Have you ever been to the DMV, only to be turned away because you didn’t have the countless forms of identification needed? Sometimes it feels like no amount of ID or proof of residence is enough, whether it’s your 2nd grade report card or an electric bill from 25 years ago.

That feeling is what it’s like for anyone working in compliance; regardless of industry. Banks are no different. They need to possess compliance documents such as Consolidated Reports of Condition and Income and other Federal Financial Institutions Examination Council (FFIEC) reports that work like the laundry list of documents you need to get a driver’s license or get your car registered.

The same can be said for newly licensed and legal cannabis companies. They often need state and local inspection documents, federal background checks and a list of other documents that make a CVS receipt look minuscule in comparison.

Historically, across all industries, the whole process of gathering and providing these sorts of documents can turn into a bit of a charade. Many companies do the bare minimum to check the compliance box and achieve certifications. Various teams and stakeholders try to skate through the compliance process by providing answers that reflect what they think the enterprise customer wants to see (vs. the reality).

In order to achieve long term growth, financial institutions (FIs) and cannabis companies alike need to start executing compliance plans. FIs are always seeking new growth and revenue opportunities, and cannabis companies are constantly under the scrutiny of regulators. Identifying new solutions that can help companies grow quickly while also maintaining compliance should be an essential part of the roadmap.

Financial Institutions and Cannabis

Many think that financial institutions and cannabis businesses would be on opposite ends of any spectrum. Banking is a mature and established industry, while legal cannabis is a new, fast moving and constantly evolving space. So, on one side, there is a risk averse fiscally conservative and traditional business model, and on the other side is an industry that is outside of the mainstream.

Let’s look at this perception from a different angle though. What is true is that both industries are highly regulated and must comply with the rules placed upon them by regulators; and if their house isn’t in order, the consequences can be disastrous (Read: Massive fines or even losing the ability to operate). CRBs and FIs deal with the security and dual control of inventory, and making sure customers are properly identified and of legal capacity to conduct business. In most cases, both are small businesses within their respective communities.

Moreover, each of the industries are forced to navigate nearly-constant regulatory change, making the act of complying with applicable regulations a moving target. For most of these types of businesses, regulatory compliance is cited as one of the largest (and most expensive) challenges they face in day-to-day operations.

Compliance as Revenue Protection

When financial institutions make the decision to offer services to the cannabis industry, they naturally look at the market opportunity to determine whether the effort associated with the increased compliance obligations outweigh the potential benefits. Traditionally, compliance is viewed as a cost center, but in reality, it’s a revenue protection center. As the old saying goes; “an ounce of prevention is worth more than a pound of cure.” Compliance is that prevention.

Cannabis companies need to demonstrate reliability and a history of compliance in order to attract investors and accumulate capital

Failing to fully comply and meet regulatory compliance standards can cost organizations billions. Having a trusted system of compliance established should not be looked at as a cost-sucking measure for businesses, when it really is negligible when the cost of getting it wrong is far more substantial. Setting up a truthful and transparent compliance program isn’t just the right thing to do, it also protects revenue.

As the cannabis industry continues to grow, navigating around pain points is becoming increasingly expensive for the companies participating in it, many of whom are still struggling to turn a profit. Specifically, an IDC forecast shows global revenue from GRC solutions growing from $11.3 billion in 2020 to nearly $16.2 billion by 2025. And the average business hires and spends upward of $50,000 to $200,000 on consultants to manage compliance. It’s not uncommon for companies to dedicate five to 10 people working on compliance every week for hours and months on end.

Many in the banking industry are worried about forging into a stigmatized stream of revenue like cannabis, but with the right compliance solutions in place, they can have peace of mind. These solutions guarantee that revenue from cannabis is done legally by analyzing where each dollar came from, and denying those that don’t meet the minimum criteria. Having visibility into cannabis-related business (CRBs) accounts that do the enhanced due diligence is the only way to operate.

By implementing purpose-built compliance management solutions, financial institutions are able to unlock new revenue streams and scale cannabis banking operations. Meaning that as cannabis continues to gain mainstream momentum, and becomes less scrutinized locally and federally, these FIs that take part will be ahead of the curve.

Looking Ahead

With recent movement towards legalization in the House, cannabis investors are optimistic about the industry’s future. So how can the cannabis market overcome these hurdles and remain highly profitable?

