Village Farms International (NASDAQ: VFF) manages and operates greenhouse facilities in North America. They’ve worked with growers for over 30 years and started supporting cannabis growers in 2017. The company was founded by Michael A. DeGiglio and Albert W. Vanzeyst in 1987 and is headquartered in Delta, Canada. But is Village Farms stock a strong buy?

What is Village Farms International?

Village Farms International has a long history of managing and operating energy efficient grow facilities for agricultural crops. This includes cannabis, recently, and vegetables which bring in over $200 million in revenue annually.

Their 2021 acquisition of Pure SunFarms, one of Canada’s best known cannabis brands, gave them around $17 million in extra revenue and a large opportunity in the flower competition in Canada. Current goals have them taking 20% of the flower market share. They also deal in vapes, oils and infused edibles.

Bottom Line: Is Village Farms Stock a Strong Buy?

Village Farms stock shows plenty of promise. They have a large footprint in Texas as well, supporting hemp cultivation and processing into CBD products for distribution in the USA. With a small stake in Altum International, they also have a presence in Asia.

Excitingly, their subsidiary Balanced Health Botanicals, has come out with their Synergy Collections of SKUs (cannabinoids such as CBDA, CBG, and CBG with non-hallucinogenic mushrooms and Kava roots). These products will come as tinctures, capsules and drinks (around 31 SKUs pending) and should diversify their product offerings even more.

Their revenue remains strong, with adjusted EBITDA up 49% YoY and Pure SunFarms reporting 12 straight quarters of positive adjusted EBITDA. They have a lot of cash and are paying off their debt and recent acquisition costs quickly. With really low P/S, Price/Book and EV/Revenue ratios (all under 4) we see a bargain price now for a company that should slowly grow for the next six quarters.

Village Farms stock presents a longer buy and hold opportunity but the recent price drop (37% in 1 year?!) is making much more of an enticing deal now.

For all these reasons we rate VFF as Strong.

83% of Cannin’s fundamentals prove true within 30 days or less on 100+ recommendations over the past 3 years.

On October 14, Canopy Growth announced their plans to acquire Wana Brands, the number one cannabis edibles brand based on market share in North America. The two companies entered into an agreement that gives Canopy the right to acquire 100% of the membership interests of Wana Brands (a call option to acquire 100% of each Wana entity) once a “triggering event,” such as when plant-touching companies begin trading on major US stock exchanges or full federal legalization, occurs.

As part of the agreement, Canopy Growth makes an upfront payment of $297.5 million to Wana Brands. Until the United States moves on cannabis legalization or companies can start trading on U.S. exchanges and Canopy uses the call option to acquire Wana Brands, they don’t get any voting or economic interest in Wana Brands. The two companies are essentially operating completely independently of each other until the US legalizes cannabis.

Nancy Whiteman co-founded Wana Brands in 2010 and since then the company has expanded significantly. Following the legalization of adult-use cannabis in Colorado, their sales skyrocketed. Over the next few years, Whiteman oversaw the company’s expansion into a number of new states. In 2016, they moved into Oregon’s market and quickly grew their brand presence, seemingly overnight. Then they expanded into Nevada, Arizona and Illinois in 2017. After that the company made a major East Coast push, expanding into Maryland, Florida and Massachusetts, with other major northeast markets expected to be added soon. The brand now has products available in twelve US states and nine Canadian provinces, with plans to add four additional states by the end of the year.

Nancy Whiteman, CEO & Co-Founder of Wana Brands

Shortly after the announcement, we sat down together over coffee in Las Vegas to discuss Whiteman’s journey to success, her plans for the company’s expansion and what the future might hold for Wana Brands.

Aaron G. Biros: First of all, congratulations on the acquisition. As a co-founder and CEO, it must be amazing to see the success of your company and all you’ve accomplished. How do you feel?

Nancy Whiteman: I feel ecstatic. I am so excited and so proud of what Wana has accomplished. Just all around a great feeling.

Biros: What was it like leading up to this moment? From the inception of the business, did you ever have any doubts you’d make it this far?

Whiteman: A thousand times. Absolutely. Anyone in cannabis that tells you they didn’t have any doubts is probably not being very honest. I had been thinking about partnership for a while. I felt the timing was right because of a variety of reasons, but also the possibility of federal legalization. I wanted to make sure that Wana was really going to be well positioned for future growth. One of the things that I said in our employee meeting – I quoted the old proverb of ‘If you want to go fast, go alone, but if you want to go far, go together.’ We’ve been going it alone for eleven years and we’ve gone very fast. But I want Wana to continue to be a major player in the industry and to go far. I really felt that this was the time in the industry to strike a partnership.

So that’s a little bit of the thinking behind it. I think when there is federal legalization, there is going to be a host of competitors entering the industry that are going to be unlike anything we’ve faced before. I think it’s going to be challenging for independent brands to scale as rapidly as they’re going to need to scale to compete against all of this new competition on their own. So that’s the why behind the timing of it.

In terms of why Canopy, I’ve known Canopy for quite a while. I met them when we were looking for partners about three and a half years ago. We did not end up putting together a deal at that point in time, but I did get to know the company quite a bit. Since then that company has changed significantly with leadership changes and became a very different company with the Constellation Brands investment behind them.

When I think about the future of the industry and particularly post-legalization, I have certain things that I am looking for in partners. Of course, I am looking for financial strength in a partner. I was really looking for a company that has a very long-term perspective on the industry, with both the proper resources and the proper mindset to make long-term investments for the future. And then my belief is that post-legalization, we’re going to see radical changes in the industry including where products are cultivated in a global market, more distribution outside of dispensaries – and I think liquor stores could be a likely form of distribution at some point in time, so the relationship with Constellation was very interesting and appealing to me. But all of those things wouldn’t mean as much to me if I didn’t feel we didn’t have a good fit in terms of our shared values and how we saw the industry. We spent a lot of time talking about that and I think one of the aspects that really attracted me to Canopy was that we are very aligned on how we see the future of the industry shaping up. Certainly, I think there is a wonderfully viable position for cannabis as an alcohol replacement, however we also have a lot of focus on innovation and the health and wellness aspects of cannabis. I was really looking for a partner that felt the same, and it ended up that we really were aligned on those values.

Biros: What does it look like going forward? Since you’re staying on board, how will your new role change?

Whiteman: My new role doesn’t change at all actually. I woke up last Monday—the week after the big announcement–and it felt very normal getting back to work and having my usual meetings. This was my fifteen minutes of fame and thankfully its diminishing so now it’s just back to work as usual.

But moving forward, we have big plans. Wana is launching in four new markets over the next couple of months, we’re in discussions to launch in an additional six markets, and we have very robust innovation pipeline. So, we’re just really busy right now just executing on our strategy. I am looking forward to getting to know our new colleagues at Canopy better and exploring different collaboration possibilities.

