Late last month, Mastercard decided to halt their debit card transactions with cannabis dispensaries, notifying financial institutions and payment processors to stop processing purchases. This isn’t the first digital payment solution to swiftly exit the industry – late last year, vendors turned off services to their cashless ATMs. These abrupt decisions have made major headlines, shocking cannabis dispensary owners, operators and consumers as they scramble to shift focus back to the remaining legal payment tools.

For the cannabis industry veterans like myself, these exits aren’t a surprise at all. Why? Cannabis is federally illegal and federal regulations restrict banks and other financial services companies from working with cannabis businesses – even if it is legal at a state level. Due to this massive legal hurdle, cannabis dispensaries often lack access to typical banking services and have limited payment options for consumers, making it challenging to manage and facilitate payments.

Some believe that this decision by Mastercard, the second largest payments provider in the world, and by other payment vendors, coupled with the political pressure to legalize cannabis could help push legalization or the Secure and Fair Enforcement (SAFE) Banking Act to help mitigate the lack of access to banking services in the longer term. Even though cannabis represents an economic opportunity – MJBizDailyestimates that combined medical and adult use cannabis sales could reach $33.6 billion by the end of 2023, and $53.5 billion by 2027 – hurdles to legalization mean that, for now, cash will be the most prevalent payments option.

Let’s Talk About Cash

Physical cash is difficult to manage for dispensaries

Cash remains the longstanding and most prevalent payment option in cannabis. However, it presents difficulties for businesses. Physical cash is difficult to manage for dispensaries for several reasons, primarily due to the costs to count, track and manage cash volumes and the labor required to count the cash. In fact, in most dispensaries, associates count cash an average of six times a day. Each time cash is manually counted, dispensaries risk miscounts, shrinkage, security and safety concerns due to robberies.

This manual labor required to oversee a business’s balance sheet and keep dispensaries operating is inefficient and unsustainable, and many have attempted to incorporate debit payments or cashless ATM transactions to help mitigate the costs associated with cash. However, while cash presents logistical and operational challenges for dispensary owners, it remains one of the more dependable payment options consumers and dispensaries have for cannabis transactions. Dispensaries can integrate simple strategies to improve their cash handling and operate more efficiently.

Best practices with cash management for dispensaries

The biggest and most impactful strategy is incorporating cash automation tools to help secure, count and manage their payments. The largest and oldest dispensary in Washington D.C. incorporated sophisticated automation tools into their cash handling practices, which have alleviated massive headaches and burdens from store associates, managers and its accounting team, who previously relied on manual cash processes to count, sort and manage their cash.

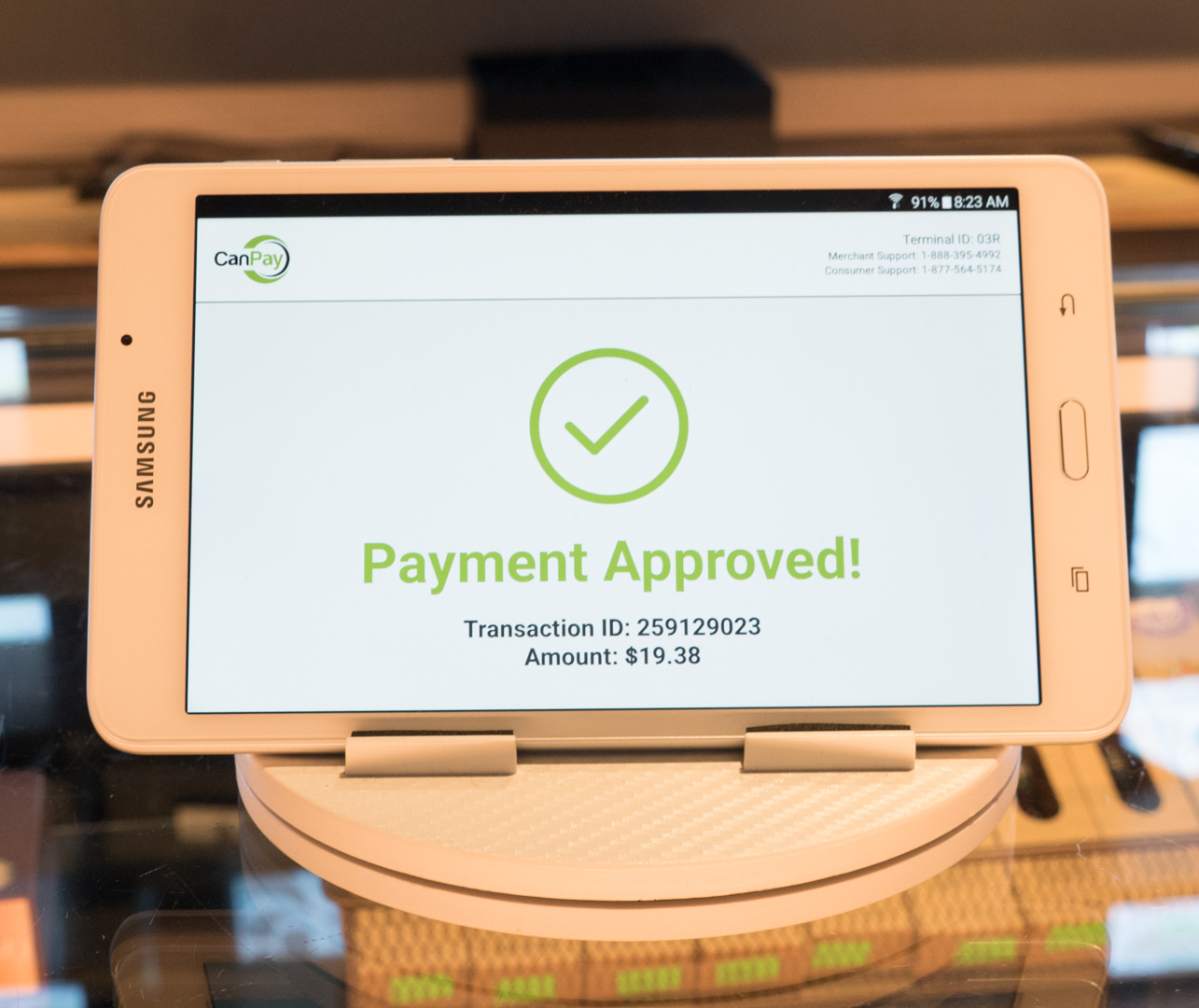

Mastercard halted debit card transactions with cannabis dispensaries just weeks ago

This cash-handling technology has improved count accuracy, saved time for staff, improved visibility and enabled real-time reporting. These tools have transformed the day-to-day duties of staff. The dispensary’s accounting team and associates no longer get overwhelmed when anticipating increased cash flow on 4/20 or other holidays because they have tools that eliminate the extreme costs of handling cash. Additionally, they now confidently support audits as they have complete reports of each transaction by user, date and time. Before automation, audits were next to impossible to execute confidently.

The greatest benefit of cash automation tools is the near elimination of shrinkage, a term referring to the cash lost due to employee theft or miscounts. With cash automation, cash is as affordable as digital payment options, with the added confidence that cash won’t disappear as a payment option for consumers.

