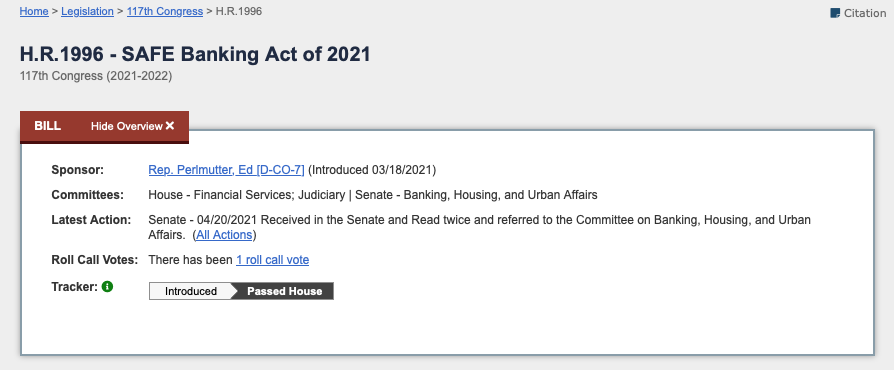

Here we are again, crossing our fingers, hoping that the Senate will approve the passage of the Secure and Fair Enforcement Banking Act (SAFE Banking Act). This Act would provide banks with regulatory protections, allowing them to offer critical financial services to cannabis businesses without risking the loss of their banking charter.

As the 2024 elections loom, the stakes have never been higher for passing the SAFE Banking Act.

Cannabis Legalization is On the Rise

As of August 2023, 40 states, four territories and the District of Columbia have legalized medical or adult use cannabis. While some states have moved more slowly, the entire West Coast (including Nevada and Colorado) has voted to pass laws allowing the sale and purchase of adult use cannabis. Most of the East Coast has followed suit; New York, Pennsylvania, New Jersey and Massachusetts have all voted to regulate cannabis. It has become evident that the majority of U.S. citizens are now comfortable with legalized cannabis (156 million people live in jurisdicitons that have legalized adult use).

Banking Roadblocks for the Cannabis Industry

Under current federal policy, banks and other large financial institutions face regulatory restrictions that make it challenging to provide the most basic services to local cannabis companies, regional cannabusinesses and MSOs (Multi-State Operators).

Federal anti-money laundering laws and related record-keeping regulations, such as the Bank Secrecy Act (BSA), have presented complex compliance protocols that prevent banks from meeting the business needs of local growers, manufacturers and dispensaries. Local cannabis business owners are therefore put in a difficult position, as they must balance daily business activity against the potential dangers of operating as a cash-only business.

How Would the SAFE Banking Act Help Banks Serve the Cannabis Industry?

The proposed SAFE Banking Act would protect banks from federal penalties for offering their services to cannabis businesses in states with regulated cannabis industries. Critically, the bill would shield banks from losing their deposit insurance. Without reform through the SAFE Banking Act, financial institutions will remain essentially prohibited from working directly with legal cannabis companies.

Policymakers may need to introduce the Act as a stand-alone bill that outlines clear objectives and specifically addresses the issue from a public safety perspective. Cannabis is a hot-button issue, so adding additional legislation will muddy the water and make it easier for Senate members on the fence to vote against the bill.

Cannabis industry representatives and political allies must be strategic in navigating the bill’s potential passage and take the process step by step. First, the SAFE Banking Act must pass to allow cannabis businesses the opportunity to stabilize, grow and prosper. As the sector grows stronger and more accepted by mainstream America, more progressive bills can be introduced and will have a greater chance of successful passage in the House and Senate.

The SAFE Banking Act is an Issue of Public Safety

Every day the Senate chooses to sit on their hands, they put more Americans in harm’s way. This is unacceptable.

Because dispensaries and other cannabis businesses must process daily transactions without basic banking services, they often accumulate large amounts of cash. Dispensaries are, therefore, frequent targets for criminals. Even as the cannabis industry matures and contributes significant tax dollars to State coffers, banks and financial institutions have no choice but to sit with their hands tied, watching with horror as organized criminals literally take aim at dispensary staff.

The passage of the SAFE Banking Act is literally life and death for many cannabis industry employees. How many workers and customers must suffer harm before the Senate wakes up and passes this critical bill? Regardless of their stance on cannabis, members of the Senate must do their jobs, heed the will of the American people and pass the SAFE Banking Act to rectify this increasingly dangerous situation for the good of their constituents.

In the rapidly evolving cannabis industry, in both new and emerging markets, securing a cannabis license is an essential step to establishing a successful business. However, navigating the application process can be complex, challenging and highly competitive.

To help aspiring entrepreneurs and investors in this burgeoning field, The Cannabis Business Advisors founder and CEO, Sara Gullickson, shares her top five ingredients for a successful cannabis license application. According to Gullickson, who has secured more than 75 licenses in over 30 states and five countries, these ingredients, when combined strategically, can significantly increase your chances of obtaining a coveted license and positioning your cannabis business for long-term success.

1. Real Estate

The author, Sara Gullickson (left) with Maxime Kot (right), president of The Cannabis Business Advisors

Real estate is the foundation of success. One of the key elements in a successful cannabis license application is securing suitable real estate. Many markets require applicants to have a designated location or property before even applying for a license. Finding the right property that complies with local zoning regulations and satisfies the specific requirements of cannabis operations is crucial. Partnering with experienced real estate professionals who understand the intricacies of the industry can be invaluable. By securing a well-suited location, you demonstrate to regulators your commitment to compliance and responsible business practices.

2. Finance

The cannabis industry brings its own set of unique challenges to navigate. The federal illegality of cannabis creates significant obstacles when accessing traditional banking and loans. Therefore, having a smart financial advisor and a comprehensive financial plan is essential for a successful license application. A well-prepared financial strategy, including accurate budgeting, projections and contingency plans, showcases your ability to manage financial resources effectively. It also demonstrates to regulators and investors that you have a sustainable and profitable business model, even amid industry uncertainties.

3. Community Support

Building strong relationships with the local community is crucial for a successful cannabis license application. Engaging with community leaders, neighborhood organizations and residents is a way to demonstrate your commitment to being a responsible and contributing member of the community. Actively seeking input, addressing concerns and incorporating feedback can help alleviate potential opposition and increase your chances of receiving support from local authorities during the licensing process. Community support is a powerful asset that showcases your dedication to fostering positive change and creating economic opportunities within the region.

4. Industry Experience

Value the expertise of the pioneers. While the cannabis industry is still nascent, there are seasoned industry pros who have been navigating its intricacies for over a decade. Leveraging their expertise and industry knowledge can be instrumental in crafting a successful application. Collaborating with experienced consultants and advisors who understand the unique challenges and nuances of the cannabis industry can provide invaluable guidance throughout the licensing process. Their insights into compliance, operational best practices and regulatory requirements can help you develop a robust application that stands out among competitors.