I feel very optimistic. I was thrilled our employees were delighted with the news and morale is very high. The feedback from the rest of the industry has been really positive and overall, I am feeling very good about this decision.

Biros: So you mentioned some expansion plans for four new markets in the next few months. How does the acquisition help Wana Brands expand?

Whiteman: You know we haven’t announced the new states so I can’t speak to those publicly yet. They were all in the works before this deal and are currently in the process of being onboarded. Where it will get interesting is how this deal impacts new states that we move into. Until Canopy decides to exercise the call option [to acquire 100% of membership interests in each Wana entity], we are still an independently owned and run company. So we are still going to be looking for the best partners that we can find in new markets, and the Canopy connection will certainly be helpful to us. But to your point about the plans, we’ll be announcing those new market expansions in the coming weeks.

Biros: As a woman leader with an extremely significant position in the cannabis industry, do you have any advice for young aspiring entrepreneurs, women leaders or other women in the cannabis space?

Whiteman: I do. I posted something on LinkedIn the other day and I’m going to make the same comment to you as I made in that post because I think it’s important and particularly important for young women. People have said a lot of nice things about me in the past couple of weeks and of course everybody loves to hear nice things about themselves. But the truth is, some of them are not true. And one of them that is definitely not true is that I am somehow fearless. And I guess what I would say to women and young entrepreneurs is that fearlessness is a myth.

Being an entrepreneur is hard. You’re putting your money on the line, you’re putting your time on the line, you’re putting your reputation, you’re potentially putting your family’s, your friends’ and your investors’ money on the line. Who would not be afraid against that backdrop? We all have times of feeling fearful, of feeling anxious, of having sleepless nights. So, what I would say is don’t aspire to be fearless. There are other aspirations that are much more useful. For example, aspire to be resilient, aspire to be persistent, aspire to be of service to other people, aspire to be very true to your values and your strategy. Don’t let this mythology of what a “leader” is supposed to look like make you feel bad about your emotions. It’s not about having those emotions, it’s what you do with them.

That’s what I would say to young entrepreneurs and especially to women. Because I do believe that women hold themselves to a very high standard a lot of the time and have a lot of misconceptions of what they’re supposed to be living up to when it comes to leadership.

Biros: What an incredible perspective to have. Okay, one last question for you: what are you doing to celebrate?

Whiteman: So far, I’ve been too busy to celebrate! This just happened so recently. I would like to take a great trip with my kids. I don’t really know I have not had time to figure that out. People tell me I need to go to Disney. But right now, it’s still taking a little while to let it all sink in.

Biros: Wonderful! And Nancy, thank you so much for your time I really appreciate it.

Whiteman: And thank you! So nice to see you in person.

Flower continues to be the dominant product category in US cannabis sales. In this “Flower-Side Chats” series of articles, Aaron Green interviews integrated cannabis companies and flower brands that are bringing unique business models to the industry. Particular attention is focused on how these businesses navigate a rapidly changing landscape of regulatory, supply chain and consumer demand.

Audacious (OCTQB: AUSA) is an Aurora (TSX: ACB) spinoff formerly known as Australis Capital, Inc. They have focused on an asset-light expansion strategy whereby they leverage their expertise in designing cannabis facilities in exchange for favorable cost plus arrangements for a percentage of the facilities’ production.

We interviewed Marc Lakmaaker, SVP of Capital Markets at Audacious. Prior to joining Audacious, Marc worked with Terry Booth at Aurora. His background is in investor relations.

Aaron Green: Marc, how did you get involved in the cannabis industry?

Marc Lakmaaker: I was working for an investor relations agency. and one of my colleagues left and she had a cannabis client that I took over, which was Bedrocan, Canada. I started working with them. They were then acquired by Tweed, which became Canopy. The guy I was working with at the time at Bedrocan was Cam Battley, who then went to Aurora. As soon as he joined Aurora, he said, “I need some help.” So, I came in house and worked there until July 2019. When I left, I set up my own agency, but by that time, I’d been working with Terry Booth for a few years. Then, this past December, Terry got in touch with me and said he needed my help. It was after the concerned shareholders had won the shareholder battle around Australis and the rest is history. So, I’ve now been working with Audacious, which was Australis, since December of last year, roughly.

Green: Just quickly on Australis: So, Audacious is basically a spin off of Aurora, correct?

Lakmaaker: Correct. So, at the time, Aurora had a couple of US assets on its balance sheet, a piece of land an annuity through a company Michigan. We were listed on the TSX. We were going to list or had just listed on the NYSE and were arranging for loan facility with a syndicate of banks. They said, “even though these assets are dormant, you can’t have any US assets on your balance sheet.” So, we spun Australis off – a little bit how Canopy had spun off Canopy Rivers. But it was really the idea that Australis is going to become the foothold for Aurora in the US cannabis market because Aurora has back-in rights.

The management team was put in place and started making some investments in the cannabis space, but kind of drifted away, sort of more into FinTech. First, it was FinTech related to cannabis and then FinTech, full stop. That’s when the shareholders were like, “we don’t agree with this.” Then the proxy battle started in which the dissident shareholders, or the concerned shareholders, won overwhelmingly. The Board left. The management team left. A new management team was put in place, a new Board in place, and it was kind of a restart.

So, we feel like we’re a bit of a startup. But a very rapidly moving startup. We’ve done an incredible amount of work in just the last seven to ten months. There was a lot of housekeeping to do. A lot of stuff related to restructuring the company, dealing with the departing management teams, dealing with bringing new management, etc. There were some deals that had to be unwound… Housekeeping if you will.

Green: Australis went down the FinTech route. What are the plans for Audacious now?

Lakmaaker: We’ve already started. We pivoted right away. In early January, we announced two acquisitions. One of ALPS, and the other one of Green Therapeutics. ALPS is really what is enabling us to execute on our strategy. It’s a very different strategy. It’s an asset light model, because we figured out that in order to grow quickly in this market without spending huge amounts of shareholder money, you need to be able to get into markets in a capital-light fashion. ALPS is the world’s preeminent greenhouse design company. Not just greenhouses, but also indoor facilities. They’ve got a 35-year track record in fruits and vegetables. They’ve got an eight-year-plus track record in cannabis – and built some of the best facilities in the world. They’ve got a lot of IP.

Marc Lakmaaker, SVP of Capital Markets at Audacious (formerly Australis)

The proof point of that is our relationship with Belle Fleur. It’s a social equity license holder in Massachusetts. We helped them build their facility. We’re not contractors, but we do the design and engineering. We help them with partner selection. We do the construction management. We bring in a general contractor. Then we do the commissioning, and optionally, post-commissioning services, making sure that the facilities are dialed in. In return for all that IP, because what people know that what they get at the end of it is high quality, consistent cannabis and very low operating costs, we ask our clients to dedicate a certain percentage of their canopies to grow with our cultivars. Those we will buy back on a cost plus arrangement and we use that to launch our brands into whatever jurisdiction.