To start with, CRBs must have greater access to accredited financial institutions like banks and credit unions. Owning bank accounts, obtaining credit cards, and applying for small business loans is essential to growth. Providing CRBs with access to proper financial support and compliance control is crucial for the cannabis market to continue to thrive.

Federal legislation such as the SAFE Banking Act is currently thought of to be the silver bullet that will open the floodgates for CRBs and FIs to work together. But in reality, this is a myth, as the SAFE Banking Act will simply make the current compliance rules stricter.

To be a first mover FI in your area, businesses must start by implementing a scalable, verifiable cannabis banking program. The real customers and financial opportunities are out there, and are even greater than what you might have modeled given the growth of the industry. The ability to do this today is real.

Cannabis is still federally illegal and is included on Schedule 1 of the Controlled Substances Act (CSA), along with such other substances as heroin, fentanyl and methamphetamines.1 It is a federal crime to grow, possess or sell cannabis.

Despite being federally illegal, 36 U.S. states and the District of Columbia have legalized the sale and use of cannabis for medical and/or adult use purposes,2 and both direct and indirect cannabis-related businesses (CRBs) are growing at a rapid rate. Revenue from medical and adult use cannabis sales in the US in 2019 is estimated to have reached $10.6B-$13B and is on track to reach nearly $37B in 2024.3

Because the sale of cannabis is federally illegal, financial institutions face a dilemma when deciding to provide services to CRBs. Should they take a significant legal risk or stay out of the market and miss out on a significant revenue opportunity? So far, the vast majority of financial institutions have been unwilling to take the risk, resulting in a dearth of options for CRB’s. Until recently, cannabis business operators had few options for financial services, but times are changing.

This piece will discuss current trends in banking for cannabis-related businesses. We will cover differences in legality at state and federal levels, complexities in dealing in cash versus digital currencies, Congressional actions impacting banking and CRBs and how banking is changing. The explosion of state legalization of cannabis over the past several years has had a strong ripple effect across the US economy, touching many industries both directly and indirectly. Understanding the implications of doing business with a CRB is both challenging and necessary.

Feds Versus States

Money laundering is the process used to conceal the existence, illegal source or illegal application of funds.4 In 1986 Congress enacted the Money Laundering Control Act (MLCA), which makes it a federal crime to engage in certain financial and monetary transactions with the proceeds of “specified unlawful activity.”5 Therefore, CRB transactions are technically illegal transactions under the MLCA.

Financial institutions therefore face a risk of violating the MLCA if they choose to do business with CRBs, even in states where cannabis operations are permitted. In addition, financial institutions could also face criminal liability under the Bank Secrecy Act (BSA) for failing to identify or report financial transactions that involve the proceeds of cannabis businesses operating legally under state law.6

Federal authorities continued to aggressively enforce federal cannabis laws

In short, because cannabis is illegal at the federal level, processing funds derived from CRBs could be considered aiding and abetting criminal activity or money laundering. States, however, began legalizing cannabis in 1996, and by 2009, thirteen states had laws allowing cannabis possession and use.7 Despite this legislation, federal authorities continued to aggressively enforce federal cannabis laws.8 That changed under the Obama administration when, shortly after being elected, President Obama stated that his administration would not target legal CRB’s who were abiding by state laws.[9] In an attempt to provide clarity in this murky environment, beginning in 2009, the Department of Justice (DOJ) issued three memos designed to guide federal prosecutors in this area. However, none of the DOJ memos issued from 2009 through 2013 addressed potential financial crime related to the legal sale or distribution of cannabis in states allowing the use of medicinal or recreational cannabis.

To assist financial institutions in navigating potential financial crime implications of banking CRBs, the Financial Crimes Enforcement Network (FinCen) issued guidance in 2014 that clarified how financial institutions could conduct business with CRBs and maintain compliance with their Bank Secrecy Act requirements (2014 Guidance).9 According to the 2014 Guidance, financial institutions may choose to interact with CRBs based on factors specific to each institution, including the institution’s business objectives, the evaluated risks associated with offering such services, and its ability to manage those risks effectively.