5. Team

The composition of your team is the cornerstone of your success and plays a vital role in the success of your cannabis license application. Assembling a knowledgeable and diverse team with expertise in various aspects of the industry is essential. From cultivation and manufacturing to retail and compliance, each team member should bring specialized skills and experience that align with your business objectives. Demonstrating a well-rounded team with a track record of success increases your credibility and instills confidence in regulators and investors alike. Your team represents your brand and serves as the backbone of your operations, making it crucial to prioritize hiring and cultivating talent.

Securing a cannabis license is critical to establishing a successful business in the rapidly growing cannabis industry. By focusing on real estate, finance, community support, industry experience and a strong team—you can significantly enhance your chances of success in the licensing process. Partnering with experienced consultants, leveraging the knowledge of industry veterans and demonstrating a commitment to compliance and responsible business practices will position you for long-term success in this dynamic and evolving industry.

A report issued three years ago by the Department of Treasury, Treasury Inspector General for Tax Administration (TIGTA), states that the IRS will begin to increase its audit of cannabis businesses throughout the country. The report, released on March 30, 2020, states that the IRS believes that most cannabis businesses have not accurately applied IRC 280E and as a result cannabis businesses could potentially owe hundreds of millions of dollars in outstanding taxes. This determination is based on an audit of tax filings of cannabis businesses in tax year 2016.

TIGTA conducted an audit of cannabis businesses in three different states, California, Colorado and Washington. Of the businesses audited, TIGTA determined, as a result of the incorrect application of IRC 280E, that 59% of those businesses required adjustments to their returns. These adjustments totaled over $48 million in unassessed taxes for 2016. The results of this audit caused the IRS to consider auditing cannabis businesses throughout the country where medical and/or adult use cannabis is sold. According to experts, cannabis (plant touching) businesses can expect an increase in tax returns to be audited now that the IRS has begun to increase their staffing resources and their ability to conduct most audits virtually.

Although the report calls for the IRS to develop guidance for the cannabis industry, the resources available are not very helpful nor does it provide the guidance that plant touching business owners need to make sure they are audit ready because audits have begun in Massachusetts, Michigan, Arizona, Oregon, Washington and Colorado.

As a plant touching business owner, you need to be prepared for a potential audit of your tax returns. To be prepared you should have the right tools to help you perform cannabis accounting. You will need to implement sound policies and procedures.

Preparation is Key

As a plant touching business owner, you should always be prepared for a potential audit whether by the IRS for IRC 280E compliance, or a financial state audit as a requirement by your investors. To prepare for an IRC 280E audit, you must first have an accounting and reporting system set up to perform accounting for your vertical – dispensary, cultivation or manufacturing business. This will include a chart of accounts for your business type because this is the foundation for your accounting system and help to track all transactions that are specific to your particular operation. It will simplify recordkeeping for recording revenue, inventory, cost of goods sold as well as direct and indirect labor costs. It will also help with maintaining your library of documentation that is tied to each transaction. The level of detail will enable you to perform accurate cost accounting as well as provide backup for how your accounting team arrived at their calculations. In addition to having a robust chart of accounts and a document library, you will also need to have written policies and procedures.

The 3 P’s – Policies, Procedures & Processes

The key to making sure you are always audit ready is to implement sound policies, procedures and processes. You want to make sure you have written accounting policies that provide guidance on how your business performs various accounting tasks. It should reflect requirements based on Generally Accepted Accounting Principles or could reference IRS requirements per IRC 280E and/or IRC 471-11. For example, you should have an accounting policy for how your organization values inventory which is important for plant touching businesses.

You should also have Standard Operating Procedures (SOPs) that provide step by step instructions on how specific tasks are performed. This will make sure that everyone within your organization is performing the various tasks the same. Your SOPs should be for all key tasks within the organization, especially those tasks that affect how transactions are recorded in your accounting system. It ensures accuracy and reliability of your financial statements.

Organizations should go a step further and create end-to-end business processes that go a step beyond SOPs. End-to-end processes are created from sequential steps that will allow auditors to follow each step to identify key controls, assess risks as well as potential fraud within an organization. Although having detailed end-to-end processes for your business is not a requirement, they do provide an extra layer of proof of the accuracy of your financial statements because you will have identified your key controls, mitigated potential risks associated with misstatements in your financial statements, and identified risks associated with fraud.

Although no one knows when or if their business will be audited, being prepared is the key to a less stressful and more successful audit. Being able to show an auditor items they may request but also having organized, easy to reference documentation that provides a detailed look at your accounting and reporting operations shows that you are serious about your business and you want to operate compliantly.

Remember those heady days of the Green Rush a decade ago, when markets were small and it seemed everyone had a chance? Now it’s more of a mad rush to get some green in the form of investment capital.

The majority of states in the country now have some type of legal cannabis market. Businesses in those states operate in spite of regulations that are restrictive, confusing and make it very difficult to make a profit. Meanwhile, heavy tax burdens, differences in enforcement techniques and varying degrees of oversight are other factors that influence bottom lines in the cannabis industry.

Saturated markets are giving businesses trouble when it comes to their bottom line

Inflation also continues to be a prominent force across world markets. Sales of cannabis products have fallen as consumers adjust to inflation and post-COVID supply chain issues that are causing higher prices on necessary staples like food and gas. An oversaturation of cannabis flower is becoming a perennial problem in some states and another factor causing industry distress.

When cash flow slows to a trickle, companies of all sizes seek out investment funding to keep their momentum. But catching the eye of an investor group requires more than just sticking your hand out.

What Attracts Potential Investors?

A company is best positioned to attract those interested in cannabis investment opportunities when it appears serious about its growth plans. That means being well positioned with a solid upper-management foundation and so much the better if there’s an advisory board in place too. A company built with a diverse group of talent—ideally from consumer packaged goods companies—presents an attractive opportunity for investors.

Talent from the CPG space can help attract investors

Top-quality and industry savvy finance employees who maintain sound financial books and establish a solid banking arrangement are also important. If the company’s financial scenario is robust enough to provide confidence in case of an audit and the books are in good shape with auditable METRC logs investors will be far more inclined to put money on the line.

A cannabis company with full inclusion (or seed to sale) is often a smart choice for investment. The vertical integration of cultivation, processing/manufacturing and retail allows them to sell their own products while also stocking other brands’ products on the floors of their dispensaries. If their products are respected and the brand is held in high regard, even better. Similarly, a cultivation enterprise that can grow crops for multiple brands can also be very attractive. The ability to pivot and adjust production to reflect the market and consumer demands indicates a strong business foundation.

Despite the current headwinds and saturated markets, other chances for growth exist. When a local municipality finally decides to “opt-in” to adult-use cannabis sales, there’s opportunity for both established brands and startups. It’s a matter of being ready for those opportunities and having a plan to leap in whenever new licenses become available.

What Businesses Will Struggle to Attract Investment?

Culture is key here. Poor employee relations and weak cohesion across departments are indicative of deeper problems. Do people actually want to work for the business? Do they feel supported by human resources? A company with underdeveloped or non-existent workers’ compensation policies and a management team that is not respected by its employees is not going to look good in the eyes of potential investors.