So, in Massachusetts, we’re working with Belle Fleur. We’re getting 10% of their canopy. We’re buying it back at cost plus 5%. So, we don’t have to sink money into building the facility. We’re not carrying the cost of capital there. We’re also not paying wholesale prices. And these relationships are locked in for a long time. I can’t remember if it was five or 10 years. So, it’s a very, it’s a different strategy, but it’s not contrarian – it’s very de-risked, that allows us to launch into new countries.

Then for Green Therapeutics, we’ve got a number of award-winning brands like Provisions and Tsunami. We’re kind of phasing out GT Flowers and there will be something else in its place. We also acquired Loose, which caters to a younger demographic, with a high potency shot beverage line that is now for sale in California.

We also have a partnership with PBR, the Professional Bull Riders Association. There’s some statistics around that that just absolutely blew me away – 83 million permanent fans! That’s 25% of the US population. I think the average income is $70,000. That’s well above the national average and the general split is fairly even too; it’s 53/47, male/female. Proper American sport! They have hundreds of hours of exposure on CBS. They’ve got 2 billion imprints on social media. So, with PBR, we launched Wreck Relief, which has several recognized and approved pain products in the lineup.

Green: What markets are you in right now?

Lakmaaker: Right now we’re in Nevada with cannabis products. This is our home market where our head offices are in Las Vegas. We’re in California. We just bought a dispensary in San Jose that comes with a partnership with Eaze. On top of that, we’re operationalizing in Missouri and Oklahoma, and officially building in Massachusetts.

Then through ALPS because they does both cannabis and non-cannabis, we’re in a number of states. We’re looking to get more of the supply deals. We’re also doing a lot of vegetable facilities throughout the entire world. We’re in Europe, we’re in Asia, in the Middle and in North America, we build these facilities from the desert up to the Arctic.

There’s a big movement right now to produce food that is safe and has a smaller carbon footprint. So, our facilities are kind of inherently more sustainable. They use up to 95% less water, less labor, less energy, they are less prone to disease, crop failure, everything. And because you are local producing for local communities, you reduce the transport carbon footprint.

Green: What in your personal life or in cannabis are you most interested in learning about?

Lakmaaker: I really like the sciences. I’m a chemical engineer by training. I think what is going to take an incredible flight in the years to come is the application of medical scientific research that’s being done right now. To me, that’s fascinating because the cannabis plant is something special. It’s got such a broad utility that we know, anecdotally. I think we’re moving towards a world where we’re going to see a lot of breakthroughs on the medical side.

I’m very excited about the other end too – cultivation. I think tissue culture is going to play an incredible and important role.

Three years ago, Canada became one of the first countries in the world to legalize and regulate cannabis. We’ve covered various aspects of cannabis regulation since, but now with a few years of data readily available, it’s time to step back and assess: what can we learn from three years of cannabis recalls in the world’s largest legal market?

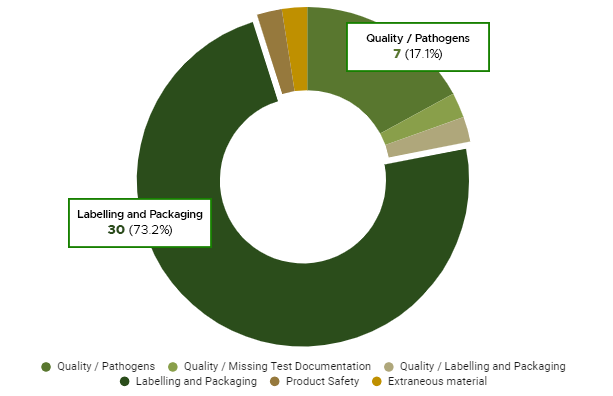

Labelling Errors are the Leading Cause of Canadian Cannabis Recalls

Our analysis of Health Canada’s data revealed a clear leader: most cannabis recalls since legalization in October 2018 have been due to labelling and packaging errors. In fact, over three quarters of total cannabis recalls were issued for this reason, covering more than 140,000 units of recalled product.

The most common source of labelling and packaging recalls in the cannabis industry (more than half) is inaccurate cannabinoid information. Peace Naturals Project’s recall of Spinach Blue Dream dried cannabis pre-rolls this year is a good example. Not only did the packaging incorrectly read that the product contained CBD, but the THC quantity listed was lower than the actual amount of THC in the product. The recall covered over 13,000 units from a single lot sold over 10 weeks.

In another example, a minor error made a huge impact. British Columbia-based We Grow BC Ltd. experienced this firsthand when it misplaced the decimal points in its cannabinoid content. The recalled products displayed the total THC and CBD values as 20.50 mg/g and 0.06 mg/g, respectively, when the products contained 205.0 mg/g and 0.6 mg/g.

Accurate potency details are not just crucial for compliance. For many customers, potency is a deciding factor when selecting a cannabis product, and this is especially important for medicinal users (including children), people who are sensitive to certain cannabinoids and consumers looking for non-psychoactive effects. In this case, at least six consumer complaints were submitted to Peace Naturals Project, the highest number for any cannabis recall in Canada.

Pathogens are the #2 Cause of Cannabis Recalls in Canada

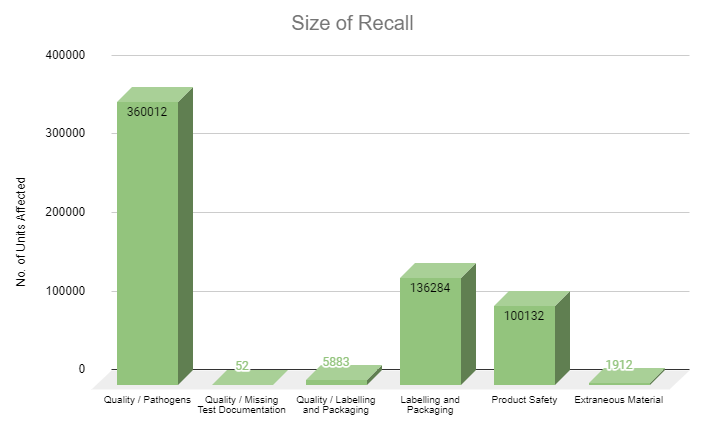

Pathogens are the second most common cause of recalls in Canada, claiming 18% of total cannabis recall incidents. And while that doesn’t sound like much compared to the recalls caused by labelling errors, it affects the highest volume of product recalled with over 360,000 units affected.

Canadian Cannabis Recalls – Total number of affected units and noted causes

A primary cause of allergens and microbiological contamination of cannabis products is yeast, mold and bacteria found on cannabis flower (chemical contaminants like pesticides can also be a major concern). Companies like Atlas Growers, Natural MedCo and Agro-Greens Natural Products have all learned this lesson through costly recalls.

