It takes a lot to hack it in the wild world of cannabis.

To dip your toes in this game and open your own business, it could cost you between a quarter to three-quarters of a million dollars after licensure and other start-up expenses – and the battle doesn’t end there. Recent data supports that the turnover rate for the cannabis industry at large is extremely high when compared to other industries, coming in at a whopping 40-60% within the first 2 months.

Oh, and let’s not forget: we’re not living in the easiest of times in general. The Bureau of Labor Statistics now reports that inflation has hit 9.1 percent, the highest ever recorded level of inflation since records began. We know that people are struggling all over the place – and those struggles are even more amplified for cannabis operators and business owners. It’s no secret that amid these struggles, many legacy operators, MSOs and mom-and-pop brands alike are making the tough decision to take on costly loans, seek funding or even ultimately close their doors.

Every time a customer abandons their cart, your business is leaving money on the table.

But, in times like these, you have to remember what brought you to the table to begin with. The cannabis industry is still projected to hit a valuation of over $33B by the end of 2022 and despite the blood in the water that we’ve seen lately, operators of all sizes are still getting wins and making a profit. So, do you throw the towel in and give up on your dreams? Should you just accept that all hope is lost?

Absolutely not.

If you’re a cannabis operator who is struggling, you aren’t alone – and more importantly, you aren’t out of options yet. Not ready to go down with the ship just yet? We didn’t think so.

Here are five, expert-approved tips to create an influx of cash for your cannabis business without significantly increasing spending:

‘Trim the Fat’ of Your Business by Cutting Lean Costs

While it may seem obvious, many cannabis operators forget that “nice to have” is not the same thing as a “must have” when it comes to keeping your doors open and your bottom line healthy. Take an eagle-eyed second look at your budget and cut back as much as possible on areas that aren’t boosting revenue. Reconsider the “extras” – like software solutions, hiring non-essential staff and slow-moving inventory – and focus your attention on the products that contribute the most to your bottom line.

Make Your Customers a Priority

Focus your attention on the products that contribute the most to your bottom line.

One of the biggest mistakes that cannabis brands make is throwing so much of their marketing budget into getting new customers through the door while neglecting to show existing customers the attention they deserve for their loyalty. In today’s market, cannabis consumers have more options than ever. Why should they keep choosing you? Happy customers are customers that will weather the storm with you. Honing in on targeted ads and marketing efforts geared toward existing customers, in combination with loyalty perks, VIP deals and more is a great way to ensure your business is truly unforgettable in the eyes of the customers that keep your doors open. Looking for an extra leg up? Here’s an insider pro tip: refer-a-friend programs are a great way to get the best of both worlds and help those marketing dollars stretch a little further.

SOS: Save Our Shopping Carts

Shopping cart abandonment is a serious problem for cannabis retailers – and it happens all the time. For mobile users, it can creep as high as 85%. Shopping cart abandonment happens when a potential customer visits your site, builds an order in the cart and then either forgets to check out or chose not to execute the purchase. Every time a customer abandons their cart, your business is leaving money on the table. Fight back against shopping cart abandonment by providing clear calls to action through the shopping and checkout process and targeting customers with emails or SMS messages that include discount offers or reminders to check out.

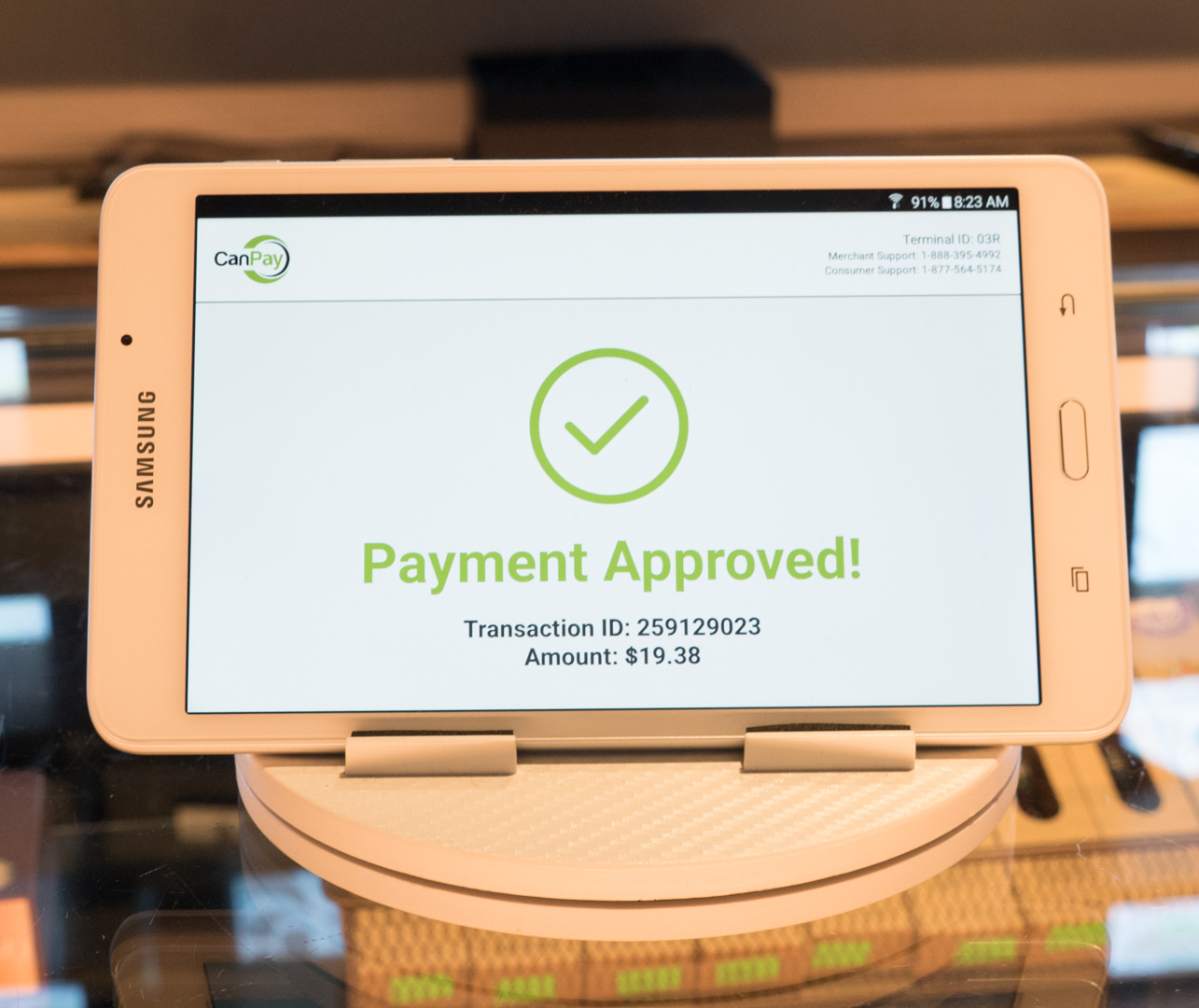

Pump Up Your Payment Solutions

It’s like Canadian rapper and singer-songwriter, Drake, said in his hit song, “Omerta”, “I don’t carry cash ‘cause the money is digital.”

Payment providers often give back a portion of transaction fees to business owners.

Let’s be honest, it’s 2022 – not a lot of people love carrying around cash. If your cannabis business is cash-only, you could be missing out on extra revenue from card and mobile payment-loving customers. On average, mobile payment users, on average, spend approximately twice as much through all digital channels as those not using mobile payments. Cash-only retailers also miss out on upsell opportunities by limiting themselves – let’s say a customer comes in with $40 in cash, they won’t be able to pick up that extra pack of cones or the grinder they were eyeing up at the checkout if they’re limited to cash-only transactions.

In addition, retailers who patronize payment solutions via debit card providers or online ACH can benefit from payment kickbacks as an additional stream of income, as these payment providers often give back a portion of transaction fees to business owners.

Don’t Forget About Employee Retention Credit (ERC)

If you haven’t heard of ERC – you could be leaving as much as $26,000 per employee on the table. Many cannabis business owners would be surprised to learn that they can still take advantage of the employee retention credit program that started during the pandemic.

