Mergers and acquisition activity in the cannabis space tripled from 2020 to 2021, and that pace is on track to continue in 2022. With big players entering the global cannabis market, we’re fielding more questions about mergers and acquisitions of cannabis businesses.

In this guide, we look at the evolution of the U.S. cannabis industry and some best practices and considerations for M&A deals in this environment.

The New Reality of Cannabis M&A Activity

The industry has evolved since adult use cannabis was first legalized in some U.S. states in 2012. More cannabis companies have a professional infrastructure—legal, financial and operational—with executive teams and board members ensuring the organization establishes proper governance procedures. Investors and private equity firms are showing more interest, and some cannabis companies have celebrated their first IPOs on the Canadian Securities Exchange (CSE).

At the same time, we are seeing a kind of “market grab” by multistate operators (MSOs) looking to acquire various licenses and expand their market share. MSOs tend to understand the current state of the market. For example, in California and some other states, there is a surplus of cannabis on the market for various reasons, partially due to so-called “burner distribution”—rogue distributors using licenses to buy vast amounts of legally grown cannabis at wholesale prices and selling the product on the black market, thereby undercutting retailers and other legal cannabis businesses. Another reason for the surplus is simply the entrance of many legal cultivators into the market over the past year.

Due to these trends, MSOs are interested in acquiring the outlets to be able to sell the surplus cannabis within California and other new markets.

Transferring Cannabis License Rights

One of the biggest challenges to M&A activity in the cannabis sector is the difficulty of transferring or selling a cannabis license.

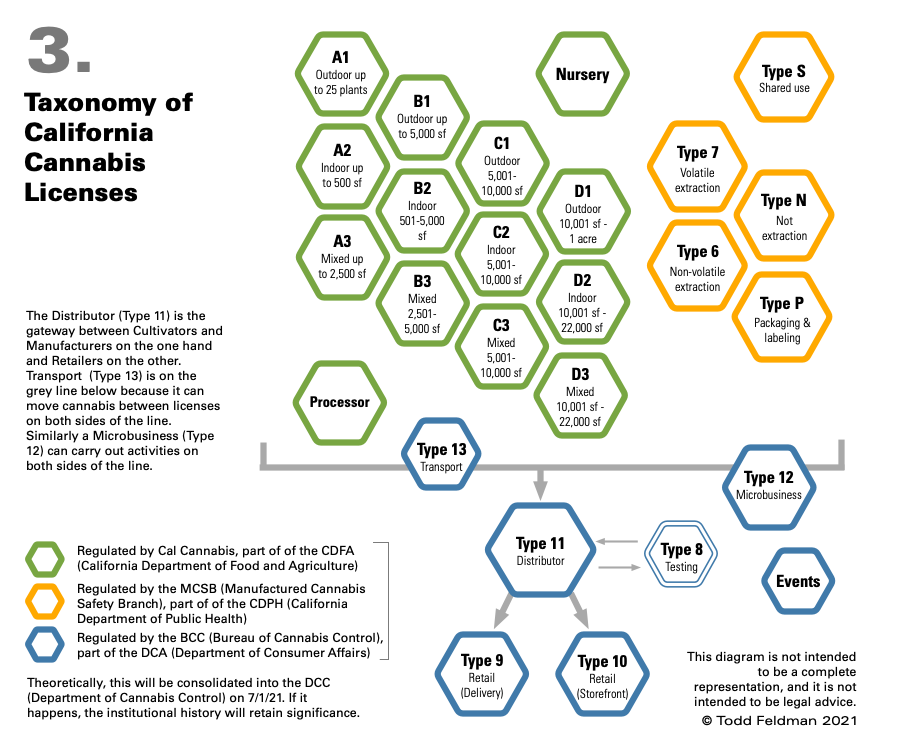

Different types of cannabis licenses in California

Cannabis licenses are not expressly transferable or assignable under California law and many other states. However, the parties involved aren’t without options. For example, a business that is sold to a new owner may be able to retain its existing cannabis license while the new owner’s license application is pending, as long as at least one existing owner is staying on board. At the state license level, a change of up to 20% financial interest does not constitute a change in ownership, although the Bureau of Cannabis Control (BCC) must be notified and approve the change.

This process can take a while—often a year or more—since licensing involves overcoming hurdles at the local level as well as the state level with the BCC. It’s crucial to talk with legal counsel about the particulars of the license and location early in the process to best structure the terms of the agreement while complying with state and local requirements.

Seeking a Tax-Free Reorganization in the Cannabis Space

In many cannabis mergers and acquisitions, the goal is to accomplish a tax-free reorganization, where the parties involved acquire or dispose of the assets of a business without generating the income tax consequences that would result from a straight sale or purchase of those assets.

IRC Section 368(a) defines various types of tax-free reorganizations, including:

In a stock-for-stock reorganization, all of the target company’s stock is traded for a portion of the stock of the acquiring parent corporation, and target company shareholders become minority shareholders of the acquiring company.

Often, it’s tough to meet the requirements to qualify for this type of tax-free reorganization because at least 80% of the target stock must be paid for in voting stock of the acquirer.

Additionally, companies may be saddled with too much debt. If the acquirer assumes that debt, it may be classified as consideration paid to the seller and therefore disqualify the transaction as a tax-free reorganization.

In other M&A deals, the acquiring corporation may be unwilling to assume the debt of the target corporation—perhaps because showing these items on its balance sheet would impact its debt-to-equity and other financial ratios.

Rather than acquiring the target company’s stock, the acquirer may purchase its assets. In a stock-for assets exchange, the buyer must purchase “substantially all” of the target’s assets in exchange for voting stock of the acquiring corporation.

A stock-for-assets format offers the buyer the benefit of not having to assume the unknown or contingent liabilities of the target. However, it’s only feasible if the acquirer purchases at least 80% of the fair market value of the target’s assets AND all or virtually all of the deal consideration will be stock of the acquirer.

Tax Consequences Arising from Sale of Assets

If the sale price doesn’t consist primarily of the buyer’s stock, the transaction may be a standard asset sale. This leads to very different tax results.

If the seller is a C corporation, it will typically face double taxation—paying tax once on the sale of assets within the corporation and again when those profits are distributed to shareholders. If the target company has net operating losses (NOLs), it can use those NOLs to offset the tax hit.

If the seller is an S corporation, it won’t have to pay corporate tax on the transaction at the federal level. Instead, shareholders will pay tax on the gain on their individual returns.

For the buyer, the benefit of an asset sale is that the assets acquired get a “step-up basis” to their purchase price. This is beneficial from a tax perspective, as the buyer can depreciate the assets and may be able to claim accelerated or bonus depreciation to help offset acquisition costs.

The subsidiary merges into the target company before liquidating,

The target company then becomes a subsidiary of the acquirer, and

The target company’s shareholders receive cash.

Structuring the deal this way may work to overcome the hurdle of transferring the license but may not qualify as a tax-free reorganization.

Bottom Line

The circumstances and motivations for mergers and acquisitions in the cannabis industry are diverse. As a result, there is no one-size-fits-all approach to structuring the transaction. In any event, it’s crucial to start the process early and seek advice from legal counsel and tax advisors to minimize the tax burden and ensure that both parties to the transaction get the best deal possible. If you need assistance, contact your 420CPA strategic financial advisor.

As the regulated cannabis industry matures, M&A activity is expected to continue accelerating. Whether they are existing licensed businesses looking for acquisition opportunities or new investor groups seeking to enter or expand their positions in the industry, investors should recognize the special due diligence challenges associated with cannabis industry transactions.

Above all, investors should avoid the temptation to omit or short-circuit long-established due diligence practices, mistakenly believing that some of these steps might not be relevant to cannabis and hemp operations. Despite the unique nature of the industry, thorough and professional financial, tax and legal due diligence are essential to a successful acquisition.