These allergenic contaminants pose an obvious health risk, often leading to reactions such as wheezing, sneezing and itchy eyes. For people using cannabis for medical conditions and may be more susceptible to illness, pathogens can cause more serious health complications. Moreover, this type of cannabis recall not only drives significant cost since microbiological contamination of flower could easily affect several product batches processed in the same facility and/or trigger downstream recalls, but also affect consumer confidence for established cannabis brands.

Preventive control plan requirements for cannabis manufacturers mandate that holders of a license for processing that produce edible cannabis or cannabis extracts in Canada must identify and analyze the biological, chemical and physical hazards that present a risk of contamination to the cannabis or anything that would be used as an ingredient in the production of the edible cannabis or cannabis extract. Biological hazards can come from a number of sources, including:

Incoming ingredients, including raw materials

Cross-contamination in the processing or storage environment

Employees

Cannabis extract, edible cannabis and ingredient contact surfaces

Air

Water

Insects and rodents

To mitigate risks, addressing root causes with preventative measures and controls is essential. For instance, high humidity levels and honeydew secreted by insects are common causes of mold on cannabis flowers. Measures such as leaving a reasonable distance between plants, using climate-controlled areas to dry flowers, applying antifungal agents and conducting regular tests are necessary to combat such incidents.

Preventative measures and controls can save a business from extremely costly recalls.

Of course, placing all the necessary controls into action is not as simple as it may sound. Multiple facilities and a wide range of products in production mean more complexity for cannabis producers and processors. Any gaps in processing flower, extracts or edibles can result in an uncontrolled safety hazard that may lead to a costly cannabis recall.

These challenges are not just limited to cannabis growers. The food industry has been effectively mitigating the risk of biological hazards for decades with the help of food ERP solutions.

Avoid Recalls Altogether with Advanced ERP Technology

An effective preventative control plan with regular quality checks, internal audits and standardized testing is important to minimize the threats evident from Canada’s recall data. If these measures ever fail, real-time traceability systems play a pivotal role in the event of a cannabis recall by enabling manufacturers to trace back incidents to the exact point of contamination and identify affected products with surgical precision.

Instead of starting from zero, savvy cannabis industry leaders turn to the proven solutions from the food industry and take advantage of data-driven, automated systems that deliver the reliability and safety that the growing industry needs. From automated label generation to integrated lab testing to quality checks to precision traceability and advanced reporting, production and quality control systems are keys to success for the years ahead.

The edible cannabis market in Canada is still green. Delayed by a year from the legalization of dried flower, the edibles and extracts market poses significant opportunities for manufacturers. Edibles and extracts typically have higher profit margins than dried flower (“value-added” products) and consumer demand appears to be high and rising. So, what is causing trouble for cannabis companies trying to break into edibles and extracts? Below are four observations on the market potential of edibles in Canada.

Canada’s Edibles Market: The Numbers

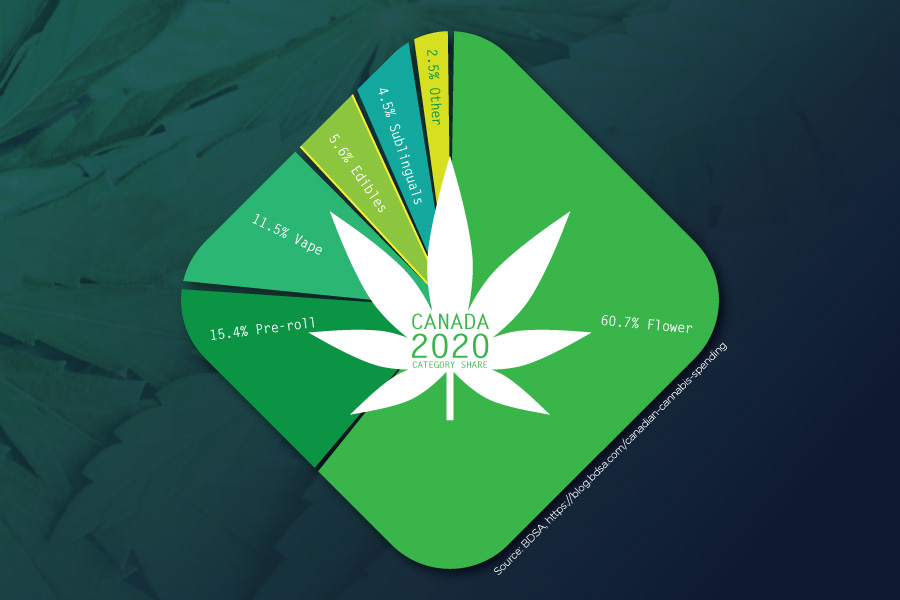

In 2020, Canada – the largest national market in the world for cannabis products – grew more than 60%, largely as a result of the introduction of new products introduced in late 2019, often called “Cannabis 2.0,” which allowed the sale of derivative products like edibles. Deloitte estimates that the Canadian market for edibles and alternative cannabis products is worth $2.7 billion, with about half of that amount taken up by edibles and the rest distributed amongst cannabis-infused beverages, topicals, concentrates, tinctures and capsules. More recently, BDSA forecasts the size of the Canadian edibles market to triple in size by 2025 to about 8% of the total cannabis dollar sales.

Source: BDSA

In December 2020, the Government of Canada reported that edibles made up 20% of total cannabis sales; Statistics Canada data shows that 41.4% of Canadians who reported using cannabis in 2020 consumed edibles. While sales have gone up and down over the course of the COVID-19 pandemic, there are clear indications that there is a substantial demand for edibles and extract products, which can be consumed more discreetly, with greater dosage precision and with fewer adverse effects (as opposed to smoking).

While sales of regulated edibles products continue to grow, edibles, extracts and topicals sales in Canada are facing a similar problem as dried flower sales: inventory growth is outpacing sales. Unsold stock sitting in inventory is growing at a dramatic pace, showing a clear lag in demand for these products on the legal market. How do we understand this contradiction?

1) Complex Regulatory Standards are a Major Barrier

Cannabis edibles compound the already existing problems around the conceptualization of cannabis products regulation. How should it work? Edibles can be considered in any of the following categories:

Cannabis as a pharmaceutical with medical application. Requires strict dosage and packaging requirements;

CBD as a nutraceutical with health benefits claimed. Requires specific nutraceutical regulations be followed;

Food product to be consumed. Must comply with food safety regulations around biological, chemical, physical hazards through a risk-based preventive control program. A full supply chain and ready-to-recall based system of regulatory standards need to be followed.

Incorporating elements from each of these three regulatory regimes into a single regulatory standards body is a confusing logistical and compliance challenge for both the regulators, and the producers and retailers of the product.