Have a Cash Strategy

While Mastercard’s decision to leave the cannabis industry leaves dispensaries in the lurch, the cannabis payments ecosystem continues to evolve and transition quickly. Dispensaries must be agile and incorporate strategies for the payment options, both inbound from consumers and outbound to their vendors, that they can rely on.

As the cannabis industry continues to evolve, embracing cash automation will be crucial for sustainable growth and success. Cash automation is a transformative solution for cannabis reducing the cost of managing cash while addressing the unique challenges associated with high cash volume operations. Embracing cash automation allows dispensaries to thrive in an evolving industry while maintaining control over their cash ecosystem, no matter who enters or exits the payments space.

In the regulated cannabis sector, retail shrinkage is a concern as business owners must navigate tight regulations in an often cash-only environment combined with the usual causes of retail shrinkage, including theft and inefficient operations.

Retail shrinkage occurs when a company loses inventory from causes other than sales—and it’s a problem that costs companies $100 billion annually, according to the National Retail Federation’s (NRF) 2022 National Retail Security Survey (NRSS). The cannabis industry is not immune.

Utilizing Technology to Combat Retail Shrinkage

The 2022 survey estimates that 65% of inventory loss is due to theft, a trend that is expected to continue with the rising cost of goods. Other factors may include administrative and human error. Nearly half of the retail respondents reported an increase in technology spending to combat these threats.

In Q1 of 2023, Proteus 420, an online enterprise resource planning (ERP) system for highly regulated industries, including alcohol and cannabis, saw a substantial uptick in POS software requests, in part attributed to the need for additional automation and auditing tools in order to more easily and accurately monitor and control inventory.

Physical security measures can aid in loss prevention

In the cannabis industry, along with a challenging regulatory environment, retail businesses are facing declining sales. Loss prevention is where dispensaries can protect their bottom line with a targeted approach and the right system in place.

How can cannabis businesses do this? By avoiding antiquated spreadsheets and by having the ability to quickly analyze vast amounts of data. Business owners should be proactive and utilize technology, such as a quality ERP system, to mitigate risk and safeguard inventory.

When choosing a software provider, cannabis retailers should focus on systems that offer day-to-day support and emergency assistance, and systems that can seamlessly monitor employees, cash and inventory. Software, and employees who work with it, should also be able to track and trace compliance, identify suspicious transactions and look at data from multiple locations. Detailed reporting is crucial from a compliance perspective.

Loss Prevention Practices

Because cannabis is a heavy cash-only industry, having the right tools to monitor the physical cash as it moves through your business is necessary to prevent loss. This is done with cash drawer-specific transaction tracking, employee module access, and the ability to open and close drawers at the employee level.

Here are some of our top loss-prevention tips:

There should always be multiple eyes on cash and products. Managers and assistant managers should always verify counts of cash and products as a check and balance measure.

Make sure employee access to your POS or operational system is granulated. This means that different positions have varying levels of access and capabilities.

Have a solid inventory auditing process. To stay on top of this, make sure that your staff and system can do spot inventory audits and can track the audits long-term.

Have physical security measures in place. This can include security cameras and alarm systems and a dispensary designed to keep inventory strategically placed.

Build a workplace culture that empowers employees to feel ownership in their work and feel accountable for loss prevention in their This includes emphasizing the policies and procedures needed for loss prevention, including consequences for theft. This culture is not an overnight process but develops over time.

The Right Employees Make a Difference

The first line of defense against product or cash loss is your employees

In addition to the right technology and prevention practices, the first line of defense against product or cash loss is your employees. From your budtender to your general manager, you need to make sure the right people are in place in the correct positions for fair compensation.

Some questions you can ask yourself during the hiring process include:

Do they have the right experience for the position?

Are they motivated, flexible, detail-oriented, team players?

Are they passionate about cannabis and want a future in the industry?

Have you checked their references?

Things move fast in the cannabis sector – are they willing to learn new skills?

Once you have the right people, do they have the standard operating procedures (SOPs) needed to do their jobs? If not, it’s time to create them.

When it comes to loss-prevention, you must trust that your cannabis point-of-sale and operations ERP system will monitor and provide the needed reports. You can also make sure there are additional measures in place to prevent retail shrinkages, such as empowered employees and solid loss prevention practices so that your inventory and cash stay right where they belong until sold.

As the cannabis industry experiences a significant shift toward general acceptance and mainstream adoption, new modes of operation are popping up everywhere. The evolution and expansion of the industry beg for constant innovation, and the integration of NFTs and cryptocurrencies as payment options is at the crossroads between tech and cannabis.

Crypto and NFTs have grown in popularity in recent years. Non-fungible tokens are an interesting asset in the art and collectibles world, while cryptocurrency has made a name for itself by providing a unique kind of financial independence. More and more payment processors are embracing these new payment methods, and the cannabis industry is also slowly welcoming them.

In order to fully understand the cannabis-crypto connection, Swaroop Suri, founder of Melee Dose, a cannabis brand that’s been embracing NFTs and crypto as payment options, shared some insights. Their innovative approach to creating unique cannabis experiences with technology and creative branding makes them a pioneer of this movement.

What’s Happening with Cannabis and NFTs?

NFTs and cryptocurrency are exciting developments in an industry that carries the reputation for having a rocky relationship with the banking industry. The legal gray area surrounding the connection between cannabis businesses and the banking industry has given way to an onslaught of challenges, with many banks shunning cannabis because of its federally illegal status. While traditional banking can limit cannabis companies’ access to basic financial services, the decentralization that’s characteristic of blockchain opens up many doors.

In recent years, different brands have tested the waters by using cryptocurrencies and NFTs to enhance marketing and offer alternate payment options. While it’s still early in the game, trends are starting to appear.

Bitcoin quickly became one of the more popular cryptocurrencies

One of these trends is using NFTs in marketing and branding, creating unique digital assets that can be collected. This gives an air of exclusivity, creates more immersive experiences, and helps forge a brand identity. NFTs are often a great tool to engage with customers and create a sense of community.

Melee Dose recently started integrating NFTs from Bored Ape Yacht Club (BAYC) into product packaging and branding. This has allowed the brand to offer unique experiences, foster community engagement, enhance storytelling and demonstrate adaptability to an ever-changing world.

“This collaboration merges the worlds of fashion, art and technology, providing our customers with exclusive “IRL” products incorporating digital assets and driving brand affinity”, says Swaroop Suri. “By embracing the digital revolution and connecting with the influential BAYC community, we aim to redefine consumer experiences and build lasting relationships with our audience.”

Crypto Payments Aren’t Futuristic Anymore

Payment is another trend to look out for. Cryptocurrencies are becoming more accepted in many big industries, including cannabis. With traditional banks limiting access to banking services, crypto allows cannabis companies to offer decentralized and secure payment options.

Cryptocurrency offers more enhanced privacy than traditional payment methods, which is great for those who want to stay under the radar. Lower transaction fees are another plus, as a decentralized system is more flexible. The speed of crypto payments is also an enticing feature, as payments are usually processed more quickly than traditional payment methods.

Swaroop Suri, Founder of Melee Dose

So, how are brands accepting crypto as payment? Is it safe? Melee Dose started accepting cryptocurrency payments on their e-commerce store by partnering with Coinbase Payments, a leader in the crypto industry with a strong reputation and ease of integration.