Surging M&A activity

Over the past few years, as the cannabis industry matured and the regulatory environment evolved, M&A activity involving cannabis and hemp companies has undergone several cycles of expansion and contraction. Today, the expansion trend clearly has resumed. Although the exact numbers vary from one source to another, virtually all industry observers agree that 2021 saw a strong resurgence in cannabis-related M&A activity, with total transactions numbering in the hundreds and total deal values reaching into billions of dollars. Moreover, most analysts seem to agree that so far, the pace for 2022 is accelerating even more.

Today, many existing cannabis and hemp multistate operating companies are in an acquisitive mood as they look for opportunities to scale up their operations, enter new markets, and vertically integrate. At the same time, the projections for continued industry growth over the next decade have attracted a number of investment funds and private equity groups, which were formed specifically for the purpose of investing in cannabis and hemp businesses.

These two classes of investors often pursue distinctly different approaches to their transactions. Unlike the largely entrepreneurial cannabis industry pioneers now looking to expand, the more institutional investors are accustomed to working with professional advisers to perform financial, tax and legal due diligence as they would for a transaction in any other industry.

Among both groups, however, there is sometimes a tendency to misunderstand some of the transactional risk elements associated with cannabis M&A deals. In many instances, buyers who are generally sensitive to potential legal and regulatory risks will underestimate or overlook other risks they also should examine as part of a more conventional financial and tax due diligence effort.

For example, since much of the value of a licensed cannabis operation is the license itself, investors often rely largely on their own industry understanding and expertise to assess the merits of a proposed acquisition, based primarily on their estimation of the license’s value. This practice provides acquirers with a narrow and incomplete view of the deal’s overall value. More importantly, it also overlooks significant areas of risk.

Because cannabis acquisition targets typically are still quite new and have no consistent earning records, acquirers also sometimes eschew quality of earnings studies and other elements of conventional due diligence that are designed to assess the accuracy of historical earnings and the feasibility of future projections.

Such assumptions and oversights often can derail an otherwise promising transaction prior to closing, causing both the target and the acquirer to incur unnecessary costs and lost opportunities. What’s more, even if the deal is eventually consummated, short-circuiting the normal due diligence processes can expose buyers to significant unanticipated risk down the road.

Recurring issues in cannabis acquisitions

The most widely recognized risks in the industry stem from the conflict between federal law and the laws of various states that have legalized cannabis for medical or adult recreational use. The most prominent of these concerns relates to Section 280E of the Internal Revenue Code (IRC 280E).

Although its use is now legal in many states, cannabis is still classified as a Schedule I substance under the federal Controlled Substances Act. IRC 280E states that any trade or business trafficking in a controlled substance must pay income tax based on its gross income, rather than net income after deductions. As a result, cannabis businesses are not entitled to any of the common expense deductions or tax credits other businesses can claim.

The practical effect of this situation is that cannabis-related businesses – including growers, processors, shippers and retailers – often owe significant federal income tax even if they are not yet profitable. Everyone active in the industry is aware of the issue, of course, and any existing operating company or investment group will undoubtedly factor this risk into its assessment of a proposed acquisition target.

The challenge can be exacerbated, however, by other, less widely discussed factors that also affect many cannabis businesses. These issues further cloud the financial, tax and regulatory risk picture, making thorough and professional due diligence even more critical to a successful acquisition.

Several of these issues merit special attention:

Nonstandard accounting and financial reporting practices. As is often the case in relatively young, still-maturing businesses, acquisition targets in the cannabis industry might not have yet developed highly sophisticated accounting operations. It is not uncommon to encounter inadequate accounting department staffing along with financial reporting procedures that do not align with either generally accepted accounting principles or other standard practices. In many instances, company management is still preparing its own financial statements with minimal outside guidance or involvement by objective, third-party professionals. Significant turnover in the management team – and particularly in the chief financial officer position –is also common, as is a general view that accounting is a cost center rather than a value-enhancing part of the management structure.

Such conditions are not unusual in young businesses that are still largely entrepreneurial in spirit and practice. In the cannabis industry, however, this situation is also a reflection of many professional and business services firms’ longstanding reluctance to engage with cannabis operators – a hesitancy that still affects some organizations.

When customary business practices are not applied or are applied inconsistently, acquiring companies or investors should be prepared to devote more time and attention – not less – to conventional financial due diligence. The expertise of professional advisers with direct experience in the industry can be of immense benefit to all parties in this effort.

Restructuring events or nonrecurring items in financial statements. Restructuring events and nonrecurring items are relatively common in many new or fast-growing businesses, and they are especially prevalent among cannabis operations. In many instances, such companies have engaged in multiple restructuring events over a short period of time, often consolidating operations, taking on new debt, and incurring various one-time costs that are not directly related to the ongoing operations of the business.

The inclusion of various nonrecurring items within the historical financial statements can make it much more difficult for a buyer or investor to accurately identify and assess proforma operating results, especially in businesses that have not yet generated consistent profits. Here again, applying previous experience in clearing up the noise in the financial statements can help improve both the accuracy and timeliness of the due diligence effort.

Run-rate results inconsistent with historical earnings or losses. A company’s run rate – an extraction of current financial information as a predictor of future performance – is a widely used tool for creating performance estimates for companies that have been operating for short periods of time or that have only recently become profitable. In cannabis businesses, however, run-rate estimates sometimes can be unreliable or misleading.

Because it is based only on the most current data, the run rate often does not reflect significant past events that could skew projections or recent changes in the company’s fundamental business operations. Because such occurrences are relatively common in the industry, the results of run-rate calculations can be inconsistent with the target company’s historical record of earnings or losses.

Historical tax and structuring risks new owners must assume. Like many other new businesses, cannabis operations often face cash flow and financing challenges, which owners can address through alternative strategies such as debt financing, stock warrants, or preferred equity conversions. Such approaches can give rise to complex tax and financial reporting issues as tax authorities exercise their judgment in interpreting whether these items should be reported as liabilities or equity derivatives. The situation is often complicated further by various nonstandard business practices and the absence of sophisticated accounting capabilities, as noted earlier.

As a consequence, financial statements for many cannabis companies – including a number of publicly listed companies – often contain complex capital structures with numerous types of debt warrants, conversion factors and share ownership options. Although an acquisition would, in theory, clean up these complications, buyers nevertheless must factor in the risk of previous noncompliance that might still be hidden within the organization – a risk that can be identified and quantified only through competent and thorough due diligence.

Not as simple as it seems

On the surface, the fundamentals of the cannabis industry are relatively straightforward, which is one reason it appeals to both operators and investors. For example, participants at every stage of the cannabis business cycle – growing and harvesting, processing and packaging, shipping and distribution, and ultimately marketing and retailing – can readily apply well-established practices from their counterparts in more conventional product lines.

The major exception to this rule, of course, is the area of regulatory compliance, which is still shifting and likely will continue to do so for the foreseeable future. Outside of this obvious and significant exception, however, most other aspects of the industry are relatively predictable and manageable.

When viewed in this light and in light of the continued growth of the industry, it is easy to see why cannabis-related acquisitions are so appealing to existing business operators and outside investors alike. It is also easy to understand why buyers might feel pressure to move quickly to take advantage of promising opportunities in a fast-changing industry.

As attractive as such opportunities might be, however, buyers should take care to avoid shortcuts and resist the urge to sidestep established due diligence procedures that can reveal potential accounting and financial statement complications and the related compliance risks they create. The unique nature of the cannabis industry does not make these practices irrelevant or unnecessary. If anything, it makes professional financial, tax, and legal due diligence more important than ever.

Crowe Disclaimer: Qualified organizations only. Independence and regulatory restrictions may apply. Some firm services may not be available to all clients. Given the continued evolution and inconsistency of various state and federal cannabis-related laws, any company should seek competent legal advice relating to its involvement in the cannabis industry, including when considering a potential public offering as a cannabis-related company.

