traditional foods, accidentally ingested by children or taken in higher doses than intended. “The products we are warning against intentionally mimic well-known snack food brands by using similar brand names, logos, or pictures on packaging, that consumers, especially children, may confuse with traditional snack foods,” says Janet Woodcock, M.D., principal deputy commissioner at the FDA. “The FDA remains committed to taking action against any company illegally selling regulated products that could pose a risk to public health.”

This is the first time since 2019 that the FTC has gotten involved, when they issued similar joint letters to companies making unsubstantiated health claims. “Marketing edible THC products that can be easily mistaken by children for regular foods is reckless and illegal,” says Samuel Levine, director of the Bureau of Consumer Protection at the FTC. “Companies must ensure that their products are marketed safely and responsibly, especially when it comes to protecting the well-being of children.”

By Andrew Solow, David Kerschner, Alessandra Lopez No Comments

In 2022, product liability lawsuits in the cannabis/cannabidiol (CBD) industry continued to focus on levels of THC and the psychoactive ingredient in cannabis, while federal agencies continued issuing warning letters for CBD products (including CBD-infused food and dietary supplements) that made misleading medical claims. Against this backdrop of ongoing litigation and regulatory enforcement, 2022 showed that at the Federal level, there is more recognition that marijuana is becoming increasingly normalized. For example, President Biden pardoned federal offenses of simple marijuana possession and requested a reassessment of marijuana’s classification as a Schedule I drug under federal law. Additionally, Congress passed its first standalone piece of cannabis reform with the Medical Marijuana and Cannabidiol Research Expansion Act (MMCREA) which, among other things, will ease restrictions on cannabis research and allow for more clinical trials. And even though the Food and Drug Administration (FDA) declined to act on CBD products, the agency announced that it will work with Congress to create a new regulatory framework for CBD products (2023 FDA Announcement).

These events of the past year provide a glimpse into what the future may hold for cannabis and CBD companies when it comes to product liability risks. This article looks at the types of product liability actions that the cannabis and CBD industry faced in 2022 and may encounter in the future, and provides some basic guidance on how to best mitigate, and if necessary, defend these potentially costly litigations.

Focus on Cannabis and CBD Risks

A central part of any product liability lawsuit—regardless of whether brought under a design defect and/or adequate warning theory—is that a product caused or was a substantial contributing factor to a Plaintiff’s injury or illness. Thus, any potential safety concerns over cannabis/CBD could end up as the subject of litigation in the future. In the 2023 FDA Announcement, the FDA recognized that “the use of CBD raises various safety concerns, especially with long-term use,” including potential harm to the liver and negative interactions with certain medications. The agency also noted that questions still exist on how much CBD can be consumed, and for how long, before causing harm. Furthermore, on December 2, 2022, President Biden signed the MMCREA into law, which is intended to advance research on the potential risks and medical benefits of cannabis and cannabis products.1 This additional funding will not only help researchers learn more about possible safety risks that may lead to future product liability claims, but will also allow for better exploration of the benefits of these products to possibly expand product indications and help reach new customers.

Given the FDA’s statements and the increased funding for new research, CBD and cannabis companies should ensure that they are properly monitoring both regulatory communications and new research regarding risks that may be associated with their products. As new information is released, companies should evaluate how their product labels and marketing messages should be altered. Announcements like this one by the FDA can be seen as providing industry participants with knowledge about certain risks, and how companies react could be analyzed, post hoc, in any litigation down the road.

2022 Product Liability Actions

Over the last year, misbranding/mislabeling issues presented some of the most prevalent litigation risks for industry participants.

An example of a warning letter the FDA sent to a CBD products company making health claims

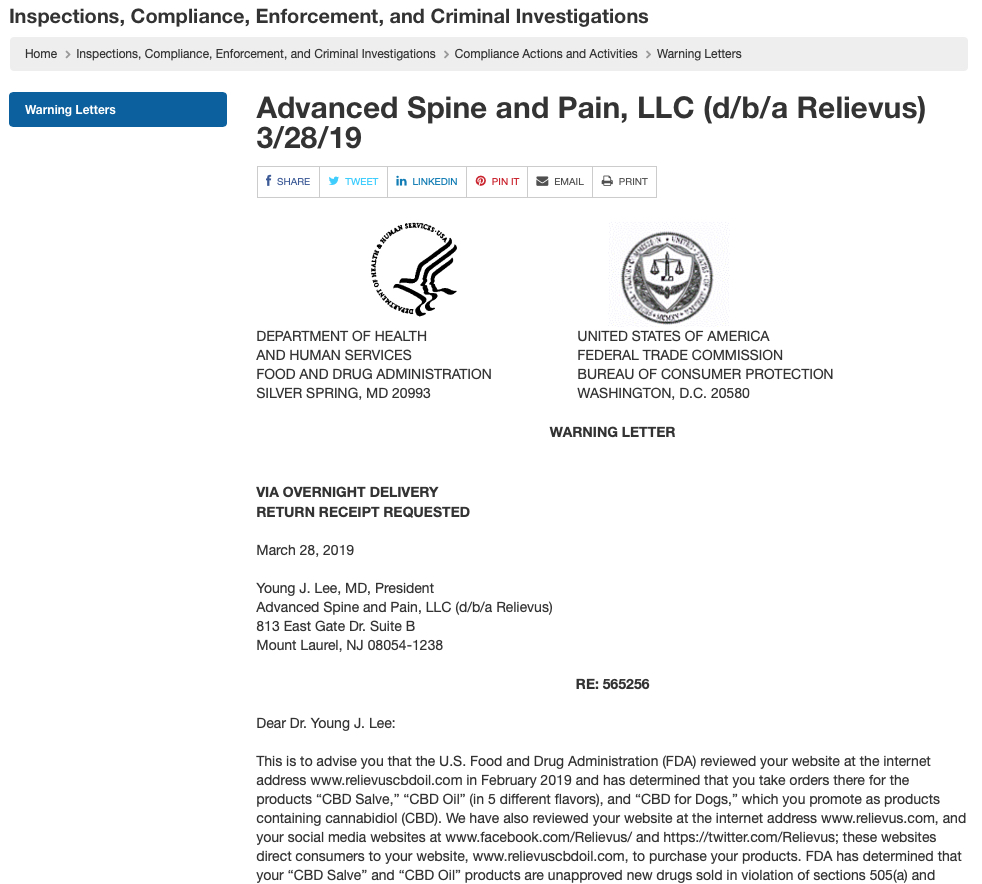

For example, at the Federal level in 2022, the FDA issued thirty-three warning letters to CBD companies, a nearly 400% increase from 2021. These letters generally focused on CBD products that made medical claims. Some of these warning letters addressed misbranding, where the product labels provided inadequate directions for consumer use. In one letter, the FDA noted that because the CBD products were “offered for conditions that are not amendable to self-diagnosis and treatment by individuals who are not medical practitioners,” ranging from cancer to diabetes, labeling compliance was only possible if the product was an FDA-approved prescription drug with FDA-approved labeling. Other companies receivedwarning letters in March of 2022 for making misleading representations that their CBD products were safe and/or effective to prevent or treat COVID-19. Many of these representations were made via companies’ websites and social media platforms. The warning letters—often triggers for product liability actions, as well as consumer protection/fraud actions—serve as a reminder that companies cannot make medical claims on non-FDA approved drug products and must otherwise present accurate information to consumers not only on product packaging, but any form of marketing or advertising, including company websites and social media platforms.