In mid-2019, the Government of Canada released the Good Production Practices Guide for Cannabis. This merged cannabis-specific regulations with food safety-specific regulations. Rigorous food safety requirements were combined with equally rigorous cannabis production and processing requirements, resulting in extremely laborious, detailed and specific regulations. These span everything from building design and maintenance, to pest control, to employee sanitation, to traceability – at all levels of the process. Navigating these regulations is a challenge, especially for many smaller producers who lack the necessary resources, like automation technology, to devote to understanding and tracking compliance.

2) Low Dosage Regulations Give an Edge to the Illicit Market

When edibles were legalized, THC dosage was capped at 10mg per package. For more experienced consumers, especially those who are dealing with chronic pain and other medical needs, this limit is far too low – and the unregulated market is more than able to fill this gap. One analyst from Brightfield pointed out that the dosage restriction, in combination with other regulations, will make it harder for the edibles market to grow in Canada.

It also makes the unregulated market almost impossible to beat. Barely more than half of cannabis consumers in Canada buy exclusively from government-licensed retailers, while 20% say that they will only buy unregulated products. According to a Deloitte report, 32% of legacy cannabis consumers said that unregulated products were better quality, and 21% reported that they preferred unlicensed products because there were more options available. Almost half of respondents also reported that quality was the biggest factor that would cause them to switch to regulated sources, and 28% said that higher THC content would prompt them to switch.

3) There is a Big Price Disparity between Legal and Illicit Edibles

As a result of dosage requirements and other factors, price per gram of regulated edible product is much higher than that of flower, unregulated edibles and edibles available through regulated medical distributors.

If you take the BC Cannabis Store’s price for Peach Mango Chews as an example: a 2pc package is $5.99. Since the dosage limits at 10mg per package, that’s the equivalent of $0.60/mg or $600/gram. A quick Google search reveals that an easily available edible from a medical cannabis distributor contains 300mg of THC and sells for $19.00, a price of $63.00/gram.

That means that not only is 10mg too low a dose for many users to achieve the result they were looking for, but the dosage restriction also makes the products less attractive from both a nutrition and cost standpoint. Deloitte reportsthat higher prices is the reason that 76% of long-time cannabis consumers continued to purchase from unregulated sources. The regulated industry as a whole is missing its legal market opportunity, where consumers prefer a lower price product with a greater range of dosage availability.

4) The Range of Products Available is Too Limited for Consumers

For most of 2020, chocolate edibles were the dominant product in this category in the Canadian market, garnering 65% of all edibles sales. But is this reflective of consumer wants? Despite a demand for other kinds of edibles like the ever-popular gummies, there are still only a few edible brands that offer the range of products consumers are asking for. According to research from Headset, there are 12 manufacturers in Canada making edibles but only two of them produce gummies. In comparison, 187 brands make gummies in the United States.

While some of this delay is likely due to the long licensing process in Canada and the newness of the market, there are other factors that make it challenging to bring a variety of products to market. The province of Quebec, Canada’s second-largest province, has banned the sale of edibles that resemble candies, confections, or desserts that could be attractive to children – giving yet another edge to unregulated sellers who can also capitalize on illegal marketing that copies from existing candy brands like Maynard’s.

When companies do want to introduce new products or advertise improvements to existing product lines, they are restricted by stringent requirements for packaging and marketing, making it harder to raise brand awareness for their products in both the legal and unregulated markets. Industry players are also complaining about government restrictions on consumers taste-testing products, which further compounds challenges of getting the right products to market.

In the meantime, illicit producers have also shown themselves to be savvy in their strategies to capture consumers. It is not uncommon to find illicit products packaged in extremely convincing counterfeit packaging complete with fake excise stamps. New consumers may assume the product they are purchasing is legal. Availability of delivery options for higher dosage, lower price illicit products is also widespread. All of this adds up to significant competition, even if it were easier to meet regulatory requirements.

Conclusion: Significant Room for Growth Remains Limited by Government Regulations

These four challenges are significant, but there are a number of opportunities that present themselves alongside them. A year and a half into the legalization of edibles, cannabis companies are getting a better picture of what Canadian consumers want and low dosages are proving to be desirable for Canadian consumers in some areas.

Some of the many infused products on the market today

In particular, sales of cannabinoid-infused beverages far outpaced other edibles categories last year, likely tied to the availability of these products in stores over the summer of 2020. BDSA’s research has shown that, in contrast with American consumers, the lower THC dosage for cannabis beverages is an advantage for Canadian consumers. Major alcohol brands like Molson Coors and Constellation Brands are investing heavily in this growing product area – though there the dosage limits also apply to how many products a consumer can buy at a time.

At the same time, the large quantity of unsold cannabis flower sitting in storage also poses an opportunity. While its quality as a smokeable product may have degraded, this biomass can be repurposed into extracts and edibles. Health Canada has also shown some responsiveness to industry needs when it shifted its stance to allow for Modified Atmosphere Packaging (MAP), which will help improve shelf life of products.

While strict regulatory obstacles remain, challenges will continue to outweigh opportunities and the illicit market will remain a strong player in the edibles market. As regulations become clearer and producers become more accustomed to navigating the legal space, barriers to entry into the regulated cannabis market and specifically the extracts and edibles market, will decrease. Meanwhile, those getting into the edibles market will do well to be wary of the challenges ahead.

As the cannabis industry — now estimated to be worth more than USD 200 billion — continues to erupt around the world, Europe is about to take off.

This draws a parallel with the watershed legislative events of November 2012, when Colorado Amendment 64 and Washington Initiative 502 were implemented. These two bills kicked off a wave of medical and adult use acceptance in the United States. Europe’s medical referendums which started in 2017-2018 and the recent December 2020 United Nations acceptance of medical attributes of cannabis will do the same in that continental marketplace. Europe is following science and studying popular opinion about cannabis, just like the United States nearly a decade ago.

In many ways, the American “medical” market has been a political ploy, while the European market is truly medical in every way. Distribution through pharmacies and mainstream channels is the wave of the future. This method of distribution will both increase access and taxable bases quicker than the U.S. “medical” dispensary model. People who truly need cannabis should not be hindered by any rules or regulations to get the medicine, and the U.N. has paved the way for access while the U.S. still awaits rescheduling.

Markets in Europe require EU-GMP manufacturing for a variety of different products

The road to medical cannabis in Europe is more stringent than that of the U.S. and Canada. This is because most European markets have strict medical standards and medicines must be produced in European Union Good Manufacturing Practices (EU GMP) certified pharmaceutical manufacturing facilities. This is the same standard that all medical Active Pharmaceutical Ingredient (API) producers are held to.

Both Canadian companies, who have just launched extraction with Canada’s “Cannabis 2.0”, and American manufacturers alike are unfamiliar with pharmaceutical API production. Some argue that food-grade GMP standards are the most similar to already-existing systems in the U.S. and Canada. However, the meaning of “medical” is clear in Europe — it means medical. Improving access for patients to products will be the central challenge for Europe over the next few years as patient growth increases.

