Despite the US making cannabis regulations challenging to navigate, the industry is snowballing toward profitability. New Jersey legalized adult use cannabis on April 21 this year. One month earlier, The Garden State began accepting applications for Class 5: Retailers, Dispensing and Delivery.

Although New Jersey isn’t shy about its licensing requirements and standards, many people want to know how retailers can stay in the game for the long run. So, let’s talk about risk management considerations New Jersey retailers need to know.

Top Risks Cannabis Retailers Face in New Jersey

Regardless of what kind of retailer you operate —medical or adult use — it’s critical to know what you’re up against. The following are the most common risks we’ve watched cannabis retailers face daily in New Jersey, making a customized risk management strategy necessary.

Theft

Like other retailers, New Jersey cannabis retailers are vulnerable to theft. Unfortunately, theft can come from various angles, such as in-store, in-transit and insider crime. Besides cannabis retailers typically having a well-stocked inventory, it’s not uncommon for them to have more cash on hand than most other businesses.

Although the SAFE Banking Act could positively impact the cannabis industry, it’s in a notorious stall yet again. Briefly, the SAFE Banking Act would no longer allow financial institutions, such as banks and credit card companies, to refuse to do business with cannabis companies. However, cannabis retailers must operate in a cash-only environment, for now, forcing them to make bank runs multiple times a day. We probably don’t have to explain how enticing a significant inventory and fat bank bags look to criminals.

Cybersecurity

Since the onset of the global health crisis, the cyber liability landscape has nearly spun into a death spiral. In other words, cybercriminals sat on the edge of their seats during the pandemic, waiting to pounce on anything that looked slightly vulnerable. Remote workers, small businesses, and emerging industries were hard-hit.

It’s no surprise that New Jersey cannabis retailers face many cybersecurity risks through their point of sale (POS) systems. Additionally, retailers often gather and store personal information, such as email addresses, credit card numbers, shipping addresses, etc. Hackers and cybercriminals gravitate to this vital data rapidly.

Property Damage

In addition to the risk of theft, as mentioned above, cannabis retailers must protect their property from losses. Without adequate protection, damage to equipment or buildings could add up to high out-of-pocket costs. Consider the damage a weekend office fire or late-night vandalism would cause. If property damage occurs, retailers must figure out how to sustain business operations while recovering from the loss simultaneously. As a result, New Jersey retailers must protect their property and maintain business continuity.

How to Customize a Risk Management Strategy

Watch or listen to any news reports and there’s a decent chance that you’ll feel some slight sense of doom and gloom. And sure, a lot is going wrong in our world; however, that doesn’t need to impact how you perceive your businesses. Instead of casting a massive net over every possible risk that you can imagine, we recommend trying the following 5-step approach. Here’s the gist:

Identify: Pinpoint high-level risks that are specific to the cannabis industry. Then, let the process trickle down to focus on company-specific exposures.

Analyze: Determine how badly a particular risk could harm your retail company. How much will this hurt should the “what-ifs” play out?

Evaluate: Categorize risks according to how risk tolerant your company is. Will you avoid, transfer, mitigate or accept the risk?

Track: Use your history or the stats from a similar retailer to map out how you’ve handled the risk over time. Older retailers have an advantage over younger retailers, of course, but you can still get a feel for your risk management style.

Treat: Make good on your evaluation promises by avoiding, transferring, mitigating, or accepting the various risks you identified.

Recommended Insurance for New Jersey Retailers

Sales totals in the first month of New Jersey’s adult use market

The New Jersey Cannabis Regulatory Commission issued detailed requirements for new cannabis businesses. That said, part of the application requirements considered is the plan for companies to obtain liability insurance. Many new retailers opted for a “letter of commitment” as opposed to a certificate of insurance (COI), stating their plans for obtaining the following coverages:

Commercial general liability: Protects cannabis companies against basic business risks.

Product liability: Protects against claims alleging your product or service caused injury or damage.

Property: Reimburses cannabis companies for direct property losses.

Workers’ compensation: Covers employees if they are injured on the job and can no longer work.

In addition to the required insurance coverages, we recommend New Jersey retailers customize their risk management package with these policies:

Crime: Protects your cannabis company against specific money theft crimes.

Cyber: Protects your cannabis company against damages from specific electronic activities.

Directors & officers: Protects corporate directors’ and officers’ personal assets if they are sued.

Employment practices liability: Protects cannabis companies against employment-related lawsuits.

Professional liability: Protects cannabis companies against lawsuits of inferior work or service.

With more states in the US entering the marketplace soon, New Jersey is doing its fair share of the heavy lifting by spearheading the onboarding process. Remember, doing your due diligence at the start pays off in the long run — New Jersey retailers are proving that. Consider teaming with a commercial insurance broker calibrated to the cannabis industry, so you get the most out of your broker, marketplace and the cannabis industry as a whole.

In a growing number of communities around the U.S., new cannabis lounges are offering a social setting where guests can openly use cannabis products. Colorado and New Mexico both saw their first cannabis lounges open in April, Michigan’s first cannabis lounge is set to open this summer, and officials in Nevada are currently discussing how the recently approved class of businesses should be regulated. In West Hollywood, California, where the state’s first cannabis lounge opened in 2019, multiple new lounges are now in the works after two years of slowdown due to the pandemic.

The bar-like establishments add a new dimension of potential revenue — and risk — to an industry that is expected to add almost $100 billion to the U.S. economy this year. This new and emerging segment within cannabis isn’t happening in every legal state, but more are starting to enact regulations to provide for some type of on-site consumption.

These new ventures need insurance policies tailored to address the risks of serving cannabis products, which could be looked at similarly to liquor liability for bars and restaurants.

Whether it’s alcohol or cannabis, these products impair people’s judgment, meaning everyone reacts differently to them. But how do you know when to cut someone off?

Cannabis lounges could be held liable & run risk of being sued for overserving

If a cannabis lounge faced a lawsuit alleging that it overserved a patron, leading to a third-party bodily injury, the business’ Commercial General Liability (CGL) Insurance and Products Liability Insurance could potentially cover costs such as legal defense, medical expenses and settlement amounts. Until such a case occurs, it is not yet known how exactly these lawsuits would be covered by insurance.