Non-diversified cannabis businesses are also at a major disadvantage when seeking investors. Cultivators of one type of product or service are locked into a single operation geared to do one thing. Any changes to market whims or problems with the supply chain can wreak havoc on a business based around a single product.

Stick to Business Basics

The cannabis industry is unique, but the basics of running a business well enough for success still apply. Strictly adhering to the traditional methods that any successful organization follows is extra important in cannabis. Businesses that are active in their community and make a real effort to be involved will be held in higher regard by investors. They want to see cannabis businesses that are not just setting up shop to make a quick buck, but are dedicated to bettering their community. That indicates a relationship with customers that involves mutual respect and promotes business longevity and financial stability.

For U.S. venture capitalists (VCs), the burgeoning European cannabis market provides opportunities to break into the industry on the heels of adult-use legalization. Germany has set its sights on implementing a recreational market by 2024, and the country, along with several other European Union (EU) countries–Malta and Luxembourg–came together in September 2022 to draft a joint statement on why the EU needs a new approach to cannabis use for adult-use production, sale and consumption.

Photo: Ian McWilliams

In October 2022, Germany took further steps to solidify its plans for legalization further when its Health Minister Karl Lauterbach presented a cornerstone paper on planned legislation to regulate the controlled distribution and consumption of cannabis among adults. Such actions have signaled to both the EU and the world at large that cannabis legalization in Germany is imminent, and the country is championing the new age of cannabis policy.

With the new German cannabis market soon to be on the horizon, both foreign and domestic VCs are considering how to best leverage investment opportunities into existing cannabis companies within the current medical-only market that will transcend into adult use. For U.S. investors, it’s important to do their due diligence to find the company that will transcend into the next progression of cannabis policy. In addition, European cannabis companies must do their own meticulous research when it comes to aligning with investors to meet both their financial and business goals.

How U.S. VCs Can Evaluate Investment-Worthy European Cannabis Companies

As with any investment, VCs benefit from researching the company and market they are planning to invest in. Regarding the company of interest, it’s important to examine which part of the cannabis market the company is serving: growers, retailers, ancillary products, service providers and biotechnology companies all exist as potential investment options within the space. An investor should look into a company’s annual revenue, evaluating whether it has increased, remained steady or decreased over time. Revenue growth is often provided on a company’s income statement.

In addition to making sure they have a thorough understanding of the business model and its value proposition, investors should also familiarize themselves with the company’s management team to make sure that they are knowledgeable and experienced in both running a company and the cannabis industry. For those interested in entering the German market, VCs should consider the businesses that are currently key players in the country’s medical cannabis industry and that plan to expand their services into the adult-use sector once legalization comes into play.

For example, Tilray, founded in 2014, was one of Canada’s first licensed medical producers. When Canada legalized adult-use cannabis several years later, in 2018, Tilray was one of the companies that successfully transitioned to expand its market share in Canada’s medical to the adult-use cannabis industry.

Another consideration for VCs is the reputation of the business and its leaders. Investors should seek out those who have become authorities within the industry and the movers and shakers who are providing key insights into the market. These business leaders should be front and center, discussing everything from current operations and compliance to cannabis policy and legislation to new endeavors and growing their businesses. With recreational cannabis legalization being a completely new endeavor for the EU, it is important for leaders within today’s European medical space to be visionaries for the next phase of cannabis legalization and be guides for creating regulations for this new market to be safe, sustainable and scalable.

In addition to executive teams, VCs should check if the business is meeting the current marketplace’s expectations and is ready to adapt and evolve as needed. This means that the company has access to a steady supply of high-quality cannabis at an affordable price and access to consumers (medical patients) and potential consumers. With adult-use legalization soon to be a reality in Germany, investors must consider which players in the medical-only market will be able to not only survive the transition but grow to become leaders in Germany’s new recreational market and within the EU as a whole.

What Do European Companies Look For in Terms of U.S. VCs

Just as VCs must find the right fit for them in terms of investments, cannabis companies must also align with investors that help them meet their financial and business goals. For cannabis companies, many seek to align themselves with VCs experienced in consumer, technology, and healthcare investments. While there are benefits to working with a VC with a cannabis background, companies should not deter investors who do not meet those specific criteria, as the cannabis market is still a fairly new and ever-transforming industry. In light of this, it’s important that investors approach opportunities with an open mind for both the industry’s current state and its potential.

The European Union

As with most investments, both VCs and companies should be prepared to agree to a term sheet, a document that outlines the relationship between the investor and the business. An ideal investor would need to be supportive, well-connected, and add value by providing relevant business knowledge. While some investors seek a more hands-on role, in most cases, the VC’s support will not be equal to the business’s micromanagement or control of its day-to-day operations. Generally, those responsibilities would remain with the company’s executive team.

As an investor, it’s important to be supportive of the business; be a cheerleader for the company when things go well, and lift up the business when challenges occur. In addition, offering a network of referrals and strategies to excel is key to being a good asset to the business. Also, having a diverse portfolio of companies with synergistic opportunities can be very beneficial to growing cannabis businesses.

A question many investors ask before entering the space is how much in assets they should have on hand to be considered an eligible investment size. Typically, this depends on the business and its financial needs. Small profitable cannabis businesses that want additional financing may be able to secure a bank loan, if possible, in their home countries or seek a seed investment-focused VC for some capital. Leaders in Germany’s current medical-only market are seeking investors, both from the U.S. and abroad, to partake in Series A/B funding, seeking financial partners that can help them reach a goal of $20-80M USD.

European cannabis companies are within a high-growth market, so U.S. VCs looking to enter through investment do not have to go through a private equity firm. An investor can approach companies through networking or direct outreach. It is also important to note that investors do not have to convert their assets from USD to EUR, as it is done automatically when making investments. For the first time in 20 years, the USD and EUR are about equal, so now is a great time for U.S. investors to consider making the leap into European cannabis.

As the former CEO of Partner Colorado Credit Union (PCCU), Sundie Seefried has been in the credit union space for 39 years. Established in 2015, Safe Harbor Financial is now a leading provider for banking and financial services in the cannabis industry.

Seefried founded Safe Harbor as a cannabis banking program for PCCU, and since then it has withstood scrutiny of 16 separate federal and state exams. Entering its ninth year as a cannabis banking program, they have almost 600 accounts in 20 states and have processed over $14 billion in transactions for the cannabis market. In September, Safe Harbor began trading on Nasdaq under the symbol SHFS. The company has also announced a definitive agreement to acquire Abaca, an industry-leading cannabis financial technology platform.

Seefried has seen it all in the cannabis banking world. We wanted to get her thoughts on some current events, the future of cannabis banking and lending, and what the next few years might hold in store for an industry ready to grow.

Cannabis Industry Journal:Tell us a bit about yourself. What is your background and how did you find yourself in the cannabis industry? How did you get to become president and CEO of SHF?