Europe is also embracing its potential adult use markets. First came Denmark, then Luxembourg, and now the Netherlands are all beginning to engage with the question of adult use cannabis legalization. We expect Portugal will soon join this list. After all, in a post-coronavirus world, every country will be looking for a means to grapple with a devastated economy and to boost employment to widen its taxable base.

The United States was supposedly founded by Puritans escaping gregarious Europeans. Now it’s likely America will legalize cannabis within the year and Europeans will be left asking, “Why them and not us?” And it will become harder to explain why such potential for growth in employment and increased tax revenue isn’t being taken advantage of as Europe begins to emerge from lockdown. It would be shrewd to expect a wave of European adult use kick-offs in 2022.

It’s anyone’s guess what retail will look like for the cannabis market in Europe as it evolves

It is clear that 2021 is setting a blistering economic pace: from mergers and acquisitions to monster capital raises, to increased debt raises to the hot special purpose acquisition companies (SPACs) London Stock Exchange (LSE) up listings and initial public offering (IPO) fever. This year will be a cannabis-fueled explosion that Europe will not be able to ignore. With Canada, the U.S. and Mexico all likely to legalize cannabis in the near future, how long will it be before South and Central America follows suit? And then, how long for this wave to reach Europe?

The real answer is, it’s already here. Early adopters of cannabis overbuilt as the Canadians were given more money than they deserved, while the U.S. market was largely fueled by private equity and proved that it could be the biggest and best-run model. Europe will follow its own path by acknowledging the failures and successes of these markets, blending them to form its own unique European model.

The American dispensary will eventually pop up in Europe in a form similar to the current social clubs of Barcelona and coffee shops of Amsterdam. Possibly specialized pharmacies will carry more cannabis products, but it’s too early to call — countries are only just beginning to figure out how cannabis rules might be shaped to fit their needs and values.

2021 could be a decisive year for the European cannabis market

There are greater issues people are dealing with in the age of COVID-19, but that will change. Economic recovery, the need to provide medicine more quickly and affordably, social reform, green projects and many more pressing issues will become thematic of a post-COVID world; a set of themes for which a cannabis-shaped solution checks many of the necessary boxes.

There is a certain misrepresentation of cannabis as a panacea, able to cure every medical ailment and remedy every social problem if only it were legalized more broadly. While cannabis certainly is not a cure-all, it can fix many issues facing governments today. People were grateful for cannabis during these troubled times with cannabis stockpiling and usage through the roof in the early stages of the pandemic. As a result, 2021 has the potential to shatter old establishment perceptions as more consumers speak out.

Now, it is only a question of how the individual and collective European nations choose to regulate expansion across the continent. And the power to create a truly world-beating cannabis model is in their hands; without the international market differences and troubles that plague the North American sector, there will be virtually no limits to cannabis expansion throughout Europe if those in charge believe it to be so.

Charlotte’s Web Holdings, the company that just about launched the entire CBD industry, announced this week that they have just been approved for registration on Health Canada’s list of approved cultivars (LOAC) for 2021. Three of their proprietary hemp cultivars have made the cut, gaining the company access to the Canadian market.

Jared Stanley, co-founder and chief cultivation officer at Charlotte’s Web, says they plan to lead the market in Canadian hemp-derived CBD products. “The majority of approved cultivars on the LOAC to date have been for industrial hemp grown to produce food, fiber, and animal feed,” says Stanley. “Now our approved cultivars are paving the way for full-spectrum hemp CBD demand in Canada and most importantly, will provide access to Charlotte’s Web products in Canada.”

Largely due to the difference in regulatory approaches between Canada and the U.S., the CBD product market in Canada is somewhat small. Health Canada currently regulates CBD products the same as products containing more than 0.3% THC. In the U.S., a checkerboard of state laws, the 2018 Farm Bill and the subsequent state hemp programs led to massive growth for the CBD product marketplace.

Charlotte’s Web is one of the leading hemp-derived CBD companies operating in the United States. With the soon-to-be expansion into Canada, the company hopes to develop a global footprint, says Deanie Elsner, president and CEO of Charlotte’s Web. “Today, Charlotte’s Web is the leading hemp wellness company in the U.S. with the most recognized and trusted hemp CBD extract,” says Elsner. “We aspire to be the world’s leading botanicals wellness company, entering countries with an asset light model where federal laws permit hemp extracts for health and wellness. Israel and Canada are included in the first steps of our international expansion.”

This follows the launch of their first CBD-infused beverage line sold in the United States, Quatreau. In the initial phase of the agreement, Southern Glazer’s will distribute the beverage line in seven states, with plans to expand that footprint considerably in the coming months.

Being a national distributor with a strong presence throughout the country, Southern Glazer’s will be moving Canopy’s beverage line in conventional retail stores. The press release seems to credit Canopy’s partnership with Constellation Brands as the catalyst for the new distribution deal. “The agreement also showcases the benefits of the company’s strategic relationship with Constellation Brands, the global beverage leader,” reads the release.

Back in 2018, Constellation Brands made a $4 billion bet on Canopy, but immediate profitability did not come to fruition. This new deal with Southern Glazer’s, as well as the launch of the Quatreau beverage line, seems to prove Constellation’s bet is beginning to pay off, or at least showing signs of a long term play for market share.

The unusual nature of 2020 gave rise to a reciprocally roller-coaster-like cannabis market. Cannabis was cemented officially as an essential industry with the rise of COVID-19, and November elections resulted in even more United States markets welcoming medical and adult-use sales.

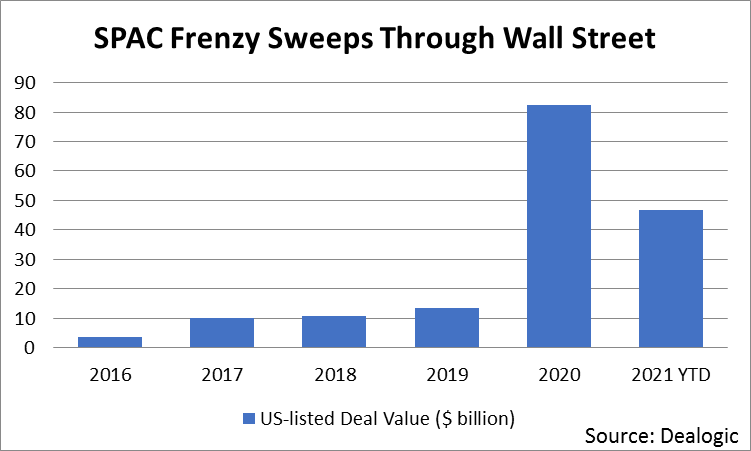

The stagnant cannabis stock market of 2019 became a thing of the past by the end of 2020. Throughout the course of last year, bag holders anxiously watched cannabis options creep back up. Now, nearly two years since market decline in 2019, the cannabis stock market is exploding with blank checks and buyout fever. Much of this expectant purchasing is due to Canadian companies considering U.S. market entrance. Combined with the recent surge in the use of special purpose acquisition companies (SPACs) to invest, this has led to an increase in asset prices.