According to a press release published last week, Cresco Labs has come to an agreement with Columbia Care Inc. to acquire the company. The $2 billion deal, expected to close in the fourth quarter of 2022, will create the largest multi-state operator (MSO) in the country by pro-forma revenue.

Cresco Labs is already one of the country’s largest MSOs with roots in Illinois. With a footprint covering a lot of the United States, their brands include Cresco, High Supply, Mindy’s Edibles, Good News, Remedi, Wonder Wellness Co. and FloraCal Farms.

Columbia Care is also one of the largest cannabis companies in the US, with licenses in 18 jurisdictions and the EU. They currently operate 99 dispensaries and 32 cultivation and manufacturing facilities. Their brands include Seed & Strain, Triple Seven, gLeaf, Classix, Press, Amber and Platinum Label CBD.

Under the agreement, shareholders with Columbia Care will receive 0.5579 of subordinate voting share in Cresco for each common share they hold. Columbia Care shareholders will hold approximately 35% of the pro forma Cresco Labs Shares once the deal goes into effect.

Coming out of the deal, Cresco’s total revenue will hit $1.4 billion, making it the largest MSO in the country. Their footprint will reach 130 retail dispensaries across 18 different markets. The companies already have the largest market share in Illinois, Pennsylvania, Colorado and Virginia and are of the top three market shares in New York, New Jersey and Florida, which gives them unique opportunities to capitalize on emerging adult use markets.

Charles Bachtell, CEO of Cresco Labs, says the deal is very complementary and they are excited about long-term growth and diversification. “This acquisition brings together two of the leading operators in the industry, pairing a leading footprint with proven operational, brand and competitive excellence,” says Bachtell. “The combination of Cresco Labs and Columbia Care accelerates our journey to become the leader in cannabis in a way no other potential transaction could. We look forward to welcoming the incredible Columbia Care team to the Cresco Labs family. I couldn’t be more excited about this enhanced platform and how it furthers the Cresco Labs Vision – to be the most important and impactful company in cannabis.”

In this “Flower-Side Chats” series of articles, Green interviews integrated cannabis companies and flower brands that are bringing unique business models to the industry. Particular attention is focused on how these businesses integrate innovative practices in order to navigate a rapidly changing landscape of regulatory, supply chain and consumer demand.

The Michigan cannabis market is making pace with big time cannabis players like California (#1) and Colorado (#2). For the first quarter of 2021, combined cannabis sales in Michigan were nearly $360 million. At that pace, Michigan could see combined sales of $1.4 billion — well outpacing 2020 sales of $984 million.

Gage is the exclusive cultivator and retailer of world-leading cannabis brands including Cookies, Lemonnade, Runtz, Grandiflora, SLANG Worldwide, OG Raskal, and its own proprietary Gage brand portfolio in Michigan. The company recently secured a $50M investment in an oversubscribed round which included a $20M investment from JW Asset Management.

We spoke with Fabian Monaco, CEO of Gage Cannabis. Fabian started Gage in 2017 after meeting his operating partners in Michigan. Prior to Gage, Fabian worked as an investment banker racking up a number of firsts in cannabis industry financing and M&A transactions.

Aaron Green: Tell me how you got involved in the cannabis industry.

Fabian Monaco: My background is in investment banking – specifically 10 years of capital market experience. I was fortunate enough to be part of the initial team that brought Tweed, now Canopy Growth public. In fact, I worked on a lot of firsts in the industry: the first acquisition, the first $100 million financing, the first IPO in the space. Shortly after that, I went to XIB Financial, which co-founded Canopy Rivers with Canopy Growth. I was working on that when I encountered these two phenomenal operators. At the time, I had visited over 100 of these cultivation facilities and these were some of the best operators in the business. So that led me to start Gage in 2017.

Green: Where is Gage currently operating?

Fabian Monaco, CEO of Gage Cannabis

Monaco: In the U.S., we are purely operating in Michigan. We do have a licensing agreement with a small producer in Canada, so you will see the brand there.

Green: Tell me about your choice to settle the company in Michigan initially?

Monaco: If you look at Michigan as a historical cannabis market, it was the second largest cannabis market from a medical card holder standpoint for nearly a decade, only behind California. This was probably the case until 2019, where they went to adult use. So, for us, we knew this medical base was going to be a great platform to an outsized adult-use market. And already we see that April was $154 million in sales, adding up to over a $1.8 billion dollar run rate. That’s the third highest run rate in the country, only behind California and Colorado.

Green: What is it that makes Michigan different? You talked about medical cannabis already. Is there anything else about the demographics in Michigan or the consumer base that makes Michigan special in that sense?

Monaco: In Michigan, over 70% of the population is old enough to consume. So, when you take a look at how much of the population is 21-years-old plus, relative to other markets, the total addressable market in Michigan is just huge. Then when you take a look at their consumption habits, especially when it comes to flower, Michigan is consuming some of the highest amounts on a per capita basis. Those two stats set up a scenario where we foresaw the potential of the market. To be honest, the market has exceeded our expectations. We didn’t think it would be this strong this quickly. Right now, the state is looking to be a $3 billion market by 2024 – and it could easily surpass that.

Green: Any plans for expansion beyond Michigan?

Monaco: We’ve been to eight or so different states in the past 60 or 75 days really trying to educate ourselves on the licensing structure, the markets there and the key players in those respective markets. What are some of the costs, in terms of acquisitions? We really want to branch out the Gage brand into other states across the US. The thing is, we believe in the model that Trulieve deployed. They really focus on being the number one player in a very, very big market. For instance, Trulieve is obviously one of the top players in Florida. We’re trying to mimic that strategy.

Trulieve is a dominant market force in Florida

Once we have that deep market penetration, that market share, then we’ll start to get into other states. But for now, why would you want to go and rush out to another state when you’re already in the third largest market in the country?

Green: Are there any criteria you look for in a potential expansion state?

Monaco: We look at consumption habits. We want states with similar demographics to Michigan. Close proximity states also allows us to quickly go from one state to the other without having to take a multi-hour flight to get there. States we’re considering are Northeast and Midwest states, like Illinois, Pennsylvania, Ohio, New Jersey, Massachusetts and Maryland.

Green: What kind of consumer trends are you seeing in Michigan as it relates to products?

Monaco: Flower continues to dominate. In a market like Michigan, we have some of the top flower consumers in the country on a per capita basis. We specialize in flower and flower only, so this created a perfect scenario where we are able to ramp up our brand quite quickly, from a flower standpoint.

Now that we have that brand equity, that brand power, we are going to potentially delve into other categories, including extract-based products, such as vape carts and concentrates. You hear talk about these new beverages, but we’re not seeing that take off in this market as much as people think it would. Flower still remains at the top and that’s something we highly anticipate going after for quite some time.

Green: Can you tell me about your vertical integration strategy?

Monaco: We’re one of the larger retail portfolios in Michigan right now. We have 13 locations. Nine are operational. So, we’re really in a great spot overall in terms of how big of a platform we do have – one of the larger ones – and, frankly, in one of the larger markets in the country.

The Cookies flagship dispensary in Detroit, Michigan

We actually have a little bit of a unique scenario on the cultivation side of things. We have our own three cultivation assets that are going to be producing, on average, about 1,000 pounds of product over the next couple of months as they fully ramp up. We’ve actually contracted out a lot of our cultivation. Cultivation is time consuming, and it’s also very, very costly to build out. Luckily for us, we’re a really well-established and strong brand. We had the opportunity to contract out our growing. So, we have 10 different contract growth partners. These are phenomenal cultivators, again, some of the best in the state. They grow Gage and Cookies branded product for us. We have a great breakdown from a financial standpoint. We share the retail revenue with them on a 50/50 basis. They pay a little bit too, for packaging and testing. So, basically for $0 we’re getting product on the shelf where we’re achieving 50% plus gross margins. It’s a phenomenal setup for us on the cultivation side where we went from two cultivation assets in the latter half of last year to now eight different cultivation assets, moving to 13 by the end of the year.

