UPDATE: Late in the evening on May 15, the House of Representatives passed the HEROES package, voting 208-199 (with 23 abstentions). The bill now now heads to the Senate where its fate is more uncertain.

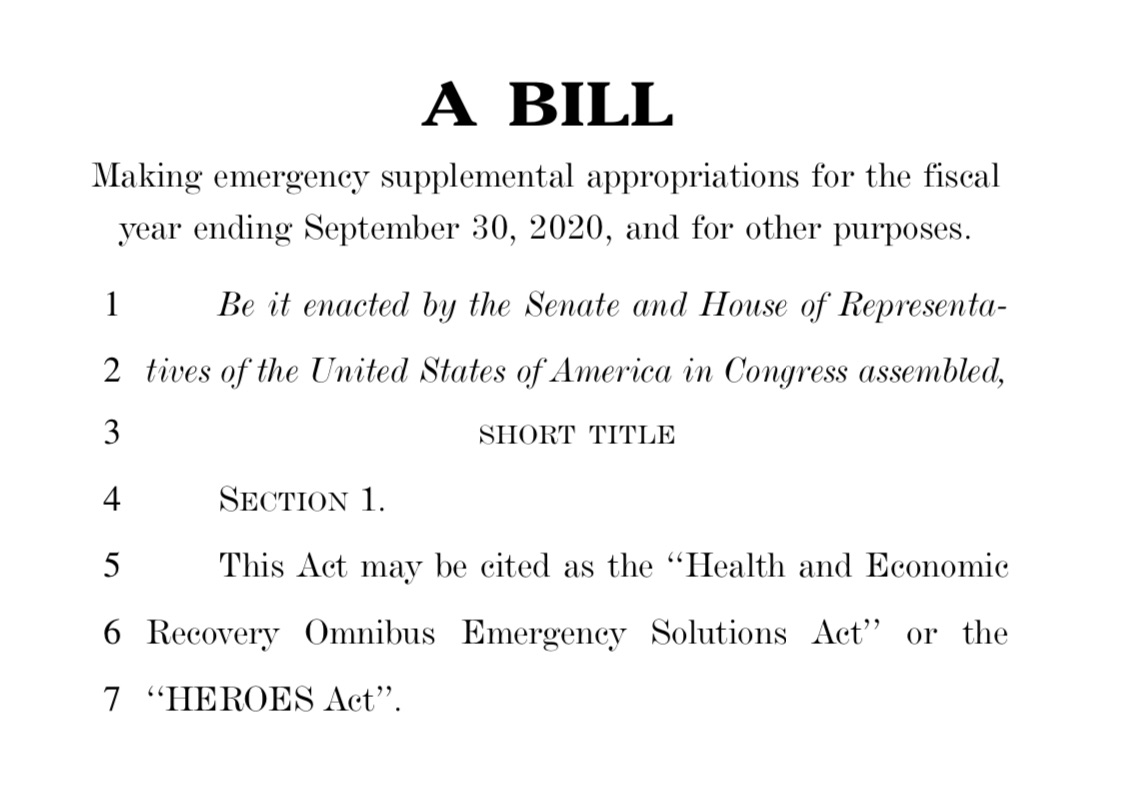

Earlier today, Speaker Nancy Pelosi debuted the latest piece of legislation to help Americans impacted by the coronavirus pandemic. The Health and Economic Recovery Omnibus Emergency Solutions Act (HEROES Act) is a large bill containing emergency supplemental appropriations more than 1,800 pages long.