A SPAC is defined as “a company with no commercial operations that is formed strictly to raise capital through an initial public offering (IPO) for the purpose of acquiring an existing company.” Though they have existed for decades, SPACs have become popular on Wall Street the last few years because they are a way for a company to go public without the associated headaches of preparing for a traditional IPO.

In a SPAC, investors interested in a specific industry pool their money together without knowledge of the company they’re starting. The SPAC then goes public as a shell company and begins acquiring other companies in the associated industry. Selling to a SPAC is usually an attractive option for owners of smaller companies built from private equity funds.

The U.S.-Canadian market questions that this rising practice asks are: Can Canadian companies enter a bigger market and be more successful? Is it advisable for U.S. companies to sell their assets to Canadian corporations whose records may be marred by a history of losses and a lack of proper corporate governance? Regardless — if both SPAC’s and Canadian bailout money is here, what comes next?

What is Driving this Bull Market?

Underpinning these movements are record cannabis sales internationally, making last year’s $15 billion dollars’ worth of sales in the U.S. look small in comparison. New markets have opened up in various states and countries throughout 2020, and that trend is only expected to continue. New demographics are opening up, especially among older age groups. This makes sense, as most cannabis sales — even in a recreational setting — are people treating something that ails them like insomnia or aches and pains.

Cannabis is set to take off, and we are entering only the second phase of its market expansion. The world is becoming competitive. Well-run companies that are profitable in key markets are prime targets for bigger, growing companies. At the same time, the world of SPACs will continue to drive valuations. Irrespective of buying assets, growing infrastructure is and will continue to be greatly needed.

The Elusive Profitability Factor

When Canada blew up, one of the biggest changes was companies began focusing the year on cost cutting and — most importantly — profitability. Profitability became the buzzword. But bigger companies are on the search for already-profitable enterprises, not just those that have the potential to be. However, profitability is currently still unobtainable in Canada. Reasonable forecasters should expect this year will show a few companies getting bailed out while many others will be forced to either merge for survival or declare bankruptcy.

An ideal company’s finances should highlight not only revenue growth, but also profitability. Attention should be focused on how well businesses are run, and not on how much money they have the potential to raise or spend. Over the years, there have been many prospective companies that spent hundreds of millions only to barely operate, and are now shells in litigation. Throwing money at any deal should have been a lesson learned in the past, but SPACs are tempting because they are trendily associated with new, interesting management styles and charismatic businesspeople.

Companies should be able to present perfect and clear financials along with maintenance logs for all equipment. In today’s day and age, books must be stellar and clean. As money pours into SPACs, asset valuations for all qualities of companies will rise. The focus instead becomes about asset plays, which will cause assets to continue rising as money is poured into SPACs.

Once upon a time, if number counters presented a negative review or had to dig too much, executives would turn a cold shoulder on investment. But in the age of SPACs, these standards of evaluation will be greatly undervalued. Aging equipment and reportability of every piece of equipment may or may not be properly serviced and recorded in a fast-moving market. Costs of repair or replacing equipment that isn’t properly maintained may be a problem of the past. Because when money comes fast, none care for the gritty details.

Issues for SPACs

Shortage of talent and training has become a big concern already in the era of SPACs. How many quality assets are out there? Big operators in the U.S. are content and don’t see Canada as an enticing market to enter. So, asset buys are likely to primarily be in the U.S. Large companies like Aphria may buy out some of the major American players, but most Canadian companies will use new funding rounds to pay down debts. Accordingly, they will then be forced to piece together smaller operators as a strategy.

A cannabis company’s personnel and office culture are very important when looking to integrate into a larger corporate culture. Remember, it’s not just the brick and mortar that is being invested into, it is also the people that run a facility. Maintaining employee retention when a deal occurs is always critical. Your personnel should be highly trained and professional if you want to exit. Easy to plug-in corporate structures make all the difference in immediately gaining from the sale or having to retool the shed and bring in all new people.

The rise of the SPAC-era and Canadian entry into the U.S. market will cause asset increases, but it is only the second chapter in the market expansion of cannabis. Proper buys will nail profitability, impeccable books, proper maintenance records and will have created an efficient corporate structure with talented personnel. The rest will be overpriced land buys that will require massive infrastructure spending. The basics of a well-run organization don’t change. The cannabis market is going to ROAR, but don’t worry if the SPACs pass you by- they are buying at the start of cannabis only.

It’s no secret that the rollout of cannabis legalization has underperformed in countries like Canada. Since legalization in October of 2018, industry experts have warned that the projections of the big cannabis firms and venture capitalists far exceeded the expected demand from the legal market.

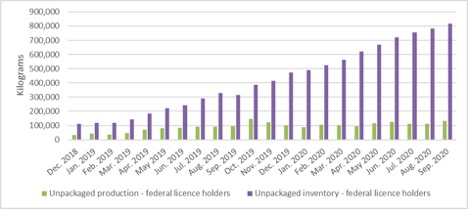

Today, major production facilities are closing down, some before they even opened, dried flower inventory is sitting on shelves in shocking quantities (and degrading in quality), and an extremely robust illicit market accounts for an estimated 80% of the estimated $8 billion Canadian cannabis industry. None of those things sound like reasons for optimism, but while some models for cannabis business are withering away, others are beginning to put down stronger roots. Crucially, we are beginning to see new business models emerge that will be able to compete against the robust black market in Canada.

The Legal Cannabis Industry Can’t Compete

Legal rollout in Canada could easily be described as chaotic, privileging larger firms with access to capital who were able to fulfil the rigid – and expensive – regulatory requirements for operating legally. But bigger in this case certainly did not mean better. The product these larger firms offered immediately following legalization was of a lower qualityand higher price than consumers would tolerate. In Ontario, cannabis being shipped to legal distributors lacks expiration dates, leaving retailers with no indication of what to sell first, and consumers stuck with a dry, poor quality product.

The majority of existing cannabis consumers across the country prefer the fresher, higher quality and generally lower priced product they can easily find on the illicit market. That preference couldn’t be clearer when you look at the growth of inventory, which is far outpacing sales, in the graph below:

Which brings us to the crux of the matter: when it comes to building up the Canadian cannabis industry, what will succeed against the black market that has decades of expertise and inventiveness behind it?

Rising From the Ashes: Craft Growers and Other Small-Scale Producers

The massive facilities like Canopy’s may be shutting down, but our friends over at Althing Consulting tell us that those millions of square feet facilities are being replaced by smaller, more boutique-style cultivation facilities in the 20,000 ft tier, which are looking to be the future of the industry.