Cryptocurrency may seem perilous to those who don’t know much about it, but siding with the right company can help ease those fears. Addressing concerns about crypto volatility, Suri “opted for a feature provided by Coinbase Payments that allows for immediate conversion of cryptocurrency payments into our local currency, ensuring stable revenue despite market fluctuations.”

By working closely with reliable payment partners like Coinbase Payments and implementing necessary features, companies like his are able to successfully overcome crypto roadblocks, providing customers with increased flexibility and convenience.

The Future of Crypto, NFTs & Cannabis

The future of integration between cannabis, crypto and NFTs is exciting and always on the move, meaning there are opportunities constantly arising and challenges ahead we have yet to tackle. As cannabis legalization continues to evolve, we might expect changes in regulatory frameworks that impact how cryptocurrency is used in the industry. While we can’t say what those changes might be, the fact that NFTs and crypto have become mainstream indicates a clear adoption, as the industry finds ways to integrate them. From blockchain integration and creative marketing to payment options and immersive experiences, they are here to stay.

Swaroop Suri and his team might’ve gotten in on the game early, but they know the future is expansive: “It’s possible that NFTs could become a significant part of cannabis marketing strategies in the future,” He says. “The cannabis industry can use NFTs in various ways, such as tracking crops and using intellectual property to promote products through packaging artwork, which is what our team at Melee Dose has accomplished.”

NFTs won’t stop there. “There is a possibility to use NFTs for establishing VIP programs that offer exclusive discounts and access”, Suri says. “The ownership of an NFT could grant special privileges and perks to customers when shopping with an e-commerce company, fostering a deeper connection with the brand and community and leading to customer loyalty in the long run.” NFTs offer diverse possibilities for cannabis brands to improve their marketing techniques and get creative.

When it comes to crypto payments, brands will surely continue to add crypto as an option in addition to merchant processors. Highly-regulated industries like cannabis can find many benefits in crypto, as experienced by Suri: “Accepting cryptocurrency can mitigate some of these issues by providing an alternative payment option that is not subject to the same restrictions as traditional payment methods.”

Final Thoughts

The excitement surrounding crypto and NFTs is understandable, and as the cannabis industry introduces new opportunities for those who are at the intersection of these two global forces, companies everywhere are changing their relationship with technology.

There are other brands hopping onto the this train as well. Household cannabis brands and popular companies like Plain Jain, Highland Pharms, American Green and Pharma Hemp are just some of the many that have begun accepting crypto as payment.

As the industry continues to evolve and grow, staying ahead of the curve and embracing technology with critical thinking and environmental consciousness is key. As a new, dynamic and exciting space with as many opportunities as it is filled with challenges to tackle down the road surrounds us, the one thing we know for sure is that this is just the beginning.

As a business owner, insurance is always a must. If you are interested in entering into the cannabis industry or you already have, it’s important to know what to expect when it comes to insuring your cannabis-related business.

That’s why we’ll be exploring what dispensary insurance is, different options for business owners and general advice regarding dispensary and other CRB insurance.

What is Dispensary Insurance?

Insurance for cannabis-related businesses refers to policies that protect the business against risk. This can include dispensaries, cultivation centers and testing labs – all of which require different levels of coverage and liability.

We spoke to Alexander Marenco, an insurance broker from Marenco Insurance, who explained what dispensary owners should know before seeking out insurance. Marenco says it’s similar to shopping for insurance for other businesess. “You need to have full details of the business and location to receive a quote.” He adds. “The applications will ask questions such as location, renovations, or improvements to the location, ownership information, payroll details, and sales or projected annual sales.”

How is Dispensary Insurance Different From Other Forms of Business Insurance?

Because non-hemp-derived cannabis is still considered a schedule one controlled substance under the Controlled Substance Act, cannabis insurance can be more expensive than regular insurance for non-cannabis businesses. Because of the risks associated with being considered a potential retailer of a controlled substance, liability policies and other options can cost a pretty penny.

The cash-only nature of the business makes insuring dispensaries more costly

Additionally, when asking Marenco about how dispensary insurance differs from other brick-and-mortar retail insurance, he says: “With more states increasingly legalizing medicinal and recreational marijuana, insurance carriers have started to open risk acceptability. However, since marijuana is still federally illegal, businesses will find it difficult to find multiple quotes from different carriers.”

Types of Insurance Available for Cannabis-Related Businesses

What kind of insurance is available for cannabis-related businesses? Let’s find out.

First off, it’s important to keep in mind that CRBs are at risk for a lot of things: workplace accidents, damage to property, theft, general liability and product liability. Plus, the fact that most dispensaries work on a cash-only business model until the Secure and Fair Enforcement (SAFE) Banking Act is approved by Congress, CRBs tend to handle big amounts of cash, further putting them at risk of theft and liability. CRB insurance can be as low as $350 and as high as $7,500 depending on the type of business and policy.

Here are some of the most common types of insurance for CRBs and what they cover:

General liability: third-party claims for bodily injury, property damage and reputational harm.

Commercial property: damage to a business-owned property.

Professional liability: third-party accusations of negligence and mistakes.

Workers’ compensation: employees’ medical bills and lost wages due to injury or illness.

Inland marine: damage or theft of business-owned property in transit.

Crop: costs from damage to seeds and plants.

With so many things to watch out for, insurance for cannabis businesses and dispensaries isn’t cheap. Here, Marenco says what CRB owners can do to keep their premiums as low as possible:

A smart safe like this one can help secure cash handling

“Premiums are primarily based on sales (actual or projected). After the term expires, the insurance carrier will conduct an audit for the prior term to confirm the information from the application. The audited discrepancy will adjust the next term’s sales figures. Dispensary insurance will typically be placed through an excess & surplus market which do not provide traditional discounts.”

So, in essence, the best thing a dispensary owner can do is be honest about their projections.

Navigating premiums can be a detailed process, as we learned when speaking to Jesse Giffith, an owner of Smokeless CBD and Vape: a chain of retail shops across the twin cities Minneapolis–Saint Paul, Minnesota:

“Our shops carry insurance that has been offered with a modified rate for vape retailers. This route was not as straightforward as some traditional retail insurance options, but may offer benefits, and a better fit for coverage than other dispensary insurance options.”

A Growing Number of Dispensaries Across America

With the growing legalization and normalization of adult use, medical and hemp-derived cannabis across the nation, it should come as no surprise that the number of dispensaries across the country grows exponentially.

In 2021, the cannabis market in the U.S. was valued at 10.8 billion dollars, with an expected annual growth of 14.9% annually. This is a sign of what’s to come. Cannabis may be an industry that’s been considered taboo for decades, but the growth shows the growing acceptance of the plant for medical and adult use reasons.

Insurance providers remain cautious as cannabis laws are still in flux.

With that growth comes a greater need for insurance providers, opening the door to the possibility that these two industries will grow in tandem. The future may bring a greater variety of options for coverage at cheaper prices. But for the time being, insurance providers remain cautious as the fate of federal and local cannabis laws are still in flux.

Are There Limited Carriers that Issue Dispensary Insurance?

Every CRB needs insurance, just like any other type of establishment, business or company. The issue within the cannabis industry is that there is still a limited insurance market, with insurers willing to provide insurance constantly exiting and entering the market. Plus, the overall capacity and variety of policies that cover different types of risks are limited. Lastly, it can be difficult to use CRB insurance when you read between the lines of the policy. Because cannabis with THC is still federally illegal (excluding hemp-derived cannabis products containing less than 0.3% THC), insurers can negate coverage when a loss or claim occurs.