Turning to state-level regulatory actions, Oregon’s Liquor and Cannabis Commission fined a cannabis company $130,000 and suspended the company’s license for 23 days over an alleged label mix-up between its CBD and THC products. According to the state’s investigative report, a company employee allegedly confused two product buckets with similar identification numbers, one that contained THC and the other CBD, and accidentally switched the labels of the two products. In addition to the fine and license-suspension, the state agency also issued a mandatory recall on the CBD drops based on the alleged undisclosed levels of THC.

This same incident also spurred a string of civil lawsuits, resulting in several settlements by the company in 2022.2 Numerous customers reported experiencing “paranoia,” “mind fog,” and feeling “extremely high,” with at least five people going to the emergency room with serious health issues due to use of the CBD drops. One lawsuit, which was publicly settled for $50,000 in January of 2022, alleged that the company failed to warn the plaintiff that the CBD drops contained THC or that the product may have been contaminated with foreign substances like THC, and that the company failed to exercise quality control standards that would have detected the THC.3 Nine other lawsuits made similar failure to warn allegations based on the same batch of CBD drops and were settled by January of 2022, although those settlements were not disclosed.4 In October of 2022, the company agreed to pay a settlement of $100,000 in a class action suit, which alleged that the company failed to disclose that the CBD product contained substantial amounts of THC.5 The class action focused on unlawful trade practices claims, including that the company falsely represented that the product had the characteristics, uses, and benefits of a CBD product that did not contain THC.6 Also in October 2022, the company settled a wrongful death lawsuit—alleging that the company failed to warn the plaintiff that the drops contained THC and had negligent quality control standards—stemming from the same CBD drops,7 where the plaintiff suffered stroke-like-symptoms, allegedly due to the tainted CBD product, and ultimately died.8

Other recent lawsuits have also focused on mislabeled cannabis products, alleging that companies failed to inform customers that products contained THC. For example, in Kentucky, a man who drove into a bus after using a CBD vape sued both the CBD manufacturer and retailer on December 14, 2022, claiming that he was not warned that the vape contained a substance that would make him intoxicated.9 According to the complaint, the store employees told the man that the vape was “all natural” but made no mention that the product contained THC.10 The man alleged that the vape actually contained Delta-8 THC and brought negligence, failure to warn, and state consumer protection law claims.11

As noted above, in addition to traditional product liability actions, companies are likely to face increased consumer fraud and false advertising actions in the absence of personal injuries. Two class actions brought in December of 2020 against a hemp tea maker alleged that the company’s website and the product’s packaging fraudulently stated that a tea contained zero THC.12 Plaintiffs claimed that they tested positive for THC after drinking the tea and that product testing similarly revealed that the tea contained some THC.13

Potency inflation marketing communications from a laboratory

Last year also saw a rise in cases focused on potency inflation, alleging that cannabis companies knowingly overstated the amount of THC in their products to charge higher prices.14 Again, while these actions focused on consumer fraud allegations rather than product liability claims, these cases underscore the importance of accurate labeling. Due to potency inflation concerns, states have started investigatinglicensedcannabis testing labs within their respective jurisdictions, resulting in product recalls and fines. Some states have also updated their regulations, requiring cannabis companies to test their products through two separate labs.

Finally, contamination and the existence of impurities and other byproducts has been a recent focus of several product liability lawsuits across the life sciences space, and this trend is something that cannabis and CBD companies should be aware of and take steps to mitigate.

For example, a Canadian cannabis producer reached a $2.31 million settlement over a class action brought in March of 2017 regarding pesticide-contaminated medical marijuana. The marijuana was recalled due to the presence of myclobutanil and bifenazate pesticides, neither of which were authorized for use on cannabis plants in Canada. The lead plaintiff experienced nausea and vomiting, allegedly from consuming the medical cannabis, and brought numerous claims on behalf of the class, including negligent design, development, testing, manufacturing, distribution, marketing, and sales.15 In the United States, California’s Department of Cannabis Control issued a mandatory recall on January 26, 2022 for a batch of cannabis flower that was contaminated with mold. On March 25, 2022, the New Mexico Cannabis Control Division recalled cannabis products sold by a local medical cannabis company because the product contained impermissibly high levels of mold. New Mexico’s Cannabis Control Division also required the company to immediately cease and desist operations at its production and manufacturing site.

A Look at the Future and What Companies Can do to Mitigate Product Liability Risks

The FDA’s 2023 announcement means that the industry will have to wait for Congressional action for the development of a regulatory scheme that can help standardize requirements and provide industry players additional defenses when facing product liability actions. Many of the proposed risk management tools in the FDA Announcement could help companies mitigate future litigation risks if implemented. These risk management tools may include “clear labels, prevention of contaminants, CBD content limits, and measures, such as minimum purchase age, to mitigate the risk of ingestion by children.” Although the FDA has had regulatory oversight over CBD and other hemp-derived products for nearly four years, the agency has not developed a regulatory framework for these products aside from issuing warning letters, leaving manufacturers and distributors without much guidance. The FDA has also left the states to fill the void, resulting in a patchwork of differing—and sometimes conflicting—state laws. Additional guidance and regulation on labeling at the federal level for cannabis and cannabis-derived products will make compliance a more straightforward proposition and may provide avenues for industry participants to explore preemption defenses in the face of future mislabeling claims.

Just some of the many CBD products on the market today

In addition to following the changing regulatory landscape and understanding how regulatory changes can impact litigation defenses, cannabis and CBD companies can continue to take various steps to help mitigate future litigation risks.

Quality Control: Adequate testing procedures and effective quality control procedures can help avoid contamination issues and situations where products are mixed up during the manufacturing process. For example, the company whose license was suspended in Oregon due to the alleged mix up between CBD and THC subsequently implemented new ingredient tracking protocols, adopted a policy to retain samples from each batch of product, and now sends additional samples to an independent lab to ensure product compliance before anything is sold.

Proper documentation of testing and quality control procedures, as well as maintaining records of compliance checks, can also help companies put together a defense to state regulatory actions or lawsuits relating to contamination or manufacturing defects. Indeed, in February of 2022, an Arizona marijuana testing lab was fined $500,000 for various incomplete records and documentation as well as improperly calibrated machines for contamination testing, with an inspector also noting that one of the employees was trained to use a technique that produced inflated potency results.