Because of the short history of cannabis lounges in the U.S., something like this is largely untested, making it hard to speak to exactly how a scenario would play out. Many of the existing cannabis insurance policies are highly exclusionary, meaning it could exclude a loss that is deemed to have arisen out of the use of cannabis.

Recent liquor liability lawsuits have shown the potential for a significant loss is clear. In early April 2022, a $20 million lawsuit was filed against a nightclub in Houston, Texas, alleging it overserved customers and allowed underage drinking, contributing to a drunk driving crash that killed a teenager.

In December 2021, a jury in Texas awarded the family of two drunk driving victims over $301 billion after a lawsuit alleged the driver was overserved at a bar before the accident; though largely symbolic, the settlement marked the largest personal injury award in U.S. history.

The Barbary Coast lounge in San Francisco

With these cannabis lounge establishments more or less encouraging intoxication of patrons on their premises, it’s very similar to a liquor liability type situation. If someone overindulges at a lounge, leaves and causes a crash resulting in injury or death, that could come back to the establishment.

While it remains to be seen how cannabis overserving lawsuits could play out in American courts, it’s worth noting Canada forbids on-site consumption of cannabis products and any loss or damage will not be covered by their insurance policies – despite it being legal country-wide.

Lawsuits possible over product issues, budtender advice

Even cannabis operations that do not allow on-site consumption can face liability related to the products they sell, making Products Liability Insurance and Product Recall Insurance necessary for growers and retailers. They should also consider Employment Practices Liability (EPL) Insurance to cover staffing-related allegations such as discrimination and ask their insurance broker whether budtender liability is included in their CGL Insurance policy.

Budtenders must walk a fine line between giving advice versus general information on products.

Budtenders, or individuals who work at cannabis retailers, are not allowed to offer medical advice to consumers. They must walk a fine line between giving advice versus general information on products. Although we are not aware of lawsuits that have been filed over a budtender’s advice, it would ultimately be up to the courts and lawyers as to how those proceedings would play out.

Budtender liability is not very different from professional liability insurance, and it’s more like an incidental coverage based off the budtender’s informal advice. There are, indeed, insurance carrier partners today that offer that service.

CGL Insurance can also cover in-store slip-and-falls and other third-party injuries and property damage. Because most cannabis retail stores are fairly small, these incidents have been rare, but GCL cannot be overlooked. Businesses must be prepared for anything to happen – and need to know that no risk is too small.

Theft, vandalism among top threats to cannabis businesses

Whether or not a cannabis business includes a lounge for cannabis use, any business in this industry may be more vulnerable to certain risks, including theft and vandalism.

In the U.S., where many cannabis companies operate on a cash-only basis because of banking difficulties tied to recreational products being federally illegal, a recent surge in cannabis shop robberies has led to calls for a new banking bill. Some of these incidents have even turned deadly, including an April 30 dispensary robbery in Los Angeles, California, during which one man was reportedly shot and killed.

Many insurance carriers require retailers to install alarm systems, video monitoring equipment or safes

Large amounts of cash are on-hand daily at these premises, and workers might have to make multiple bank runs throughout the day, leaving a heightened exposure and risk for robberies.

From robberies and vandalism to fires and flooding, Commercial Property Insurance is a key protection for cannabis retailers. Equipment Breakdown Insurance may also be needed, particularly when the stores contain expensive refrigeration equipment. The potential loss is large in this industry, especially at growing facilities, and there’s a lot at stake with such high-value equipment.

Security systems, employee training can help reduce risks

Many insurance carriers require business owners to install alarm systems, video monitoring equipment or safes to help reduce potential property losses, and employees should be trained to use the alarm systems consistently. Policyholders and business owners should also know there is a lot they can do to curb some of the risks, such as businesses doing background checks on every hire and taking steps to ensure they are hiring individuals they can trust.

Installing bars on glass windows and doors is another loss prevention measure that is strongly encouraged because it adds an additional layer of security to get through – it won’t be an easy or quick process to break-in and will trigger the alarm system.

The importance of working with an insurance broker

Working with an insurance broker who is specialized in the cannabis industry can help business owners better explore available coverage options. With cannabis or any type of risk, you should always work with someone who has knowledge and expertise in that area. When you work with someone who knows the ins-and-outs of the regulations, you can have more peace of mind.

You might have a risk warranty that always requires two drivers in that vehicle, or GPS monitoring on the vehicle.

Understanding your policy in its entirety is also essential, as these policies have any number of different limitations and exclusionary forms that could preclude you from collecting if you had not understood and followed the language of the policy.

In a transportation situation, for example, you might have a risk warranty that always requires two drivers in that vehicle, or GPS monitoring on the vehicle. In the event of a claim, if the investigation determines the business did not have those items present at the time of loss, that claim will not be covered.

In a rapidly growing and changing industry, business owners should not underestimate the value of working with a team of insurance experts who keep a close pulse on the quickly evolving industry. Brokers are aware of the different legal environments in each state or even each city or county. Cities and counties can add different levels of compliance matters, so as a buyer, you can be confident that you have the most recent information and are in compliance with state law and any insurance requirements that may be present. Being able to explain the differences between the markets and the coverage options is beneficial to any business owner in this ever-changing industry.

Cannabis continues to be a hot sector across the United States; buoyed by its ‘Essential Business’ status during the pandemic, a surge of plant touching and ancillary service providers have set up shop in the past 12 months to capture a share of this burgeoning growth. The cannabis industry is currently the leading job creator in the country, employing almost 430,000 workers according to a recent report from Leafly. Estimates on the overall size of the industry vary depending on the source, but projections of over $100bn in value by 2030 are not uncommon, while M&A activity continues to gather pace after a downturn in 2019. Clearly, investors and the public are bullish on the industry as a segment, with further state legislation to expand the number of adult use and medical markets to come. So why is the directors & officers (D&O) and management liability insurance market not embracing this growth industry?