Because of the complications that may arise even if you do have insurance, Marenco offers some advice for dispensary owners that are searching for the right insurance option for them: “Before shopping for insurance make sure you have all your licenses and are in full compliance with all regulations. Insurance carrier’s requirements from the state. Additionally, consider different coverage options.” He continues. “At a minimum, a business needs general liability insurance. Insurance companies can also consider covering business property including inventory, betterments, and improvements to a rented space, among others. When shopping for insurance make sure your agent reviews different coverage options.”

It takes a lot to hack it in the wild world of cannabis.

To dip your toes in this game and open your own business, it could cost you between a quarter to three-quarters of a million dollars after licensure and other start-up expenses – and the battle doesn’t end there. Recent data supports that the turnover rate for the cannabis industry at large is extremely high when compared to other industries, coming in at a whopping 40-60% within the first 2 months.

Oh, and let’s not forget: we’re not living in the easiest of times in general. The Bureau of Labor Statistics now reports that inflation has hit 9.1 percent, the highest ever recorded level of inflation since records began. We know that people are struggling all over the place – and those struggles are even more amplified for cannabis operators and business owners. It’s no secret that amid these struggles, many legacy operators, MSOs and mom-and-pop brands alike are making the tough decision to take on costly loans, seek funding or even ultimately close their doors.

Every time a customer abandons their cart, your business is leaving money on the table.

But, in times like these, you have to remember what brought you to the table to begin with. The cannabis industry is still projected to hit a valuation of over $33B by the end of 2022 and despite the blood in the water that we’ve seen lately, operators of all sizes are still getting wins and making a profit. So, do you throw the towel in and give up on your dreams? Should you just accept that all hope is lost?

Absolutely not.

If you’re a cannabis operator who is struggling, you aren’t alone – and more importantly, you aren’t out of options yet. Not ready to go down with the ship just yet? We didn’t think so.

Here are five, expert-approved tips to create an influx of cash for your cannabis business without significantly increasing spending:

‘Trim the Fat’ of Your Business by Cutting Lean Costs

While it may seem obvious, many cannabis operators forget that “nice to have” is not the same thing as a “must have” when it comes to keeping your doors open and your bottom line healthy. Take an eagle-eyed second look at your budget and cut back as much as possible on areas that aren’t boosting revenue. Reconsider the “extras” – like software solutions, hiring non-essential staff and slow-moving inventory – and focus your attention on the products that contribute the most to your bottom line.

Make Your Customers a Priority

Focus your attention on the products that contribute the most to your bottom line.

One of the biggest mistakes that cannabis brands make is throwing so much of their marketing budget into getting new customers through the door while neglecting to show existing customers the attention they deserve for their loyalty. In today’s market, cannabis consumers have more options than ever. Why should they keep choosing you? Happy customers are customers that will weather the storm with you. Honing in on targeted ads and marketing efforts geared toward existing customers, in combination with loyalty perks, VIP deals and more is a great way to ensure your business is truly unforgettable in the eyes of the customers that keep your doors open. Looking for an extra leg up? Here’s an insider pro tip: refer-a-friend programs are a great way to get the best of both worlds and help those marketing dollars stretch a little further.

SOS: Save Our Shopping Carts

Shopping cart abandonment is a serious problem for cannabis retailers – and it happens all the time. For mobile users, it can creep as high as 85%. Shopping cart abandonment happens when a potential customer visits your site, builds an order in the cart and then either forgets to check out or chose not to execute the purchase. Every time a customer abandons their cart, your business is leaving money on the table. Fight back against shopping cart abandonment by providing clear calls to action through the shopping and checkout process and targeting customers with emails or SMS messages that include discount offers or reminders to check out.

Pump Up Your Payment Solutions

It’s like Canadian rapper and singer-songwriter, Drake, said in his hit song, “Omerta”, “I don’t carry cash ‘cause the money is digital.”

Payment providers often give back a portion of transaction fees to business owners.

Let’s be honest, it’s 2022 – not a lot of people love carrying around cash. If your cannabis business is cash-only, you could be missing out on extra revenue from card and mobile payment-loving customers. On average, mobile payment users, on average, spend approximately twice as much through all digital channels as those not using mobile payments. Cash-only retailers also miss out on upsell opportunities by limiting themselves – let’s say a customer comes in with $40 in cash, they won’t be able to pick up that extra pack of cones or the grinder they were eyeing up at the checkout if they’re limited to cash-only transactions.

In addition, retailers who patronize payment solutions via debit card providers or online ACH can benefit from payment kickbacks as an additional stream of income, as these payment providers often give back a portion of transaction fees to business owners.

Don’t Forget About Employee Retention Credit (ERC)

If you haven’t heard of ERC – you could be leaving as much as $26,000 per employee on the table. Many cannabis business owners would be surprised to learn that they can still take advantage of the employee retention credit program that started during the pandemic.

The program was launched in March 2020 as a way to help offset the financial struggles of business owners during COVID-19. But, even this year, cannabis business owners can seek cash relief through ERC – employers can retroactively claim the ERC based on financial struggles they experienced during 2020 and the first three quarters of 2021.

Started your cannabis business after February 2020? You still may qualify under specific ERC provisions that can provide up to $100,000 in refundable credits.

At MJstack, we understand the trials and tribulations that cannabis professionals go through every day because we’re right here working alongside you.

Our team of professionals is familiar with cannabis and what it takes to make the cut in this world. Ready to boost your business and safeguard your investments against whatever comes next? Contact us today to learn more and book your FREE consultation.

Despite the US making cannabis regulations challenging to navigate, the industry is snowballing toward profitability. New Jersey legalized adult use cannabis on April 21 this year. One month earlier, The Garden State began accepting applications for Class 5: Retailers, Dispensing and Delivery.

Although New Jersey isn’t shy about its licensing requirements and standards, many people want to know how retailers can stay in the game for the long run. So, let’s talk about risk management considerations New Jersey retailers need to know.

Top Risks Cannabis Retailers Face in New Jersey

Regardless of what kind of retailer you operate —medical or adult use — it’s critical to know what you’re up against. The following are the most common risks we’ve watched cannabis retailers face daily in New Jersey, making a customized risk management strategy necessary.

Theft

Like other retailers, New Jersey cannabis retailers are vulnerable to theft. Unfortunately, theft can come from various angles, such as in-store, in-transit and insider crime. Besides cannabis retailers typically having a well-stocked inventory, it’s not uncommon for them to have more cash on hand than most other businesses.

Although the SAFE Banking Act could positively impact the cannabis industry, it’s in a notorious stall yet again. Briefly, the SAFE Banking Act would no longer allow financial institutions, such as banks and credit card companies, to refuse to do business with cannabis companies. However, cannabis retailers must operate in a cash-only environment, for now, forcing them to make bank runs multiple times a day. We probably don’t have to explain how enticing a significant inventory and fat bank bags look to criminals.

Cybersecurity

Since the onset of the global health crisis, the cyber liability landscape has nearly spun into a death spiral. In other words, cybercriminals sat on the edge of their seats during the pandemic, waiting to pounce on anything that looked slightly vulnerable. Remote workers, small businesses, and emerging industries were hard-hit.