Ongoing Safety & Regulatory Review: Keeping up to date with regulations and science will play a key role in making sure labels are accurate and defendable. Working directly with regulators and seeking guidance from regulators on labeling can help potential defendants present a clear and compelling labeling defense. Moreover, the 2023 FDA Announcement made clear that the agency will not pursue rulemaking on CBD’s potential use in foods and dietary substances. Thus, industry players should monitor agency announcements and engage with the FDA’s Cannabis Product Committee (CPC) and Congress to better understand the potential structure of this new regulatory pathway.

Stay on Top of the Science: A boost in cannabis research is on the horizon, as the Medical Marijuana and Cannabidiol Research Expansion Act (MMCREA) will advance research on the potential risks and benefits of cannabis products and promote the development of FDA-approved drugs derived from marijuana and CBD. On the litigation front, causation is an essential element in most causes of action, and plaintiffs will have to prove that the cannabis caused their injury. Thus, industry players should be aware of the current science, including potential side effects.

Litigation Monitoring: Finally, companies will also be well served by following court decisions involving CBD and cannabis products. For example, courts in 2022 were split over the legality of Delta-8 THC, a substance typically manufactured from hemp-derived CBD. The Ninth Circuit held in AK Futures v. Boyd Street Distro that Delta-8 THC found in e-cigarettes and vape products is legal under the 2018 Farm Act, at least in the intellectual property context.16 But in Kansas, a federal judge ruled that the 2018 Farm Act does not make selling hemp-derived products such as Delta-8 THC legal.17 In Texas, litigation initiated in 2021 is ongoing over the legality of Delta-8 THC.18 There, a hemp company sued the Texas Department of State Health Services for its classification of Delta-8 THC as a Schedule I drug, making the sale of this substance a felony offense. A temporary injunction was granted on November 8, 2021—temporarily lifting the ban on sales of Delta-8 THC products—but the plaintiff’s request for a permanent injunction remains pending.19 As these lawsuits show, the legality of different products may vary by jurisdiction, whether by regulation or a judicial decision.

References

Medical Marijuana and Cannabidiol Research Expansion Act, Pub. L. 117–215, 136 Stat. 2257 (2022).

Agbonkhese v. Curaleaf Inc., No. 3:21-cv-01675, (D. Or. Jan. 5, 2022).

Agbonkhese v. Curaleaf Inc., No. 3:21-cv-01675, ECF 1, 6 (D. Or.).

See Crawforth v. Curaleaf, Inc., No. 3:21-cv-1432 (D. Or. Sept. 29, 2021); Lopez v. Curaleaf, Inc., No. 3:21-cv-1465 (D. Or. Oct. 6, 2021);

Williamson v. Curaleaf, Inc., No. 3:22-cv-782, ECF 1, 8 (D. Or.).

Williamson v. Curaleaf, Inc., No. 3:22-cv-782 (D. Or. May 30, 2022).

Estate of Earl Jacobe v. Curaleaf, Inc., No. 3:22-cv-00001, 19 (D. Or. Oct. 18, 2022).

Estate of Earl Jacobe v. Curaleaf, Inc., No. 3:22-cv-00001 1 (D. Or. Jan. 1, 2022).

Howard v. GCHNC3 LLC et al., No. 5:22-cv-00326 (E.D. Ky. Dec. 14, 2022).

Complaint at ¶ 11, Howard v. GCHNC3 LLC et al., No. 5:22-cv-00326 (E.D. Ky. Dec. 14, 2022).

Complaint at ¶¶ 15-33, Howard v. GCHNC3 LLC et al., No. 5:22-cv-00326 (E.D. Ky. Dec. 14, 2022).

Williams v. Total Life Changes, LLC, No. 0:20-cv-02463 (D. Minn. Dec. 3, 2020); Santiago v. Total Life Changes LLC, No. 2:20-cv-18581 (D.N.J. Dec. 9, 2020).

Complaint at ¶¶ 54-59, Williams v. Total Life Changes, LLC, No. 0:20-cv-02463 (D. Minn. Dec. 3, 2020); Complaint at ¶¶ 21-25, Santiago v. Total Life Changes LLC, No. 2:20-cv-18581 (D.N.J. Dec. 9, 2020).

See Centeno v. Dreamfields Brands Inc., No. 22STCV33980 (Cal. Superior Ct. L.A. Cnty. Oct. 20, 2022); Shanti Gallard v. Ironworks Collective Inc., No. 22STCV38021 (Cal. Superior Ct. L.A. Cnty. Dec. 6, 2022).

Downton v. Organigram Holdings Inc., Hfx No. 460984 (Sup. Ct. Nova Scotia Mar. 3, 2017).

AK Futures LLC v. Boyd St. Distro, LLC, 35 F.4th 682 (9th Cir. 2022).

Dines v. Kelly, No. 2:22-cv-02248, 2022 WL 16762903 (D. Kan. Nov. 8, 2022).

Hometown Hero v. Tex. Dep’t of State Health Services, No. D-1-GN-21-006174 (Travis Cnty., Tex. Oct. 20, 2021).

Hometown Hero v. Tex. Dep’t of State Health Services, No. D-1-GN-21-006174 (Travis Cnty., Tex. Nov. 8, 2021).

As a business owner, insurance is always a must. If you are interested in entering into the cannabis industry or you already have, it’s important to know what to expect when it comes to insuring your cannabis-related business.

That’s why we’ll be exploring what dispensary insurance is, different options for business owners and general advice regarding dispensary and other CRB insurance.

What is Dispensary Insurance?

Insurance for cannabis-related businesses refers to policies that protect the business against risk. This can include dispensaries, cultivation centers and testing labs – all of which require different levels of coverage and liability.

We spoke to Alexander Marenco, an insurance broker from Marenco Insurance, who explained what dispensary owners should know before seeking out insurance. Marenco says it’s similar to shopping for insurance for other businesess. “You need to have full details of the business and location to receive a quote.” He adds. “The applications will ask questions such as location, renovations, or improvements to the location, ownership information, payroll details, and sales or projected annual sales.”

How is Dispensary Insurance Different From Other Forms of Business Insurance?

Because non-hemp-derived cannabis is still considered a schedule one controlled substance under the Controlled Substance Act, cannabis insurance can be more expensive than regular insurance for non-cannabis businesses. Because of the risks associated with being considered a potential retailer of a controlled substance, liability policies and other options can cost a pretty penny.

The cash-only nature of the business makes insuring dispensaries more costly

Additionally, when asking Marenco about how dispensary insurance differs from other brick-and-mortar retail insurance, he says: “With more states increasingly legalizing medicinal and recreational marijuana, insurance carriers have started to open risk acceptability. However, since marijuana is still federally illegal, businesses will find it difficult to find multiple quotes from different carriers.”

Types of Insurance Available for Cannabis-Related Businesses

What kind of insurance is available for cannabis-related businesses? Let’s find out.

First off, it’s important to keep in mind that CRBs are at risk for a lot of things: workplace accidents, damage to property, theft, general liability and product liability. Plus, the fact that most dispensaries work on a cash-only business model until the Secure and Fair Enforcement (SAFE) Banking Act is approved by Congress, CRBs tend to handle big amounts of cash, further putting them at risk of theft and liability. CRB insurance can be as low as $350 and as high as $7,500 depending on the type of business and policy.