Sundie Seefried, President & CEO of Safe Harbor Financial

Sundie Seefried: I’ve been in banking in the credit union space since 1983. I became CEO of Partner Colorado Credit Union in 2001 and stayed there for 21 years. Everything I do, I have a very conservative nature just from being in the banking world and doing things methodically and building good foundations that endure long term. In 2014 when FinCen issued guidance, I was supposed to retire, and I had dinner with some old friends that were attorneys who couldn’t get bank accounts for their clients in the cannabis industry. They asked me to help and I looked into it for them. I assumed the regulator would shut me down but he didn’t; he actually encouraged me to move forward and look further into things. As I educated the board, we saw just how unsafe Colorado was and the serious need for the community to figure things out with respect to banking and cannabis. Coming from that credit union perspective, I said I think we can do this, let’s try and I’ll go through the third parties necessary. And that’s how we got into this, just looking to try and help solve Colorado’s problems and get banking access for cannabis companies.

CIJ: Tell me about your company’s mission. What is your financing strategy in cannabis and of the companies you do business with, what do you look for most?

Seefried: Our mission remains the same, and that is to normalize banking in the cannabis industry as much as possible. Because the black market still exists, the issue becomes sorting the legal entities out from the illicit actors in the industry. We know that the illicit market is trying to hide amongst the legal environment, which really makes things difficult for upstanding cannabis businesses. We can normalize banking by making sure we help legitimize the compliant entities and sort out the bad actors. We really only want to work with legitimate players with licenses, who are fulfilling expectations on the regulatory level and have no problems with compliance. We have been able to do that on the depository side.

We have always been a low-cost provider and our clients count on that. As we move into the lending part of the industry, we’re looking to do the same thing. There are lenders who charge one-to-three percent per month, 18 to 36 percent per year. We, on the other hand, are targeting more of an eight to thirteen percent annual rate. More of a conservative approach. Real debt underwriting. No extremely high interest rates. We look for the collateral, we look for well-organized businesses and solid documentation. Those are the businesses we are trying to bring into the fold and offer them normal loans. Cannabis will always have a premium on it simply because it is illegal at the federal level and there are additional hoops we have to jump through. Because of the potential forfeiture and seizure, if there are bad actors, etc., it really behooves any clients coming to us to also place their depositary services with us so we can prove their legitimacy and provide loans to them.

CIJ: Let’s talk about the Canopy Growth news. They announced they are pulling the trigger on acquiring Wana Brands, Acreage Holdings and Jetty Extracts, under the Canopy USA holding company and ahead of federal legalization. On the surface, it looks like they are bypassing a lot of the hurdles American cannabis companies currently face with financial red tape. As a foreign company trading on the NASDAQ dealing with a schedule 1 substance, do you expect Canopy to have a significant, some would say unfair, competitive advantage with their early entry? Or is this perhaps more of a rising tide lifting all boats scenario? What effect will this have on the current market landscape?

Seefried: I find it a very interesting move on their part. Certainly, they have a big advantage in comparison to other companies. The consolidation in the industry is moving so quickly. Other players will keep up with this just as fast as Canopy is moving in. That’s my opinion in terms of what I see in the consolidation area of the market. I think what it really hurts is small businesses. My heart goes out to them. So many of them worked so many years to build excellent small companies with boutique shops, and this whole move will really change that part of the industry.

I see a lot of these small players, non-vertically integrated companies, being impacted in a negative way due to such mass consolidation and the entry of foreign businesses. We need to get more competitive on a global level in order for our companies to grow and thrive. This happened back in 2018, when so many companies started doing those reverse takeovers onto the Canadian Securities Exchange and suddenly, they were putting tens of millions of dollars into the U.S. market. People didn’t see that as a competitive disadvantage for American companies, but now this move by Canopy may really show that we have to look at things more globally.

CIJ: Biden’s announcement regarding the scheduling review for cannabis has a lot of industry folks very hopeful that federal legalization is closer to a reality than before. Do you share their optimism?

Seefried: Closer than before, yes. But how close? I am not convinced it will happen quickly. If they are really going to consider rescheduling or descheduling, everything happens in Washington very incrementally. Eight years and seven attempts at the SAFE Banking legislation and still no movement on that front. Tomorrow, we’re going straight to legalization? I have a hard time swallowing that one. I just don’t see that big of a jump all at once. I think it is interesting coming just before the midterms and votes are really needed now more than ever.

What Biden did was a great start. Especially for those people in prison for possession. The interesting part of it is, we are very serious about people who have used it, but the people who have sold it and are in prison might be in the same situation. Given how the laws worked for so long, just based on the amount of cannabis you had could get you automatically labeled as a dealer, which isn’t the case for a lot of incarcerated folks.

The fact is, the social equity and justice issue, who do you free or who do you not free from prison, is a very difficult issue to get through. I think it is a great step forward and it will help some people who were treated unjustly, but there is still a lot of work to be done.

“I believe we’ll start seeing pressure from the global market on the United States to move things along a little faster in our own country.”As far as rescheduling, if they go from a Schedule I drug to a Schedule II drug, that will do no good, but it certainly is a bone to throw to the industry if you want to look like you are making some progress. Schedule II is still subject to 280E tax code so it will only do so much. If they want to make things more equitable and actually level the playing field, they have to do something about the 280E issue hindering every cannabis business in the country.

As far as full legalization, I am not optimistic because of all the players that need to be involved. Full legalization will require a change to the IRS tax code 280E as well as other tax issues. I think there are too many players: The DOJ, FinCen, the DEA, the FDA, the IRS. All of these agencies will have to agree on full legalization and moving forward in unison. The DEA is trying to fight illicit actors and illicit drugs. FinCen is trying to follow the money to find illicit actors. As long as there is an illicit market it will make their job tough, and on top of all of that, we have politics in play. That is just my take on legalization. It is going to be a much more complex problem than just legalizing the plant and moving on. Rescheduling seems like lower hanging fruit, but they will have to move it higher than a Schedule II.

CIJ: With the midterm elections here, there are a number of legalization measures in a handful of states, along with political control of Congress on the ballot. How do you think a Republican or Democrat controlled Congress will affect cannabis legalization progress?

Seefried: I just finished doing some lobbying in September in DC and spoke to some Senator offices in person, and I heard a lot of interesting topics being discussed. One of the things that keeps popping up is that social equity and justice is a huge issue. If we can’t solve this injustice in our system that has been going on for decades and decades, maybe they’ll hold banking legislation hostage. You can’t correct 50-60 years with one piece of legislation. Everything has to be incremental, unfortunately, so there will be some give and take there. I think that was a primary focus, especially with the Democrats and I do think it is a worthy cause.

On the Republican side, economically improving our competitive advantage as a country. They are starting to see the jobs being created and the tax revenue coming in and the growth of the industry. They will have to make that decision at some point in time whether they are going to leave the American cannabis industry behind or allow them to compete on a global level. I really think everything will move slowly and continue as it has happened in the past.

I believe we’ll start seeing pressure from the global market on the United States to move things along a little faster in our own country.

CIJ: As we inch closer to 2023, what do you expect the next year to offer for the cannabis financing market?