On the processing side, we’re just actually finishing our processing lab. We should have extract-based products launched in Q3. We’re really excited to have our own line of extract-based products. We plan to focus on vape carts to start – a very popular category in Michigan on the retail side of things.

Green: Are those cultivations all indoor?

Monaco: Yes, we’re big proponents of indoor flower. It allows us to control the quality of our flavors and consistency in our strains when we grow indoors. From our consumers, there is a very strong demand for indoor grown high-premium, high-quality products.

Green: What sets Gage apart from other competitors in Michigan?

Monaco: I think focus. We just focused on our flower. We focus on our post-production process. We hang dry everything, we hand trim everything, and we hand package everything. That’s a little bit more time consuming. It’s a little more costly. But all that effort shows in the end product which is key.

A lot of people think you can grow great quality product, you cut it down, you dry it and put it in the pack and it’s going to be great. You really need a strong attention to detail, especially in a big consuming market like Michigan, because again, they are a refined consumer. They’re looking for the best. They’ve already been consuming some of the best quality products in the country for many years now. So for us, we put a painstaking process in place for flower production, not only from the growing standpoint, but also through the end of that post production process.

Ancillary to our cultivation process is also consistently providing new varieties of flavors on the flower side of things to the consumers. When you look at the successful brands in California, what makes them special is that they’re consistently pheno hunting, coming out with new flavors. This is similar to the wine industry where the best wineries come out with a new kind of grape or mix and consumers get excited, they rush out and buy half a dozen bottles or a dozen bottles.

It’s a very similar scenario in the cannabis industry. I hate when people say that cannabis is a commoditized industry. It’s so far from the truth. You look at brands like us or Cookies, Jungle Boyz and you can see their constant innovation, their constant drive. They are always bringing something new for the consumers to try. That’s what really sets apart the best brands.

Green: What’s got your attention in the cannabis industry? What are you interested in learning more about?

Monaco: I’m always intrigued with new ways of consuming. Across the U.S. and well-developed markets like California and Colorado, you see all these interesting new ways to consume the product. You’ve got patches, sublingual strips, etc. There are so many unique ways. I am currently seeing how they play out. Are they fads? Do people get excited about them initially, and then go back to their vape carts, pens and typically dried flower pre-rolls? I’m always trying to educate myself to see what’s on the market. What’s new? Who has a new drink? How does it hit? Are people excited about it?

Also, I am constantly learning about new brands that come out. There are so many new small brands that don’t necessarily have the scale or the capital to really expand, but are producing some of the best products in the country in a cool, unique form of packaging, etc..

Green: Alright, great. That concludes the interview!

The cannabis industry saw close to $15.5B in deals across VC, private equity, M&A and IPOs in 2020 according to PitchBook data. Early and growth stage capital has been a key enabler in deal activity as companies seek to innovate and scale, taking advantage of trends towards national legalization and consolidation. Entourage Effect Capital is one of the largest VC firms in cannabis with over $150MM deployed since its inception in 2014. Some of their notable investments include GTI, CANN, Harborside (CNQ: HBOR), Acreage Holdings, Ebbu, TerrAscend and Sunderstorm.

We spoke with Matt Hawkins, co-founder and managing partner at Entourage Effect Capital. Matt started Entourage in 2014 after exiting his previous company. He has 20+ years of private equity experience and serves on the Boards of numerous cannabis companies. Matt’s thought leadership has been on Fox Business in the past and he has also recently featured on CNBC, Bloomberg, Yahoo! Finance, Cheddar and more.

Aaron Green: How did you get involved in the cannabis industry?

Matt Hawkins: We’ve been making investments in the cannabis industry since 2014. We’ve made 65 investments to date. We have a full team of investment professionals, and we invest up and down the value chain of the industry.

I had been in private equity for 25 years and I kind of just fell into the industry after I’d had an exit. I started lending to warehouse owners in Denver that were looking to refinance their mortgages out of commercial debt into private debt, which would then give them the ability to lease their facilities to growers. I realized there would be a significant opportunity to place capital in the private equity side of the cannabis business. So, I just started raising money for that project and I haven’t looked back. It’s been a great run and we’ve built a fantastic portfolio. We look forward to continuing to deploy capital up to and through legalization.

Green: Do you consider Entourage Effect Capital a VC fund or private equity firm? How do you talk about yourself?

Hawkins: In the early stages of the industry, we were more purely venture capital because there was hardly any revenue. We’re probably still considered a venture capital firm, by definition, just because of the risk factors. As the industry has matured, the investments we make are going to be larger. The reality is that the checks we write now will go to companies that have a track record of not only 12 months of revenue, but EBITDA as well. We can calculate a multiple on those, and that makes it more like lower/middle-market private equity investing.

Green: What’s your investment mandate?

Matt Hawkins, Co-Founder and Managing Partner at Entourage Effect Capital

Hawkins: From here forward our mandate is to build scale in as many verticals as we can ahead of legalization. In the early days, we were focused on giving high net worth individuals and family offices access to the industry using a very diversified approach, meaning we invested up and down the value chain. We’ll continue to do that, but now we’re going to be really laser focused on combining companies and building scale within companies to where they’re going to be more attractive for exit partners upon legalization.

Green: Are there any particular segments of the industry that you focus on whether it’s cultivation, extraction or MSOs?

Hawkins: We tend to focus on everything above cultivation. We feel like cultivation by itself is a commodity, but when vertically integrated, for example with a single-state operator or multi-state operator, that makes it intrinsically more valuable. When you look at the value chain, right after cultivation is where we start to get involved.

Green: Are you also doing investments in tech and e-commerce?

Hawkins: We’ve made some investments in supply chain, management software, ERP solutions, things like that. We’re not really focused on e-commerce with the exception of the only CBD company we are invested in.

Green: How does Entourage’s investment philosophy differ from other VC and private equity firms in cannabis?

Hawkins: We really don’t pay attention to other people’s philosophies. We have co-invested with others in the past and will continue to do so. There’s not a lot of us in the industry, so it’s good that we all work together. Until legalization occurs, or institutional capital comes into play, we’re really the only game in town. So, it behooves us all to have good working relationships.

Green: Across the states, there’s a variety of markets in various stages of development. Do you tend to prefer investing in more sophisticated markets? Say California or Colorado where they’ve been legalized for longer, or are you looking more at new growth opportunities like New York and New Jersey?

Hawkins: Historically, we’ve focused on the most populous states. California is obviously where we’ve placed a lot of bets going forward. We’ll continue to build out our portfolio in California, but we will also exploit the other large population states like New Jersey, New York, Arizona, Massachusetts, Michigan, Ohio and Illinois. All of those are big targets for us.

Green: Do you think legalization will happen this Congress?

Hawkins: My personal opinion is that it will not happen this year. It could be the latter part of next year or the year after. I think there’s just too much wood to chop. I was encouraged to see the SAFE Banking Act reappear. I think that will hopefully encourage institutional capital to take another look at the game, especially with the NASDAQ and the New York Stock Exchange open up. So that’s a positive.

I think with the election of President Biden and with the Senate runoffs in Georgia going Democrat, the timeline to legalization has sped up, but I don’t think it’s an overnight situation. I certainly don’t think it’ll be easy to start crossing state lines immediately, either.

Green: Can you explain more about your thoughts on interstate commerce?

Hawkins: I think it’s pretty simple. The states don’t want to give up all the tax revenue that they get from their cultivation companies that are in the state. For example, if you allow Mexico and Colombia to start importing product, we can’t compete with that cost structure. States that are neighbors to California, but need to grow indoors which is more expensive, are not going to want to lose their tax revenues either. So, I just think there’s going to be a lot of butting heads at the state level.