Consumers have consistently shown a strong preference for craft cultivators and other small-scale producers who produce higher quality, more varied products that are more responsive to consumer needs. It also hasn’t hurt that prices are also coming down: Pure Sun Farms in Delta, BC is consistently selling out of their $100/ounce special, which is highly competitive even with the illicit market.

This vision of the industry matches up better with the picture we’ve been getting from other legalization projects around the world. It also squares with other indicators of success. Despite the small market capture of the legal market, industry employment numbers are still relatively high, especially when compared with more established legal consumer products markets such as beer. In fact, craft cannabis growers now employ nearly as many people as the popular craft brewing sector here in British Columbia.

But in order to make the craft cannabis market actually competitive in both the regulated and unregulated spaces, the government will have to address four major challenges.

Challenge #1: License Distribution is Uneven and Chaotic

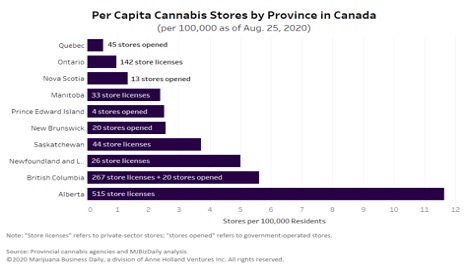

A December 2020 report by Ontario’s auditor general contains admissions by the Alcohol and Gaming Commission of Ontario (AGCO), Ontario’s cannabis industry regulator, that they lack the capacity and resources to manage the number of applications for private cannabis retailing. Problems relating to the issuing of licenses, including long delays and difficult requirements, are widespread across provinces. One way this becomes clear is by looking at the very uneven distribution of stores across the country in the graph below.

Challenge #2: Basic Regulatory Compliance is Complex and Time-Consuming

Smaller-scale micro cultivators, whose good quality craft product remains in high demand, still face prohibitive barriers to entry into the legal market. Licensing from Health Canada is one onerous challenge that everyone must tackle. Monthly reporting requirements have in excess of 477 compliance fields. Without additional support to navigate these requirements – including automation technology to ease the administrative burden – these smaller producers struggle to meet the minimum regulatory standards to compete in the legal market.

Challenge #3: A Long-Distance Road to Compliance and Safety Means Higher Costs

Even with all regulatory requirements satisfied, cannabis cultivators can’t sell their product from “farm to fork” (to borrow a phrase from the food industry). Many growers ship their product to be irradiated in order to ensure they are below the acceptable microbial threshold set by Health Canada. While irradiation positively impacts the safety of the product, new evidence shows that it may degrade quality by affecting the terpene profile of the plant. Furthermore, only a few facilities in Canada will irradiate cannabis products in the first place, meaning that companies have to ship the finished product sometimes thousands of kilometers to get their product to market.

Next year, Health Canada looks set to lower the limit on microbials, making it virtually impossible to avoid cannabis irradiation. If Health Canada follows through, the change will be a challenge for small-scale cultivators who strive to prioritize quality, cater to consumers who are increasingly becoming more educated about terpene profiles, and seek to minimize the environmental impact of production.

Challenge #4: It is Virtually Impossible to Market Improved Products

Finally, there is a marketing problem. Even though the regulated market has made dramatic improvements in terms of product quality from legalization two years ago, Health Canada’s stringent marketing restrictions means that cannabis producers are virtually unable to communicate these improvements to consumers. Cannabis producers have little to no opportunity to reach consumers directly, even at the point of sale – most legal sales are funneled through government-run physical and online stores.

What Can a Thriving, Legal Cannabis Market Look Like in Canada?

The good news is that change is being driven by cannabis growers. Groups like BC Craft Farmers Co-Op are pooling resources, helping each other navigate financial institutions still hostile to the cannabis trade, obtain licenses and organizing craft growers to advocate to the government for sensible regulatory changes. As a result of their advocacy, in October, the federal government initiated an accelerated review of the Cannabis Act’s restrictive regulations related to micro-class and nursery licenses.

Now, more co-op models are popping up. Businesses like BC Craft Supply are working to provide resources for licensing, quality assurance and distribution to craft growers as well. Indigenous growers are also showing us how cannabis regulation could work differently. Though Indigenous cultivators currently account for only 4% of Canadian federal cannabis licensees (19/459), that number looks to be growing, with 72 new site applications in process self-identified as Indigenous, including 27 micro cultivators. In September, Williams Lake First Nation entered into a government-to-government agreement with the province of British Columbia to grow and sell their own cannabis. The press release announcing the agreement includes the following statement:

“The agreement supports WLFN’s interests in operating retail cannabis stores that offer a diverse selection of cannabis products from licensed producers across Canada, as well as a cannabis production operation that offers farm-gate sales of its own craft cannabis products.”

More widespread adoption of the farm-gate model, which allows cultivators to sell their products at production sights like a winery or brewery, has a two-fold benefit: it better supports local, small-scale producers, and it offers opportunities in the canna-tourism sector. As the economy begins its recovery alongside vaccine rollouts and restrictions on travel ease, provincial governments will have the chance to leverage the reputation of unique regional cannabis offerings (i.e. BC bud) through these farm-gate operations.

While the cannabis legalization story in Canada has had its bumps, the clear path forward for greater legal market success lies in increased support for micro-cultivators. By increasing support for these small-scale producers to navigate regulatory requirements, more will be able to enter the legal market and actually compete against their illicit counterparts. The result will be higher quality and more diverse products for consumers across the country.

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

We use tracking pixels that set your arrival time at our website, this is used as part of our anti-spam and security measures. Disabling this tracking pixel would disable some of our security measures, and is therefore considered necessary for the safe operation of the website. This tracking pixel is cleared from your system when you delete files in your history.

We also use cookies to store your preferences regarding the setting of 3rd Party Cookies.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.

Village Farms International has a long history of managing and operating energy efficient grow facilities for agricultural crops. This includes cannabis, recently, and vegetables which bring in over $200 million in revenue annually.

Village Farms International has a long history of managing and operating energy efficient grow facilities for agricultural crops. This includes cannabis, recently, and vegetables which bring in over $200 million in revenue annually. Their revenue remains strong, with adjusted EBITDA up 49% YoY and Pure SunFarms reporting 12 straight quarters of positive adjusted EBITDA. They have a lot of cash and are paying off their debt and recent acquisition costs quickly. With really low P/S, Price/Book and EV/Revenue ratios (all under 4) we see a bargain price now for a company that should slowly grow for the next six quarters.

Their revenue remains strong, with adjusted EBITDA up 49% YoY and Pure SunFarms reporting 12 straight quarters of positive adjusted EBITDA. They have a lot of cash and are paying off their debt and recent acquisition costs quickly. With really low P/S, Price/Book and EV/Revenue ratios (all under 4) we see a bargain price now for a company that should slowly grow for the next six quarters.