Seefried: I would say, with or without legislation, they’re finding greater access to banking. And the reason they are getting better access to banking is because none of us have been prosecuted for simply engaging in cannabis banking. I think we have set a precedent over the past eight years, not only us but other service providers in the industry and that we are not being prosecuted.

I see more financial institutions entering the market slowly. The second reason access to capital and banking will increase is because every financial institution in the country wants that lending relationship. In order to get there, they want to start with the depository relationship, and they don’t want smaller players presently doing it and getting all of those relationships before they enter the market. I think the competitive nature of the financial industry to land that lending relationship is going to force them into the game sooner than later.

Businesses often require outside capital to finance operating activities and to enable scaling and growth. Financing in the cannabis industry is notoriously challenging with regulatory obstacles at the local, state and federal levels. Recent market dynamics pose additional challenges for both financiers and cannabis operators.

We sat down with Matt Hawkins, Founder and Managing Partner of Entourage Effect Capital (EEC) to learn more about EEC and to get his perspective on recent market trends.

Aaron Green: In a nutshell, what is your investment/lending philosophy?

Matt Hawkins, Founder & Managing Partner at Entourage Effect Capital

Matt Hawkins: Entourage Effect Capital’s long history and experienced leadership allow us to access and construct high potential later-stage growth investments with sought-after industry leaders. We want to get ahead of what is happening on the regulatory and federal level to build scale with our investments.

Green: What types of companies are you primarily financing? What qualities do you look for in a cannabis industry operator or operating group?

Hawkins: Essentially, we are focused on investing in companies that will benefit the most when legalization occurs. We are currently working on multiple such deals, and separately, we are excited by how our newly minted, early-stage focused Arcview Ventures Seed Fund will provide a pipeline to the next generation of leading growth opportunities. When evaluating opportunities, we always look for the potential for scale and a strong management team.

Green: Capital market dynamics have led to significant public cannabis company revaluations in 2022. How has this affected your business?

Hawkins: As an industry, we all want companies to be valued for what they are worth, and right now, there are a lot of companies where that’s not the case due to the downturn in valuation. For us, it works the other way, because we are now able to invest at lower valuations with the hope of more upside when valuations reset.

Green: Debt on cannabis companies balance sheets have increased significantly in recent years. What is your perspective on that?

Hawkins: Debt is at its highest in industry. Operators don’t want to take equity capital at this point because valuations have come way down. However, we are lucky to have been in this business for a long time so that we can create our own deals. Our reputation precedes us — as a result, combined with the strength of our portfolio, people want us in their capital stack.

Green: How does the lack of institutional investor participation in the cannabis industry affect your business?

Hawkins: The lack of institutional capital in the industry makes it difficult for a large chunk of companies to grow and scale. For the industry to grow, there needs to be a different type of investor, investors who are not scared to go through the peaks and valleys we go through as an industry, whereas retail investors take their losses and move on. Everybody’s competing for the same small pool of money; managing cash is the most important factor for operators, whether private or public, big or small.

Green: What would you like to see in either state or federal legalization?

Hawkins: The illicit market still has a strong presence, and until we get regulatory reform, it’s going to continue. Reducing the tax burden on legalized markets would bring more revenue to both operators and the government because they’d reduce the market share of the illicit market, with the price offset trickling down to the retail customer.

Passing the SAFE Banking Act would create consequential changes for the cannabis industry. There is also a small chance that the New York Stock Exchange and the Nasdaq could start listing legal plant-touching businesses. If that happens, more institutional capital would enter the market and flush the industry with cash, with market caps going way up. There is a lot of unease and uncertainty with retail investors that prop up the stocks in the space, and it will continue until there is regulatory movement, even on the private side.

Green: What trends are you following closely as we head towards the end of 2022?

Hawkins: I don’t see anything happening unless the SAFE Banking Act passes. Otherwise, things are status quo, especially with public companies. For private companies, we’re going to see a lot more consolidation, especially in California.

Businesses often require outside capital to finance operating activities and to enable scaling and growth. Financing in the cannabis industry is notoriously challenging with regulatory obstacles at the local, state and federal levels. Recent market dynamics pose additional challenges for both financiers and cannabis operators.

We sat down with Travis Goad, Managing Partner of Pelorus Equity Group to learn more about Pelorus and to get his perspective on recent market trends.

Aaron Green: In a nutshell, what is your investment/lending philosophy?

Travis Goad: Our investment and lending philosophy is focused on being honest, upfront and doing what we say we’re going to do for both our borrowers and our investors. At Pelorus, we lend against cannabis-use real estate assets.

Every lender in this space is a hybrid between real estate and corporate lending. However, if you think about it as a political spectrum, with one side being pure real estate lending and the other pure corporate lending, Pelorus is as close as you can be to pure real estate lending in this sector while also being properly collateralized. What sets us apart from our recently launched lending peers is that we lend against the real estate asset value only, even though we’re collateralized by the real estate and license.

We lend between 60% to 75% of the value of the real estate, which means sponsors need to raise equity for the 25% to 40% remainder of the project cost. This allows us to be covenant-lite for our borrowers while giving them the flexibility to grow their business as they see fit.

Travis Goad, Managing Partner at Pelorus Equity Group

The other lending options in the space are much different. While our lending peers may call themselves mortgage REITs, they really are based on a business development company (BDC) lending model. While they may lend borrowers as much as 150% to 180% of the real estate value, they will require significant financial covenants, require control of major decisions and most often want a board seat. We’ve seen this model severely hamstring growth of companies.

The third option available to sponsors is a sale-leaseback. In this structure, lenders will buy your real estate for 100% of the value, but require you to enter into a 15-to-20-year lease that increases 3% each year. There is a temporary benefit to this model from a federal tax perspective, but that will go away when 280E is addressed, either by descheduling cannabis or amending the tax code.

While this structure means you don’t have to raise equity, it gives up the most valuable asset cannabis companies have in the early stages of the industry. Once you sell this asset, it hampers optionality for sponsors – and in a fast-growing industry like cannabis – optionality is the most critical thing a company has. Pelorus’ structure allows maximum optionality, as well as the ability to lower your cost of capital as the industry matures.

From an investor standpoint, they should know that the BDC and sale-leaseback models are a lot riskier than our model. While we’ve seen those models work well in mature industries, we think the cannabis industry is too early-stage and too volatile to go that far out on the risk spectrum. We have the longest history in the space of deploying capital successfully and seeing it returned. Prior to making any loans, we spend a lot of time underwriting the company we’re working with, the real estate and the projections. We look for strong sponsors, great projects and attractive markets.

Before we entered the cannabis lending space, our team at Pelorus had more than 5,000 transactions under our belt, worth $5B, and we leveraged our decades of underwriting experience when starting the Pelorus Fund. As the first dedicated lender in the cannabis space, we have more data and experience than anyone in terms of transactional volume – we’ve looked at more than 2,000 deals and have made 71 deals, worth $468M. We know the intricacies of every market, the particular ordinances, what the costs should be, and utilize the data to help our borrowers succeed. Through our deals and sustained success, we’ve made a name for ourselves as the most trusted and efficient lender in the cannabis space.