At its core, a good D&O policy will protect the individual directors, officers and executive teams of companies, including their personal assets, in the event of suits and allegations filed based on their running and oversight of their business. For private companies, this also extends to balance sheet protection and coverage for the entity; for public companies, coverage for securities suits and claims.

The cannabis industry, despite the macro factors propelling its growth, faces numerous challenges when trying to procure D&O insurance. Very few D&O and management liability carriers are willing to entertain cannabis and related risks; even fewer are specialty underwriters willing to provide meaningful, expert coverage which truly addresses the exposures faced by executives and operators in the cannabis industry.

Cannabis D&O premiums can cause sticker shock, typically priced 4 to 10 times higher than non-cannabis businesses. Some operators have an air of invincibility and forego the purchase, believing it is not worth the cost. Meanwhile, the ability to attract and retain talented executives and directors away from other industries typically depends on having this coverage purchased and in place. Yet the outlay can be a burden in an industry which already faces fierce competition for market share, and a disparate tax treatment at a state and federal level.“The value of a D&O policy cannot be overstated.”

Even those carriers and underwriters who do entertain cannabis risks are constantly evaluating the nuances of the space: an ever changing complex state regulatory environment; the relative immaturity of the industry and the hyper-focus on growth; the lack of standardized valuation and accounting; the lack of access to institutional financing; the continued uncertainty of insolvency or restructuring in lieu of federal bankruptcy protections for plant touching companies; the operating inefficiencies for MSOs across state lines and the lack of interstate commerce; in short, the cannabis industry certainly poses its own unique and evolving risks for D&O insurers.

Ultimately the market will continue to evolve for cannabis insureds, as the data matures and the regulatory landscape become clearer. The value of a D&O policy cannot be overstated. Most public companies purchase D&O as a matter of course, but even for private cannabis companies, the right coverage is invaluable. Not having the protection afforded by a D&O policy can be ruinous for a cannabis operator, particularly in a niche area where defending claims and circumstances is complex, time consuming and ultimately expensive – typically much more so than the upfront cost of the D&O policy.

Partnering with the right broker who specializes in both management liability and cannabis is step one to getting the best value coverage. Step two is securing a policy from a dedicated market with underwriters who truly understand the cannabis space and tailor coverage to protect the executives, boards and companies that are driving this exciting growth industry.

Cannabis remains one of the fastest growing industries with no signs of slowing down. According to a recent article in Forbes Magazine, the legal cannabis market is poised to grow 20-30% per year to the tune of $50 billion by 2026.[1]With great opportunity comes numerous risks. Claims and lawsuits against cannabis businesses are increasing in frequency and magnitude. As an insurance broker who specializes in the cannabis industry and works with a wide variety of cannabis, hemp and CBD businesses in every state where cannabis laws are established, our recent analysis has unveiled the top five insurances your cannabis business needs in 2022.

General Liability

General liability is the most essential coverage your business needs to protect you from a variety of claims including personal injury, bodily harm, property damage and other situations that may arise including slander, libel, copyright infringement and more.

Since general liability is not always required to obtain a cannabis license, many businesses are tempted to forgo the expense. This is one of the biggest mistakes you can make as one single lawsuit has the potential to cripple your business. With a comprehensive, cannabis-specific general liability insurance policy in place, your insurance company, not you, will pay medical expenses and property damage claims from third parties, in addition to hefty legal fees and fines.

Property & Casualty Insurance

P&C insurance is an important part of your security and protection plan.

If you own a dispensary, grow operation, warehouse, testing facility or any other type of cannabis business with inventory, you need to protect your assets from potential loss or damage. Property & casualty (P&C) insurance safeguards your business against common and costly perils such as a fire, lightning, explosion/implosion, and even less common – but still possible – risks like riots, strikes and terrorism.

P&C insurance not only pays for damages to your business property resulting from a covered loss but it also covers the contents within your place of business, including office furniture, computers, inventory and other assets essential to your business operations. There are policies that will also provide the funds required to keep your business afloat until the damages from the loss are repaired. Any cannabis business with a physical property and location(s) should have a comprehensive property and casualty P&C policy in place.

Product Liability/Product Recall

Recently, we’ve seen a dramatic influx of product liability claims, and in particular, product recalls. Lawsuits have ranged from a single plaintiff seeking damages for personal injuries to class action lawsuits where a defective product is tied to an entire group of claimants.

Preventing contamination can save a business from extremely costly recalls. Having the right insurance can prevent a recall from becoming costly in the first place.

As a cannabis business owner, you can be sued for any damage resulting from products that cause harm to others, this includes false advertising, mislabeled or defective products. No matter where you are in the supply chain, your business could be held liable. The process of defending litigation or reaching a settlement agreement can completely drain a company’s resources. You’ll have to deal with regulatory compliance, producing and distributing product warnings, recalling products, claim investigation, product testing and additional risk assessment.

Product liability insurance is often overlooked, especially by small to mid-size businesses. However, your cannabis business needs this type of coverage if you sell any goods or products that end up in the hands of the public. In fact, your business may be contractually obligated to have product liability insurance. One such lawsuit is enough to fold a business due to costly legal fees and fines, as well reputation damage beyond repair.

Product liability insurance is designed to protect your cannabis company from claims that can happen anywhere along the supply chain, including product contamination, mislabeled products, false advertising or defective products. With proper coverage, your insurance company will pay for damages and legal expenses if you are sued, up to your policy limits. Your product liability policy will also cover any medical expenses for those who are harmed by your business. Making sure your insurance policy includes product liability insurance should be a top priority in 2022.

Cyber Defense/Data Breach Insurance

Cyber fraud and data breaches are two of the greatest risks facing cannabis companies in 2022. With so much cash pouring into the space, cannabis businesses of all sizes are bulls-eye targets for cybercriminals. Even the smallest of cannabis businesses are at risk of data breaches because they are part of a larger interconnected network of seed to sale vendors. These types of crimes can have detrimental effects on your business in numerous ways. In the case of a data breach resulting in the disclosure of a third party’s private information, the third party could sue your business. The SEC could also find your company negligent in cyber fraud cases and impose significant fines.