Here are some of the most common types of insurance for CRBs and what they cover:

General liability: third-party claims for bodily injury, property damage and reputational harm.

Commercial property: damage to a business-owned property.

Professional liability: third-party accusations of negligence and mistakes.

Workers’ compensation: employees’ medical bills and lost wages due to injury or illness.

Inland marine: damage or theft of business-owned property in transit.

Crop: costs from damage to seeds and plants.

With so many things to watch out for, insurance for cannabis businesses and dispensaries isn’t cheap. Here, Marenco says what CRB owners can do to keep their premiums as low as possible:

A smart safe like this one can help secure cash handling

“Premiums are primarily based on sales (actual or projected). After the term expires, the insurance carrier will conduct an audit for the prior term to confirm the information from the application. The audited discrepancy will adjust the next term’s sales figures. Dispensary insurance will typically be placed through an excess & surplus market which do not provide traditional discounts.”

So, in essence, the best thing a dispensary owner can do is be honest about their projections.

Navigating premiums can be a detailed process, as we learned when speaking to Jesse Giffith, an owner of Smokeless CBD and Vape: a chain of retail shops across the twin cities Minneapolis–Saint Paul, Minnesota:

“Our shops carry insurance that has been offered with a modified rate for vape retailers. This route was not as straightforward as some traditional retail insurance options, but may offer benefits, and a better fit for coverage than other dispensary insurance options.”

A Growing Number of Dispensaries Across America

With the growing legalization and normalization of adult use, medical and hemp-derived cannabis across the nation, it should come as no surprise that the number of dispensaries across the country grows exponentially.

In 2021, the cannabis market in the U.S. was valued at 10.8 billion dollars, with an expected annual growth of 14.9% annually. This is a sign of what’s to come. Cannabis may be an industry that’s been considered taboo for decades, but the growth shows the growing acceptance of the plant for medical and adult use reasons.

Insurance providers remain cautious as cannabis laws are still in flux.

With that growth comes a greater need for insurance providers, opening the door to the possibility that these two industries will grow in tandem. The future may bring a greater variety of options for coverage at cheaper prices. But for the time being, insurance providers remain cautious as the fate of federal and local cannabis laws are still in flux.

Are There Limited Carriers that Issue Dispensary Insurance?

Every CRB needs insurance, just like any other type of establishment, business or company. The issue within the cannabis industry is that there is still a limited insurance market, with insurers willing to provide insurance constantly exiting and entering the market. Plus, the overall capacity and variety of policies that cover different types of risks are limited. Lastly, it can be difficult to use CRB insurance when you read between the lines of the policy. Because cannabis with THC is still federally illegal (excluding hemp-derived cannabis products containing less than 0.3% THC), insurers can negate coverage when a loss or claim occurs.

Because of the complications that may arise even if you do have insurance, Marenco offers some advice for dispensary owners that are searching for the right insurance option for them: “Before shopping for insurance make sure you have all your licenses and are in full compliance with all regulations. Insurance carrier’s requirements from the state. Additionally, consider different coverage options.” He continues. “At a minimum, a business needs general liability insurance. Insurance companies can also consider covering business property including inventory, betterments, and improvements to a rented space, among others. When shopping for insurance make sure your agent reviews different coverage options.”

The success of reputable cannabis and CBD brands has inspired an influx of inexperienced and disreputable competitors in the market. These so-called “bad actors” in CBD advertise products that are not manufactured under current Good Manufacturing Practices (cGMP), which help to ensure that all products are consistently produced and controlled according to specified quality standards. cGMP helps guard against risks of adulteration, cross-contamination and mislabeling to guarantee product quality, safety and efficacy.

Joseph Dowling, Author & CEO of CV Sciences

CBD products without cGMP regulations are often inaccurately labeled and deceiving to consumers. In fact, in a test of over 100 CBD products available online and at retail locations, Johns Hopkins Medicine found significant evidence of inaccurate, misleading labeling of CBD content. The prevalence of such brands not only reduces consumer confidence in CBD but also limits the growth of the sector as a whole. Fortunately, CBD consumers and retailers can easily discriminate between a well-tested, reputable brand and inferior bad actors with a few straightforward, minimum requirements to look out for when selecting a product.

Why are “bad actors” a problem for consumers and the industry?

Bad actors in CBD sell products that are not produced under cGMP conditions and are typically not tested by third-party laboratories to ensure identity, purity, quality, strength and composition. This means they are not verified for contaminants, impurities, label claims and product specifications. This frequently results in misleading advertising with inaccurate levels of cannabinoids or traces of compounds not found on the label, like THC. To combat this, the FDA issues warning letters to actors that market products allegedly containing CBD—many of which are found not to contain the claimed levels of CBD and are not approved for the treatment of any medical condition. Still, bad actors manage to slip through the cracks and deceive consumers.

The structure of cannabidiol (CBD), one of 400 active compounds found in cannabis.

Bad actors that put anything in a bottle and make unsubstantiated medical claims hurt the reputable operators that strive to create safe and high-quality products. It is easy for consumers to be drawn to CBD products with big medical claims and lower prices, only to be disappointed when the product does not produce the advertised results. Inaccurately labeled products may contain unexpected levels of cannabinoids, including ingredients that consumers may not intend to ingest, like Delta-9 or Delta-8 THC. Along with unexpected levels of THC, many CBD products available now are not as pure as advertised, with one in four products going untested for contaminants like microbial content, pesticides, or heavy metals.

Further, inaccurate labeling of products and their compounds also prevents consumers from establishing a baseline impact of CBD on their bodies, leaving them vulnerable to inconsistent future experiences. Such a poor experience can turn consumers off to the category as a whole, drawing their trust away from not only the bad actors but also the reliable, reputable brands on the market. The saturation of the market with these disreputable brands delegitimizes a category that has only just begun to break down the stigmas, creating stagnation rather than growth as consumers remain wary of low-quality products.

How can consumers identify bad actors in CBD?

There are several simple ways to identify a bad actor among CBD products and make certain that both consumers and retailers purchase quality, reliable and safe brands in legitimate sales channels. To start, consumers should avoid all CBD products that are marketed with unsubstantiated medical claims. This is a significant area of abuse, as brands that relate any form of CBD product to a disease state, like cancer, should not be trusted. The science to support such medical claims has not been completed, yet, product marketing is years ahead of the evidence to support such claims. Unsupported medical claims could also mislead consumers that may need more serious medical intervention.

Just some of the many CBD products on the market today.

Additionally, consumers must review the packaging, which should include nutrition information in the form of a supplement fact label. The label should include the serving size, number of servings per container, a list of all dietary ingredients in the product and the amount per serving of each ingredient. All labels should include a net quantity of contents, lot number or batch ID, the name and address of the manufacturer, and an expiration or manufacturing date. These signs of a reputable brand are easy to look for and can save consumers from the trouble of selecting the wrong CBD product.