Green: What types of companies are you primarily financing?

Goad: We finance construction and stabilized loans for a range of clients including MSOs, SSOs and ancillary companies. We don’t lend on outdoor cultivation, but are open to working with any cannabis-related business that has commercial real estate, strong financials and experience in the cannabis space. Today, our sweet spot is closing loans in the $10M to $30M per transaction range, but we can fund loans $100M+ and as low as $5M. Since 2016, we’ve financed 4.2M feet of cannabis-use properties for a total of $468M in loans – roughly 15% to 20% of the entire US market.

Green: What qualities do you look for in a cannabis industry operator or operating group?

Goad: We are meticulous in our underwriting process and underwrite the company, the real estate and the market. We’re one of the few lenders today that has capital to deploy, which has given us the opportunity to continue to take market share while also increasing the quality of our borrowers. Whether you’re an MSO, smaller state operator or ancillary business, we recognize quality across the sector. Brand affinity and shelf space are critical in this market, and we like working with companies that have a competitive edge in getting their branded product to customers. We try to target companies that offer a unique product, or have a unique position within the state they are located.

To qualify for our lending program, borrowers need to own their real estate. If the sponsors own the real estate or intend to own the real estate, we offer two main lending products: we provide construction loans that range between 60% to 75% of the project that are typically 18-month terms; and more recently implemented, we also lend on fully stabilized assets that are cash flowing and operational up to 75% of the value and up to a 5-year term.

By the time a borrower comes to us, they should already have a license (or be acquiring a license at closing), have their required equity raised to completely fund the project and have all local approvals to begin construction.

Green: Capital market dynamics have led to significant public cannabis company revaluations in 2022. How has this affected your business?

Goad: As far as how market dynamics have impacted our fund, we’ve been pretty insulated because we are a privately held company. From our inception, we’ve worked hard to create an innovative model, and have had many firsts. We were: the first dedicated lender in the cannabis sector; the first lender to become a private mortgage REIT; the first to be issued an FDIC warehouse line of credit; the first to get an investment grade rating; the first to issue an unsecured bond with institutional investors; the first to update our fund to a billion dollars. Amid all these firsts, we made a conscious decision not to go public. This has been one of the best decisions we’ve made and has shielded us from much of the market volatility we are seeing.

As for the broader market, we’ve seen our sponsors that are publicly traded impacted pretty significantly by the recent market dynamics. We’ve also seen flow-on effects for non-publicly traded firms. Our loan book is performing excellently, but we’re in a very challenging market for marijuana-related businesses to raise equity, making debt even more attractive. For most of our competitors, who chose to go public, they’ve been unable to raise much capital to deploy, whereas our market share is increasing and we continue to grow in this tough environment. We remain bullish on the sector in the medium/long term and are finding excellent opportunities to lend in this challenging environment.

Green: Debt on cannabis companies balance sheets have increased significantly in recent years. What is your perspective on that?

Goad: Increased access to debt capital markets is a sign of a maturing market. The U.S. cannabis sector has a great tailwind with growth of new markets, but it’s facing some significant headwinds tied to tax inefficiencies and inadequate state-level enforcement. All of these issues can be solved with political action, but so far that hasn’t happened and it’s causing pain in the industry. These industry dynamics are set against a broader macro backdrop of risk-asset repricing and increased volatility, which leads to outsized volatility in cannabis due to limited liquidity. That increased volatility has made it very challenging to raise equity in this market.

For companies that have strong assets on their balance sheet, they’re still able to access capital via the debt markets. This is creating clear winners and losers, as companies that choose to sell their real estate have significantly fewer capital raising options than those that choose to keep real estate assets on their balance sheets. Overall, this increased debt trend has been great for our business – our pipeline has increased rapidly and we’re able to lend to strong operators with solid assets at attractive rates for investors. Our fund continues to have inflows, and since we’re one of the few lenders with capital to deploy, we’re still open for business and deploying capital in this challenging environment.

Green: How does the lack of institutional investor participation in the cannabis industry affect your business?

Goad: The current regulatory environment impacts the type of investor that comes into this space. Rather than being dominated by institutions, this sector has largely been funded by retail investors and family offices. This has created challenges in aggregating large amounts of capital, both on the operator and the debt-fund side of the business. It can lead to delays in loan closings, as it takes borrowers a longer amount of time to raise the required equity to close their transaction. As we’re seeing with our publicly traded peer group, it can also lead to lenders having trouble raising capital to deploy. As for Pelorus, we’ve been very fortunate that our length of time in the industry and track record of successfully making loans and having them repaid has set us apart in fundraising. Our decision to stay private has been a critical factor in our fundraising success as well. Overall, the lack of institutional investor participation is a double-edged sword: the lack of liquidity has caused challenges broadly, but since we’ve had significant capital to deploy, it’s created great opportunities for us to make loans with attractive risk/returns in this challenging market.

Green: What would you like to see in either state or federal legalization?

Goad: Given the stalemate in the Senate and the sharp bipartisan divide, I don’t think federal legalization will happen during this administration. That said, there are incremental actions that the government should take to strengthen the cannabis sector. First of all, the Cole Memo needs to be reinstated to add additional protections for cannabis and cannabis-related businesses. As 280E has clearly been detrimental to the overall health of the cannabis industry, we also believe the tax code should be amended, or better yet, we should address the conflict between state and federal policy. We also need to get SAFE Banking approved in order to open up the cannabis sector to credit cards and potentially open up banking to the sector in a more material way. Unfortunately, there’s a choke point in the Senate to get SAFE Banking approved, since there needs to be 60 votes to be filibuster proof. And while there is some talk of SAFE Banking passing during the lame duck session, we are not holding our breath.

Green: What trends are you following closely as we head towards the end of 2022?

Goad: The biggest trends we’re following are on the legislative front (both federally and at state level), which heavily impact revenue and net cash flow growth for the industry. We’re following emerging state markets, such as Alabama and Mississippi, as well as current medical markets poised to transition to adult use in the near term, such as Missouri. The more addressable the population, the faster the industry can grow.

We’d also like to see current legal states address the often-heavy tax burdens that have led to additional challenges for legal businesses and kept illicit markets thriving. No state got everything right at the beginning, but we’re starting to see states address some of the inequities and harmful policies now. California has made some progress in this area, however there are many issues that still need to be addressed.

Federally, 280E is the other major headwind that needs to be addressed as extremely high tax rates are one of the biggest problems for the industry. We’d really like to see that addressed, as cannabis is the only new industry, I’m aware of in the U.S. that has had such disadvantages out of the gate.

Business often require outside capital to finance operating activities and to enable scaling and growth. Financing in the cannabis industry is notoriously challenging with regulatory obstacles at the local, state and federal levels. Recent market dynamics pose additional challenges for both financiers and cannabis operators.

We sat down with Len Tannenbaum, CEO & Partner of Advanced Flower Capital Gamma (AFC Gamma, NASDAQ: AFCG) to learn more about AFC Gamma and to get his perspective on recent market trends.