By forgoing cyber defense & data breach insurance, your business will be solely responsible for expensive legal bills, significant revenue losses and hefty fines and penalties from regulators. Cyber defense & data breach insurance is a must-have coverage in 2022, and beyond, to protect your business from cybercrimes.

Directors & Officers Insurance

If you are looking to secure venture capital or funding from investors in 2022, and/or attract and retain qualified leadership, you need directors & officers (D&O) Insurance. D&O protects corporate directors and officers, as well as their spouses and estates, from being personally liable in the event your company is sued by investors, employees, vendors, competitors, customers, or other parties, for actual or alleged wrongful acts in managing the company. In the event of litigation, your D&O insurance will cover legal fees, fines, settlements and other expensive costs.

D&O is often the most overlooked coverage because many cannabis businesses are independently run, and no one foresees the potential for operational failures and mismanagement. However, businesses with any sort of vision for growth should make D&O a top priority. It not only protects your current executives and board members but is critical in attracting leading talent in the space, as well as drawing in new investors to scale up your business. In fact, we’re seeing more prospective investors and board members requiring D&O insurance prior to engaging with a company to ensure they are fully protected in the event of litigation.

When it comes to mitigating risk in this business, the stakes are sky high. Cannabis companies that have not incorporated risk management into their business/operational plans will need to in 2022. It all boils down to the THREE P’s: being “Proactive, Prepared and Protected.”

Cannabis risks have always outpaced the availability of insurance, in large part because of its status as a federally illegal substance and the dangers in extraction and production. But it now shares many of the same risks as other industries — catastrophic crop damage, cyber risk and a shortage of skilled workers.

With legalization becoming more common, the industry is positioned for enormous growth despite these challenges. However, enterprises that will benefit the most are those best positioned to manage risk.

Here are four obstacles to growth in the industry in 2022 and how enterprises can combat them:

Cybercrime will be the top manufacturing risk

Both cybercrime and cannabis have experienced major booms since the start of the COVID-19 pandemic. Cannabis companies watched as healthcare and pharmaceutical organizations were hit hard by cybercriminals in 2020, and now the threat could be headed their way.

For retailers, the vulnerability often lies in their POS tech

For cannabis retailers, the vulnerability lies in their dependence on point-of-sale tech, while the threat for cultivators exists within their strong use of intelligent automation to manage the grow environment. Across the industry, the lack of sophisticated IT security systems is like a beacon for bad actors.

Nearly 60% of cannabis businesses say they haven’t taken the necessary steps to prevent cyberattack, but the winds are changing. Due to these concerns and the growing attention on cybercrime in the industry, cyber coverage is expected to rise 30% or more in 2022, which puts the onus on risk management practices that will help prevent cyberattacks and ensure coverage from insurers concerned about risk.

Barriers to business growth may result in more M&A

As of summer 2021, 18 U.S. states have legalized adult use and 37 states have legalized medical cannabis.

While this is opening opportunities for many cannabis businesses, the U.S. remains a complicated market. Federal regulations continue to hinder even more cannabis industry growth by restricting lending to the industry from traditional banking and financial institutions. While it’s not illegal to do service with the cannabis industry, many institutions stay away due to its high risk.

Smaller cannabis companies are impacted most heavily by this barrier and await passage of the Secure and Fair Enforcement (SAFE) Banking and Clarifying Law Around Insurance of Marijuana (CLAIM) Acts to allow easier access to capital. Together, these two acts of legislation will provide guidelines on how to work lawfully with legal cannabis businesses and prohibit penalizing or discouraging institutions from working with them.

In the meantime, M&A activity is expected to increase in 2022 as large cannabis businesses have the means to access capital and acquire these small companies. This includes Canadian cannabis companies, unburdened by federal restrictions, who are expected to increase their cross-border mergers and acquisitions.

Severe weather isn’t easing up

Extreme natural catastrophes are no longer rare, and they have only added greater uncertainty to the industry which has always had difficulties securing crop insurance.

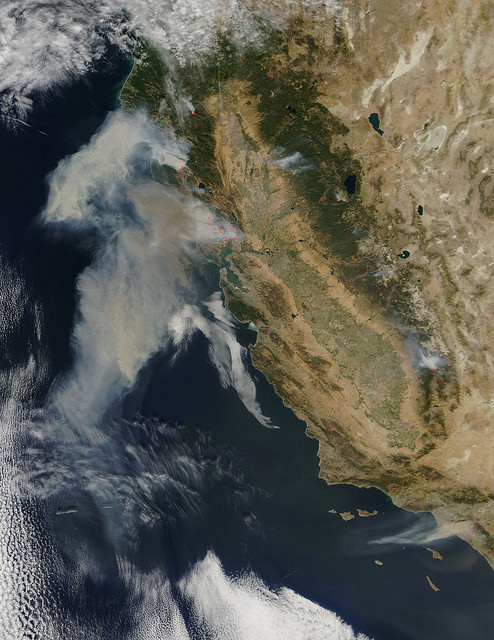

NASA’s Aqua satellite took this picture of the smoke over California in 2017 Photo: NASA

For example, policies that transfer wind and hurricane damage risk in Florida or wildfire and smoke taint in California are virtually non-existent for cannabis — and for outdoor growers, a single weather event can wipe out an entire crop with no recourse.

One possible solution for cannabis companies that cannot secure traditional crop insurance is parametric insurance, which pays out in full when a weather element reaches a threshold, regardless of the actual damage.

Growers with indoor operations, or those considering moving that way, must cope with energy conservation initiatives. Measures like the one in California that would require indoor growers to use LED lighting by 2023 could cost the industry millions and present a direct threat to small operations’ viability. This makes it important for cannabis producers to institute conservation measures and undertake risk mitigation measures like improved safety measures at indoor growth facilities ahead of 2022 renewals.

As a continually emerging market, cannabis risks are great. Adding to these pressures is the growing impacts of climate change and cybercrime raising the bar even further. Growth for the cannabis industry in 2022 will depend upon strong risk management solutions and the ability for cannabis companies to implement them.