The federal government is going to have to outline what the tax implications will be, because at the end of the day the industry is currently taxed as high as it ever will be or should be. Anything North of current tax levels will prohibit businesses from thriving further, effectively meaning not being able to tamp down the illicit market. One of the biggest goals of legalization in my opinion should be reducing the tax burden on the companies and thereby allowing them to be able to compete more directly with the illicit market, which obviously has all the benefits of reduced crime, etc.

Green: Do you foresee 280E changes coming in the future?

Hawkins: For sure. If the federal illegality veil is removed – which means there’ll be some type of rescheduling – cannabis would be removed from the 280E category. I think 280E by definition is about just illegal drugs and manufacturing and selling of that. As long as cannabis isn’t part of that, then it won’t be subject to it.

Green: What have been some of the winners in your portfolio in terms of successful exits?

Hawkins: When the CSC started allowing companies in Canada to own U.S. assets, the whole landscape changed. We were fortunate to be early investors in Acreage and companies that sold to Curaleaf and GTI before they were public. We are big investors in TerrAscend. We were early investors in Ebbu which sold to Canopy Growth. Those were huge wins for us in Fund I. We also have some interesting plays in Fund II that are on the precipice of having similar-type exits.

You read about the big ones, but at the end of the day, the ones that kind of fall under the radar – the private deals – actually have even greater multiples than what we see on some of the public M&A activity.

Green: Governor Cuomo has been hinting recently at being “very close” on a deal for opening up the cannabis market in New York. What do you think are the biggest opportunities in New York right now?

Hawkins: If it can get done, that’s great. I’m just concerned that distractions in the state house right now in New York may get in the way of progress there. But if it doesn’t, and it is able to come to fruition, then there isn’t a sector that doesn’t have a chance to thrive and thrive extremely well in the state of New York.

Green: Looking at other markets, Curaleaf recently announced a big investment in Europe. How do you look at Europe in general as an investment opportunity?

Hawkins: We have a pretty interesting play in Europe right now through a company called Relief Europe. It’s poised to be one of the first entrants to Germany. We think it could be a big win for us. But let’s face it, Europe is still a little behind, in fact, a lot behind the United States in terms of where they are as an industry. Most of the capital that we’re going to be deploying is going to be done domestically in advance of legalization.

Green: What industry trends are you seeing in the year ahead?“We’re constantly learning from other industries that are steps ahead of us to figure out how to use those lessons as we continue to invest in cannabis.”

Hawkins: Well, I think you’ll see a lot of consolidation and a lot of ramping up in advance of legalization. I think that’s going to apply in all sectors. I just don’t see a scenario wherein mom and pops or smaller players are going to be successful exit partners with some of the new capital that’s coming in. They’re going to have to get to a point where they’re either selling to somebody bigger than them right now or joining forces with companies around the same size as them and creating mass. That’s the only way you’re going to compete with companies coming in with billions of dollars to deploy.

Green: How do you see this shaking out?

Hawkins: That’s where you start to look into the crystal ball. It’s really difficult to say because I think until we get to where we truly have a national footprint of brands, which would require crossing state lines, it’s going be really difficult to tell where things go. I do know that liquor, tobacco, beer, the distribution companies, they all are standing in line. Big Pharma, big CPG, nutraceuticals, they all want access to this, too.

In some form or fashion, these bigger players will dictate how they want to go about attacking the market on their own. So, that part remains to be seen. We’ll just have to wait and see where this goes and how quickly it goes there.

Green: Are you looking at other geographies to deploy capital such as APAC or Latin America regions?

Hawkins: Not at this point. It’s not a focus at all. What recently transpired here in the elections just really makes us want to focus here and generate positive returns for investors.

Green: As cannabis goes more and more mainstream, federal legalization is maybe more likely. How do you think the institutional investor scene is evolving around that? And is it a good thing to bring in new capital to the cannabis market?

Hawkins: I don’t see a downside to it. Some people are saying that it could damage the collegial and cottage-like nature of the industry. At the end of the day, if you’ve got tens of billions of dollars that are waiting to pour into companies listed on the CSC and up-listing to the NASDAQ or New York Stock Exchange, that’s only going to increase their market caps and give them more cash to acquire other companies. The trickle-down effect of that will be so great to the industry that I just don’t know how you can look the other way and say we don’t want it.

Green: Last question: What’s got your attention these days? What’s the thing you’re most interested in learning about?

Hawkins: We’re constantly learning about just where this industry is headed. We’re constantly learning from other industries that are steps ahead of us to figure out how to use those lessons as we continue to invest in cannabis. We all saw the correlation between cannabis and alcohol prohibition. The reality is that the industry is mature enough now where you can see similarities to industries that have gone from infancy to their adolescent years. That’s kind of where we are now and so we spend a lot of time studying industries that have been down this path before and see what lessons we can apply here.

Green: Okay, great. So that concludes the interview!

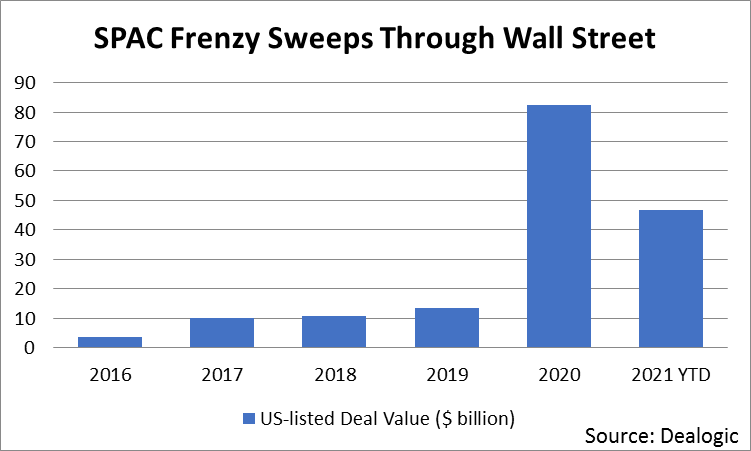

The unusual nature of 2020 gave rise to a reciprocally roller-coaster-like cannabis market. Cannabis was cemented officially as an essential industry with the rise of COVID-19, and November elections resulted in even more United States markets welcoming medical and adult-use sales.

The stagnant cannabis stock market of 2019 became a thing of the past by the end of 2020. Throughout the course of last year, bag holders anxiously watched cannabis options creep back up. Now, nearly two years since market decline in 2019, the cannabis stock market is exploding with blank checks and buyout fever. Much of this expectant purchasing is due to Canadian companies considering U.S. market entrance. Combined with the recent surge in the use of special purpose acquisition companies (SPACs) to invest, this has led to an increase in asset prices.

A SPAC is defined as “a company with no commercial operations that is formed strictly to raise capital through an initial public offering (IPO) for the purpose of acquiring an existing company.” Though they have existed for decades, SPACs have become popular on Wall Street the last few years because they are a way for a company to go public without the associated headaches of preparing for a traditional IPO.

In a SPAC, investors interested in a specific industry pool their money together without knowledge of the company they’re starting. The SPAC then goes public as a shell company and begins acquiring other companies in the associated industry. Selling to a SPAC is usually an attractive option for owners of smaller companies built from private equity funds.

The U.S.-Canadian market questions that this rising practice asks are: Can Canadian companies enter a bigger market and be more successful? Is it advisable for U.S. companies to sell their assets to Canadian corporations whose records may be marred by a history of losses and a lack of proper corporate governance? Regardless — if both SPAC’s and Canadian bailout money is here, what comes next?

What is Driving this Bull Market?

Underpinning these movements are record cannabis sales internationally, making last year’s $15 billion dollars’ worth of sales in the U.S. look small in comparison. New markets have opened up in various states and countries throughout 2020, and that trend is only expected to continue. New demographics are opening up, especially among older age groups. This makes sense, as most cannabis sales — even in a recreational setting — are people treating something that ails them like insomnia or aches and pains.