The program was launched in March 2020 as a way to help offset the financial struggles of business owners during COVID-19. But, even this year, cannabis business owners can seek cash relief through ERC – employers can retroactively claim the ERC based on financial struggles they experienced during 2020 and the first three quarters of 2021.

Started your cannabis business after February 2020? You still may qualify under specific ERC provisions that can provide up to $100,000 in refundable credits.

At MJstack, we understand the trials and tribulations that cannabis professionals go through every day because we’re right here working alongside you.

Our team of professionals is familiar with cannabis and what it takes to make the cut in this world. Ready to boost your business and safeguard your investments against whatever comes next? Contact us today to learn more and book your FREE consultation.

By Tamara L. Kolb, Amy Bean, Caitlin Strelioff No Comments

As the legal cannabis market expands, banks and nonbank financial institutions (NBFIs) across the United States continue to explore how to safely provide banking and other financial services to cannabis-related businesses (CRBs) and other CRB ecosystem players. At the same time, these organizations are taking into account changes they might need to consider relative to their Bank Secrecy Act ( BSA), anti-money laundering (AML) and related compliance programs.

Regulatory conundrum

The Controlled Substances Act (CSA) identifies the cannabis plant and all its derivatives as a Schedule 1 controlled substance. Schedule 1 controlled substances have a “high abuse potential with no accepted medical use,” and they cannot be “prescribed, dispensed, or administered.” Because cannabis remains classified as a Schedule 1 controlled substance, the CSA “imposes strict controls on possession, manufacturing, distribution, and dispensing” of cannabis.

Under the Money Laundering Control Act of 1986 (MLCA) and the BSA as amended, covered banks and NBFIs are prohibited from providing financial services to businesses that are engaged in illicit activities. Because federal law prohibits the distribution and sale of cannabis, financial transactions involving CRBs are therefore deemed to be transactions that involve funds derived from illegal activities.

As of Feb. 3, 2022, 18 states, two territories, and the District of Columbia have enacted legislation to regulate cannabis for adult use. Thirty-seven states, the District of Columbia and four territories have approved comprehensive, publicly available medical and cannabis programs. Eleven states allow for the use of low-THC, high-CBD substances for medical reasons in limited situations or as a legal defense.

The growing divide between federal prohibition and state legalization of the cannabis industry creates a precarious position for federally regulated banks and NBFIs with the main concern involving exposure to legal, operational and regulatory risk. The situation begs the question: How might the federal government and regulators pursue and prosecute players in the legal cannabis industry?

The current economic trajectory predicts that retail sales of legal cannabis products in the U.S. will surpass an estimated $41.5 billion annually by 2025, and many banks and NBFIs are eagerly awaiting the federal green light to do business with CRBs without fear of prosecution or legal ramifications.

From 2018 forward, Congress has made several attempts to pass legislation that would protect CRBs when cultivating, distributing, marketing, and selling cannabis products in their state-legalized form. These efforts to declassify cannabis-related activity as a specified unlawful activity have thus far been unsuccessful.

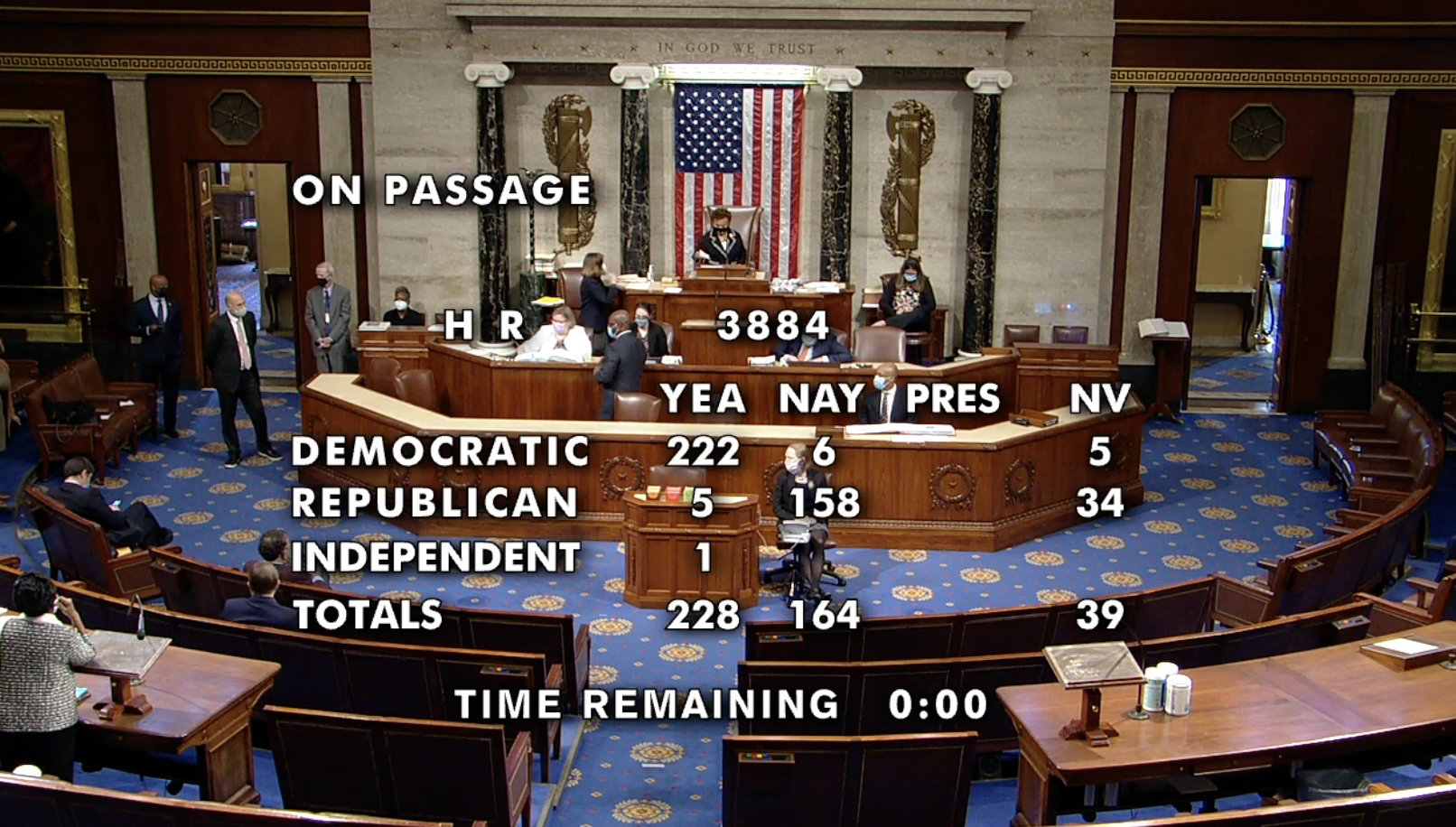

The House passing the MORE Act back in 2020

Passage of the Secure and Fair Enforcement Banking Act of 2021 (SAFE Banking Act) and the Marijuana Opportunity Reinvestment and Expungement Act of 2021 (MORE Act) would enable banks and NBFIs to provide financial services to CRBs. The SAFE Banking Act would provide a safe harbor for banks and NBFIs that provide financial services to CRBs. The MORE Act would deschedule cannabis from the CSA entirely.

Questions to ask

Banks and NBFIs interested in providing financial services to CRBs should ask these questions:

Do we adequately understand our risk, and what are the implications for our organization? How should we augment our risk assessment process and our controls?

To what extent are we willing to accept the risk of banking CRBs? Do we have the ability to identify CRB customers, and if so, do we have any?

How should we advise the board of directors about setting risk appetite?

What customer due diligence (CDD) and enhanced due diligence (EDD) will we need to safely continue with existing customers and onboard new ones?

How will we monitor for unusual and suspicious activity? What will be the alerting and judgmental criteria?

How will our resource needs change so that we stay abreast of new processes and controls?