The cannabis industry in the United States represents about a $50 billion asset class making it one of the largest new asset classes in the country. Commercial real estate lending is a key enabler for companies seeking to expand and scale. Pelorus Equity Group is one of the largest commercial lenders in cannabis with over $170 million deployed since its first cannabis transaction in 2016.

Since 1991, Pelorus principals have participated in more than $1 billion of real estate investment transactions using both debt and equity solutions. Pelorus offers a range of transactional solutions addressing the diverse needs of cannabis related business operators. While most cannabis private equity lenders focus on real estate acquisition and refinancing, Pelorus has leveraged its experience in more than 5,000 transactions of varying size and complexity to offer value-add loans, a rarity in the industry.

We spoke with Rob Sechrist, president of Pelorus Equity Group and manager of the Pelorus Fund. Rob joined Pelorus in 2010 after several years in the California real estate market. In 2018, Pelorus launched the Pelorus Fund where Rob is currently the manager. The Fund converted to an REIT in 2020.

Aaron Green: How did you get involved in the cannabis industry?

Rob Sechrist: Pelorus is a value-add bridge lender. We’ve been lending for a long time, originally in the non-cannabis space. We’ve done 5000 transactions for over a billion dollars – more than a lot of banks.

In 2014, our local congressman Dana Rohrabacher passed the Rohrabacher-Blumenauer Amendment that defunded the Department of Justice from prosecuting any cannabis related business in a medically licensed state. We were a supporter of that legislation and once that passed, we took a serious look at utilizing our expertise in being a value-add lender and applying it to the largest asset class of real estate that is newly coming about today. That cannabis related asset class is about $50 billion.

Rob Sechrist, president of Pelorus Equity Group and manager of the Pelorus Fund

We decided that we had the expertise to move into this space and to build these facilities out for our borrowers so that the cannabis use tenants would have a fully stabilized facility and make it operate. After the amendment passed in 2014, by 2016 we had originated our first transaction. Since that time, we’ve originated 51 transactions in the cannabis space for over $177 million so far. It wasn’t that big of a pivot when you’re just providing the value-add loan.

“Value-add” in the loan business means that a portion of the loan amount, let’s just say is a million dollars, maybe 250,000 of that, is a pre-approved budget to go back into the property. In cannabis property those are typically tenant improvements and/or equipment to fully stabilize that tenant. So, we’re the first fully dedicated lender in the nation exclusively to cannabis and we’ve done more transactions than anybody else in the nation.

Green: What are some challenges of cannabis lending compared to traditional lending?

Sechrist: The number one challenge in cannabis is that you must disclose to your investors that you’re originating the loans to cannabis use tenants. Many people have concerns that lending indirectly might be federally illegal. If you did not disclose that to your investors when you form that capital stack to fund these transactions, you’re going to run into issues. So, you would need to create a vehicle where you disclose to your investors that you’re intending to lend into cannabis and it’s still federally illegal. Doing one-off stand-alone transactions deal by deal is not sustainable if you’re going to be a large lender.

There are other challenges. Because cannabis is still federally illegal, it gives insurers and other third parties the ability to deny a claim, or certain lender protections. Some examples include errors and omissions insurance, title insurance, property insurance, etc. and all of them say in those policies that if you’re doing something federally illegal, then the policy is null and void. So, you must think your way through very carefully all the things that could potentially be an issue. You also have to disclose to those third parties and find a way to get them to acknowledge it to make sure you have the coverage if you ever have to make a claim. That’s a very difficult process.

Green: How has the investor profile in cannabis lending changed over time?

Sechrist: Our fund was structured to allow for institutional capital from the inception. We were able to do that because we are completely non-plant touching. Our fund only lends to the owners of commercial real estate. We do not lend to any cannabis licensed operator directly whatsoever. Our borrowers – the owners of the properties – would then have a lease agreement with the cannabis use tenant. Even if it’s an owner-operator, those are separate entities. That’s how we’ve distinguished ourselves.

Pelorus Equity Group, Inc. Logo

Regarding the investor profile, the first $100 million plus we raised was primarily from retail investors who were individuals writing checks up to a million dollars. Once we had three years of audited track record and our fund was $100 million, we then pivoted over to family offices and institutional investors and pension funds. We’re now working primarily with those types of investors.

The reason that we started with retail investors is that it’s very easy for me to explain our model to a single decision maker and answer their questions. Once I move into family offices or institutional investors, the opportunity goes to a credit committee where I’m relying on some other party to educate the investor about our investment. It’s enormously challenging at that point if it’s not me doing the talking. I know the answers, but I’m having to rely on somebody else to answer questions. We’ve tried to educate everybody we speak with and craft our documentation in such a way that even when it’s not myself answering the questions directly, people can understand how we thread the needle through some of the legal hurdles.

Green: How do you prioritize deal flow, and what are the qualities of a successful loan applicant?

Sechrist: We typically maintain a pipeline of around $150 million in transactions at any one time.

Applicants must have real estate. We’re not doing business loans or operator loans directly to tenants or business operations. So, that’s the starting point. We want a real estate piece of collateral where we feel more than comfortable with the loan-to-value and ratios and the loan to cost and other figures, that we feel that this transaction is going to be a success for our borrower and ultimately the tenant.

Next, we will only work with very experienced operators who have a proven track record where this is not their first transaction. Ideally, we are working someone who is looking to expand their operations and who is ready to either move from being a tenant of their previous facility and buying their next facility.

The next aspect that we’re looking for is the strength of the borrower’s guarantor. They must be able to qualify to support that transaction. Many of our transactions are millions or 10s of millions of dollars. You must have a sponsor that can support that size of a transaction.

Green: What sort of value-adds should a cannabis property owner look for in their lender?

Sechrist: Most people that are looking for loans are only familiar with getting loans for themselves on their owner-occupied house. Most loans have points, they have a rate and a term, loan-to-value and things like that.

“We wanted to make sure that when we underwrite the transaction, that every single piece of capital is necessary to get that facility all the way to where that tenant can start generating their first crops and make their lease payments.”When you move into construction loans or value-add lending, there are other elements that are more important than the pricing of the loan. The number one thing is to get that property fully stabilized and built as quickly as possible. Cannabis tenants are generating 10 to 15 times more revenue per month than non-cannabis tenants.