Cannabis is set to take off, and we are entering only the second phase of its market expansion. The world is becoming competitive. Well-run companies that are profitable in key markets are prime targets for bigger, growing companies. At the same time, the world of SPACs will continue to drive valuations. Irrespective of buying assets, growing infrastructure is and will continue to be greatly needed.

The Elusive Profitability Factor

When Canada blew up, one of the biggest changes was companies began focusing the year on cost cutting and — most importantly — profitability. Profitability became the buzzword. But bigger companies are on the search for already-profitable enterprises, not just those that have the potential to be. However, profitability is currently still unobtainable in Canada. Reasonable forecasters should expect this year will show a few companies getting bailed out while many others will be forced to either merge for survival or declare bankruptcy.

An ideal company’s finances should highlight not only revenue growth, but also profitability. Attention should be focused on how well businesses are run, and not on how much money they have the potential to raise or spend. Over the years, there have been many prospective companies that spent hundreds of millions only to barely operate, and are now shells in litigation. Throwing money at any deal should have been a lesson learned in the past, but SPACs are tempting because they are trendily associated with new, interesting management styles and charismatic businesspeople.

Companies should be able to present perfect and clear financials along with maintenance logs for all equipment. In today’s day and age, books must be stellar and clean. As money pours into SPACs, asset valuations for all qualities of companies will rise. The focus instead becomes about asset plays, which will cause assets to continue rising as money is poured into SPACs.

Once upon a time, if number counters presented a negative review or had to dig too much, executives would turn a cold shoulder on investment. But in the age of SPACs, these standards of evaluation will be greatly undervalued. Aging equipment and reportability of every piece of equipment may or may not be properly serviced and recorded in a fast-moving market. Costs of repair or replacing equipment that isn’t properly maintained may be a problem of the past. Because when money comes fast, none care for the gritty details.

Issues for SPACs

Shortage of talent and training has become a big concern already in the era of SPACs. How many quality assets are out there? Big operators in the U.S. are content and don’t see Canada as an enticing market to enter. So, asset buys are likely to primarily be in the U.S. Large companies like Aphria may buy out some of the major American players, but most Canadian companies will use new funding rounds to pay down debts. Accordingly, they will then be forced to piece together smaller operators as a strategy.

A cannabis company’s personnel and office culture are very important when looking to integrate into a larger corporate culture. Remember, it’s not just the brick and mortar that is being invested into, it is also the people that run a facility. Maintaining employee retention when a deal occurs is always critical. Your personnel should be highly trained and professional if you want to exit. Easy to plug-in corporate structures make all the difference in immediately gaining from the sale or having to retool the shed and bring in all new people.

The rise of the SPAC-era and Canadian entry into the U.S. market will cause asset increases, but it is only the second chapter in the market expansion of cannabis. Proper buys will nail profitability, impeccable books, proper maintenance records and will have created an efficient corporate structure with talented personnel. The rest will be overpriced land buys that will require massive infrastructure spending. The basics of a well-run organization don’t change. The cannabis market is going to ROAR, but don’t worry if the SPACs pass you by- they are buying at the start of cannabis only.

Cresco Labs, one of the largest multistate operators (MSOs) in the country, announced the acquisition of Bluma Wellness Inc., a vertically integrated cannabis company based in Florida.

Cresco Labs, with roots in Chicago, Illinois, operate 29 licenses in 6 states across the United States. With this new acquisition, Cresco Labs solidifies their ubiquitous brand presence in the most populous markets and cements their position in Florida, a new market for them.

According to the press release, the two companies entered an agreement where Cresco will buy all of Bluma’s issued and outstanding shares for an equity value of $213 million. They expect the transaction to be completed by the second quarter of this year.

Charles Bachtell, CEO of Cresco Labs, says their expansion strategy is based largely on population. “Our strategy at Cresco Labs is to build the most strategic geographic footprint possible and achieve material market positions in each of our states,” says Bachtell. “With Florida, we will have a meaningful presence in all 7 of the 10 most populated states in the country with cannabis programs – an incredibly strategic and valuable footprint by any definition. We recognize the importance of the Florida market and the importance of entering Florida in a thoughtful way – we identified Bluma as having the right tools and key advantages for growth.”

Bluma Wellness operates through its subsidiary, One Plant Florida, which has 7 dispensaries across the state and ranks second in sales in the state. They also have an impressive delivery arm of their retail business, deriving 15% of their revenue from it.

After a slow start following a disappointing 2019, M&A in the cannabis space closed 2020 with a bang, with more than $600 million in deals announced immediately following the November elections. Prospects for the New Year are expected to continue the explosive year-end trend with a backlog of nearly $2 billion in deals heading into 2021. The COVID-19 pandemic boosted sales of cannabis products, and election results opening up five new states to legal cannabis use and possible federal regulatory reform are further boosting prospects. Analysts now predict the U.S. cannabis market is poised to double by 2025.

Growth is expected to be led by multi-state operators who have achieved scale, cleaned up their balance sheets and stockpiled dry powder for roll-up acquisitions. Cannabis companies raised nearly $134 million in the two weeks before Election Day, a 185% increase over the same period last year. Most of the money flowed to multistate operators. In addition, the biggest stocks by market capitalization saw a roughly 20% bump ahead of the election and now are trading at record volumes, providing plenty of stock currency for further acquisitions.

Among the headline acquisitions last year:

Curaleaf continued its multi-state expansion with two of its largest acquisitions – the all-stock purchases of its affiliated cannabis oil company Select and of Grassroot, another MSO player. Curaleaf is now the largest cannabis company in the world based on annualized revenues, with annualized sales of $1 billion and operations in 23 states and 96 open dispensaries. Curaleaf also raised $215 million privately last year end for further expansion.

Close behind, Aphria and Tilray announced in December that they will merge, creating what they say will be the largest cannabis company in the world with an equity value of roughly $3.8 billion. The combined entity will have facilities and offices in the U.S., Canada, Portugal and Germany. The deal is expected to close during the second quarter of this year.

Also in December, Illinois-based Verano Holdings LLC unveiled plans to go public at a $2.8 billion valuation through a reverse takeover of a Canadian shell company. That deal followed the announcement that Verano will merge with Florida-based AltMed.

In addition, publicly traded New York cannabis firm Columbia Care signed a definitive agreement last month to acquire Green Leaf Medical, a privately held Maryland-based cannabis manufacturer and retailer, for $45 million in cash and $195 million in stock. The acquisition is expected to close this summer. Including Green Leaf’s inventory, the Columbia Care will operate 107 facilities, including 80 dispensaries and 27 cultivation and manufacturing facilities. Columbia Care also took advantage of cannabis fever last year by raising $100 million privately.

Also in December, Ayr Strategies announced it would acquire Liberty Health Sciences, one of the largest cannabis companies in Florida, for $290 million in stock, as well Garden State Dispensary, a New Jersey marijuana company for $41 million in cash, $30 million in stock and $30 million in the form of a note. This follows Ayr’s $81 million acquisition of an Arizona medical marijuana operator in November. Voters approved marijuana use in Arizona and New Jersey in November. Ayr has completed a string of acquisitions in Nevada, Massachusetts, Pennsylvania, Arizona, Ohio and, upon the closing of December’s deals, New Jersey and Florida.

Not all cannabis companies will rely on acquisitions, however. Trulieve, as an example, has focused its efforts on Florida and organic growth. It remains to be seen whether a multi-state approach fueled by acquisitions or a single-state organic growth model will prove the more lasting. Growth and profitability in the short term likely will continue to be hampered by limits on economies of scale due to federal restrictions and differing state laws.

In light of the maturing industry and the 2019 bust, the valuation model for acquisitions in the cannabis space is evolving from one based on sales, typically associated with emerging growth industries, to a more mature industry model based on profits or Earnings Before Interest, Taxes, Depreciation, and Amortization (EBITDA). Most cannabis MSOs have stabilized and generate positive EBITDA, which justifies the evolution away from a sales-driven model.