Aaron Green: In a nutshell, what is your investment/lending philosophy?

Len Tannenbaum: AFC Gamma is one of the largest providers of institutional loans to cannabis companies nationwide in all aspects of production: cultivation, processing, and distribution. Cannabis companies, no matter the size, traditionally lack the lending opportunities that other enterprises have available, and that’s where AFC Gamma comes in. As an institutional lender, we provide financial solutions to the cannabis industry.

AFC Gamma is a commercial mortgage REIT that provides loans to companies secured by three pillars: cash flows, licenses, and real estate. We provide term loans, draw facilities, and construction loans. Each loan is unique and tailored specifically to meet the needs of our borrowers. This unique partnership approach with our clients allows us to find solutions to help them expand and grow alongside them.

Since starting AFC Gamma, we have completed almost $500 million of transactions. We provide capital to an industry that others do not and, in turn, allow these operators to build cultivation facilities, production facilities, and dispensaries.

Green: What types of companies are you primarily financing?

Len Tannenbaum, CEO & Partner of Advanced Flower Capital Gamma

Tannenbaum: AFC Gamma seeks to work with operators, ideally in limited license states. We make loans to companies secured by three pillars: cash flows, licenses, and real estate. We tend to lend to operators in regulatory-friendly states, such as: Ohio, Pennsylvania, New York, New Jersey, Maryland, Massachusetts, Arizona, New Mexico, Missouri, Illinois, Michigan, and Nevada. Traditionally, we shy away from states like California, Washington and Oregon given our approach to lending. We have 16 borrowers in 17 states, and what we look for are companies that we can grow with over the long term.

Green: What qualities do you look for in a cannabis industry operator or operating group?

Tannenbaum: We tend to work with three different buckets of operators. You have the large publicly traded multi-state operators (MSOs) we have lent to, such as Verano. Then you have the tier right below the top tier MSOs, where you have some public enterprises like Acreage, who is one of our borrowers, and then some private companies such as Nature’s Medicine and Justice Grown. The third tier are smaller operators. They’re single or two-state operators, and we’re typically coming in to help them build out licenses that they want or help them expand within that state. That’s why state-by-state dynamics are so important to us and why we typically only lend to limited license states.

We look at portfolio diversity on a step-by-step basis rather than a borrower-by-borrower basis. We tend to focus on deals in limited license states and also deals that have real estate as collateral. We have found that REIT loans give our clients the most flexibility, and we are able to finance more companies this way.

Green: Capital market dynamics have led to significant public cannabis company revaluations in 2022. How has this affected your business?

Tannenbaum: Although capital market dynamics have made an impact on a significant number of public cannabis companies’ revaluations this year, our overall business hasn’t been affected too much and that’s because the other lending options available right now are not ideal choices for most borrowers. One of the ways a lender can achieve credit enhancements or securities is by raising capital in the public markets. When the markets are more challenging, those companies have a harder time accessing capital when they may need it most. In turn, this could cause slow growth overall, more cash conservation and it removes one of the benefits to lenders. We’d like everyone to have more robust equity from that standpoint, but the flip side is, if equity gets too high in price, those borrowers won’t come to us lenders and they’ll raise capital in the equity markets since the equity is cheap. We’re definitely conducting a lot of business because the equity market is not available to cannabis companies. If that were to change, while our loans would be theoretically safer, they would choose equity instead of debt.

Green: Debt on cannabis companies balance sheets have increased significantly in recent years. What is your perspective on that?

Tannenbaum: When equity markets were free and the valuations were high, cannabis companies raised money in the equity markets rather than take on debt. Now that the equity markets have been somewhat closed and valuations are much lower, we see their debt has increased over the past two years.

Green: How does the lack of institutional investor participation in the cannabis industry affect your business?

Tannenbaum: Right now, we are one of the biggest lenders in cannabis. Looking to the future, though, if the SAFE Banking Act passes, we could see an influx of institutional capital that would increase competition amongst cannabis-specific and mainstream lenders. From the outset, most of the competition will come from hedge funds, not big banks. This competition will drive down interest rates and attract borrowers like MSOs.

Green: What would you like to see in either state or federal legalization?

Tannenbaum: The Senate passing the SAFE Banking Act. Should this happen, lenders, including AFC Gamma, will be able to borrow cheaper, which will, in turn, allow lenders to lend cheaper. It will be a net positive for all operators. It could also be positive for lenders assuming they have the infrastructure and capabilities to scale and decrease the cost of capital once the money starts flowing and more deals are being made.

Green: What trends are you following closely as we head towards the end of 2022?

Tannenbaum: The most important trend we’re following is state by state trends. We’re excited to see new states getting their act together like New York. We’re excited about Georgia. We’re also looking forward to Missouri going rec. On the flip side, we’re also watching Virginia issue more than 400 licenses, diluting down the limited license states into basically an unlimited license state, which personally doesn’t make sense.

The other trend we’re watching across the country is cannabis prices. There is definitely a gray and legacy market that goes across border that should be enforced. That flow of cannabis product is depressing prices, especially in the unlimited license states. I believe there is a chance that trend starts reversing as many grows are now inefficient. The low end of inefficient grows are going to start closing, which may increase prices going into next year.

Mergers and acquisition activity in the cannabis space tripled from 2020 to 2021, and that pace is on track to continue in 2022. With big players entering the global cannabis market, we’re fielding more questions about mergers and acquisitions of cannabis businesses.

In this guide, we look at the evolution of the U.S. cannabis industry and some best practices and considerations for M&A deals in this environment.

The New Reality of Cannabis M&A Activity

The industry has evolved since adult use cannabis was first legalized in some U.S. states in 2012. More cannabis companies have a professional infrastructure—legal, financial and operational—with executive teams and board members ensuring the organization establishes proper governance procedures. Investors and private equity firms are showing more interest, and some cannabis companies have celebrated their first IPOs on the Canadian Securities Exchange (CSE).

At the same time, we are seeing a kind of “market grab” by multistate operators (MSOs) looking to acquire various licenses and expand their market share. MSOs tend to understand the current state of the market. For example, in California and some other states, there is a surplus of cannabis on the market for various reasons, partially due to so-called “burner distribution”—rogue distributors using licenses to buy vast amounts of legally grown cannabis at wholesale prices and selling the product on the black market, thereby undercutting retailers and other legal cannabis businesses. Another reason for the surplus is simply the entrance of many legal cultivators into the market over the past year.

Due to these trends, MSOs are interested in acquiring the outlets to be able to sell the surplus cannabis within California and other new markets.