Risk appetite considerations

In order to determine whether to accept or prohibit CRBs, banks and NBFIs should identify the level of acceptable risk they are willing to take on. Several key components need to be considered, such as:

The board of directors’ stance on legal cannabis, given that good governance recommends and regulators expect that the board sets risk appetite

Cannabis laws in states within the customer footprint and the impact on customers’ communities

Risk profile, customer base, geographic location, products, and services

Relationship with regulators and any recent deficiencies or weaknesses in the BSA and associated compliance programs

Ability to implement appropriate controls and staffing

Developing a strategic road map

If the decision is made to bank CRBs, banks and NBFIs should perform an assessment of compliance maturity for existing BSA/AML program processes and controls to identify potential gaps and develop a strategic road map that helps the organization achieve its vision for future state compliance and sustainable operations.

A well-developed and well-articulated strategic road map visualizes what actions or key outcomes are needed to help organizations achieve their long-term goals. When creating the road map, banks and NBFIs need to demonstrate a keen understanding of their desired strategy, outcomes, markets, and products for onboarding and banking CRB customers. Specifically, banks and NBFIs need to define and explain how desired outcomes and business strategies create risk and exposure.

In addition to a road map, banks and NBFIs should develop and document a detailed risk-based approach that is aligned to the organization’s risk tolerance to determine necessary compliance steps when banking CRB customers.

Specifically, the following activities should be considered when developing a CRB banking program that meets regulatory expectations:

Identifying BSA/AML control gaps related to CRB risk identification and mitigation and formulating a plan to address them

Updating a board-approved policy framework

Updating detailed operating policies and procedures

Planning for capacity, developing job descriptions, and onboarding new personnel

Training for all three lines of defense, senior management, and the board

Developing and documenting a phased or full approach to acceptance of CRB customers

Developing and documenting a CRB program oversight policy

This framework is intended to help banks and NBFIs differentiate types of CRBs and their corresponding risks, and it separates CRBs into three tiers and details risks for each tier. The following exhibit summarizes the approach:

Risk framework by tier

Level

Risk

Tier 1

Direct

Tier 2

Indirect with substantial revenue from Tier 1

Tier 3

Indirect with incidental revenue from Tier 1

Source: CRB Monitor

Even the most conservative of risk appetites equivalent to outright prohibition is not devoid of significant risk considerations. Residual risk frequently encompasses a large number of indirect connections in the total CRB ecosystem. Common examples are printers, lawyers, accountants, landlords, and even utilities and taxing authorities, and all of these are subject to regulatory scrutiny and, importantly, visibility to law enforcement. Also, policies to prohibit or restrict will be audited and examined for compliance, and exceptions will require explanations.

This panorama necessitates expertise and prudence in identifying and evaluating risks within the many layers of CRBs. For example, consider a bank or NBFI that banks a CRB’s employee or vendor. If a bank fails to properly implement controls that would allow it to identify and mitigate risk associated with banking CRBs, it will be susceptible to severe violations of the BSA, including civil money penalties, criminal penalties, and regulatory enforcement actions.

Implementing necessary precautions

A well-developed road map should consider and implement the following activities:

Understanding the most current state and federal cannabis laws and regulations to ensure the bank or NBFI’s compliance

Understanding the local, state, or tribal program to ensure CRB customers are compliant with the program

Implementing a CRB risk assessment

Implementing executive approval practices for direct CRBs

Developing adequate risk ratings (possibly through a risk-based, tiered approach) and corresponding monitoring for CRB customers that includes:

Integrating various customer onboarding and AML solutions at both onboarding and periodic levels

Scheduling regular reviews to include recurring enhanced due diligence, site visits, and transaction monitoring

Monitoring for suspicious activity, including red flags, via open sources for adverse information about the CRB customers and related parties such as beneficial owners

Performing adequate CDD and EDD that will validate that the CRB-offered products, services, and programs are compliant with most current state laws and regulations by:

Collecting appropriate documentation as evidence of compliance, perhaps including a comprehensive onboarding questionnaire, beneficial ownership information, and contracts for the growing, harvesting, transporting and processing of the product

Reviewing applications and supporting documentation used to obtain a legal cannabis state license

Understanding the normal and expected activity of the organization’s CRB customers and their product usage

Developing adequate training programs and governance and oversight programs to address this customer type by:

Updating existing policies and procedures to review inherent risk presented by banking CRB customers

Updating annual training for employees

Auditing initial program design and periodic operational effectiveness

Moving forward cautiously

The ins, outs, and unknowns of cannabis banking are complex, and they require banks and NBFIs to be extremely vigilant with current policy and aware of new developments. Overall, the idea of creating a cannabis program might seem like a daunting task, but with appropriate guidance and care, organizations can provide services in compliance with laws and regulations.

Crowe disclaimer: Qualified organizations only. Independence and regulatory restrictions may apply. Some firm services may not be available to all clients. Given the continued evolution and inconsistency of various state and federal cannabis-related laws, any company should seek competent legal advice relating to its involvement in the cannabis industry, including when considering a potential public offering as a cannabis-related company.

Federal regulations have made compliant credit processing in the cannabis industry difficult to achieve. As a result, most cannabis retailers operate a cash-only model, limiting their ability to upsell customers and placing a burden on customers who might rather use credit. While some dispensaries offer debit, credit or cashless ATM transactions, regulators and payment processors have recently been cracking down on these offerings as they are often non-compliant with regulations and policies.

KindTap Technologies, LLC operates a financial technology platform that offers credit and loyalty-enabled payment solutions for highly regulated industries typically driven by cash and ATM-based transactions. KindTap offers payment processing and related consumer applications for e-commerce and brick-and-mortar retailers. Founded in 2019, the company is backed by KreditForce LLC plus several strategic investors, with debt capital provided by U.S.-based institutions.

We interviewed Cathy Corby Iannuzzelli, co-founder and chief payments officer at KindTap Technologies. Cathy co-founded KindTap after a career in the banking and payments industries where she launched multiple financial and credit products.

Aaron Green: Cathy, thanks for taking the time today. How did you get involved in the cannabis industry?

Cathy Corby Iannuzzelli, co-founder and chief payments officer at KindTap Technologies

Cathy Corby Iannuzzelli: I’ve been in the payments industry for a long time. I was doing some consulting a few years ago for a client in Colorado and that gave me exposure to the issues in cannabis like the fact that you couldn’t have real payments in cannabis. Then, a close family member with health issues turned to medical cannabis when nothing else seemed to work. I was amazed by the difference it made in her life. At that point, I put those two things together and I said, I need to focus on helping this industry get a real cannabis payments solution because I thought it was ridiculous that you had an industry of this size and importance that had been abandoned by the payments industry.

Aaron Green: Can you highlight some of your background prior to entering cannabis?

Corby Iannuzzelli: Throughout my career, I’ve been a banker, I’ve been a payment processing executive and I’ve been a consultant. So, I’ve kind of done it all in the payments and financial services space.

Aaron Green: Why is it that most dispensaries only take cash?

Corby Iannuzzelli: In the US, even though cannabis is legal in many states, it’s still illegal federally. There are big banks and card networks like Visa, MasterCard, etc., who are national, even global companies and frankly, the executives of those companies don’t want to end up in jail for violating national laws. So, they have put cannabis dispensaries on what’s called a “prohibited merchants” list. This means you cannot accept Visa, MasterCard, Discover, American Express, or similar payments as a cannabis business and so it’s forcing the industry to a cash-based solution.

About the only thing you’re seeing that’s not cash in dispensaries are ATMs. But if you think about it, ATMs are machines where the consumer goes and pulls cash out and pays upwards of $5 or more in fees for doing that. They then hand that cash back to the dispensary who then has the costs of having to deal with that cash. The industry is just stuck in a cash-based business until federal legislation changes.

Aaron Green: I’ve been to some dispensaries where they accept credit cards or debit cards. What is going on there?

Corby Iannuzzelli: I’ve heard reports of consumers who’ve been able to use a credit card or a debit card in a dispensary. Sometimes the processor who sold that solution to the dispensary says, “Oh, it’s compliant, I guarantee you it’s compliant.” But if you dig in, that’s not the case. And eventually, Visa or MasterCard figures it out and shuts it down. In some cases, it’s outright fraud where the processor who sold the payment terminal to the dispensary is misrepresenting it as say a doctor’s office rather than a dispensary. There’s no merchant category code in the payment networks that says this is for processing dispensary payments, so they pretend it’s something else until they get shut down.