If you go to a bank and borrow money it may be a third of what it costs to borrow from us, but they process draws maybe once a month. So, if you’re having to advance the money for improvements of the property, and then the bank reimburses once a month, at a certain point you’re not going to be able to advance any more money until you get reimbursed. The project comes to a stop. So, in your mind, you might have saved an enormous amount on the pricing of the rate, but it’s costing you dearly in revenue and opportunity costs. We typically process 50 to 100 draws post-closing on transactions, and we get that facility built and the money reimbursed to all the contractors on a multiple-times-a-week basis. It’s happening in real flow all the time.

A typical problem for a tenant is that the tenant improvements are orders of magnitude higher than a non-cannabis tenant – anywhere from $150 to $250 per square foot. In addition, the equipment is often enormously expensive as well. It’s tough to put money into a buildout for a building that you may not own. Our vision at Pelorus was, let’s not force these tenants – the cannabis operators – to raise equity at the worst possible time when they’re not generating revenue through the facility. Let’s shift that capital balance for those tenant improvements and equipment from the from the tenant to the owner of the building, which is where it’s secured and adds value to that building anyway. Our vision was to shift that money from the balance sheet of the tenant over to the owner of the real estate so the tenant didn’t have to sell equity to come up with that money. Then the tenant is paying for the improvements in the lease rate and the borrower is paying for improvements in the note rate. And so we’ve shifted tenant improvements from being an equity component to now it’s just priced in the debt. This way you know what the terms are and you know what your total exposure is there.

We wanted to make sure that when we underwrite the transaction, that every single piece of capital is necessary to get that facility all the way to where that tenant can start generating their first crops and make their lease payments. Most of our peers in the space don’t look at it that way. They just do the acquisition or the refinance. They don’t do anything for the tenant improvements. They don’t do anything for the equipment. The tenant is left out there to either raise that equity or the borrower – the owner of the real estate – is having to come up with that additional capital on their own. We think you’re set up for failure in that circumstance. So, we blend all that into one capital stack. It’s important that the tenants can get all the way up to being able to cash flow and support that facility and be fully stabilized so they can refinance into a lower cost bank or credit union transaction.

Green: What federal policies and trends are you monitoring?

Sechrist: First, I think that it’s important to remind people that the Rohrabacher-Blumenauer Amendment has protected everybody from any prosecution. So, there’s no jeopardy out there that exists. The second thing I like to tell people is there are 695 banks on FinCEN’s website of cannabis Tier 1 depositors, and of those, we’re tracking numerous FDIC insured state banks and credit unions that are lending directly. We’ve been paid off by banks.

So, there’s this massive misconception that there’s no banking at all and that everything is happening by cash. The only cash buildup that happens is at the retail dispensary level because credit cards aren’t allowed for retail sales at the dispensaries. Out of the 2,000 transactions that we’ve either processed or reviewed, not one has ever not had banking set up. So, it is a big misnomer that there’s no depositor relations for Tier 1 banking, which is plant touching.

Tier 2/3 depositors are ancillary, which is what we are at Pelorus. There are 100 private lenders and dozens and dozens of state and federal credit unions or state banks and credit unions, not federal, that are FDIC insured and lending. Those banks are difficult to get loans from because they only want to do urban environments. They want to do fully stabilized companies and they want to use alternative views and the facility has to have seasoning for cash flow. It’s difficult to qualify for them. So, banking and lending exists out there, and most people are not aware of that.

Green: What are you most interested in learning about? This could be either in cannabis or in your personal life.

Sechrist: My two passions are snowboarding and racetrack driving. I just came back from the Mille Miglia race in Italy, and I do a lot of driving on the racetracks. I’m always looking to learn from those experiences.

In the cannabis sector, social equity programs are happening across the nation and cannabis licenses are being issued to operators. We would like to help participate in some system of educating these applicants that win the awards. Lending to an owner of a property who just won a license but has no experience is going to be problematic. Somebody needs to be thinking that out and making sure that these people that win have enough experience and education to set them up for success. Cannabis is one of the most complicated businesses ever, and they’ve got this license as their ticket, but they need to know how to make sure they’re going to be successful.

HUB International, a leading insurance brokerage serving the cannabis industry, just announced today their new U.S. cannabis specialty leader. Bradley Rutt, senior vice president at HUB and Cannabis Industry Journal contributor, will now take the lead on cannabis insurance for the brokerage.

Bradley Rutt, senior vice president and U.S. cannabis specialty leader at HUB International

Rutt will work alongside Jay Virdi, another frequent CIJ contributor and chief sales officer of cannabis specialty at HUB to support the practice strategy on a national level. Rutt’s role will put him in charge of expanding HUB’s growth in the cannabis space as well as “enhancing cannabis insurance solutions and risk services, further developing cutting-edge resources for clients to support their needs, and attracting and retaining talent to deepen knowledge and expertise to help cannabis clients thrive.”

Rutt’s role as senior vice president has been to specialize in cannabis executive liability, working with public and private management services organizations to develop insurance and risk management programs. “Brad is an industry leader, and his diverse experience and deep understanding of the cannabis industry to insure its unique risks will play a critical role in continuing to strengthen our practice,” says Jay Virdi. “More importantly, we continue our commitment as trusted advisors to our clients to provide them with relevant support and solutions to help them continue to grow.”

Things are about to change for cannabis and cannabis-related businesses, as landmark legislation to reform federal cannabis banking and insurance laws is just around the corner with the SAFE and CLAIM Acts now making their way through Congress.

The Secure and Fair Enforcement (SAFE) Banking Act, which already passed in the House, would allow financial institutions to do business with cannabis companies without facing federal penalties. There are high expectations the proposal will make its way through the Senate and onto President Biden’s desk.

The Clarifying Law Around Insurance of Marijuana (CLAIM) Act was introduced in Congress in March and is in the first stage of the legislative process. If it passed, it would allow insurance companies to service cannabis businesses without the threat of federal penalties.