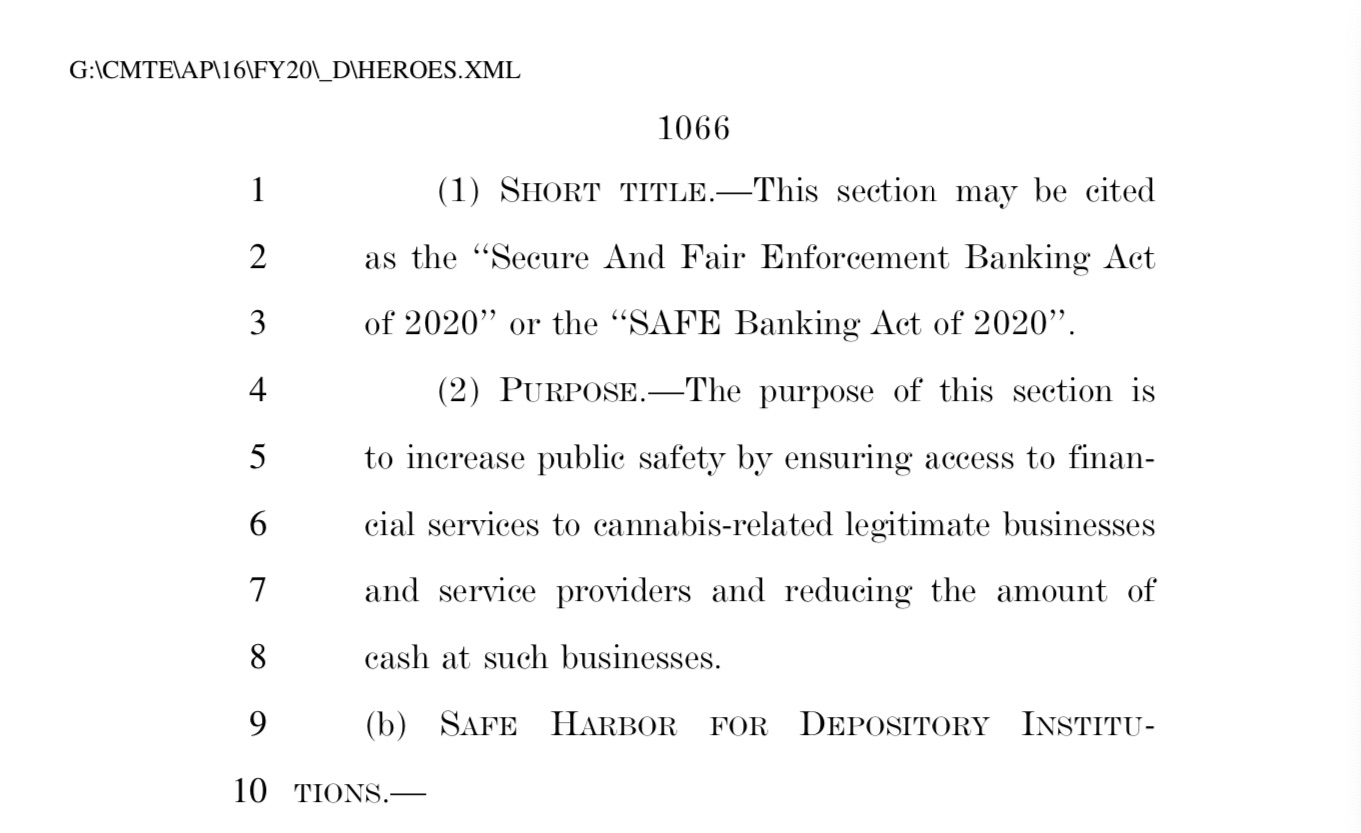

On page 1,066, those in the cannabis industry will find a very exciting addition: the Secure and Fair Enforcement (SAFE) Banking Act. For the uninitiated, the SAFE Banking Act would ensure access to financial services for cannabis-related businesses and service providers.

Currently, federally regulated financial institutions face penalties for dealing with cannabis companies due to the Controlled Substances Act. The bill, if passed, would eliminate the possibility of any repercussions for doing business with cannabis companies.

The impact of this bill becoming law would be widespread and immediate for both the cannabis market and banks looking to invest in the cannabis industry. With banks given the green light to conduct business with the cannabis industry, there is no doubt that many financial institutions will rush to the opportunity. Cannabis businesses will benefit greatly, no longer having to deal with massive quantities of cash and gain access to things like loans, bank accounts and credit lines. Furthermore, cannabis companies will benefit from the rush of banks getting in the game, leading to a competitive and affordable banking market.

The impact of this bill becoming law would be widespread and immediate for both the cannabis market and banks looking to invest in the cannabis industry. With banks given the green light to conduct business with the cannabis industry, there is no doubt that many financial institutions will rush to the opportunity. Cannabis businesses will benefit greatly, no longer having to deal with massive quantities of cash and gain access to things like loans, bank accounts and credit lines. Furthermore, cannabis companies will benefit from the rush of banks getting in the game, leading to a competitive and affordable banking market.

It is no secret that cannabis businesses have had a cash problem for decades now. Given the coronavirus pandemic, CDC guidelines dictate minimizing the handling of cash and encourage payment options like credit cards. Cannabis businesses dealing with large quantities of cash puts them, their employees, their customers and even regulators at risk.

According to Aaron Smith, executive director of the National Cannabis Industry Association (NCIA), the cash problem is a serious, unnecessary health risk. “On behalf of the legal cannabis industry, we commend the congressional leadership for prioritizing public health and safety by including sensible cannabis banking policy in this legislation,” says Smith. “Our industry employs hundreds of thousands of Americans and has been deemed ‘essential’ in most states. It’s critically important that essential cannabis workers are not exposed to unnecessary health risks due to outdated federal banking regulations.”

In fact, it was the NCIA and a handful of other industry organizations that lobbied Congress last week to include language from the SAFE Banking Act in the HEROES Act, citing the known fact that cash can harbor coronavirus and other pathogens, along with the “personal proximity required by cash transactions as reasons for urgency in addition to the other safety and transparency concerns addressed by the legislation.”

The SAFE Banking Act was already approved by the House of Representatives. In September of 2019, the bill made a lot of progress through Congress, but stalled once it made it to the Senate Banking Committee.

The HEROES Act will be debated by the House of Representatives prior to a floor vote. If it passes the House, it moves to the Senate, which is about as far as it made it the last go around. However, because the banking reform is included in coronavirus relief legislation, there is a newborn sense of hope that the bill could be signed into law.