The 2014 Guidance requires those who choose to provide services to CRBs to design and implement a thorough customer due diligence review that includes, in part, analyzing the licensing of the entity, developing an understanding of the business operations of the entity, and ongoing monitoring of the entity.9 In addition, financial institutions are required to file a Suspicious Activity Report (SAR) for every transaction they process for a CRB, should they choose to accept the business.

Although the 2014 Guidance does outline a path for financial institutions to engage with CRBs, it does not change federal law and, therefore, does not eliminate the legal risk to financial institutions.10 By its very nature, the 2014 Guidance was a temporary fix, subject to changing views of different administrations, evidenced by the fact that all three of the DOJ guidance documents noted above were rescinded by then Attorney General Jeff Sessions on January 4, 2018.12 The DOJ enforcement posture could change once again in a Biden administration. Biden is on record as favoring decriminalization, and Attorney General candidate Merrick Garland has stated that if confirmed he will deprioritize enforcement of low-level cannabis crimes. Garland also believes using limited government resources to pursue prosecution of cannabis crimes states where cannabis is legal does not make sense.12

Because of the uncertainty and high risk, most banks remain unwilling to serve CRBs. Those that do serve CRBs charge exorbitant fees (fees of $750-$1,000 or more per account per month are not uncommon), pricing many smaller operators out of the financial services market.

Cash is King – Or Is It?

Cannabis operators have discovered the old adage “cash is king” is not necessarily true when it comes to the cannabis space. Bank-less CRBs are forced to utilize cash to pay business expenses, which can be particularly difficult. Utility companies, payroll companies, and taxing authorities are just some of the providers that are difficult, if not impossible, to pay in cash. For example, cannabis operators have been turned away from IRS offices when attempting to pay large federal tax obligations in cash. Likewise, cannabis operators have been unable to utilize payroll processing companies to administer payroll and benefits for their businesses because the processors won’t take cash. CRBs can’t use Amazon or other online retailers because online providers cannot accept cash.

Because dealing in cash is so difficult, CRB operators look for workarounds such as using personal credit/debit cards to purchase business equipment and supplies. This doesn’t eliminate the cash problem, however, because the credit card holder will likely have to accept cash as reimbursement. Such transactions could be considered an attempt to hide the source of the cash, which is, by definition, money laundering.

CRBs often have large sums of money onsite

Some bank-less CRBs try to skirt the system by obtaining bank accounts in the name of management companies or other entities one step removed from the actual business. While operators often choose this route in an effort to streamline business and operate out of the shadows, it again runs afoul of banking laws. Transferring cannabis related financial transactions to another entity is actually the very definition of money laundering – which, as noted above, is defined as the process used to conceal the existence or source of “illegal” funds.

In addition to the difficulties in making payments or purchasing business supplies, operating in a cash-heavy environment poses significant safety risks for cannabis operators. CRBs often have large sums of money onsite and transport large sums of cash when purchasing product or paying bills, making them a target for robbery. In 2017, there was a spate of dispensary robberies across the Phoenix Metro area, including one at Bloom Dispensary that took place during operating hours.13

Managing all that cash increases the cost of doing business as well, in the form of increased labor, insurance, and security costs. Cash must be counted and double counted, which can be time consuming for staff, not to mention the time it takes to deliver physical cash payments to hither and yon. Ironically, lack of banking significantly decreases transparency and clouds the waters of compliance, as operating strictly in cash makes it easier to manipulate reported financial results.

Potential Congressional Solutions

In recent years Congress has undertaken several efforts to pass legislation designed to address the state/federal divide on cannabis, which would likely clear the way for financial institutions to provide services to CRBs, including:

R. 1595 – Secure and Fair Enforcement Banking Act of 2019 (“SAFE Act”);

1028 & H.R. 2093 – Strengthening the Tenth Amendment Through Entrusting States Act (STATES Act); and

2227 – Marijuana Opportunity Reinvestment and Expungement Act of 2019 (MORE Act).

The climate in Washington DC, however, did not allow any of these initiatives to pass both houses of congress. Had any been sent to the White House, President Trump was unlikely to sign them into law.

The cannabis industry has new reason to believe reform is on the horizon with shift in political leadership in the White House and Senate. Newly anointed Senate Majority Leader Chuck Schumer recently committed to making federal cannabis reform a priority, and President Biden appears committed to decriminalization, reviving the hope of passage of one of these pieces of legislation.