For years, fear of sanctions kept banks and credit unions from working with the cannabis industry, forcing cannabis businesses to operate on a cash basis which made them targets of crime and created complications for financial regulators. This is a significant first step for cannabis businesses toward conducting more legitimate and safe operations.

The SAFE Banking Act: Providing a Legitimate Avenue to Banking and Loans

With 37 states and D.C. having taken action to legalize cannabis in some way, it is clear the federal cannabis regulatory model has shifted and the path forward for the SAFE Banking Act shows promise.

The bill creates a safe harbor for banks and credit unions to the extent they would not be liable or subject to federal forfeiture action for providing financial services to a cannabis-related business.More competition means greater capacity and lower premiums for all.

The bill would prohibit a federal banking regulator from:

Recommending, incentivizing or encouraging a depository institution not to offer financial services to an account holder affiliated with a cannabis-related business or prohibit or otherwise discouraging a depository institution from offering services to such a business

Terminating or limiting the deposit insurance or share insurance of a depository institution solely because the institution provides services to a cannabis-related business

Taking any adverse or corrective supervisory action on a loan made to a person solely because the person either owns such a business or owns real estate or equipment leased to such a business.

The CLAIM Act: Backing Cannabis Businesses with the Right Insurance Coverage

Should the CLAIM Act pass, it will protect insurance companies that provide coverage to a state-sanctioned and regulated cannabis business. It would also prohibit the federal government from terminating an insurance policy issued to a cannabis business and protect employees of an insurer from liability due to backing a cannabis-related business.

The CLAIM Act will be a boost for the insurance market and drive more underwriters to write cannabis policies. More competition means greater capacity and lower premiums for all. The act would also have a notable impact on currently hard-to-source policies like Cyber coverage, Directors & Officers (D&O) insurance, Errors & Omissions (E&O) and other management liability policies that have been extremely limited to cannabis businesses.

Cannabis Sales Still Growing Strong Globally

The cannabis market is not slowing down in the United States or globally. Recent forecasts have U.S. sales reaching $28 billion in 2022.

As was the case in Canada where cannabis was made federally legal in 2018, there’s going to be a steep learning curve industry-wide for financial services and insurance vendors who don’t yet understand the risks and liabilities of cannabis operations, even if the SAFE and CLAIM Acts pass this year. And yet this is one giant step in the right direction toward the safe and equitable sales of cannabis country-wide.

Worth an estimated $54 to $67 billion, the bourgeoning U.S cannabis industry continues to grow at record pace despite conflicting state and federal laws that cause obstacles at every turn.

This conflict remains a source of uncertainty for retailers, cultivators and the general public. And, unfortunately, the palpable tug of war between the states and the federal government will only increase when legalization is introduced at the federal level, putting tax dollars up for grabs.

A tug-of-war between the states and the federal government makes it difficult for cannabis businesses to obtain bank accounts, insurance and investors. It also means additional security and compliance challenges. It is the reason that the cannabis industry is an unsupportive environment for start-ups and employees who face primitive or even dangerous R&D conditions in order to advance the extraction process.

As cannabis companies fight to grow their market share, many lag behind when instituting a proper risk management structure from R&D to daily operations. Cannabis businesses that haven’t incorporated risk management will need to in 2021, especially when seeking to secure funding from PE firms.

As the 8th fastest growing industry in the U.S., maturing at more than 25% annually, adult use and medical cannabis sales are unlikely to decrease anytime soon. Rather, experts predict continued growing pains – and gains – to shape the U.S. cannabis industry in 2021.

The COVID-19 pandemic will continue to increase the growth of the cannabis industry— with a few roadblocks

Deemed “essential businesses,” many retail outlets and dispensaries stayed open throughout the pandemic and adopted new ways of serving customers, from curbside pick-up to drive-through windows and deliveries. At the same time, the pandemic hindered growth for some cannabis operations on the cusp of obtaining a license, as many applications were put on hold when state offices closed their doors for months. In some cases that meant raised capital was pulled and funding ceased. For start-ups who are seeking to apply again in 2021, it’ll be an uphill climb.

As a result of routine COVID-19 inspections in 2020, state officials uncovered a host of other issues at cannabis operations, including improper labeling, poor health and safety practices, lack of PPE compliance by staff and customers, incorrect counting of cash and more. In extreme cases, these visits resulted in regulatory fines and shutdowns. This led to the need to use seed money for something other than the organization’s original mission. In 2021, these scenarios are likely to turn into lawsuits from shareholders and activate directors & officers (D&O) and employment practices liability (EPL) claims from laid-off workers. These accusations dovetail with another major charge often levied against cannabis businesses —lightning speed growth without the business operations and risk management protocols necessary to support it.

Many cannabis businesses have not procured the necessary liability insurance coverage for the great risk that come with rapid growth. Whether it’s D&O and EPL policies as in the case above, or cyber, property or general liability (GL) policies, it’s critical to think more holistically about insurance coverage. Cannabis operations need to work with an insurance broker who specializes in the cannabis industry and understands different operations and business location, as exposures vary greatly.

R&D extraction dangers lead to unique risks

In 2021, extraction will be a major focus for cannabis organizations. Operations will continue searching for a competitive advantage to increase yield and develop superior products. Cannabis extractors will experiment with new ways to apply existing laboratory methods utilizing ethanol and CO2 as well as innovative cultivation methods adopted from the agriculture industry, using water and light exposure and different nutrients. R&D becomes a potential liability when cannabis extractors modify the use of existing equipment for a different type of extraction. Flammable products are often required, and explosions can occur.

If you are considering experimenting with R&D, engage your insurance broker to ensure the risk is covered within your existing policies and to explore best practices for experimentation and varying equipment use.

Desire for more security both inside and outside the operation

A cannabis operation’s security risk is two-fold. In light of the looting and civil unrest across the U.S. this year, heightened security measures were necessary for cannabis businesses to secure their goods. Additionally, a common risk— employee theft —increased as well.

Cannabis retail operations maintain a large supply of cash and product. As looting occurred, it was impossible to relocate cannabis product away from retail storefronts as a majority of state regulations prohibit cannabis to be removed from retail facilities. Owners and operators who did so risked being fined for non-compliance or losing their license.