What to look for when selecting a CBD product

With this in mind, products from reputable, tested brands can be identified by a few key factors. Reputable CBD companies are already compliant with the FDA regulations on nutritional supplements, including a nutritional or supplement fact panel on the packaging—just like vitamins. The information in this panel should include all the active cannabinoids in the product, both per serving and package. Clear potency labeling allows consumers to confidently select products that suit their needs and understand the baseline impact of CBD concentration on their bodies, thus helping them to tailor their experience with thoughtful product selection.

Reputable brands also include a convenient QR code on the packaging, linking the product to a certificate of analysis that details the testing results to demonstrate compliance with product standards and label claims. In terms of specific ingredients, consumers should be skeptical of high concentration levels of “flavor of the month” minor cannabinoids, which are often associated with unsubstantiated medical claims. Current scientific research has set its focus on major cannabinoids like CBD and Delta-9 THC, leaving additional research necessary for understanding minor cannabinoids. Minor cannabinoids are typically included in full spectrum products at concentrations found naturally in the cannabis plant, which is a safer approach to consuming CBD until more research is completed.

Consumers should not let the existence of unreliable, untrustworthy brands curtail their confidence in the CBD sector—there are many high-quality, safe and trusted brands on the market. With a knowledgeable and discerning eye, consumers and retailers can easily select top-quality CBD products that millions of consumers have found to improve many aspects of their health and well-being. Looking ahead, clear federal regulations for CBD products that require mandatory product registration, compliance with product labeling, packaging and cGMP will be crucial in weeding out bad actors and will allow compliant companies to gain consumer trust and responsibly grow the CBD category.

In a growing number of communities around the U.S., new cannabis lounges are offering a social setting where guests can openly use cannabis products. Colorado and New Mexico both saw their first cannabis lounges open in April, Michigan’s first cannabis lounge is set to open this summer, and officials in Nevada are currently discussing how the recently approved class of businesses should be regulated. In West Hollywood, California, where the state’s first cannabis lounge opened in 2019, multiple new lounges are now in the works after two years of slowdown due to the pandemic.

The bar-like establishments add a new dimension of potential revenue — and risk — to an industry that is expected to add almost $100 billion to the U.S. economy this year. This new and emerging segment within cannabis isn’t happening in every legal state, but more are starting to enact regulations to provide for some type of on-site consumption.

These new ventures need insurance policies tailored to address the risks of serving cannabis products, which could be looked at similarly to liquor liability for bars and restaurants.

Whether it’s alcohol or cannabis, these products impair people’s judgment, meaning everyone reacts differently to them. But how do you know when to cut someone off?

Cannabis lounges could be held liable & run risk of being sued for overserving

If a cannabis lounge faced a lawsuit alleging that it overserved a patron, leading to a third-party bodily injury, the business’ Commercial General Liability (CGL) Insurance and Products Liability Insurance could potentially cover costs such as legal defense, medical expenses and settlement amounts. Until such a case occurs, it is not yet known how exactly these lawsuits would be covered by insurance.

Because of the short history of cannabis lounges in the U.S., something like this is largely untested, making it hard to speak to exactly how a scenario would play out. Many of the existing cannabis insurance policies are highly exclusionary, meaning it could exclude a loss that is deemed to have arisen out of the use of cannabis.

Recent liquor liability lawsuits have shown the potential for a significant loss is clear. In early April 2022, a $20 million lawsuit was filed against a nightclub in Houston, Texas, alleging it overserved customers and allowed underage drinking, contributing to a drunk driving crash that killed a teenager.

In December 2021, a jury in Texas awarded the family of two drunk driving victims over $301 billion after a lawsuit alleged the driver was overserved at a bar before the accident; though largely symbolic, the settlement marked the largest personal injury award in U.S. history.

The Barbary Coast lounge in San Francisco

With these cannabis lounge establishments more or less encouraging intoxication of patrons on their premises, it’s very similar to a liquor liability type situation. If someone overindulges at a lounge, leaves and causes a crash resulting in injury or death, that could come back to the establishment.

While it remains to be seen how cannabis overserving lawsuits could play out in American courts, it’s worth noting Canada forbids on-site consumption of cannabis products and any loss or damage will not be covered by their insurance policies – despite it being legal country-wide.

Lawsuits possible over product issues, budtender advice

Even cannabis operations that do not allow on-site consumption can face liability related to the products they sell, making Products Liability Insurance and Product Recall Insurance necessary for growers and retailers. They should also consider Employment Practices Liability (EPL) Insurance to cover staffing-related allegations such as discrimination and ask their insurance broker whether budtender liability is included in their CGL Insurance policy.

Budtenders must walk a fine line between giving advice versus general information on products.

Budtenders, or individuals who work at cannabis retailers, are not allowed to offer medical advice to consumers. They must walk a fine line between giving advice versus general information on products. Although we are not aware of lawsuits that have been filed over a budtender’s advice, it would ultimately be up to the courts and lawyers as to how those proceedings would play out.

Budtender liability is not very different from professional liability insurance, and it’s more like an incidental coverage based off the budtender’s informal advice. There are, indeed, insurance carrier partners today that offer that service.

CGL Insurance can also cover in-store slip-and-falls and other third-party injuries and property damage. Because most cannabis retail stores are fairly small, these incidents have been rare, but GCL cannot be overlooked. Businesses must be prepared for anything to happen – and need to know that no risk is too small.

Theft, vandalism among top threats to cannabis businesses

Whether or not a cannabis business includes a lounge for cannabis use, any business in this industry may be more vulnerable to certain risks, including theft and vandalism.

In the U.S., where many cannabis companies operate on a cash-only basis because of banking difficulties tied to recreational products being federally illegal, a recent surge in cannabis shop robberies has led to calls for a new banking bill. Some of these incidents have even turned deadly, including an April 30 dispensary robbery in Los Angeles, California, during which one man was reportedly shot and killed.

Many insurance carriers require retailers to install alarm systems, video monitoring equipment or safes

Large amounts of cash are on-hand daily at these premises, and workers might have to make multiple bank runs throughout the day, leaving a heightened exposure and risk for robberies.

From robberies and vandalism to fires and flooding, Commercial Property Insurance is a key protection for cannabis retailers. Equipment Breakdown Insurance may also be needed, particularly when the stores contain expensive refrigeration equipment. The potential loss is large in this industry, especially at growing facilities, and there’s a lot at stake with such high-value equipment.

Security systems, employee training can help reduce risks

Many insurance carriers require business owners to install alarm systems, video monitoring equipment or safes to help reduce potential property losses, and employees should be trained to use the alarm systems consistently. Policyholders and business owners should also know there is a lot they can do to curb some of the risks, such as businesses doing background checks on every hire and taking steps to ensure they are hiring individuals they can trust.

Installing bars on glass windows and doors is another loss prevention measure that is strongly encouraged because it adds an additional layer of security to get through – it won’t be an easy or quick process to break-in and will trigger the alarm system.