When they do get shut down, I’ve heard of cases in Las Vegas where it was basically 100% Visa or MasterCard one day and 100% cash the next day. It completely disrupted the whole business. It’s not just the retail store, but the inventories and everything else throughout the business.

“About the only thing you’re seeing that’s not cash in dispensaries are ATMs”

There have also been some cases where you’ll see something called a cashless ATM. In a store, they call it a debit card transaction. It’s really a cashless ATM where the consumer is making what looks to the ATM network like a cash withdrawal in $10 or $20 increments, but the consumer is getting a receipt instead of cash, and they’re turning around and handing that receipt back to the dispensary who then makes a change because the cashless ATM only dispensed in $10 or $20 increments.

Now ATM networks are looking at these cashless ATM transactions to see if they are compliant. Do consumers know the fees that they’re paying? Are these transactions coming in and looking to the network like real cash when it’s not? Cashless ATM transactions are probably the most common thing you see, but that’s being called into question after the Eaze incident where a large company was misrepresenting its terminals. The federal government stepped in and called it bank fraud and the individuals behind it, the executives, are in jail. Since then, the networks are looking at this and saying, what about these cashless ATMs? Are those transactions within our rules, or is there something funny going on here?

Aaron Green: So, to summarize here: you’ve got federal regulations at the national level that says that cannabis banking is not allowed so major institutions are not offering it. Yet you found a way through the regulations and compliance issues. I’m curious can you pull back the curtains a little bit and tell us how you came up with a solutionhere?

Corby Iannuzzelli: Well, we came up with the solution by stubbornly refusing to believe that cannabis payment processing could not be done in a compliant manner. We just said, “there is a compliant way to do this, let’s figure it out.” We took the same components that are out there for the financial services and payments industry and reassembled them in such a way that we do not violate any rules. We do not use any of the Visa, MasterCard, Discover or Amex rails, we built our own network. We have direct contracts with the merchants and direct contracts with the consumers. We control everything and all the funds flow through regulated financial institutions. So, we designed something that looks and acts to consumers and retailers the way Visa and MasterCard look and act when a consumer goes to make a purchase, but they run on a separate set of payment rails and in compliance with banking regulations and state regulations. When you’re looking at the problem from a different perspective, sometimes you can come up with a better answer.

Green: On the consumer side, what does that user experience look like?

Corby Iannuzzelli: Our product is completely digital. The consumer experience starts with integration at the online checkout. When it’s an e-commerce shopping cart and somebody is placing an order, they will see a button called “Pay with KindTap.” The first time they click that button they’re automatically brought to our integrated web app where they do a quick and easy application for our digital revolving line of credit product. If approved, they instantly go back to the checkout screen and their first purchase will just happen immediately, with flexible payment options over time. If the consumer decides they don’t want our KindTap credit and would rather have a pay now-product where we pull the funds from their bank account, then the consumer can do so. So, there is no physical card per se, it’s integrated like PayPal or Affirm at the point of checkout online. For the consumers who use KindTap credit, there is a mobile app where they can see their transactions, view statements, pay their bills, etc.

Additionally, there is a loyalty program for all purchases – KindTap credit or through the consumer’s bank, because we feel very strongly that a lot of the reasons consumers choose to pay with one card over another is the points and the rewards that they get. So, we’re providing loyalty rewards with KindTap so that consumers can get rewarded for that spending with KindTap and it’s better for the retailers.

Green: On the retailer side, what does that experience look like and what is your business model?

Corby Iannuzzelli: We are not going store by store doing integrations, rather, we’re integrating with various software, delivery and e-commerce providers. That gives us broad reach and ability to expand rapidly in various state markets where cannabis is legal. Once a merchant says “yes, I want to be a member of the KindTap Merchant Network,” then we work to get them set up on our platform in a matter of days. The merchants receive continuous support from our success team, marketing co-investment and a depth of analytics reporting. We made the entire process and ongoing operations streamlined and frictionless for both merchants and consumers.

Aaron Green: What are the benefits of moving from cash to credit type of payments?

Corby Iannuzzelli: On the retail side, there are the obvious benefits of not having all the security, safety and theft issues associated with operating a physical cash business. Consumers very often don’t carry cash anymore, except when they’re making a cannabis purchase. There are a lot of hidden costs to retailers because payments are not just about moving money from the consumer to the business.

“I really am optimistic that with so many scientific breakthroughs we’ve had that we’re going to be able to figure this out.”Payment options – or lack thereof – can shape where people shop, how much they spend and what they buy. It’s a proven science how consumers make impulse purchases. If you’re a cash-based business in cannabis, and you’re trying to get somebody to make an impulse purchase, and they walked in with $100, then you can’t get them to spend more than $100, no matter how creative your marketing is! The consumer is limited by how much cash they have in their bank account or in their pocket at that point in time. So, it’s really about the upsell that comes with the bigger basket sizes that retailers experience when you move from a cash-based business to credit and suddenly, the merchant doesn’t have to deal with long lines of consumers on payday when the store was beyond slow two days before. Now the consumer can spread purchases with the thinking, “I’d rather not be the one standing in that line on payday. I’m going to go Wednesday [instead of Friday] because I have KindTap credit so I can budget and manage my cash flow throughout the month rather than around my paydays.”

So, we think that the lack of an efficient and effective payment system for cannabis is holding back sales. We all focus on how much the industry is growing. KindTap thinks about how much faster it could be growing if it was supported by a decent payment system.

Aaron Green: What are some other cash-only markets you are looking at?

Corby Iannuzzelli: We are laser-focused on the cannabis ecosystem and bringing a compliant credit and loyalty-based digital payments solution to cannabis merchants and customers and rewarding those stakeholders for accepting/using KindTap. Additionally, we are planning to extend the KindTap Merchant Network so that consumers can use/earn our loyalty points with other goods and services they’re purchasing that are adjacent to cannabis or that are important to the cannabis consumer. That’s the direction we’re going.

Aaron Green: Today people can receive gas points for spending with their credit card. Now with KindTap, you can spend to get cannabis points?

Corby Iannuzzelli: That’s exactly right.

Aaron Green: What in either cannabis or your personal life are you most interested in learning about?

Corby Iannuzzelli: Personally, I am most interested in seeing breakthrough technologies in climate change. We’re going to need to correct this situation and I’m reading about collecting carbon dioxide from the air and burying it in the earth and things like that. I really am optimistic that with so many scientific breakthroughs we’ve had that we’re going to be able to figure this out. Certainly, it’s going to take a lot of smart people and a lot of investment, but I really look forward to watching them do their stuff and hopefully taking us out of this nightmare situation that we’re heading into if we don’t make some changes.

Aaron Green: Thanks Cathy, that concludes the interview.

Few people will disagree that financial compliance isn’t the most exciting topic within the cannabis industry. But compliance is, and always will be, the engine grease to the legal cannabis market. Cannabis operators have the arduous task of dealing with multiple layers of compliance, both operational (maintaining and adhering to regulations enforced by the state licensing board) and financial. These compliance measures include managing everything from seed-to-sale systems for all plant-related activity to on-site requirements like facility access points and alarms systems to name a few.

With complex compliance requirements for the business, the last thing cannabis operators want to think about is financial compliance. We created Confia on this notion. Just as cannabis regulators impose the tracking of plants through the supply chain via a seed-to-sale system, we have developed a storyboard similarly designed to follow the money, which is the equivalent of a transaction-to-deposit system.

Having experience in regulatory technology, artificial intelligence and machine learning, we’ve been fortunate enough to work with some of the world’s largest banks across multiple countries. This experience has afforded us the luxury of working alongside regulators, chief compliance officers and chief risk officers, understanding how risk is perceived by financial institutions and how it ought to be mitigated. It was this access and knowledge that allowed us to effectively reform, enhance and improve the antiquated BSA programs with a technology-enabled process. Leveraging technology is a necessity, almost a requirement, for the cannabis industry as legalization nears and banking access begins to broaden.

Jamming cannabis requirements into an existing BSA program doesn’t scale well. BSA programs are very manual, descriptive and process oriented. So, we’ve taken our prior experience and success in banking to form Confia, distilling the complexities and simplifying the deliverables surrounding cannabis banking compliance. To best articulate cannabis banking requirements, I break it down into three pillars.