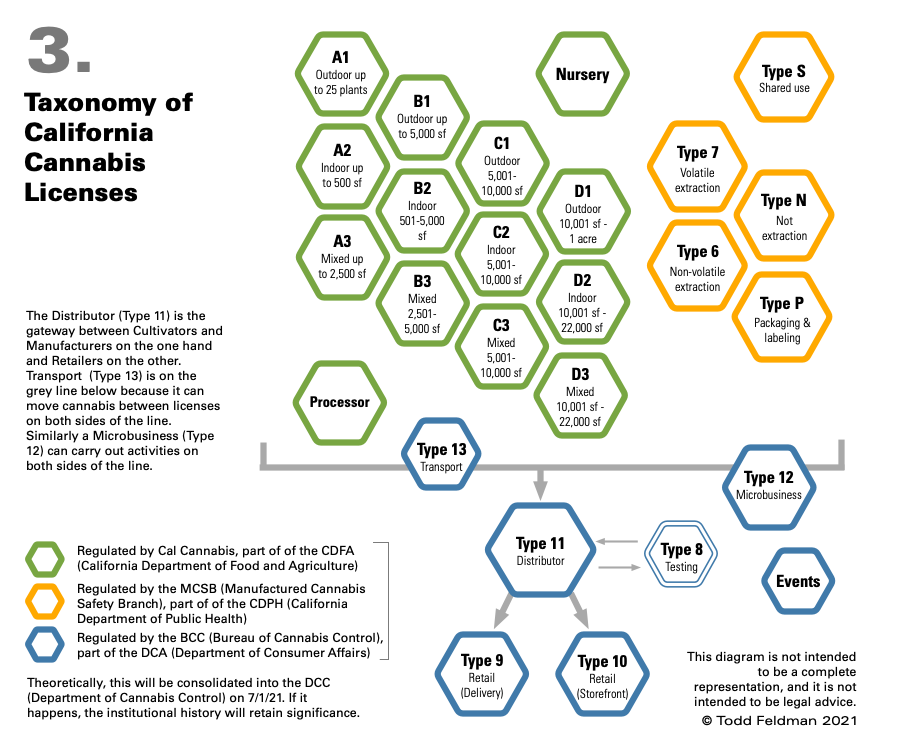

Transferring Cannabis License Rights

One of the biggest challenges to M&A activity in the cannabis sector is the difficulty of transferring or selling a cannabis license.

Different types of cannabis licenses in California

Cannabis licenses are not expressly transferable or assignable under California law and many other states. However, the parties involved aren’t without options. For example, a business that is sold to a new owner may be able to retain its existing cannabis license while the new owner’s license application is pending, as long as at least one existing owner is staying on board. At the state license level, a change of up to 20% financial interest does not constitute a change in ownership, although the Bureau of Cannabis Control (BCC) must be notified and approve the change.

This process can take a while—often a year or more—since licensing involves overcoming hurdles at the local level as well as the state level with the BCC. It’s crucial to talk with legal counsel about the particulars of the license and location early in the process to best structure the terms of the agreement while complying with state and local requirements.

Seeking a Tax-Free Reorganization in the Cannabis Space

In many cannabis mergers and acquisitions, the goal is to accomplish a tax-free reorganization, where the parties involved acquire or dispose of the assets of a business without generating the income tax consequences that would result from a straight sale or purchase of those assets.

IRC Section 368(a) defines various types of tax-free reorganizations, including:

In a stock-for-stock reorganization, all of the target company’s stock is traded for a portion of the stock of the acquiring parent corporation, and target company shareholders become minority shareholders of the acquiring company.

Often, it’s tough to meet the requirements to qualify for this type of tax-free reorganization because at least 80% of the target stock must be paid for in voting stock of the acquirer.

Additionally, companies may be saddled with too much debt. If the acquirer assumes that debt, it may be classified as consideration paid to the seller and therefore disqualify the transaction as a tax-free reorganization.

In other M&A deals, the acquiring corporation may be unwilling to assume the debt of the target corporation—perhaps because showing these items on its balance sheet would impact its debt-to-equity and other financial ratios.

Rather than acquiring the target company’s stock, the acquirer may purchase its assets. In a stock-for assets exchange, the buyer must purchase “substantially all” of the target’s assets in exchange for voting stock of the acquiring corporation.

A stock-for-assets format offers the buyer the benefit of not having to assume the unknown or contingent liabilities of the target. However, it’s only feasible if the acquirer purchases at least 80% of the fair market value of the target’s assets AND all or virtually all of the deal consideration will be stock of the acquirer.

Tax Consequences Arising from Sale of Assets

If the sale price doesn’t consist primarily of the buyer’s stock, the transaction may be a standard asset sale. This leads to very different tax results.

If the seller is a C corporation, it will typically face double taxation—paying tax once on the sale of assets within the corporation and again when those profits are distributed to shareholders. If the target company has net operating losses (NOLs), it can use those NOLs to offset the tax hit.

If the seller is an S corporation, it won’t have to pay corporate tax on the transaction at the federal level. Instead, shareholders will pay tax on the gain on their individual returns.

For the buyer, the benefit of an asset sale is that the assets acquired get a “step-up basis” to their purchase price. This is beneficial from a tax perspective, as the buyer can depreciate the assets and may be able to claim accelerated or bonus depreciation to help offset acquisition costs.

The subsidiary merges into the target company before liquidating,

The target company then becomes a subsidiary of the acquirer, and

The target company’s shareholders receive cash.

Structuring the deal this way may work to overcome the hurdle of transferring the license but may not qualify as a tax-free reorganization.

Bottom Line

The circumstances and motivations for mergers and acquisitions in the cannabis industry are diverse. As a result, there is no one-size-fits-all approach to structuring the transaction. In any event, it’s crucial to start the process early and seek advice from legal counsel and tax advisors to minimize the tax burden and ensure that both parties to the transaction get the best deal possible. If you need assistance, contact your 420CPA strategic financial advisor.

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

We use tracking pixels that set your arrival time at our website, this is used as part of our anti-spam and security measures. Disabling this tracking pixel would disable some of our security measures, and is therefore considered necessary for the safe operation of the website. This tracking pixel is cleared from your system when you delete files in your history.

We also use cookies to store your preferences regarding the setting of 3rd Party Cookies.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.

Federal anti-money laundering laws and related record-keeping regulations, such as the Bank Secrecy Act (BSA), have presented complex compliance protocols that prevent banks from meeting the business needs of local growers, manufacturers and dispensaries. Local cannabis business owners are therefore put in a difficult position, as they must balance daily business activity against the potential dangers of operating as a cash-only business.

Federal anti-money laundering laws and related record-keeping regulations, such as the Bank Secrecy Act (BSA), have presented complex compliance protocols that prevent banks from meeting the business needs of local growers, manufacturers and dispensaries. Local cannabis business owners are therefore put in a difficult position, as they must balance daily business activity against the potential dangers of operating as a cash-only business. Policymakers may need to introduce the Act as a stand-alone bill that outlines clear objectives and specifically addresses the issue from a public safety perspective. Cannabis is a hot-button issue, so adding additional legislation will muddy the water and make it easier for Senate members on the fence to vote against the bill.

Policymakers may need to introduce the Act as a stand-alone bill that outlines clear objectives and specifically addresses the issue from a public safety perspective. Cannabis is a hot-button issue, so adding additional legislation will muddy the water and make it easier for Senate members on the fence to vote against the bill.