The importance of working with an insurance broker

Working with an insurance broker who is specialized in the cannabis industry can help business owners better explore available coverage options. With cannabis or any type of risk, you should always work with someone who has knowledge and expertise in that area. When you work with someone who knows the ins-and-outs of the regulations, you can have more peace of mind.

You might have a risk warranty that always requires two drivers in that vehicle, or GPS monitoring on the vehicle.

Understanding your policy in its entirety is also essential, as these policies have any number of different limitations and exclusionary forms that could preclude you from collecting if you had not understood and followed the language of the policy.

In a transportation situation, for example, you might have a risk warranty that always requires two drivers in that vehicle, or GPS monitoring on the vehicle. In the event of a claim, if the investigation determines the business did not have those items present at the time of loss, that claim will not be covered.

In a rapidly growing and changing industry, business owners should not underestimate the value of working with a team of insurance experts who keep a close pulse on the quickly evolving industry. Brokers are aware of the different legal environments in each state or even each city or county. Cities and counties can add different levels of compliance matters, so as a buyer, you can be confident that you have the most recent information and are in compliance with state law and any insurance requirements that may be present. Being able to explain the differences between the markets and the coverage options is beneficial to any business owner in this ever-changing industry.

In an unprecedented move, the U.S. Food & Drug Administration (FDA) has issued warning letters today to companies selling products containing delta-8 THC. In total, the FDA sent out five warning letters to companies for violating the Federal Food, Drug, and Cosmetic Act (FD&C Act).

Image from the FDA’s consumer update on Delta-8 THC

The violations include illegal marketing of unapproved delta-8 THC products as treatment for medical conditions, misbranding and adding delta-8 THC to food products. Back in September of last year, the FDA published a consumer update on their website, seeking to educate the public and offer a public health warning on delta-8 tetrahydrocannabinol, otherwise known as delta-8 THC.

Delta-8 THC is a cannabinoid that can be synthesized from cannabidiol (CBD) derived from hemp. It is an isomer of delta-9 THC, the more commonly known psychoactive cannabinoid found in cannabis. Delta-8 THC does produce psychoactive effects, though not quite as much as its better-known cousin, delta-9 THC. Many regulators and industry stakeholders are increasingly concerned about the rise in popularity of delta-8 products, namely because of the processing involved to produce it. Delta-8 THC is often synthesized using potentially harmful chemicals.

The FDA has a history of sending a lot of warning letters to companies marketing CBD products inaccurately and making drug claims. Earlier this year, they sent a number of letters to companies claiming that CBD can cure or prevent Covid-19.

According to Janet Woodcock, M.D., principal deputy commissioner at the FDA, they are getting more and more concerned about the popularity of delta-8 THC products sold online. “These products often include claims that they treat or alleviate the side effects related to a wide variety of diseases or medical disorders, such as cancer, multiple sclerosis, chronic pain, nausea and anxiety,” says Woodcock. “It is extremely troubling that some of the food products are packaged and labeled in ways that may appeal to children. We will continue to safeguard Americans’ health and safety by monitoring the marketplace and taking action when companies illegally sell products that pose a risk to public health.”

The FDA sent warning letters to the following companies selling delta-8 THC products:

Once again, the U.S. Food and Drug Administration (FDA) has issued a number of warning letters to companies selling hemp-derived cannabidiol (CBD) products. This time around, the FDA sent these warning letters to companies that had statements on their website claiming CBD is an effective treatment or prevention of Covid-19.

In this latest round, the FDA sent a total of seven warning letters to:

Just some of the many hemp-derived CBD products on the market today

Earlier this year, a slew of preliminary research studies went viral for shedding light on promising signs that certain cannabis compounds could help treat or prevent Covid-19. The conclusions from most of that research is: It is still too early to tell if any of these studies will show evidence of cannabis treating Covid-19, let alone if they mean cannabis products can be used as a treatment or preventative for Covid-19. However, the research is significant and we should keep an eye on any developments that come from those studies.

The hemp-derived CBD market has a history of clashes with the FDA over health claims. Since the Farm Bill legalized cannabis with less than 0.3% THC back in 2018, the hemp-derived CBD market has proliferated, with all sorts of companies seizing the opportunity. Jumping on the health and wellness trend, companies incorporated this messaging into their marketing campaigns. Over the past four years, the FDA has issued dozens and dozens of warning letters and threatened enforcement actions to companies making unsubstantiated health claims about CBD.

While CBD definitely does have medical benefits, such as being used as an anti-inflammatory or anticonvulsant, preliminary research alone is not enough to say it does. Products need to be approved by the FDA with a new drug application (NDA) in order to make those claims. Therefore when companies make unsubstantiated health claims about their CBD products, like claiming it can prevent Covid-19, they are violating the FD&C Act by marketing “unapproved new drugs” or “misbranded drugs.”

The bottom line is companies that are marketing CBD products need to ensure that their marketing materials and labeling comply with FDA requirements and avoid making unapproved drug claims.

Cannabis remains one of the fastest growing industries with no signs of slowing down. According to a recent article in Forbes Magazine, the legal cannabis market is poised to grow 20-30% per year to the tune of $50 billion by 2026.[1]With great opportunity comes numerous risks. Claims and lawsuits against cannabis businesses are increasing in frequency and magnitude. As an insurance broker who specializes in the cannabis industry and works with a wide variety of cannabis, hemp and CBD businesses in every state where cannabis laws are established, our recent analysis has unveiled the top five insurances your cannabis business needs in 2022.

General Liability

General liability is the most essential coverage your business needs to protect you from a variety of claims including personal injury, bodily harm, property damage and other situations that may arise including slander, libel, copyright infringement and more.

Since general liability is not always required to obtain a cannabis license, many businesses are tempted to forgo the expense. This is one of the biggest mistakes you can make as one single lawsuit has the potential to cripple your business. With a comprehensive, cannabis-specific general liability insurance policy in place, your insurance company, not you, will pay medical expenses and property damage claims from third parties, in addition to hefty legal fees and fines.

Property & Casualty Insurance

P&C insurance is an important part of your security and protection plan.

If you own a dispensary, grow operation, warehouse, testing facility or any other type of cannabis business with inventory, you need to protect your assets from potential loss or damage. Property & casualty (P&C) insurance safeguards your business against common and costly perils such as a fire, lightning, explosion/implosion, and even less common – but still possible – risks like riots, strikes and terrorism.

P&C insurance not only pays for damages to your business property resulting from a covered loss but it also covers the contents within your place of business, including office furniture, computers, inventory and other assets essential to your business operations. There are policies that will also provide the funds required to keep your business afloat until the damages from the loss are repaired. Any cannabis business with a physical property and location(s) should have a comprehensive property and casualty P&C policy in place.

Product Liability/Product Recall

Recently, we’ve seen a dramatic influx of product liability claims, and in particular, product recalls. Lawsuits have ranged from a single plaintiff seeking damages for personal injuries to class action lawsuits where a defective product is tied to an entire group of claimants.