Pillar One: KYC-Enhanced Due Diligence

The first pillar is the client-onboarding bucket or KYC – Know Your Customer. In the complex world of cannabis banking, banks must know and understand their clients to great depths. It’s not enough to simply know that the client exists; you also have to understand whether or not that client could be a potential risk to the bank, and one step further, the financial system. Cannabis is a high-risk industry, so the KYC requirement is escalated to a deeper diligence and review, called Enhanced Due Diligence (EDD).

Cannabis is a high-risk industry so extra due diligence is needed

Banks need to know and understand their customers’ story, and all the key parties (officers, directors, and those with key decision-making powers or access to the bank accounts) within that organization. This includes reviewing personal, business, and legal history – not to mention watchlists and negative news presence. An initial onboarding review must then be followed with daily screening and monitoring of all watchlists and adverse media. Typically, banks do KYC refreshes every three years. In cannabis, a full refresh should be done annually with the daily monitoring systems in place.

The high-risk nature of the industry also requires a level of diligence on all parties to a transaction, even if one of the parties, whether a payer or recipient, is not a client of your bank. Unlike traditional banking sectors, reliance on other banks’ KYC programs is far less defensible in the cannabis industry.

Pillar Two: Transactional Monitoring & Detection

Tracking and monitoring the actual financial transactions comprises the second pillar required for cannabis banking. At Confia, we have focused on streamlining processes, so the cannabis operator can seamlessly support the compliance obligation for every transaction. A bank must demonstrate supporting documentation for every cannabis transaction, and gathering such information is a large undertaking in and of itself and can pose future issues if not done properly, see the pitfalls for lack of compliance. Banks are obligated to understand the nature and reason for each transaction, the source of funds, ensure cannabis licenses are in good standing for all parties, and collect evidence such as accounting records and seed-to-sale data.

Core to transaction monitoring in the traditional sense, is the overarching support through anomaly detection. Relying on information is important, but testing those inputs keeps everyone honest. It is important to evaluate transactions from a holistic point of view relative to peers and relative to the general contents of a transaction. This anomaly detection layer is your last line of defense, and as new information is collected, it continues to refine itself.

Pillar Three: Filing and Reporting Requirements

The third component to compliant cannabis banking is regulatory filing and reporting. Once a client is onboarded, the account requires an initial suspicious activity report or SAR-Initial within 30 days of that client being approved by the bank. Then, a report must be filed every 90 days after that for all the transactions of that cannabis operator. Banks must file the SAR-Initial and the Continuing-SAR reports for each cannabis client they have.

The high-risk nature of the industry requires a level of diligence on all parties to a transaction

Solutions like Confia automate the filing process and support the filing with transactional data evidenced on our distributed ledger of record. This provides immutable audibility and simplifies the process for all parties involved.

Compliance Requirements After US Legalization

The anticipation of federal legalization and banking reform bills has many operators hoping for easier banking. Yet, in my opinion, regulatory oversight and audits will likely increase after such reform or legalization. As other financial institutions start to support cannabis, it will inadvertently create greater opportunity and expose the financial system to nefarious or illegitimate transaction activity. This is why cannabis banking will be carefully monitored by regulators, and more so, why banks will be slow and pragmatic in standing up their internal cannabis banking programs. Some banks may forever avoid the cannabis industry due to the known pitfalls of an industry specific program, while others may simply mitigate the possible exposure to reputational risk.

Choose Wisely: Pitfalls for Lack of Compliance

Financial compliance is the responsibility and duty of the banks, but the real losers and result of non-compliance always fall on the cannabis operators. Regulatory action against an institution may result in the bank shutting down its cannabis program or may require them to complete a remediation of all their cannabis transactions for a certain period from its clients. At the end of the day, regardless of action, the cannabis operator is the one being punished. Operators either lose their bank account and have business massively disrupted, or they are asked to provide all the compliance docs for a historic period, which is a huge undertaking and operational distraction, ultimately impacting business and productivity. So, choose your banking partner wisely.

Summarizing Key Banking Requirements

In summary, banking in the cannabis industry will undoubtedly remain a high-risk industry, with or without legalization. Although banking opportunities may expand as US policies change, there will be continued compliance and regulatory requirements for the foreseeable future.

Onboarding and ongoing screening are critical

Evidence for every transaction is a significant portion of compliance and must not be dismissed

Evaluating activity with broader strokes is essential in mitigating against money laundering

Managing the staggered filing timelines and due dates for each client

Compliance is the most crucial factor in cannabis banking at this point. It cannot be overlooked or taken for granted. Cannabis operators must take an active role in evaluating the compliance programs of their financial providers. To open a bank account is one thing, but the consideration and effort that goes into keeping a bank account is the difference that will protect your business in the long run.

Cannabis is still federally illegal and is included on Schedule 1 of the Controlled Substances Act (CSA), along with such other substances as heroin, fentanyl and methamphetamines.1 It is a federal crime to grow, possess or sell cannabis.

Despite being federally illegal, 36 U.S. states and the District of Columbia have legalized the sale and use of cannabis for medical and/or adult use purposes,2 and both direct and indirect cannabis-related businesses (CRBs) are growing at a rapid rate. Revenue from medical and adult use cannabis sales in the US in 2019 is estimated to have reached $10.6B-$13B and is on track to reach nearly $37B in 2024.3

Because the sale of cannabis is federally illegal, financial institutions face a dilemma when deciding to provide services to CRBs. Should they take a significant legal risk or stay out of the market and miss out on a significant revenue opportunity? So far, the vast majority of financial institutions have been unwilling to take the risk, resulting in a dearth of options for CRB’s. Until recently, cannabis business operators had few options for financial services, but times are changing.

This piece will discuss current trends in banking for cannabis-related businesses. We will cover differences in legality at state and federal levels, complexities in dealing in cash versus digital currencies, Congressional actions impacting banking and CRBs and how banking is changing. The explosion of state legalization of cannabis over the past several years has had a strong ripple effect across the US economy, touching many industries both directly and indirectly. Understanding the implications of doing business with a CRB is both challenging and necessary.

Feds Versus States

Money laundering is the process used to conceal the existence, illegal source or illegal application of funds.4 In 1986 Congress enacted the Money Laundering Control Act (MLCA), which makes it a federal crime to engage in certain financial and monetary transactions with the proceeds of “specified unlawful activity.”5 Therefore, CRB transactions are technically illegal transactions under the MLCA.

Financial institutions therefore face a risk of violating the MLCA if they choose to do business with CRBs, even in states where cannabis operations are permitted. In addition, financial institutions could also face criminal liability under the Bank Secrecy Act (BSA) for failing to identify or report financial transactions that involve the proceeds of cannabis businesses operating legally under state law.6

Federal authorities continued to aggressively enforce federal cannabis laws

In short, because cannabis is illegal at the federal level, processing funds derived from CRBs could be considered aiding and abetting criminal activity or money laundering. States, however, began legalizing cannabis in 1996, and by 2009, thirteen states had laws allowing cannabis possession and use.7 Despite this legislation, federal authorities continued to aggressively enforce federal cannabis laws.8 That changed under the Obama administration when, shortly after being elected, President Obama stated that his administration would not target legal CRB’s who were abiding by state laws.[9] In an attempt to provide clarity in this murky environment, beginning in 2009, the Department of Justice (DOJ) issued three memos designed to guide federal prosecutors in this area. However, none of the DOJ memos issued from 2009 through 2013 addressed potential financial crime related to the legal sale or distribution of cannabis in states allowing the use of medicinal or recreational cannabis.

To assist financial institutions in navigating potential financial crime implications of banking CRBs, the Financial Crimes Enforcement Network (FinCen) issued guidance in 2014 that clarified how financial institutions could conduct business with CRBs and maintain compliance with their Bank Secrecy Act requirements (2014 Guidance).9 According to the 2014 Guidance, financial institutions may choose to interact with CRBs based on factors specific to each institution, including the institution’s business objectives, the evaluated risks associated with offering such services, and its ability to manage those risks effectively.

The 2014 Guidance requires those who choose to provide services to CRBs to design and implement a thorough customer due diligence review that includes, in part, analyzing the licensing of the entity, developing an understanding of the business operations of the entity, and ongoing monitoring of the entity.9 In addition, financial institutions are required to file a Suspicious Activity Report (SAR) for every transaction they process for a CRB, should they choose to accept the business.