It’s no surprise that New Jersey cannabis retailers face many cybersecurity risks through their point of sale (POS) systems. Additionally, retailers often gather and store personal information, such as email addresses, credit card numbers, shipping addresses, etc. Hackers and cybercriminals gravitate to this vital data rapidly.

Property Damage

In addition to the risk of theft, as mentioned above, cannabis retailers must protect their property from losses. Without adequate protection, damage to equipment or buildings could add up to high out-of-pocket costs. Consider the damage a weekend office fire or late-night vandalism would cause. If property damage occurs, retailers must figure out how to sustain business operations while recovering from the loss simultaneously. As a result, New Jersey retailers must protect their property and maintain business continuity.

How to Customize a Risk Management Strategy

Watch or listen to any news reports and there’s a decent chance that you’ll feel some slight sense of doom and gloom. And sure, a lot is going wrong in our world; however, that doesn’t need to impact how you perceive your businesses. Instead of casting a massive net over every possible risk that you can imagine, we recommend trying the following 5-step approach. Here’s the gist:

Identify: Pinpoint high-level risks that are specific to the cannabis industry. Then, let the process trickle down to focus on company-specific exposures.

Analyze: Determine how badly a particular risk could harm your retail company. How much will this hurt should the “what-ifs” play out?

Evaluate: Categorize risks according to how risk tolerant your company is. Will you avoid, transfer, mitigate or accept the risk?

Track: Use your history or the stats from a similar retailer to map out how you’ve handled the risk over time. Older retailers have an advantage over younger retailers, of course, but you can still get a feel for your risk management style.

Treat: Make good on your evaluation promises by avoiding, transferring, mitigating, or accepting the various risks you identified.

Recommended Insurance for New Jersey Retailers

Sales totals in the first month of New Jersey’s adult use market

The New Jersey Cannabis Regulatory Commission issued detailed requirements for new cannabis businesses. That said, part of the application requirements considered is the plan for companies to obtain liability insurance. Many new retailers opted for a “letter of commitment” as opposed to a certificate of insurance (COI), stating their plans for obtaining the following coverages:

Commercial general liability: Protects cannabis companies against basic business risks.

Product liability: Protects against claims alleging your product or service caused injury or damage.

Property: Reimburses cannabis companies for direct property losses.

Workers’ compensation: Covers employees if they are injured on the job and can no longer work.

In addition to the required insurance coverages, we recommend New Jersey retailers customize their risk management package with these policies:

Crime: Protects your cannabis company against specific money theft crimes.

Cyber: Protects your cannabis company against damages from specific electronic activities.

Directors & officers: Protects corporate directors’ and officers’ personal assets if they are sued.

Employment practices liability: Protects cannabis companies against employment-related lawsuits.

Professional liability: Protects cannabis companies against lawsuits of inferior work or service.

With more states in the US entering the marketplace soon, New Jersey is doing its fair share of the heavy lifting by spearheading the onboarding process. Remember, doing your due diligence at the start pays off in the long run — New Jersey retailers are proving that. Consider teaming with a commercial insurance broker calibrated to the cannabis industry, so you get the most out of your broker, marketplace and the cannabis industry as a whole.

Federal regulations have made compliant credit processing in the cannabis industry difficult to achieve. As a result, most cannabis retailers operate a cash-only model, limiting their ability to upsell customers and placing a burden on customers who might rather use credit. While some dispensaries offer debit, credit or cashless ATM transactions, regulators and traditional payment processors have been cracking down on these offerings as they are often non-compliant with regulations and policies.

Two companies, KindTap Technologies and Aeropay, are addressing the cannabis industry’s payment processing challenges with innovative digital solutions geared towards retailers and consumers.

We interviewed both Cathy Corby Iannuzzelli, president at KindTap Technologies and Daniel Muller, CEO at Aeropay. Cathy co-founded KindTap in 2019 after a career in the banking and payments industries where she launched multiple financial and credit products. Daniel founded AeroPay in 2017 after a career in digital product innovation, most recently at GPShopper (acquired by Financial), where he oversaw the design and development of over 300 web and mobile applications for large scale Fortune 500 companies.

Green: What is the biggest challenge your customers are facing?

Cathy Corby Iannuzzelli, co-founder and president at KindTap Technologies

Iannuzzelli: Our customers include both cannabis retailers and their end consumers. As long as cannabis is illegal at the federal level, normal payment solutions such as debit and credit cards cannot be accepted for cannabis purchases. This has resulted in heavy cash-based sales and unstable, transient work-around ATM payment solutions that can be ripped out with little notice, disrupting the entire business. The lack of a mature payment network to support retail payments for cannabis purchases is a huge challenge for all stakeholders. Cannabis retailers bear the high cost and safety issues of operating a heavily cash-based retail business. Consumers encounter several friction points that require them to change their behavior when purchasing cannabis relative to how they purchase everything else.

Muller: Our cannabis business customers have faced a constantly changing and, frankly, exhausting financial services environment. From the need to move and manage large amounts of cash, to card workarounds, added to the disappointment from legislation around the SAFE Banking Act, these inconsistencies have acted as a roadblock to their potential growth and profitability. Aeropay is in the position to be a stable, long-term, reliable payments partner ready to help them scale their businesses. We believe these opportunities are limitless.

Green: What geographies have got your attention and why?

Daniel Muller, CEO and founder of Aeropay

Iannuzzelli: KindTap’s focus is on the U.S. market where federal policy has created the need for alternatives to traditional payment networks. KindTap is available in every U.S. state where cannabis is legally sold. In terms of our distribution channels, KindTap’s digital payment solution was brought to market during the COVID-19 pandemic when curbside pick-up and delivery became critically important. These channels are where the exchange of cash at pick-up posed the greatest security risk to employees and customers. Our early integrations were with e-commerce platforms focused on delivery and pick-up orders, and our integration partners have strong customer bases in California and the northeast. So, while KindTap can provide its “Pay Later” lines of credit and “Pay Now” bank account solutions anywhere, we have heavier penetration in those regions.

Muller: California, for its established tech culture and how it plays into the cannabis industry – your product simply has to live up to their tech standards to be heard. Also, Chicago, our headquarters, with its newly emerged commitment to financing the cannabis industry and bringing with it a more traditional business approach. In Chicago, you have to have elevated standards of professional practices in any industry you enter. And of course, we love to watch emerging markets like New York and Florida as they head towards adult-use and what shape cannabis and payments will take.

Green: What are the broader industry trends you are following?

Iannuzzelli: We continue to see a strong transition from cash and ATM transactions over to digital payments. Since KindTap has a fully-integrated payment “button” on e-commerce checkout screens, the adoption rate of end consumers to that one-click experience is quite strong. We are also seeing trends of more “express lines” in the retail environment – for those KindTap users who paid online/ahead – and faster/safer delivery experiences to people’s homes since there is no longer the need to collect any payment upon delivery. We are firm believers in the delivery/digital payments combination and a strong increase of that trend as more states allow for delivery.

Muller: The cannabis industry is starting to normalize payments and mirror traditional online and brick-and-mortar. With bank-to-bank (ACH) payments, cannabis businesses can now offer modern customer shopping experiences including pre-payment for delivery orders without the need for a cash exchange at the door, offering the option to buy online pickup in-store and contactless in-store QR scan-to-pay customer experiences. With these familiar and customer-driven options now available, we are seeing widespread adoption, as well as meaningful increases in spend and returning customers.