The Changing Banking Landscape

Even though there is little in the way of formal protections for financial institutions, and with the timeline for a legislative fix unknown, an increasing number of banks are working with cannabis operators.

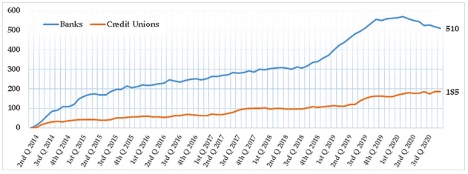

According to FinCen statistics, there were approximately 695 financial institutions actively involved with CRBs as of June 30, 2020. It is important to note that these statistics are based on SAR filings, which banks are required to file when an account or transaction is suspected of being affiliated with a cannabis business. However, some of these SARs may have been generated on genuine suspicious activity rather than on a transaction with a known cannabis customer.

Number of Depository Institutions Actively Banking Cannabis-Related Businesses in the United States (Reported in SARS)14

There are arguably more banking institutions offering services to CRBs than ever before. The challenges for CRBs are (1) finding an institution that is willing to offer services; (2) building/maintaining a compliance regime that will be acceptable to that institution; and (3) cost, given the high fees associated with these types of accounts.

How CRBs Get Accepted by Banks

The gap between CRBs’ need for banking and the financial services providers’ sparse and expensive offerings to the sector has created an opportunity for third-party firms to intervene and provide a compliance structure that will satisfy the needs of the financial institutions, making it easier for the CRB to find a bank.

These third-party firms perform extensive BSA-compliant due diligence on applicants to ensure potential customers are following FinCen guidance required to receive banking services. After the completion of due diligence, they connect the CRBs with financial institutions that are willing to do business with CRBs and provide checking/savings accounts, check writing capability, and merchant processor accounts. These firms often provide additional services such as armored car and cash vaulting services. Some of these firms also offer vendor screening, pre-approving vendors before any payments can be made.

One such firm, Safe Harbor Private Banking, started as a project implemented by the CEO of Partners Credit Union in Denver, Colorado, who set out to design a cannabis banking program that would allow Partners to do business with Colorado CRBs.15 The program was successful and has since expanded into other states who have legalized cannabis. Other operators include Dama Financial and NaturePay.

While these services offer hope for many CRBs, the downside is cost. These services perform the operations necessary to find, open, and maintain a compliant bank account; however, the costs of compliance are still high, pricing some small operators out of the market.

Is Digital Currency an Answer?

Digital currency is also making its way into the cannabis world. Digital currency, or cryptocurrency, is a medium of exchange that utilizes a decentralized ledger to record transactions, otherwise known as a blockchain. One of the largest benefits of blockchain is that it is a secure, incorruptible digital ledger used for, among other things, financial transactions.16 Blockchain technology offers CRBs a transparent and immutable audit trail for business and financial transactions. Several cannabis-specific cryptocurrencies have sprung up in the past several years, including PotCoin, CannabisCoin, and DopeCoin, to name a few.

In July 2019, Arizona approved cryptocurrency startup ALTA to offer services to the state’s medical cannabis operators.17 ALTA describes itself as a “digital payment club where cash-intensive businesses pay each other using digital tokens instead of cash.”18 ALTA members purchase digital tokens that are used to pay other members using a proprietary blockchain based system. The tokens are redeemable for US dollars at a stable rate of 1:1, and CRBs do not need a bank account to participate in the ALTA program.

ALTA proposes to pick up members’ cash and exchanges it for tokens, which are then used to pay other members for goods and services. Tokens may be redeemed for cash at any time.18 The company has been approved by the Arizona State Attorney General, and one of the first members they hope to enlist is the Arizona Department of Revenue (ADOR). Enlisting ADOR into the program would allow dispensary members to pay state taxes digitally rather than hauling large amounts of cash to ADOR offices.

Similarly, Nevada recently contracted with Multichain Ventures to supply a digital currency solution to the Nevada cannabis industry. Nevada Assembly Bill 466 requires the state create a pilot program to design a “closed loop” system like Venmo in an effort to reduce cash transactions in the cannabis sector. Like ALTA, Nevada’s proposed system will convert cash to tokens which can then be transacted between system participants.19

While both proposals are promising for Arizona and Nevada CRBs, the timeline as to when, or if, these offerings will come online is unknown. Action on cannabis reform at the federal level may render these options moot.