The majority of cannabis theft — as high as 90% by some estimates — is employee related. In many cases, employees in cannabis grow facilities and retail storefronts scheme to cheat employers. Part of the challenge is that state regulations require plant and production facility blueprints to be publicly available. Thieves are using these layouts to plot their infiltration. In other scenarios, cannabis operators are recording walk-throughs of their facilities and publishing online documentaries. These also leave operators vulnerable.

Employers can increase security by restricting access exclusively to employee areas, while also investing in better internal access controls. Conduct an audit of your work areas with your cannabis insurance broker who can provide you with a list of best practices and do’s and don’ts for reducing theft.

Complications continue in compliance, banking and financial services

Even though cannabis is legal for medicinal or recreational use in 43 states, businesses still struggle to secure bank accounts, business loans and insurance coverage. Small local banks and savings and loan businesses may be more willing to engage with cannabis businesses in 2021, while large institutions will keep shying away.

At every stop of the supply chain, cannabis business operators need to be proactive when developing strategies to manage risk. That means implementing risk management protocols to protect their business, their workforce as well as securing the proper insurance coverage.

This also includes growing the cannabis business’ safety net by engaging necessary insurance policies, appropriate to the business’ size and exposure, including cyber, environmental liability and crime policies, or applying for emerging loan programs in an effort to secure additional capital.

Evolution of the industry into 2021 and beyond

While the cannabis industry is evolving and changing, much will ultimately remain the same in 2021. Even if the U.S. government takes steps to federally legalize cannabis, a bill would not go into effect until later in the year at best, more likely in 2022 or beyond. Until a bill is passed, cannabis businesses will look to remain viable beyond the state level. For all cannabis businesses, 2021 will be about building on what they’re already doing and preparing for what will hopefully come next.

Since the beginning of this year, more than 8,100 wildfires have burned in California, torching a record 3.7 million acres of land in a state with one of the largest cannabis economies in the world. With the effects of climate change continuing to wreak havoc on the entire West Coast, smoke from those fires has spread across much of the country throughout the summer.

As we approach October, colloquially referred to as Croptober in the outdoor cannabis market for the harvest season, we’re seeing the August Complex Fire creep towards the Emerald Triangle, an area in northern California and southern Oregon known for its ideal cannabis growing conditions and thousands of cultivators. The wildfires are close to engulfing towns like Post Mountain and Trinity Pines, which are home to a large number of cannabis cultivators.

Hezekiah Allen, executive director of the California Growers Association, says losses could reach hundreds of millions of dollars. Fires across Oregon have torched dozens of cultivation operations, with business owners losing everything they had. The Glass Fire has already affected a large number of growers in Sonoma and Napa Counties and is 0% contained. None of these cultivators have crop insurance and many of them have no insurance at all.

The impact from all of these fires on the entire cannabis supply chain is something that takes time to bear witness; a batch of harvested flower typically takes months to make its way down the entire supply chain following post-harvest drying and curing, testing and further processing into concentrates or infused products.

Image: Heidi De Vries, Flickr

The fires affect everyone in the supply chain differently, some much more than others. Sweet Creek Farms, located in Sonoma County, lost all but one fifth of their crops to fires. Other cultivators further south of the Bay Area have lost thousands of plants tainted by smoke.

Harry Kazazian, CEO of 22Red, a cannabis brand distributed throughout California, Nevada and Arizona, says he is increasing their indoor capacity to make up for any outdoor flower loss. But he said it has not impacted his business significantly. “Wildfires have been a part of California and many businesses have adapted to dealing with them,” says Kazazian. He went on to add that most of his flower comes from indoor grows in the southern part of the state, so he doesn’t expect it to impact too much of his supply chain. Kazazian is right that this is not a new concept – the cannabis industry on the West Coast has been dealing with wildfires for years.

George Sadler, President of Platinum Vape

George Sadler, President of Platinum Vape, has a similar story to tell – the fires have impacted his supply chain only slightly, saying they had a handful of flower orders delayed or cancelled, but it’s still business as usual. “It’s possible this won’t affect the supply chain until later in the fall,” says Sadler. “There has definitely been an effect on crops that are being harvested now. It may end up driving the price of flower up, but we won’t really know that until January or February if it had an effect.”

Sadler believes this problem could become more extreme in years to come. “Climate change definitely will have an effect on the industry more inland, where we’re seeing fires more commonly – it could be pretty dramatic.”

One beacon of hope we see every year from these fires is how quickly the cannabis community comes together during times of hardship. Sadler’s company donated $5,000 to the CalFire Benevolent Foundation, an organization that supports firefighters and their families in times of crisis.

A large number of cannabis companies, like CannaCraft, Mondo, Platinum Vape and Henry’s Original, just to name a few, have come together to help with relief efforts, donate supplies, offer product storage and open their doors to families.

If you want to help, there are a lot of donation pages, and crowdfunding campaigns to support the communities impacted. The California Community Foundation has set up a Wildfire Relief Fund that you can donate to.

This GoFundMe campaign is called Farmers Helping Farmers and still needs a lot of funding to reach their goal. Check out their updates section to see how they are helping cultivators in real time. This Leafly page is also a very useful guide for how you can donate supplies, volunteer and help those impacted the fires.

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

We use tracking pixels that set your arrival time at our website, this is used as part of our anti-spam and security measures. Disabling this tracking pixel would disable some of our security measures, and is therefore considered necessary for the safe operation of the website. This tracking pixel is cleared from your system when you delete files in your history.

We also use cookies to store your preferences regarding the setting of 3rd Party Cookies.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.

Since the onset of the global health crisis, the cyber liability landscape has nearly spun into a death spiral. In other words, cybercriminals sat on the edge of their seats during the pandemic, waiting to pounce on anything that looked slightly vulnerable. Remote workers, small businesses, and emerging industries were hard-hit.

Since the onset of the global health crisis, the cyber liability landscape has nearly spun into a death spiral. In other words, cybercriminals sat on the edge of their seats during the pandemic, waiting to pounce on anything that looked slightly vulnerable. Remote workers, small businesses, and emerging industries were hard-hit.