Green: Thank you both. That concludes the interview!

About KindTap: KindTap Technologies, LLC operates a financial technology platform that offers credit and loyalty-enabled payment solutions for highly-regulated industries typically driven by cash and ATM-based transactions. KindTap offers payment processing and related consumer applications for e-commerce and brick-and-mortar retailers. Founded in 2019, the company is backed by KreditForce LLC plus several strategic investors, with debt capital provided by U.S.-based institutions. Learn more at kindtaptech.com.

About AeroPay: AeroPay is a financial technology company reimagining the way money is moved in exchange for goods and services. Frustrated with the current, antiquated payments landscape, we believe there is a better way to pay and a better way to get paid. AeroPay set out to build a payments platform that works for all- businesses, consumers, and their communities. Learn more at aeropay.com.

The cannabis industry is an unprecedented industry and one under constant review and control. Following the November 2020 elections, fifteen states and Washington DC have legalized adult use cannabis, a number that will continue to grow as legalization slowly becomes more widely adopted in other states. Beyond that, a continuously growing number of states allow residents to purchase legal medicinal cannabis, and many have also decriminalized adult use. However, it still remains a Schedule I substance under the Controlled Substances Act and is therefore illegal on all accounts at the U.S. federal level, which creates a number of issues for businesses in the cannabis industry duly operating in states where it has been legalized.

Not only is it difficult for cannabis companies to avail themselves of alternative banking solutions, but there are also obstacles in place preventing these companies from taking advantage of notable tax deductions. The primary obstacle being Internal Revenue Code (IRC) Section 280E.

What is Section 280E?

Section 280E is a relatively short code section, only 77 words to be exact, but it carries significant weight and can have a debilitating effect on the taxable income of marijuana [sic] related businesses (MRB). Section 280E of the IRC prohibits taxpayers who are engaged in the business of trafficking certain controlled substances, including cannabis, from deducting typical business expenses associated those activities. Section 280E, which was enacted in 1982 during the “War on Drugs” era, has become increasingly relevant for cannabis businesses. The cannabis industry has grown substantially in recent years with annual market values expected to reach $30 billion by 2025.

However, while Section 280E greatly restricts the tax deductions of state-legal cannabis businesses, there is some reprieve. Current IRC provisions permit state-legal cannabis businesses, including growers, producers, wholesalers or retailers, to deduct the Cost of Goods Sold (COGS) in computing their US federal income tax liability, despite the application of Section 280E.

Impact of Section 280E on Businesses

What does Section 280E mean for cannabis businesses today? It is intended to prevent dealers from claiming tax deductions for their business expenses, interpreted to include state-legal cannabis businesses, reduced deductions that result in increased taxable income and MRBs will face higher federal tax rates.

The IRC disallows any deductions or credits paid or incurred during a tax year if those deductions or credits relate to trafficking controlled substances. The courts have taken the position that the term “trafficking” in this case means “engaging in a commercial activity – that is, to buy and sell regularly.” Simply, the law denies cannabis businesses any U.S. federal income tax deduction for ordinary and necessary business expenses, despite being duly licensed as a legal business in their state of operation.

Typically, the ability to deduct ordinary business expenses means that a business is subject to federal tax on its net income (i.e., gross receipts minus expenses). However, the definition of Section 280E and the classification of cannabis as a Schedule I substance severely hinders legal cannabis companies from taking advantage of tax deductions for actual economic expenses incurred in the ordinary course of business, which results in a significantly higher effective tax rate as compared to other businesses.

Legal Actions and Challenges to Section 280E

There have been court challenges and concessions made to Section 280E. Specifically, the 2007 court case Californians Helping to Alleviate Medical Problems, Inc., v. Commissioner. This court case reinforced the precedence that Section 280E does not apply to cost of goods sold. The Internal Revenue Service (IRS) defines cost of goods sold to be “expenditures necessary to acquire, construct or extract a physical product which is to be sold.” Generally, for a retail MRB, this means that the direct cost of acquiring cannabis products for resale. Deductions for rent, utilities, wages, insurance and other operating costs common to ordinary businesses are generally disallowed. New York State has specifically indicated that it intends to follow Section 280E for its own income tax calculations, disallowing these same deductions against New York taxable income

Tax Court and Section 280E

The Tax Court has also been aggressive in tamping down efforts by MRBs to separate cannabis related and non-cannabis related activities. The courts argue that these separate activities constitute a single trade or business when they share a close and inseparable organizational and economic relationship. In addition, the risk of cannabis related activities tainting a taxpayer’s other business concerns exists if services or employees are shared between an MRB and a non-MRB. Allocation of expenditures to cost of goods sold, as well as any allocations of costs between MRB and non-MRB entities, need to be well thought out and supported by defensible tax and accounting positions.

The Future of MRBs and Section 280E

All indications point to an increased frequency of IRS audits of MRBs compared to audits of non-cannabis related businesses. Therefore, documenting the methodology behind the calculation of costs of goods sold is even more important for MRBs. It is vital to consult with a tax advisor to ensure you are maximizing your cost of goods sold deductions and preparing the best documentation possible to support your 280E tax positions.

Disclaimer: The information presented in this article should not be considered legal advice or counsel and does not create an attorney-client relationship between the author and the reader. If the reader of this has legal or accounting questions, it is recommended they consult with their attorney or accountant.

It wasn’t that long ago that cannabis was underground, sometimes literally, and operators protected what was theirs any way they knew how. Before legalization, cannabis operators needed to secure their plants, cash, supplies and equipment not just from people who wanted to steal them, but also from law enforcement. The legacy cannabis market is now transitioning into a legal one, and licensed operators are joining the industry at an incredible rate, but security is still part of the success equation. Like before, operators need to protect plants, products, equipment and cash, but they now also need to protect records, privacy and data, and do so in a manner that complies with state regulations.

Cannabis regulatory authorities set security guidelines that cannabis business owners must follow in order to obtain and renew operational licenses. For instance, there are state-specific security regulations regarding video surveillance, camera placement, safes, ID verification, and more. While security measures help protect the business, they also protect the public. It’s a win-win for everyone involved. Here are five best practices and techniques to protect cash, records, products and people.

Hybrid cloud storage

State regulations call for reliable video surveillance footage that is accessible, in most cases, 24/7 and upon demand by cannabis regulatory authorities and local law enforcement acting within the limits of their jurisdiction. SecurityInfoWatch.com reports that video data is the industry’s next big investment, meaning there will be an increased demand and need to store video surveillance footage. Most states require video surveillance footage to be retained for a specific amount of time, often 45-90 days or longer if there is an ongoing investigation or case that requires the footage. While some businesses only retain video data for the state-required length of time, others choose to keep it longer.

Storing data on-site can become expensive and precarious. Best practices call for a hybrid cloud storage solution model as it provides on-site and both public and private cloud data storage solutions. This model provides users with the ability to choose which files are stored on-site and which files live in the cloud. Doing so improves file accessibility without impacting or compromising on-premises storage. In addition, it’s helpful to have two methods of digitizing data, for safety’s sake. In the event an on-site storage method crashes—though hopefully this won’t ever happen—there’s a version available off-site via the cloud. That said, with cloud-based storage solutions come cybersecurity threats that must be managed.