Looking to the Future

Although states are legalizing cannabis in one form or another in growing numbers, the fact that cannabis is still federally illegal poses a significant barrier to accessing the financial services market for CRBs. While most banks are still reluctant to offer services to this rapidly growing industry, there are more banks than ever before willing to participate in the cannabis industry. Recent changes in leadership in Washington DC offer a positive outlook for cannabis reform at the federal level.

As the “green rush” continues to envelop the country, financial services options available to CRBs are slowly growing. Many new options are now available to help CRBs find a bank, develop compliance programs, and manage the cash related problems encountered by most CRBs. However, these solutions may be out of reach for the budget-conscious small operator. Also, there are a number of cryptocurrency solutions designed specifically for CRBs; however, when, or if, these solutions will gain significant traction is still unknown.

References

Controlled Substances Act, 21 U.S.C., Subchapter I, Part B, §812.

“State Marijuana Laws”; National Conference of State Legislatures, February 19, 2021.

“Exclusive: US Retail Marijuana Sales On Pace to Rise 40% in 2020, near $37B by 2024”. Marijuana Business Daily, June 30, 2020.

Kaufman, Irving. “The Cash Connection: Organized Crime, Financial Institutions, and Money Laundering”. Interim Report to the President, October 1984.

S. Code § 1956 – Laundering of Monetary Instruments.

Rowe, Robert. “Compliance and the Cannabis Conundrum.” ABA Banking Journal, September 11, 2016.

“History of Marijuana as a Medicine – 2900 BC to Present”. ProCon.org, December 4, 2020.

Truble, Sarah and Kasai, Nathan. “The Past – and Future – of Federal Marijuana Enforcement”. org, May 12, 2017.

Sessions, Jefferson B. “Memorandum for All United States Attorneys”. January 4, 2018.

“Attorney General Nominee Garland Signals Friendlier Marijuana Stance”. Marijuana Business Daily, February 22, 2021.

Stern, Ray. “Robbers Hitting Phoenix Medical Marijuana Dispensaries: Is Bank Reform Needed?” The Phoenix New Times, April 11, 2017.

FinCen Marijuana Banking Update, June 30, 2020.

Mandelbaum, Robb. “Where Pot Entrepreneurs Go When the Banks Just Say No.” The New York Times, January 4, 2018.

Rosic, Ameer. “What is Blockchain Technology? A Step-by-Step Guide for Beginners.” com, 2016.

Emem, Mark. “Marijuana Stablecoin Asked to Play in Arizona Fintech Sandbox.” CCN.com, October 25, 2019.

http:\\Whatisalta.com\

Wagner, Michael, CFA. “Multichain Ventures Secures Public Sector Contract with Nevada to Supply Tokenized Financial Ecosystem for the Legal Cannabis Industry”, January 26, 2021.

All major industries took a hit during the COVID-19 pandemic, but in many states, cannabis dispensaries were labeled as essential, which has allowed the industry to continue with some alterations. The impact now will come from what innovations and improvements the industry can leverage going forward.

From changes to protocols and buyer behaviors to supply chain disruptions, there were many new hurdles for the industry in addition to the ones cannabis businesses already faced, such as funding. But the silver lining could be that businesses within the cannabis industry become less of a specialty and more ‘every day’ than ever before.

The effects of the pandemic on the cannabis industry

Overall, the industry has fared well, in part thanks to its distinction as an essential service in states where cannabis is legal. It’s possible states made this decision for the same reason that alcohol businesses were deemed essential in most places: hospitals are not equipped during pandemic times to take care of people who are being forced to detox or those suffering from anxiety because they don’t have access to their legal drug of choice.

In a multitude of ways, cannabis businesses have adapted to bring calm in a storm while at the same time making manufacturing adjustments to meet the CDC guidelines. For example, there is more attention placed on individually pre-packaged products for single use; something that is less sharable as an experience but eminently practical.

Another area that has shifted a little is in the limiting of the exchange and interaction between business owners and staff relative to the customers. It’s all in the aim of mitigating the risk of exposure, but it has changed the dynamic in many cannabis businesses. This is the new normal for the time being and the industry has adapted well.