Preventing contamination can save a business from extremely costly recalls. Having the right insurance can prevent a recall from becoming costly in the first place.

As a cannabis business owner, you can be sued for any damage resulting from products that cause harm to others, this includes false advertising, mislabeled or defective products. No matter where you are in the supply chain, your business could be held liable. The process of defending litigation or reaching a settlement agreement can completely drain a company’s resources. You’ll have to deal with regulatory compliance, producing and distributing product warnings, recalling products, claim investigation, product testing and additional risk assessment.

Product liability insurance is often overlooked, especially by small to mid-size businesses. However, your cannabis business needs this type of coverage if you sell any goods or products that end up in the hands of the public. In fact, your business may be contractually obligated to have product liability insurance. One such lawsuit is enough to fold a business due to costly legal fees and fines, as well reputation damage beyond repair.

Product liability insurance is designed to protect your cannabis company from claims that can happen anywhere along the supply chain, including product contamination, mislabeled products, false advertising or defective products. With proper coverage, your insurance company will pay for damages and legal expenses if you are sued, up to your policy limits. Your product liability policy will also cover any medical expenses for those who are harmed by your business. Making sure your insurance policy includes product liability insurance should be a top priority in 2022.

Cyber Defense/Data Breach Insurance

Cyber fraud and data breaches are two of the greatest risks facing cannabis companies in 2022. With so much cash pouring into the space, cannabis businesses of all sizes are bulls-eye targets for cybercriminals. Even the smallest of cannabis businesses are at risk of data breaches because they are part of a larger interconnected network of seed to sale vendors. These types of crimes can have detrimental effects on your business in numerous ways. In the case of a data breach resulting in the disclosure of a third party’s private information, the third party could sue your business. The SEC could also find your company negligent in cyber fraud cases and impose significant fines.

By forgoing cyber defense & data breach insurance, your business will be solely responsible for expensive legal bills, significant revenue losses and hefty fines and penalties from regulators. Cyber defense & data breach insurance is a must-have coverage in 2022, and beyond, to protect your business from cybercrimes.

Directors & Officers Insurance

If you are looking to secure venture capital or funding from investors in 2022, and/or attract and retain qualified leadership, you need directors & officers (D&O) Insurance. D&O protects corporate directors and officers, as well as their spouses and estates, from being personally liable in the event your company is sued by investors, employees, vendors, competitors, customers, or other parties, for actual or alleged wrongful acts in managing the company. In the event of litigation, your D&O insurance will cover legal fees, fines, settlements and other expensive costs.

D&O is often the most overlooked coverage because many cannabis businesses are independently run, and no one foresees the potential for operational failures and mismanagement. However, businesses with any sort of vision for growth should make D&O a top priority. It not only protects your current executives and board members but is critical in attracting leading talent in the space, as well as drawing in new investors to scale up your business. In fact, we’re seeing more prospective investors and board members requiring D&O insurance prior to engaging with a company to ensure they are fully protected in the event of litigation.

When it comes to mitigating risk in this business, the stakes are sky high. Cannabis companies that have not incorporated risk management into their business/operational plans will need to in 2022. It all boils down to the THREE P’s: being “Proactive, Prepared and Protected.”

Cannabis risks have always outpaced the availability of insurance, in large part because of its status as a federally illegal substance and the dangers in extraction and production. But it now shares many of the same risks as other industries — catastrophic crop damage, cyber risk and a shortage of skilled workers.

With legalization becoming more common, the industry is positioned for enormous growth despite these challenges. However, enterprises that will benefit the most are those best positioned to manage risk.

Here are four obstacles to growth in the industry in 2022 and how enterprises can combat them:

Cybercrime will be the top manufacturing risk

Both cybercrime and cannabis have experienced major booms since the start of the COVID-19 pandemic. Cannabis companies watched as healthcare and pharmaceutical organizations were hit hard by cybercriminals in 2020, and now the threat could be headed their way.

For retailers, the vulnerability often lies in their POS tech

For cannabis retailers, the vulnerability lies in their dependence on point-of-sale tech, while the threat for cultivators exists within their strong use of intelligent automation to manage the grow environment. Across the industry, the lack of sophisticated IT security systems is like a beacon for bad actors.

Nearly 60% of cannabis businesses say they haven’t taken the necessary steps to prevent cyberattack, but the winds are changing. Due to these concerns and the growing attention on cybercrime in the industry, cyber coverage is expected to rise 30% or more in 2022, which puts the onus on risk management practices that will help prevent cyberattacks and ensure coverage from insurers concerned about risk.

Barriers to business growth may result in more M&A

As of summer 2021, 18 U.S. states have legalized adult use and 37 states have legalized medical cannabis.

While this is opening opportunities for many cannabis businesses, the U.S. remains a complicated market. Federal regulations continue to hinder even more cannabis industry growth by restricting lending to the industry from traditional banking and financial institutions. While it’s not illegal to do service with the cannabis industry, many institutions stay away due to its high risk.

Smaller cannabis companies are impacted most heavily by this barrier and await passage of the Secure and Fair Enforcement (SAFE) Banking and Clarifying Law Around Insurance of Marijuana (CLAIM) Acts to allow easier access to capital. Together, these two acts of legislation will provide guidelines on how to work lawfully with legal cannabis businesses and prohibit penalizing or discouraging institutions from working with them.

In the meantime, M&A activity is expected to increase in 2022 as large cannabis businesses have the means to access capital and acquire these small companies. This includes Canadian cannabis companies, unburdened by federal restrictions, who are expected to increase their cross-border mergers and acquisitions.

Severe weather isn’t easing up

Extreme natural catastrophes are no longer rare, and they have only added greater uncertainty to the industry which has always had difficulties securing crop insurance.

NASA’s Aqua satellite took this picture of the smoke over California in 2017 Photo: NASA

For example, policies that transfer wind and hurricane damage risk in Florida or wildfire and smoke taint in California are virtually non-existent for cannabis — and for outdoor growers, a single weather event can wipe out an entire crop with no recourse.

One possible solution for cannabis companies that cannot secure traditional crop insurance is parametric insurance, which pays out in full when a weather element reaches a threshold, regardless of the actual damage.

Growers with indoor operations, or those considering moving that way, must cope with energy conservation initiatives. Measures like the one in California that would require indoor growers to use LED lighting by 2023 could cost the industry millions and present a direct threat to small operations’ viability. This makes it important for cannabis producers to institute conservation measures and undertake risk mitigation measures like improved safety measures at indoor growth facilities ahead of 2022 renewals.

As a continually emerging market, cannabis risks are great. Adding to these pressures is the growing impacts of climate change and cybercrime raising the bar even further. Growth for the cannabis industry in 2022 will depend upon strong risk management solutions and the ability for cannabis companies to implement them.

As more states legalize the use of cannabis for both medicinal and adult use, the market is growing exponentially. For growers and dispensaries, that means bringing their ‘A’ game when it comes to marketing their cannabis products – and that includes labels.