Cybersecurity

Dispensaries are prime targets for burglary. Defending a storefront requires a comprehensive security plan

Due to the ongoing COVID-19 pandemic, more businesses are online than ever before. Unsurprisingly, cyberthreats are on an upward trend, including in the cannabis industry. Earlier this year, MJBizDaily reported that a data breach exposed personal information of current and former employees of Aurora Cannabis. The incident involved “unauthorized parties [accessing] data in (Microsoft cloud software) SharePoint and OneDrive”. Although this breach involved only employees, confidential customer information is also at risk of being compromised during a data breach.

On a separate occasion, an unsecured Amazon S3 data storage bucket caused a large-scale database breach that impacted almost 30,000 people across the industry, according to the National Cannabis Industry Association. The breach included scanned versions of government-issued ID cards, purchase dates, customer history and purchase quantities. Unlike the Aurora Cannabis breach, this one included customer data.

Just like other more established industries, the cannabis industry needs to protect and secure confidential data. If you don’t have a cybersecurity expert on your team, consider hiring a consultant to evaluate your risk or partnering with a credible cybersecurity technology company to implement proactive solutions. Before signing a contract, do your due diligence. Does the consultant and/or technology company understand the compliance regulations specific to the cannabis industry? Do their solutions meet the regulations in the state(s) where your facility operates? Taking the time to protect your company’s data before a breach occurs is proactive, smart business.

Smart Safes

A smart safe like this one can helps secure cash handling

Smart safes help secure cash handling, which given the difficult banking environment for cannabis companies, means they’re on the list of best practice security technology products. What is a smart safe? A smart safe is a device that securely accepts, validates, records and stores cash and connects to the other cash management technology solutions such as point of sale systems. They connect to the internet and provide off-site stakeholders visibility into a facility’s cash position.

A high-speed smart safe counts cash by hand faster than a human and is an overall more secure way to deliver cash bank deposits. At the end of the night, making a deposit at a physical bank location can be dangerous, exposing your cash and the individuals responsible for making the deposit to unsecured threats. Using a smart safe reduces that threat and also helps cannabis operators comply with financial recordkeeping and documentation requirements. Due to federal cannabis prohibition, many cannabis businesses lack enough insurance to fully cover their exposure to cash theft, which has led to a trending industry-wide investment in smart safes.

Advanced access control

Best practice access control means more than a ring of keys hanging off the facility manager’s belt. Advanced access control gives cannabis business owners and managers the ability to manage employee access remotely via the cloud. This feature can limit access areas within a facility, enabling an individual to revoke access instantly from a remote location making it a useful tool in the event of a facility lockdown or emergency. A mobile app and/or website can be used to lock or unlock secure doors, monitor access in real time and export access logs.

Advanced access control devices aren’t a standard in the industry yet. Although many state regulators don’t require cannabis businesses to utilize advanced electronic access control, using this technology is a best practice and may be required in the future.

Compliance software

Understanding the ramifications and keeping up with state-mandated compliance is challenging. While state regulations can be found online, they’re often in pieces, leaving operators unsure about whether or not they have them all. Once an operator is confident that they have the most current version of all the laws, rules, and regulations that apply to their cannabis business, making way through the dense legal jargon can be exhausting. Even after multiple readings, it can be unclear about how to apply these guidelines to the operator’s cannabis business, which is one reason cannabis businesses work with a trusted legal counsel to meet compliance requirements. For trusted advisors and cannabis business licensees and operators alike, cannabis compliance software solutions are designed to not just check boxes for a cannabis business, but to help everyone involved understand how the regulations apply to the operation. These solutions improve accessibility so that employees at all organizational levels understand the rules and requirements of their position and the products they work with.

In addition, compliance software can help licensees and operators establish and implement best practice SOPs to meet regulatory requirements. Because the cannabis industry is young and many operators are moving fast, many cannabis businesses are vulnerable to security breaches and threats. Prioritizing security and compliance can help cannabis leaders protect against potential threats. Investing in the latest and most innovative security technology solutions—beyond what is required by state regulations—can help operators outsmart those who seek to steal from them and position their companies as industry leaders that prioritize safety and compliance, protecting not just cash and products, but the people who work in their facilities and the customers who purchase their products.

Federal regulations have made compliant credit processing in the cannabis industry difficult to achieve. As a result, most cannabis retailers operate a cash-only model, limiting their ability to upsell customers and placing a burden on customers who might rather use credit. While some dispensaries offer debit, credit or cashless ATM transactions, regulators and payment processors have recently been cracking down on these offerings as they are often non-compliant with regulations and policies.

KindTap Technologies, LLC operates a financial technology platform that offers credit and loyalty-enabled payment solutions for highly regulated industries typically driven by cash and ATM-based transactions. KindTap offers payment processing and related consumer applications for e-commerce and brick-and-mortar retailers. Founded in 2019, the company is backed by KreditForce LLC plus several strategic investors, with debt capital provided by U.S.-based institutions.

We interviewed Cathy Corby Iannuzzelli, co-founder and chief payments officer at KindTap Technologies. Cathy co-founded KindTap after a career in the banking and payments industries where she launched multiple financial and credit products.

Aaron Green: Cathy, thanks for taking the time today. How did you get involved in the cannabis industry?

Cathy Corby Iannuzzelli, co-founder and chief payments officer at KindTap Technologies

Cathy Corby Iannuzzelli: I’ve been in the payments industry for a long time. I was doing some consulting a few years ago for a client in Colorado and that gave me exposure to the issues in cannabis like the fact that you couldn’t have real payments in cannabis. Then, a close family member with health issues turned to medical cannabis when nothing else seemed to work. I was amazed by the difference it made in her life. At that point, I put those two things together and I said, I need to focus on helping this industry get a real cannabis payments solution because I thought it was ridiculous that you had an industry of this size and importance that had been abandoned by the payments industry.

Aaron Green: Can you highlight some of your background prior to entering cannabis?

Corby Iannuzzelli: Throughout my career, I’ve been a banker, I’ve been a payment processing executive and I’ve been a consultant. So, I’ve kind of done it all in the payments and financial services space.

Aaron Green: Why is it that most dispensaries only take cash?

Corby Iannuzzelli: In the US, even though cannabis is legal in many states, it’s still illegal federally. There are big banks and card networks like Visa, MasterCard, etc., who are national, even global companies and frankly, the executives of those companies don’t want to end up in jail for violating national laws. So, they have put cannabis dispensaries on what’s called a “prohibited merchants” list. This means you cannot accept Visa, MasterCard, Discover, American Express, or similar payments as a cannabis business and so it’s forcing the industry to a cash-based solution.

About the only thing you’re seeing that’s not cash in dispensaries are ATMs. But if you think about it, ATMs are machines where the consumer goes and pulls cash out and pays upwards of $5 or more in fees for doing that. They then hand that cash back to the dispensary who then has the costs of having to deal with that cash. The industry is just stuck in a cash-based business until federal legislation changes.

Aaron Green: I’ve been to some dispensaries where they accept credit cards or debit cards. What is going on there?

Corby Iannuzzelli: I’ve heard reports of consumers who’ve been able to use a credit card or a debit card in a dispensary. Sometimes the processor who sold that solution to the dispensary says, “Oh, it’s compliant, I guarantee you it’s compliant.” But if you dig in, that’s not the case. And eventually, Visa or MasterCard figures it out and shuts it down. In some cases, it’s outright fraud where the processor who sold the payment terminal to the dispensary is misrepresenting it as say a doctor’s office rather than a dispensary. There’s no merchant category code in the payment networks that says this is for processing dispensary payments, so they pretend it’s something else until they get shut down.