Ultimately, retail cannabis businesses today are no different than the retail of candy, cigarettes or alcohol. Certainly, segments of the industry have still struggled. Lack of tourism and the curbside/take out circumstances at dispensaries took their toll. But without the opportunity to still conduct business in some capacity, 50-60% of all operators would have gone out of business. Plus, as many people use cannabis to offset medical symptoms, including pain management, there is a legitimate need for cannabis to be available. The pandemic has provided the opportunity for many who might not have tried it before to give it a chance to help them medicinally.

Behaviors have changed, including those of buyers

Driven by consumer interests, many dispensaries have adapted to provide curbside pickup options, delivery of online orders and more. That has meant that the customer also needs to be more knowledgeable about cannabis: the experienced consumer knows what they like and want and can make their choices at a distance. Someone who is new to cannabis use might find navigating the choices and options a little more difficult, without the help of experienced staff. The breadth of material online and the ability of some dispensaries to share content that helps the consumer to make choices, in the absence of walking around the dispensary, have been additional tools at the disposal of businesses.

That said, the cannabis industry today is not a vastly different one: it is adapting to the new rules and new reality. Whether this way of doing business—at a distance—is a temporary or permanent solution will be dependent upon what federal and state regulators dictate in the months ahead, but there is likely to be ongoing demand for being able to order online and keep social distance protocols in place.

An interesting example is the Ontario Cannabis Store (OCS) in Ontario, Canada. This is a government run shop that has retail as well as a robust online presence, with free delivery during the pandemic. This has facilitated an increase in new customers, which had already jumped, post legalization. People who might have felt uncomfortable going into a dispensary can still learn about cannabis online and order it, from the relative comfort and safety of their sofa.

Supply chain disruptions and the cannabis industry

The industry has long been focused on overseas suppliers. With the arrival of the pandemic and restrictions on obtaining products from other countries, supply chains have been disrupted for many cannabis businesses. That has forced many to shift their supply chains to more local manufacturers, in North and South America.

In the long run, this should have a positive impact for the industry, so that despite the short-term disruption to the supply chain, which is having an impact on the industry as a whole, there could be an upside for local producers, growers and manufacturers. It will take time to know how this will all play out.

Funding and other issues for the cannabis industry

For a new cannabis startup in these times, the key will be what it has always been for any business, just to a greater degree: due diligence. Companies that want to open a cannabis business, whether during the pandemic or not, need to evaluate the opportunity as one would any investment. It’s all about the numbers: data for the industry as a whole and specifically from competition. These days, that data is widely available and more and more consultants and investors have expertise in this industry. “Overall, there is more interest in the industry than ever before”

It’s vital to be extremely well versed, particularly for businesses that are relatively new in the industry, because the single biggest issue for many has and will continue to be funding and investment. The cannabis industry is no different than any other business, except for the fact that it is a specialty business. With that comes the need to look for funding among investors who have some knowledge or appreciation for the industry.

Some of the key concerns traditional investors will have include:

Regulatory differences from state to state: since cannabis is still illegal at the federal level, there can be an array of hurdles at state and local level that make cannabis businesses trickier to work with.

There are religious based/morality issues for some lenders in dealing with the industry. These aren’t dissimilar from issues with other industries such as adult entertainment and gaming. It’s also fair to point out that, morality aside, these industries have thrived in the last several decades.

So, while traditional banking institutions will often deal with the proceeds from the cannabis industry, including allowing bank accounts for these businesses, there is far less of a chance that they would invest in a cannabis business, for fear of risking their license. They can even go so far as to refuse to include income from a cannabis business in the determination of a loan application.

There are more unique lending or investing groups that either specialize in cannabis or are starting to open their books to specialize in cannabis. Overall, there is more interest in the industry than ever before, as it becomes normalized in American society: more participants and more insiders of the industries that are willing to invest in the right idea.

Will legalization be more likely in the future?

The fact that cannabis businesses and dispensaries have been deemed essential services during the pandemic, where they legally operate, has shed new light on the relevance of these businesses and the advantages of more widespread legalization.“Consumers will help drive the innovations as they demand clean consumption methods”

In fact, the pandemic has normalized a lot of new behaviors, including the acceptable use of cannabis to help with stress and anxiety. People are, perhaps thanks to staying at home more, doing the legwork to understand how cannabis could be useful to them in managing their stress. The medicinal benefits of cannabis have long been researched and understood: consumers are coming into the fray to express their interest in it, which can only fuel the possibility of more widespread legalization.