Although the 2014 Guidance does outline a path for financial institutions to engage with CRBs, it does not change federal law and, therefore, does not eliminate the legal risk to financial institutions.10 By its very nature, the 2014 Guidance was a temporary fix, subject to changing views of different administrations, evidenced by the fact that all three of the DOJ guidance documents noted above were rescinded by then Attorney General Jeff Sessions on January 4, 2018.12 The DOJ enforcement posture could change once again in a Biden administration. Biden is on record as favoring decriminalization, and Attorney General candidate Merrick Garland has stated that if confirmed he will deprioritize enforcement of low-level cannabis crimes. Garland also believes using limited government resources to pursue prosecution of cannabis crimes states where cannabis is legal does not make sense.12

Because of the uncertainty and high risk, most banks remain unwilling to serve CRBs. Those that do serve CRBs charge exorbitant fees (fees of $750-$1,000 or more per account per month are not uncommon), pricing many smaller operators out of the financial services market.

Cash is King – Or Is It?

Cannabis operators have discovered the old adage “cash is king” is not necessarily true when it comes to the cannabis space. Bank-less CRBs are forced to utilize cash to pay business expenses, which can be particularly difficult. Utility companies, payroll companies, and taxing authorities are just some of the providers that are difficult, if not impossible, to pay in cash. For example, cannabis operators have been turned away from IRS offices when attempting to pay large federal tax obligations in cash. Likewise, cannabis operators have been unable to utilize payroll processing companies to administer payroll and benefits for their businesses because the processors won’t take cash. CRBs can’t use Amazon or other online retailers because online providers cannot accept cash.

Because dealing in cash is so difficult, CRB operators look for workarounds such as using personal credit/debit cards to purchase business equipment and supplies. This doesn’t eliminate the cash problem, however, because the credit card holder will likely have to accept cash as reimbursement. Such transactions could be considered an attempt to hide the source of the cash, which is, by definition, money laundering.

CRBs often have large sums of money onsite

Some bank-less CRBs try to skirt the system by obtaining bank accounts in the name of management companies or other entities one step removed from the actual business. While operators often choose this route in an effort to streamline business and operate out of the shadows, it again runs afoul of banking laws. Transferring cannabis related financial transactions to another entity is actually the very definition of money laundering – which, as noted above, is defined as the process used to conceal the existence or source of “illegal” funds.

In addition to the difficulties in making payments or purchasing business supplies, operating in a cash-heavy environment poses significant safety risks for cannabis operators. CRBs often have large sums of money onsite and transport large sums of cash when purchasing product or paying bills, making them a target for robbery. In 2017, there was a spate of dispensary robberies across the Phoenix Metro area, including one at Bloom Dispensary that took place during operating hours.13

Managing all that cash increases the cost of doing business as well, in the form of increased labor, insurance, and security costs. Cash must be counted and double counted, which can be time consuming for staff, not to mention the time it takes to deliver physical cash payments to hither and yon. Ironically, lack of banking significantly decreases transparency and clouds the waters of compliance, as operating strictly in cash makes it easier to manipulate reported financial results.

Potential Congressional Solutions

In recent years Congress has undertaken several efforts to pass legislation designed to address the state/federal divide on cannabis, which would likely clear the way for financial institutions to provide services to CRBs, including:

R. 1595 – Secure and Fair Enforcement Banking Act of 2019 (“SAFE Act”);

1028 & H.R. 2093 – Strengthening the Tenth Amendment Through Entrusting States Act (STATES Act); and

2227 – Marijuana Opportunity Reinvestment and Expungement Act of 2019 (MORE Act).

The climate in Washington DC, however, did not allow any of these initiatives to pass both houses of congress. Had any been sent to the White House, President Trump was unlikely to sign them into law.

The cannabis industry has new reason to believe reform is on the horizon with shift in political leadership in the White House and Senate. Newly anointed Senate Majority Leader Chuck Schumer recently committed to making federal cannabis reform a priority, and President Biden appears committed to decriminalization, reviving the hope of passage of one of these pieces of legislation.

The Changing Banking Landscape

Even though there is little in the way of formal protections for financial institutions, and with the timeline for a legislative fix unknown, an increasing number of banks are working with cannabis operators.

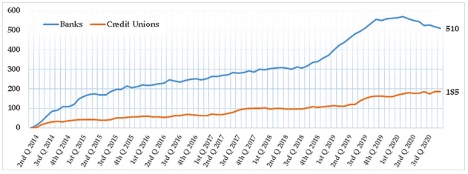

According to FinCen statistics, there were approximately 695 financial institutions actively involved with CRBs as of June 30, 2020. It is important to note that these statistics are based on SAR filings, which banks are required to file when an account or transaction is suspected of being affiliated with a cannabis business. However, some of these SARs may have been generated on genuine suspicious activity rather than on a transaction with a known cannabis customer.

Number of Depository Institutions Actively Banking Cannabis-Related Businesses in the United States (Reported in SARS)14

There are arguably more banking institutions offering services to CRBs than ever before. The challenges for CRBs are (1) finding an institution that is willing to offer services; (2) building/maintaining a compliance regime that will be acceptable to that institution; and (3) cost, given the high fees associated with these types of accounts.

How CRBs Get Accepted by Banks

The gap between CRBs’ need for banking and the financial services providers’ sparse and expensive offerings to the sector has created an opportunity for third-party firms to intervene and provide a compliance structure that will satisfy the needs of the financial institutions, making it easier for the CRB to find a bank.

These third-party firms perform extensive BSA-compliant due diligence on applicants to ensure potential customers are following FinCen guidance required to receive banking services. After the completion of due diligence, they connect the CRBs with financial institutions that are willing to do business with CRBs and provide checking/savings accounts, check writing capability, and merchant processor accounts. These firms often provide additional services such as armored car and cash vaulting services. Some of these firms also offer vendor screening, pre-approving vendors before any payments can be made.

One such firm, Safe Harbor Private Banking, started as a project implemented by the CEO of Partners Credit Union in Denver, Colorado, who set out to design a cannabis banking program that would allow Partners to do business with Colorado CRBs.15 The program was successful and has since expanded into other states who have legalized cannabis. Other operators include Dama Financial and NaturePay.

While these services offer hope for many CRBs, the downside is cost. These services perform the operations necessary to find, open, and maintain a compliant bank account; however, the costs of compliance are still high, pricing some small operators out of the market.

Is Digital Currency an Answer?

Digital currency is also making its way into the cannabis world. Digital currency, or cryptocurrency, is a medium of exchange that utilizes a decentralized ledger to record transactions, otherwise known as a blockchain. One of the largest benefits of blockchain is that it is a secure, incorruptible digital ledger used for, among other things, financial transactions.16 Blockchain technology offers CRBs a transparent and immutable audit trail for business and financial transactions. Several cannabis-specific cryptocurrencies have sprung up in the past several years, including PotCoin, CannabisCoin, and DopeCoin, to name a few.

In July 2019, Arizona approved cryptocurrency startup ALTA to offer services to the state’s medical cannabis operators.17 ALTA describes itself as a “digital payment club where cash-intensive businesses pay each other using digital tokens instead of cash.”18 ALTA members purchase digital tokens that are used to pay other members using a proprietary blockchain based system. The tokens are redeemable for US dollars at a stable rate of 1:1, and CRBs do not need a bank account to participate in the ALTA program.

ALTA proposes to pick up members’ cash and exchanges it for tokens, which are then used to pay other members for goods and services. Tokens may be redeemed for cash at any time.18 The company has been approved by the Arizona State Attorney General, and one of the first members they hope to enlist is the Arizona Department of Revenue (ADOR). Enlisting ADOR into the program would allow dispensary members to pay state taxes digitally rather than hauling large amounts of cash to ADOR offices.

Similarly, Nevada recently contracted with Multichain Ventures to supply a digital currency solution to the Nevada cannabis industry. Nevada Assembly Bill 466 requires the state create a pilot program to design a “closed loop” system like Venmo in an effort to reduce cash transactions in the cannabis sector. Like ALTA, Nevada’s proposed system will convert cash to tokens which can then be transacted between system participants.19

While both proposals are promising for Arizona and Nevada CRBs, the timeline as to when, or if, these offerings will come online is unknown. Action on cannabis reform at the federal level may render these options moot.