From a legal standpoint, the same limitations that have vexed the cannabis industry for years will continue to challenge deal makers until there is greater clarity on the federal front. Institutional investor reluctance, financial industry constraints, haphazard state regulation and the unavailability of federal forums such as national copyright and trademark registration will continue to be issues for acquirers and their lawyers in the space.

Acquisition agreements will continue to have to address the federal Damocles’ sword should expected relaxation of federal enforcement under the Biden administration and further legislative relief does not materialize as expected. Although the U.S. House in December passed the “Marijuana Opportunity Reinvestment and Expungement Act” (MORE) to remove cannabis from the Controlled Substances Act, the Senate did not take up the bill in 2020 and it will have to be re-introduced in 2021. Notably, the MORE Act does not affect existing federal regulation of cannabis, such as the Food, Drug and Cosmetics Act, under which the FDA has limited the use of CBD in certain products despite hemp being removed from the Controlled Substances Act in 2018.

The cannabis M&A market is moving into a more mature phase, as MSOs will be choosier in their approach rather than continuing the land-grab mentality of years past. Due to improved financial strength, 2021 should see these MSOs continuing to expand their footprints either within existing states or new ones. Although uncertainties abound, further consolidation and expansion through add-on acquisitions is likely to continue apace in 2021, providing plenty of opportunities for deal makers and their lawyers.

On December 16, 2020, Aphria Inc. (TSX: APHA and Nasdaq: APHA) announced a merger with Tilray, Inc. (Nasdaq: TLRY), creating the world’s largest cannabis company. The two Canadian companies combined have an equity value of $3.9 billion.

Following the news of the merger, Tilray’s stock rose more than 21% the same day. Once the reverse-merger is finalized, Aphria shareholders will own 62% of the outstanding Tilray shares. That is a premium of 23% based on share price at market close on the 15th. Based on the past twelve months of reports, the two companies’ revenue totals more than $685 million.

Both of the companies have had international expansion strategies in place well beyond the Canadian market, with an eye focused on the European and United States markets. In Germany, Aphria already has a well-established footprint for distribution and Tilray owns a production facility in Portugal.

About two weeks ago, Aphria closed on their $300 million acquisition of Sweetwater Brewing Company, one of the largest independent craft brewers in the United States. Sweetwater is well known for their 420 Extra Pale Ale, their cannabis-curious lifestyle brands and their music festivals.

Once the Aphria/Tilray merger is finalized, the company will have offices in New York, Seattle, Toronto, Leamington, Vancouver Island, Portugal and in Germany. The new combined company will do business under the Tilray name with shares trading on NASDAQ under ticker symbol “TLRY”.

Aphria’s current chairman and CEO, Irwin Simon, will be the chairman and CEO of the combined company, Tilray. “We are bringing together two world-class companies that share a culture of innovation, brand development and cultivation to enhance our Canadian, U.S., and international scale as we pursue opportunities for accelerated growth with the strength and flexibility of our balance sheet and access to capital,” says Simon. “Our highly complementary businesses create a combined company with a leading branded product portfolio, including the most comprehensive Cannabis 2.0 product offerings for patients and consumers, along with significant synergies across our operations in Canada, Europe and the United States. Our business combination with Tilray aligns with our strategic focus and emphasis on our highest return priorities as we strive to generate value for all stakeholders.”

The drug war has harmed communities of color since its inception. For decades and decades, BIPOC (Black, Indigenous, and other People of Color) have been nearly six times more likely to be arrested for drug use than White Americans, despite similar rates of use.

Over the years that legalized cannabis has proliferated across the country, the same trends of market consolidation have emerged in every state that has legalized the plant. BIPOC communities already impacted by the drug war have less access to capital and therefore less access to the cannabis industry. Cannabis market consolidation has always led to white people taking a greater market share while BIPOC communities are left behind.

The legal cannabis industry currently lacks representation of BIPOC executives, business owners, and professionals. Ernest Toney, former global marketing and partnerships manager at Marijuana Business Daily, wants to change that. He founded the BIPOC Cannabis Business Network – a membership community that is working to make the cannabis industry more accessible and profitable for BIPOC professionals and business owners.

BIPOCANN is a place to meet cannabis industry leaders, a place to exchange goods, services and ideas that promote BIPOC economic growth in cannabis, an innovation hub for unique voices and perspectives, and it’s all BIPOC-owned and managed.

In this interview, we sit down with Ernest Toney to hear about BIPOCANN and ask him some questions about what the future of the cannabis industry could look like.

Cannabis Industry Journal: Tell me about your background- how did you get involved in the cannabis industry?

Ernest Toney: I grew up in Virginia and went to James Madison University where I studied kinesiology, and sports management in graduate school. That led me to pursue a career in sports administration, beginning as a sales and marketing director for a large YMCA in the southwest, followed by a stint as a sales consultant for the Arizona Diamondbacks in Major League Baseball. Immediately prior to joining the cannabis industry, I worked at USA Ultimate – the national governing body for the niche sport of ultimate (frisbee) in the United States. During that time, I managed and scaled adult programs and events across the country. A big part of my job required collaborating with national stakeholders and creating and enforcing policies to grow the sport by making it more accessible to diverse demographics. We also worked hard to increase the commercial visibility of the sport through mainstream media, including ESPN, with gender equity being a major focus area. It was cool because looking back, I learned a lot of things during that five-year period that is directly applicable to the work I’m doing to support the cannabis industry.

Ernest Toney, founder of BIPOCANN

But my interest in the cannabis industry became strong when I moved to Denver in 2011, a year before Amendment 64 passed. When Colorado became the first adult use cannabis market in the USA, it was an exciting time. I have always been curious about economics and how policies can impact people’s lives. I was interested in what was going to happen when the new market opened.

Early on, I followed the industry trends very closely. Living in downtown Denver, I saw firsthand the effects the cannabis industry was having on day-to-day life, like increased tourism, a housing market boom, a lot of new start-ups, dispensaries opening everywhere. It was just something I knew I wanted to learn more about.

Around 2016, I started making industry connections, but didn’t pursue opportunities until a few years later. Eventually, I was hired in 2018 by MJBizDaily to focus on new business initiatives. Some of my past successes with scaling programs, national and international event management, and community-building aligned with what they were looking for.

I started as the company’s first international marketing manager. In that role, I was responsible for driving marketing campaigns to increase the company’s global readership, event registrations, and business conference presence in foreign markets. After the first year, I transitioned to identify and manage marketing partnerships for the company – which included international and domestic media, event, and affiliate partnerships within and outside of cannabis.

I felt compelled to make a change amidst the social unrest this summer. I was doing my own protesting and volunteer advocacy in Denver, but started to see more broadly, in the cannabis industry, that cannabis executives and companies were bringing attention to the fact that the War On Drugs has been problematic for minorities and communities of color. There was greater talk about social equity programs and how they are not as effective as they should be. There was greater attention to the fact that over 40,000 people are still incarcerated for the plant that others are profiting from – and that the people behind bars are predominantly coming from communities of color. I was in a position that afforded me the opportunity to see what the composition of the global cannabis industry looked like, and I could see minority representation was lacking in business ownership, leadership positions, and more.

I thought – what is the best way for me to use my talents, insights, and knowledge to affect and change this narrative? Ultimately, I decided to start my own business. Not only was this an opportunity for me to “walk the walk,” being a black man starting a business in this industry where there is a lack of black ownership, but more importantly I was uniquely positioned to be able to educate and let people know about the opportunities to be a part of the booming industry. So, I did some brainstorming and came up with a company, which is called BIPOCANN and it stands for connecting BIPOC communities to the cannabis industry.

The work I have been doing for the last quarter includes directly recruiting people into the industry. If you are curious and want to learn more about the industry, then BIPOCANN can be the entry point. We figure out what your goals are and use the network and our resources to get you connected and figure out where you want to go. Likewise, if you are a service provider, like a graphic designer, accountant, marketer or business owner for example, that sees opportunities for your business to play a role and support it from an ancillary standpoint, BIPOCANN can be an entry point for you too.