Add to this the fact that the cannabis industry is a growth industry. There are companies and jobs that aren’t coming back, post-pandemic. There is an opportunity to grow the cannabis industry to the general benefit of many, both as business owners and employees. The revenue generated from taxation following legalization would also benefit many state coffers. Federal level legalization would be the panacea to eliminate the mixed message, state by state regulation that currently exists.

Opportunities for innovation, moving forward

As more and more people become interested in the industry, and as cannabis use is normalized within society through legalization, the opportunities for the industry can only expand.

For an industry that started on the simple concept of smoking cannabis, the advances have already been legion: edibles, nanotechnology-based formulations for effective, clean consumption and many more innovations.

In a world that increasingly sees smoking as a negative, for the obvious impact to lung health, there are so many opportunities to grow the industry to find consumption methods that are safe and still deliver the impact of the inhaled version.

Here again, consumers will help drive the innovations as they demand clean consumption methods. The technology is available to make this possible; it only takes innovation and education to find the best ways to move this industry forward.

As legalization expands—and particularly if it is dealt with at the federal level—the industry will be able to capitalize on existing infrastructure for manufacturing and distribution, allowing new businesses to grow, get funded and thrive in the new normal.

Back in August, Lake Superior State University (LSSU) announced the formation of a strategic partnership with Agilent Technologies to “facilitate education and research in cannabis chemistry and analysis.” The university formed the LSSU Cannabis Center of Excellence (CoE), which is sponsored by Agilent. The facility, powered by top-of-the-line Agilent instrumentation, is designed for research and education in cannabis science, according to a press release.

Chemistry student, Justin Blalock, calibrates an Agilent 1290 Ultra-High Pressure Liquid Chromatograph with a 6470 Tandem Mass Spectrometer in the new LSSU Cannabis Center of Excellence, Sponsored by Agilent.

The LSSU Cannabis CoE will help train undergraduate students in the field of cannabis science and analytical chemistry. “The focus of the new LSSU Cannabis CoE will be training undergraduate students as job-ready chemists, experienced in multi-million-dollar instrumentation and modern techniques,” reads the press release. “Students will be using Agilent’s preeminent scientific instruments in their coursework and in faculty-mentored undergraduate research.”

The facility has over $2 million dollars of Agilent instruments including their UHPLC-MS/MS, UHPLC-TOF, GC-MS/MS, LC-DAD, GC/MS, GC-FID/ECD, ICP-MS and MP-AES. Those instruments are housed in a 2600 square-foot facility in the Crawford Hall of Science. In February earlier this year, LSSU launched the very first program for undergraduate students focused completely on cannabis chemistry. With the new facility and all the technology that comes with it, they hope to develop a leading training center for chemists in the cannabis space.

Dr. Steve Johnson, Dean of the College of Science and the Environment at LSSU, says making this kind of instrumentation available to undergraduate studies is a game changer. “The LSSU Cannabis Center of Excellence, Sponsored by Agilent was created to provide a platform for our students to be at the forefront of the cannabis analytics industry,” says Dr. Johnson. “The instrumentation available is rarely paralleled at other undergraduate institutions. The focus of the cannabis program is to provide our graduates with the analytical skills necessary to move successfully into the cannabis industry.”

Storm Shriver is the Laboratory Director at Unitech Laboratories, a cannabis testing lab in Michigan, and sounds eager to work with students in the program. “I was very excited to learn about your degree offerings as there is a definite shortage of chemists who have experience with data analysis and operation of the analytical equipment required for the analysis of cannabis,” says Shriver. “I am running into this now as I begin hiring and scouting for qualified individuals. I am definitely interested in a summer internship program with my laboratory.”

LSSU hopes the new facility and program will help lead the way for more innovation in cannabis science and research. For more information, visit LSSU.edu.

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

We use tracking pixels that set your arrival time at our website, this is used as part of our anti-spam and security measures. Disabling this tracking pixel would disable some of our security measures, and is therefore considered necessary for the safe operation of the website. This tracking pixel is cleared from your system when you delete files in your history.

We also use cookies to store your preferences regarding the setting of 3rd Party Cookies.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.