Not only do your cannabis labels need to be compliant with regulations, but you also need to make sure they stand out from the competitors. However, while creating a label seems like it should be easy, it can be a challenge to navigate the complex and murky legal landscape.

But don’t worry, we’ve got your back! Let’s take a look at the key federal regulations you need to be aware of, what NOT to put on cannabis labels and expert advice to help you find the perfect label material for your brand. Let’s get started.

Cannabis Labeling Requirements: What You Need to Know

As of now, cannabis has not been ruled legal in all 50 states. However, states where cannabis is legalized determine their own set of rules and guidelines. These legislative guidelines are constantly being updated and revised for the labeling and packaging of cannabis products, so staying compliant can be challenging for dispensaries and manufacturers.

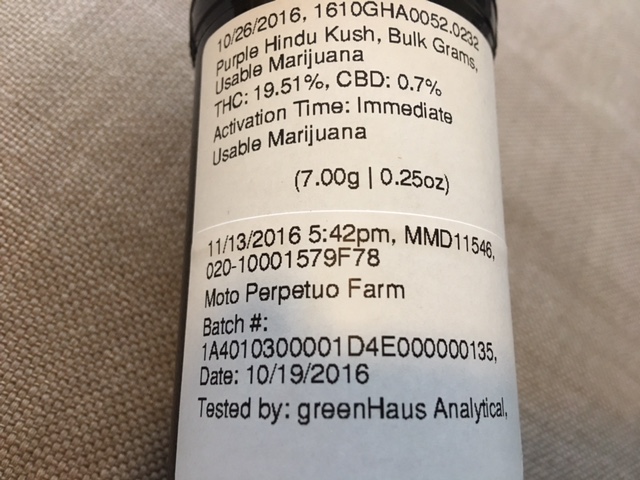

It’s important to follow general federal regulations for your product, such as the nutrition facts section (Image: TEKLYNX)

Since packaging laws vary by state, it’s important to follow general federal regulations for your product, as well as check your state for cannabis-specific label requirements.

At the very least, you should understand and follow cannabis labeling regulations in accordance with the Federal Food, Drug, and Cosmetics Act (FDCA). Let’s dive right into the basic elements that FDCA requires when labeling cannabis products.

Name and Location of Business: It is critical to always include the name and location of your business on both the inner and outer information panel. In doing so, customers always have a way to contact you for any questions. If you are worried about taking up too much space, a QR code is a great way to offer additional information.

Product Identity: Is your product meant to be used for adult or medicinal use? You must include what your cannabis product is or does on the Product Display Panel (PDP) so it’s easy for customers to locate.

Net Quantity of Contents: Net quantity refers to the total weight or volume of a finished product (excluding packaging) and is federally mandated on labels. For packaged liquid cannabis products, net quantity should be labeled in fluid measure. Meanwhile, packaged solid, semi-solid and viscous cannabis products should be labeled in dry weight.

Warning Statements: Since cannabis is still listed as a Schedule 1 Controlled Substance, it’s recommended to include warning statements for the specific product types. For example, the warning statement should stay “for medical use only” for all medical cannabis products.

List of Ingredients: You must include a complete declaration of all ingredients in your cannabis product. This must be listed on the informational panel on the outer packaging. If there is no outer packaging, then it must be placed on the product package itself.

Disclosure of Critical Facts: In general, this includes critical information that customers would want to know when buying your product. This can include:

Suggested use for the product

Application instructions

Expiration date

What NOT To Put On a Cannabis Label

Proper cannabis labeling can ensure you remain compliant with regulations and legal requirements. Without compliance, you won’t be able to sell your products and could lead to a hefty fine – and nobody wants that! Here are the things you should stay away from adding to your label:

Unapproved Health Claims: As of now, both federal law and state laws do not recognize cannabis as a dietary supplement or substance that can help prevent, cure or treat serious diseases. For that reason, your safest bet is to stay away from making any false health claims on labels and websites.

An example of a cannabis flower label in Oregon with all of the required information.

Obscured Fonts: Text and font issues can muddle the look of your cannabis label and land you into compliance issues. Most states require cannabis labels to have a font and text size that is prominent, clear and easy to read for information panels. Therefore, it is critical to find typography that showcases your brand while maintaining compliance with federal and state regulations.

Faulty Ingredient List: Cannabis labels must accurately include the types of compounds present, it’s percentage and dosage found in the product. Plus, it is required that all cannabis products include cannabinoid profiles and provide a list of any active ingredients.

Considerations for Labeling Materials

To cut through the noise in a highly competitive retail environment, it’s critical to carefully consider the label materials for your cannabis product. Here are some things to consider.

Label Material Choice: Polypropylene or Paper

Take into account what your cannabis product is (tincture, gummies, etc.) when choosing your label material. For example, if it’s a liquid cannabis product, your label can come into contact with the liquid itself, causing damage and risk the label falling off over time. For that reason, the polypropylene label would be the better choice because it’s waterproof, oil-resistant and offers more durability. On the other hand, if your cannabis product does not require a lot of protection and you are looking for a more affordable option, then paper labels would be the better option.

Coating Choice: Matte or Glossy

Choosing between matte or glossy finish depends on your preferred brand aesthetic. If you are looking to dazzle some customers and have a vibrant design on your cannabis label, then it’s best to choose a glossy finish because it holds the ink better. As a result, your label design will appear striking and crisp when printed! But, maybe that’s not the vibe of your cannabis brand so you’re looking for something more traditional. If so, a matte finish is a better choice because it absorbs some of the ink – producing that vintage, distressed look!

Final Thoughts

Your cannabis products deserve to stand out and shine in this booming market. But your product won’t even make it to the market if you are not following label requirements. Proper cannabis labeling ensures that the product is compliant, builds trust with your customers and boosts your credibility within the space. Since requirements are constantly evolving in this new industry, you must always triple-check with both federal and state regulations for the most up-to-date information in regards to cannabis product labeling. In doing so, you’ll be able to design an enticing package with proper labels that will earn heart eyes from consumers, while providing essential information about your product.

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

We use tracking pixels that set your arrival time at our website, this is used as part of our anti-spam and security measures. Disabling this tracking pixel would disable some of our security measures, and is therefore considered necessary for the safe operation of the website. This tracking pixel is cleared from your system when you delete files in your history.

We also use cookies to store your preferences regarding the setting of 3rd Party Cookies.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.

Back in May of last year, the FDA sent out their first warning letters to companies selling Delta-8 THC products, then issued a consumer update and warning about the compound a month later. The FDA and some industry stakeholders are concerned not only about the psychoactive substance itself, but also the way it is produced that could use potentially harmful chemicals.

Back in May of last year, the FDA sent out their first warning letters to companies selling Delta-8 THC products, then issued a consumer update and warning about the compound a month later. The FDA and some industry stakeholders are concerned not only about the psychoactive substance itself, but also the way it is produced that could use potentially harmful chemicals.