The other component to it is working with existing businesses who are trying to make the industry more accessible. I work with existing companies and brands to create platforms that amplify voices and make BIPOC folks more visible, seen and heard within the cannabis industry. We are also helping businesses increase their profitability through diversification tactics and marketing tactics that contribute to their bottom line.

CIJ: Tell me about BIPOCANN- what is it, what are your goals with this project and how has it been received so far?

Ernest: The prohibition of cannabis has disproportionately impacted communities of color in the Americas. I alluded to this earlier, but there are more than 40,000 people behind bars in the U.S. for cannabis possession and use. There’s evidence suggesting that Black Americans are up to six times more likely to get arrested for cannabis use than White Americans despite use rates being the same. And when you look at the makeup of the professional industry, there is poor representation of business ownership by people of color. The Cannabis Impact Fund references that only 4.3% of dispensaries are Black or Latinx-owned. These problems intersect in a lot of ways.

BIPOCANN is a small business working to make the cannabis industry more accessible and profitable for BIPOC professionals and business owners. Now, I know that one company cannot change 100 years of cannabis prohibition and how policy works. But if you want to make this industry more accessible, inclusive, and profitable for those who do not have the access then there are a lot of levers to pull. Policy is one. But BIPOCANN is using more direct strategies. We actively recruit people to come in and be a part of this industry, through employment, entrepreneurship, consulting, and collaborations.

We have also created the BIPOC Cannabis Business Network, a community where members can exchange services, network, and collaborate. It’s all about creating more opportunities for BIPOC professionals and business owners, and it’s a safe space to share your experiences and to ideate. Similar to your Cannabis Quality Virtual Conference, where there was a dedicated space for BIPOC folks to be seen and heard and tell their story through your virtual panels, we use our resources and network to help advocates for equity and access be seen, heard, and find opportunities to thrive as a business owner or professional.

CIJ: How do you hope BIPOCANN will be embraced by the cannabis community?

Ernest: I think it has been received well in its first quarter of business. We have had opportunities to share our story across a lot of platforms, including multiple cannabis industry conferences, podcasts, and interviews with varied media outlets. We are in startup mode, so currently we are about building a brand, being seen, and helping people understand what we are trying to achieve. We are working towards that right now. We have had some success and folks are supporting our vision and goals.

I am hoping the cannabis industry will look at BIPOCANN as another important resource within the social equity, business development, and networking landscape. I don’t want to be seen as a competitor to the organizations and individuals who have been doing similar work in this space, for much longer, but as an ally. Some of our approaches to bring new people into the industry will include strategically aligning communities and markets where we have strong ties – such as state governments, national nonprofits, and global cannabis networks.

CIJ: Where do you see the cannabis industry making progress with respect to diversity and including people of color?

Ernest: When I look at the types of conversations and coverage the industry is having, even compared to last year, it seems like more conferences, media entities, brands, and individual leaders are tuned in and trying to figure out how they can contribute to making this industry better, more equitable and more accessible. I am seeing a lot of more attention, attempts to understand where the gaps are and what to do about it.

When I take a step back to think of all the virtual conferences that have made dedicated conference tracks or even entire programs – like the National Association of Cannabis Business’ Social Equity Conference, the Emerge Canna Conference, the Cannabis Sustainability Symposium, and the Cannabis Industry Journal’s post-election social justice panel – or weekly segments from Black leaders like Dasheeda Dawson (She Blaze) and Tahir Johnson (The Cannabis Diversity Report) — those are good signs. They are creating opportunities for voices representing underserved communities in cannabis to share their perspectives and be advocates for change.

But there is still much to do and that includes greater education about the realities, histories, and challenges BIPOC and other minority communities are facing. Going back to the NACB, they recently drafted a social equity standard for state legislatures to use as a baseline for crafting policies and provisions for social equity programs. That and resources from organizations like the Minority Cannabis Business Association, Supernova Women, Cannaclusive, Minorities for Medical Marijuana, and the Massachusetts Recreational Consumer Council, for example are some useful resources for the industry.

Wana Brands is also continuing to do good work, and it was exciting to see them become the first sponsor of the inaugural Black CannaConference by the Black CannaBusiness Magazine. That was a great example of an industry leader using their dollars, marketing resources, and company values to support an event specifically dedicated to creating, developing, and enhancing Black entrepreneurs and businesses in the cannabis industry.

“It is hard to know what even a year from now will look like.”On the policy front, we just saw on election day cannabis having a ton of success at the polls, passing in every single state where there was a ballot measure.

Arizona did a good job with having social equity provisions directly included in the language on their ballot measure. I think for the states that have yet to draft a social equity program, they can look at what has worked well in some other states and also look at what has not worked well, like loopholes that invite predatory behaviors.

I’m excited to see that Governor Ralph Northam and the Virginia Marijuana Legalization Working Group are already identifying the best ways to make a recreational market a beneficial and sustainable one, and tackling how to incorporate social equity, racial equity, and economic equity into a future legalization bill. I am looking forward to learning more after an upcoming meeting with a Working Group member. Eventually, I hope to contribute towards any social equity efforts that will benefit my home state and hometown (a high poverty community that has been at the crossroads of America’s major civil rights movements, with a correctional facility that houses an inmate population equivalent to nearly 10% of the town population).

CIJ: Where do you see the industry moving in the next five years?

Ernest: Ha-ha! It is hard to know what even a year from now will look like.

Just this week the United Nations rescheduled cannabis, which is a big deal! We also saw the U.S. House of Representatives pass the MORE Act. We are inching closer towards federal legalization in the US and I think it will happen within that five-year timeframe, and it will be contentious. There will be compromises on things some folks don’t want compromises on, there will be more big money influencing the outcomes of the industry, and there will be unforeseen or unintended consequences to whatever the federal legislation looks like. I recently moderated a panel of social equity license holders, who felt that federal legalization would harm the disproportionately impacted areas (by the War on Drugs) even more! Their preference was to see cannabis de-scheduled and remain under state control.

I think federal legalization will bring another wave of major mergers and acquisitions, similar to what the Canadian market experienced in 2019, benefiting big business over small business.“We need folks who are educated and informed about these matters to be at the policymaking level to have a fighting chance.”

CIJ: Do you think we can change that?

Ernest: There are so many things at play. The legislators need to have diverse perspectives and representation from the folks in the industry, especially people of color who can speak to the impact that a century of prohibition policies have had on their communities. Those voices and stories need to be heard, but that type of representation is grossly lacking on Capitol Hill…which is all the more reason we need leaders from the aforementioned communities to have a seat at the table when decisions are made.

I say that because a lot of time there are unforeseen consequences when policies are created, so decision makers at the federal level can learn from those of us already doing the work on the local level. I recently had a conversation with a former journalist and colleague who is currently in a cannabis regulatory role. We were talking about how policy and operations intersect with social equity. He made the points that “many markets implement license caps, which are intended to prevent oversaturation of cannabis business (the idea being that density of outlets impacts use rates, and particularly youth use rates); in theory, that’s a good policy – but it comes with very real consequences for social equity applicants (because those licenses often go to the wealthiest applicants). License caps also artificially inflate the cost of those licenses (for a transfer of ownership), which also harms social equity applicants. Lotteries are also generally the result of policy and usually have disastrous results for the social equity applicant.”

So yeah – the rare opportunity to define a new industry that doesn’t just do business as usual, that can right its historical wrongs, and that will reward the communities that have been most harmed by cannabis enforcement, is now. And we need folks who are educated and informed about these matters to be at the policymaking level to have a fighting chance. The optimist in me says “we can do it!” The pessimist in me reminds me that it is 2020 and people still believe the Earth is flat. I’ll keep pushing for change, but I also won’t be surprised if this perfect opportunity to get it right goes wrong.

CIJ: How can people get involved in BIPOCANN?