When they do get shut down, I’ve heard of cases in Las Vegas where it was basically 100% Visa or MasterCard one day and 100% cash the next day. It completely disrupted the whole business. It’s not just the retail store, but the inventories and everything else throughout the business.

“About the only thing you’re seeing that’s not cash in dispensaries are ATMs”

There have also been some cases where you’ll see something called a cashless ATM. In a store, they call it a debit card transaction. It’s really a cashless ATM where the consumer is making what looks to the ATM network like a cash withdrawal in $10 or $20 increments, but the consumer is getting a receipt instead of cash, and they’re turning around and handing that receipt back to the dispensary who then makes a change because the cashless ATM only dispensed in $10 or $20 increments.

Now ATM networks are looking at these cashless ATM transactions to see if they are compliant. Do consumers know the fees that they’re paying? Are these transactions coming in and looking to the network like real cash when it’s not? Cashless ATM transactions are probably the most common thing you see, but that’s being called into question after the Eaze incident where a large company was misrepresenting its terminals. The federal government stepped in and called it bank fraud and the individuals behind it, the executives, are in jail. Since then, the networks are looking at this and saying, what about these cashless ATMs? Are those transactions within our rules, or is there something funny going on here?

Aaron Green: So, to summarize here: you’ve got federal regulations at the national level that says that cannabis banking is not allowed so major institutions are not offering it. Yet you found a way through the regulations and compliance issues. I’m curious can you pull back the curtains a little bit and tell us how you came up with a solutionhere?

Corby Iannuzzelli: Well, we came up with the solution by stubbornly refusing to believe that cannabis payment processing could not be done in a compliant manner. We just said, “there is a compliant way to do this, let’s figure it out.” We took the same components that are out there for the financial services and payments industry and reassembled them in such a way that we do not violate any rules. We do not use any of the Visa, MasterCard, Discover or Amex rails, we built our own network. We have direct contracts with the merchants and direct contracts with the consumers. We control everything and all the funds flow through regulated financial institutions. So, we designed something that looks and acts to consumers and retailers the way Visa and MasterCard look and act when a consumer goes to make a purchase, but they run on a separate set of payment rails and in compliance with banking regulations and state regulations. When you’re looking at the problem from a different perspective, sometimes you can come up with a better answer.

Green: On the consumer side, what does that user experience look like?

Corby Iannuzzelli: Our product is completely digital. The consumer experience starts with integration at the online checkout. When it’s an e-commerce shopping cart and somebody is placing an order, they will see a button called “Pay with KindTap.” The first time they click that button they’re automatically brought to our integrated web app where they do a quick and easy application for our digital revolving line of credit product. If approved, they instantly go back to the checkout screen and their first purchase will just happen immediately, with flexible payment options over time. If the consumer decides they don’t want our KindTap credit and would rather have a pay now-product where we pull the funds from their bank account, then the consumer can do so. So, there is no physical card per se, it’s integrated like PayPal or Affirm at the point of checkout online. For the consumers who use KindTap credit, there is a mobile app where they can see their transactions, view statements, pay their bills, etc.

Additionally, there is a loyalty program for all purchases – KindTap credit or through the consumer’s bank, because we feel very strongly that a lot of the reasons consumers choose to pay with one card over another is the points and the rewards that they get. So, we’re providing loyalty rewards with KindTap so that consumers can get rewarded for that spending with KindTap and it’s better for the retailers.

Green: On the retailer side, what does that experience look like and what is your business model?

Corby Iannuzzelli: We are not going store by store doing integrations, rather, we’re integrating with various software, delivery and e-commerce providers. That gives us broad reach and ability to expand rapidly in various state markets where cannabis is legal. Once a merchant says “yes, I want to be a member of the KindTap Merchant Network,” then we work to get them set up on our platform in a matter of days. The merchants receive continuous support from our success team, marketing co-investment and a depth of analytics reporting. We made the entire process and ongoing operations streamlined and frictionless for both merchants and consumers.

Aaron Green: What are the benefits of moving from cash to credit type of payments?

Corby Iannuzzelli: On the retail side, there are the obvious benefits of not having all the security, safety and theft issues associated with operating a physical cash business. Consumers very often don’t carry cash anymore, except when they’re making a cannabis purchase. There are a lot of hidden costs to retailers because payments are not just about moving money from the consumer to the business.

“I really am optimistic that with so many scientific breakthroughs we’ve had that we’re going to be able to figure this out.”Payment options – or lack thereof – can shape where people shop, how much they spend and what they buy. It’s a proven science how consumers make impulse purchases. If you’re a cash-based business in cannabis, and you’re trying to get somebody to make an impulse purchase, and they walked in with $100, then you can’t get them to spend more than $100, no matter how creative your marketing is! The consumer is limited by how much cash they have in their bank account or in their pocket at that point in time. So, it’s really about the upsell that comes with the bigger basket sizes that retailers experience when you move from a cash-based business to credit and suddenly, the merchant doesn’t have to deal with long lines of consumers on payday when the store was beyond slow two days before. Now the consumer can spread purchases with the thinking, “I’d rather not be the one standing in that line on payday. I’m going to go Wednesday [instead of Friday] because I have KindTap credit so I can budget and manage my cash flow throughout the month rather than around my paydays.”

So, we think that the lack of an efficient and effective payment system for cannabis is holding back sales. We all focus on how much the industry is growing. KindTap thinks about how much faster it could be growing if it was supported by a decent payment system.

Aaron Green: What are some other cash-only markets you are looking at?

Corby Iannuzzelli: We are laser-focused on the cannabis ecosystem and bringing a compliant credit and loyalty-based digital payments solution to cannabis merchants and customers and rewarding those stakeholders for accepting/using KindTap. Additionally, we are planning to extend the KindTap Merchant Network so that consumers can use/earn our loyalty points with other goods and services they’re purchasing that are adjacent to cannabis or that are important to the cannabis consumer. That’s the direction we’re going.

Aaron Green: Today people can receive gas points for spending with their credit card. Now with KindTap, you can spend to get cannabis points?

Corby Iannuzzelli: That’s exactly right.

Aaron Green: What in either cannabis or your personal life are you most interested in learning about?

Corby Iannuzzelli: Personally, I am most interested in seeing breakthrough technologies in climate change. We’re going to need to correct this situation and I’m reading about collecting carbon dioxide from the air and burying it in the earth and things like that. I really am optimistic that with so many scientific breakthroughs we’ve had that we’re going to be able to figure this out. Certainly, it’s going to take a lot of smart people and a lot of investment, but I really look forward to watching them do their stuff and hopefully taking us out of this nightmare situation that we’re heading into if we don’t make some changes.

Aaron Green: Thanks Cathy, that concludes the interview.

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

We use tracking pixels that set your arrival time at our website, this is used as part of our anti-spam and security measures. Disabling this tracking pixel would disable some of our security measures, and is therefore considered necessary for the safe operation of the website. This tracking pixel is cleared from your system when you delete files in your history.

We also use cookies to store your preferences regarding the setting of 3rd Party Cookies.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.