Looking to the Future

Although states are legalizing cannabis in one form or another in growing numbers, the fact that cannabis is still federally illegal poses a significant barrier to accessing the financial services market for CRBs. While most banks are still reluctant to offer services to this rapidly growing industry, there are more banks than ever before willing to participate in the cannabis industry. Recent changes in leadership in Washington DC offer a positive outlook for cannabis reform at the federal level.

As the “green rush” continues to envelop the country, financial services options available to CRBs are slowly growing. Many new options are now available to help CRBs find a bank, develop compliance programs, and manage the cash related problems encountered by most CRBs. However, these solutions may be out of reach for the budget-conscious small operator. Also, there are a number of cryptocurrency solutions designed specifically for CRBs; however, when, or if, these solutions will gain significant traction is still unknown.

References

Controlled Substances Act, 21 U.S.C., Subchapter I, Part B, §812.

“State Marijuana Laws”; National Conference of State Legislatures, February 19, 2021.

“Exclusive: US Retail Marijuana Sales On Pace to Rise 40% in 2020, near $37B by 2024”. Marijuana Business Daily, June 30, 2020.

Kaufman, Irving. “The Cash Connection: Organized Crime, Financial Institutions, and Money Laundering”. Interim Report to the President, October 1984.

S. Code § 1956 – Laundering of Monetary Instruments.

Rowe, Robert. “Compliance and the Cannabis Conundrum.” ABA Banking Journal, September 11, 2016.

“History of Marijuana as a Medicine – 2900 BC to Present”. ProCon.org, December 4, 2020.

Truble, Sarah and Kasai, Nathan. “The Past – and Future – of Federal Marijuana Enforcement”. org, May 12, 2017.

Sessions, Jefferson B. “Memorandum for All United States Attorneys”. January 4, 2018.

“Attorney General Nominee Garland Signals Friendlier Marijuana Stance”. Marijuana Business Daily, February 22, 2021.

Stern, Ray. “Robbers Hitting Phoenix Medical Marijuana Dispensaries: Is Bank Reform Needed?” The Phoenix New Times, April 11, 2017.

FinCen Marijuana Banking Update, June 30, 2020.

Mandelbaum, Robb. “Where Pot Entrepreneurs Go When the Banks Just Say No.” The New York Times, January 4, 2018.

Rosic, Ameer. “What is Blockchain Technology? A Step-by-Step Guide for Beginners.” com, 2016.

Emem, Mark. “Marijuana Stablecoin Asked to Play in Arizona Fintech Sandbox.” CCN.com, October 25, 2019.

http:\\Whatisalta.com\

Wagner, Michael, CFA. “Multichain Ventures Secures Public Sector Contract with Nevada to Supply Tokenized Financial Ecosystem for the Legal Cannabis Industry”, January 26, 2021.

In a press release sent out this morning, a new coalition announced their launch to “end the prohibition, criminalization, and overregulation of cannabis in the United States.” The Cannabis Freedom Alliance (CFA) says their core values include federal descheduling, criminal justice reform, “reentry and successful second chances,” promoting entrepreneurship in free markets and reasonable tax rates.

Who’s Behind the CFA?

The organizations that founded the CFA are Americans for Prosperity (AFP), Mission Green/The Weldon Project, the Reason Foundation, and the Global Alliance for Cannabis Commerce (GACC). Take a look at that list and see if you recognize the names. AFP is a well-known conservative and libertarian political lobbying group founded and funded by the Koch brothers. The Reason Foundation, another Libertarian think-tank and an advocate for prison privatization, also listed the Koch brothers as some of their largest donors in disclosures filed in 2012.

The Koch family business, Koch industries, makes hundreds of billions of dollars a year in the oil and gas industry and has held massive political influence for decades. They regularly donate hundreds of millions of dollars to Republican campaigns. Historically, they’ve played a major role in opposing climate change legislation. They’re widely known as conservative advocates for lower corporate taxes, less social services and deregulation.

Interestingly enough, prominent criminal justice reform advocate Weldon Angelos and rapper Snoop Dogg appear to have joined forces with the Koch-backed group, CFA, following a Zoom meeting where Charles Koch told them he thinks all drugs should be legalized, according to Politico. “We can’t cut with one scissor blade. We need Republicans in order to pass [a legalization bill],” Angelos told Politico. The tie between cannabis legalization and traditional Republican and Libertarian values is obvious: their free market, personal liberties and small government ideology fits well within the legalization movement.

Big Oil, Alcohol and Tobacco, Oh My!

The Coalition for Cannabis Policy, Education and Regulation (CPEAR) is a group that was founded in March 2021. Two of the founding members are Altria, the company that makes Marlboro cigarettes, and Molson Coors, a multinational alcohol company. The CPEAR website says that they want to work on responsible federal reform. “We represent a vast group of stakeholders — from public safety to social equity — focused on establishing a responsible and equitable federal regulatory framework for cannabis in the United States.”

Founding members of CPEAR also include: The Brink’s, a private security firm, the National Association of Convenience Stores, the Council of Insurance Agents & Brokers and the Convenience Distribution Association. In other words, the group is made up of large and powerful corporate interest groups that represent the alcohol, tobacco, insurance and security industries.

Both NORML and the Drug Policy Alliance (DPA) have spoken out against CPEAR. Erik Altieri, executive director of NORML, says it’s a matter of corporate interests coming in and working to change laws for their companies to capitalize on legalization. “We’ve seen how big corporate money and influence have corrupted and corroded many other industries,” says Altieri. “We can’t let the legal marijuana industry become their next payday.”

The DPA also released a statement opposing CPEAR. Kassandra Frederique, executive director of the DPA, says that she urges caution to elected officials in taking counsel from these corporate powers. “We have long been concerned about the entry of large commercial interests into the legal marijuana market,” says Frederique. “Big Alcohol and Tobacco have an abysmal track record of using predatory tactics to sell their products and build their brands – often targeting low-income communities of color and fighting public health regulations that would protect people.”

While their motives and desired outcomes remain unclear, it is apparent that we’re reaching a new age in the cannabis legalization movement, one where powerful corporations outside of the cannabis space want in. Whether its oil and gas, insurance, security, tobacco or alcohol, these groups are using their power and money to influence cannabis policy reform.

The unusual nature of 2020 gave rise to a reciprocally roller-coaster-like cannabis market. Cannabis was cemented officially as an essential industry with the rise of COVID-19, and November elections resulted in even more United States markets welcoming medical and adult-use sales.

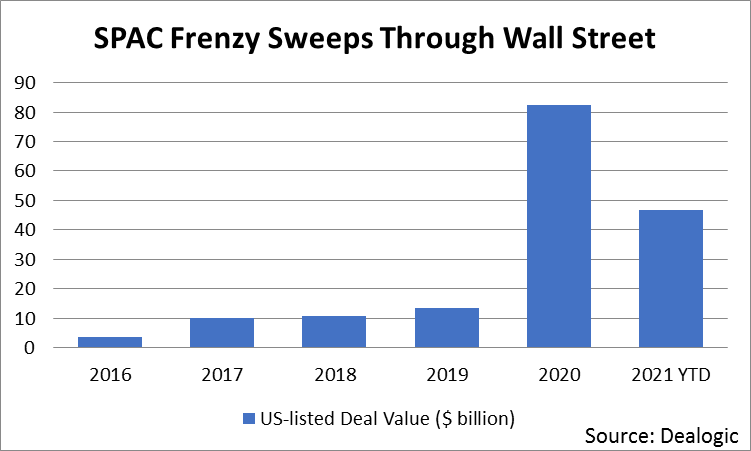

The stagnant cannabis stock market of 2019 became a thing of the past by the end of 2020. Throughout the course of last year, bag holders anxiously watched cannabis options creep back up. Now, nearly two years since market decline in 2019, the cannabis stock market is exploding with blank checks and buyout fever. Much of this expectant purchasing is due to Canadian companies considering U.S. market entrance. Combined with the recent surge in the use of special purpose acquisition companies (SPACs) to invest, this has led to an increase in asset prices.

A SPAC is defined as “a company with no commercial operations that is formed strictly to raise capital through an initial public offering (IPO) for the purpose of acquiring an existing company.” Though they have existed for decades, SPACs have become popular on Wall Street the last few years because they are a way for a company to go public without the associated headaches of preparing for a traditional IPO.

In a SPAC, investors interested in a specific industry pool their money together without knowledge of the company they’re starting. The SPAC then goes public as a shell company and begins acquiring other companies in the associated industry. Selling to a SPAC is usually an attractive option for owners of smaller companies built from private equity funds.

The U.S.-Canadian market questions that this rising practice asks are: Can Canadian companies enter a bigger market and be more successful? Is it advisable for U.S. companies to sell their assets to Canadian corporations whose records may be marred by a history of losses and a lack of proper corporate governance? Regardless — if both SPAC’s and Canadian bailout money is here, what comes next?

What is Driving this Bull Market?

Underpinning these movements are record cannabis sales internationally, making last year’s $15 billion dollars’ worth of sales in the U.S. look small in comparison. New markets have opened up in various states and countries throughout 2020, and that trend is only expected to continue. New demographics are opening up, especially among older age groups. This makes sense, as most cannabis sales — even in a recreational setting — are people treating something that ails them like insomnia or aches and pains.

Cannabis is set to take off, and we are entering only the second phase of its market expansion. The world is becoming competitive. Well-run companies that are profitable in key markets are prime targets for bigger, growing companies. At the same time, the world of SPACs will continue to drive valuations. Irrespective of buying assets, growing infrastructure is and will continue to be greatly needed.

The Elusive Profitability Factor

When Canada blew up, one of the biggest changes was companies began focusing the year on cost cutting and — most importantly — profitability. Profitability became the buzzword. But bigger companies are on the search for already-profitable enterprises, not just those that have the potential to be. However, profitability is currently still unobtainable in Canada. Reasonable forecasters should expect this year will show a few companies getting bailed out while many others will be forced to either merge for survival or declare bankruptcy.

An ideal company’s finances should highlight not only revenue growth, but also profitability. Attention should be focused on how well businesses are run, and not on how much money they have the potential to raise or spend. Over the years, there have been many prospective companies that spent hundreds of millions only to barely operate, and are now shells in litigation. Throwing money at any deal should have been a lesson learned in the past, but SPACs are tempting because they are trendily associated with new, interesting management styles and charismatic businesspeople.

Companies should be able to present perfect and clear financials along with maintenance logs for all equipment. In today’s day and age, books must be stellar and clean. As money pours into SPACs, asset valuations for all qualities of companies will rise. The focus instead becomes about asset plays, which will cause assets to continue rising as money is poured into SPACs.

Once upon a time, if number counters presented a negative review or had to dig too much, executives would turn a cold shoulder on investment. But in the age of SPACs, these standards of evaluation will be greatly undervalued. Aging equipment and reportability of every piece of equipment may or may not be properly serviced and recorded in a fast-moving market. Costs of repair or replacing equipment that isn’t properly maintained may be a problem of the past. Because when money comes fast, none care for the gritty details.

Issues for SPACs

Shortage of talent and training has become a big concern already in the era of SPACs. How many quality assets are out there? Big operators in the U.S. are content and don’t see Canada as an enticing market to enter. So, asset buys are likely to primarily be in the U.S. Large companies like Aphria may buy out some of the major American players, but most Canadian companies will use new funding rounds to pay down debts. Accordingly, they will then be forced to piece together smaller operators as a strategy.

A cannabis company’s personnel and office culture are very important when looking to integrate into a larger corporate culture. Remember, it’s not just the brick and mortar that is being invested into, it is also the people that run a facility. Maintaining employee retention when a deal occurs is always critical. Your personnel should be highly trained and professional if you want to exit. Easy to plug-in corporate structures make all the difference in immediately gaining from the sale or having to retool the shed and bring in all new people.

The rise of the SPAC-era and Canadian entry into the U.S. market will cause asset increases, but it is only the second chapter in the market expansion of cannabis. Proper buys will nail profitability, impeccable books, proper maintenance records and will have created an efficient corporate structure with talented personnel. The rest will be overpriced land buys that will require massive infrastructure spending. The basics of a well-run organization don’t change. The cannabis market is going to ROAR, but don’t worry if the SPACs pass you by- they are buying at the start of cannabis only.

Update: The House Judiciary Committee has passed the legalization bill, HB0209, by a 6-3 vote. After moving out of the Judiciary Committee, the bill now awaits a floor hearing, which is expected to come within the next week or two during the legislative session that ends on April 2.

A bipartisan group of lawmakers in Wyoming have introduced a bill to legalize cannabis in the state’s legislature. First reported by Buckrail.com, HB0209 was assigned on March 2. The bill would legalize possession, home grow and sales for adults, as well as establish a regulatory framework for licensing, tracking and taxation.

In November 2020, voters in Montana and South Dakota passed ballot measures that legalize adult use and sales of cannabis. About a month after Election Day, the University of Wyoming conducted a poll that found roughly 54% of Wyoming residents now support legal adult use cannabis. In 2018, UW found that 85% of Wyoming residents support medical cannabis legalization.

In March of 2019, Wyoming Governor Mark Gordon signed a bill into law that essentially legalized hemp in the state. That bill was a boon for the state’s agricultural economy, giving many farmers a much-needed boost in their crop diversity.

Wyoming Governor Mark Gordon

You can find the current version of HB0209 here. Sponsors of the bill include: Representatives Jared Olsen (R-Laramie), Mark Baker (R-Sweetwater) Eric Barlow (R-Campbell/Converse), Landon Brown (R-Laramie), Marshall Burt (L-Sweetwater), Cathy Connolly (D-Albany), Karlee Provenza (D-Albany), John Romero-Martinez (R-Laramie), Pat Sweeney (R-Natrona), Cyrus Western (R-Sheridan), Mike Yin (R-Teton) and Dan Zwonitzer (R-Laramie) and Senators Cale Case (R-Fremont) and Chris Rothfuss (D-Albany).

According to Buckrail, if the bill becomes law, Wyoming could get roughly $49.15 million in tax and license fee revenue in 2022. That number would mean a sizable windfall for the state that saw an 8.5% decline in tax revenue in 2020. Governor Gordon proposed budget cuts as high as 15% for agencies across the state last year. Most of the revenue generated from cannabis taxes would be earmarked for education.

As we’ve covered previously, the coronavirus pandemic has impacted the cannabis industry in the United States in a number of ways. Many states with legal medical and recreational cannabis markets have deemed those cannabis businesses essential, allowing them to remain open during statewide stay-at-home orders. Congress passed the Coronavirus Aid, Relief, and Economic Security Act (CARES Act) to help small businesses through the economic downturn, directing trillions of dollars to the Small Business Administration (SBA) to administer emergency loans, paycheck protection programs and other financial assistance to small businesses affected by the coronavirus pandemic.

CV Sciences received $2.9 million in federal aid from the SBA

However, pretty much all state-legal medical and recreational cannabis businesses are ineligible to receive money from the SBA because cannabis is designated as a Schedule 1 controlled substance. While Rep. Earl Blumenauer (D-OR) and Rep. Ed Perlmutter (D-CO) introduced legislation recently that would allow cannabis businesses to become eligible for federal assistance, it is unclear if that bill will become law. Furthermore, even if it does pass, cannabis businesses will likely receive little or no help at all, as a vast majority of the funds administered by the SBA have already been spoken for.

Enter the hemp and CBD products market. Thanks to the 2018 Farm Bill, which removed cannabis containing less than 0.3% THC from the list of controlled substances, hemp and CBD companies are not exempt from the SBA’s relief efforts.

According to VICE News, The Trump Administration has handed out millions of dollars to companies that sell CBD products. When VICE News looked into some SEC filings, they found more than $4 million in federal loans that have been granted to CBD products companies.

They found three CBD companies that scored big with federal assistance:

Despite state-legal medical and recreational cannabis businesses being left to fend for themselves, these large online CBD products retailers have received more than $4 million in federal aid money.

I was wrong. And that’s a good thing! Based on all available data, I assumed that evaporating ethanol from a cannabis oil/ethanol solution would result in terpene loss. As it turns out, it doesn’t. There are so many beliefs and assumptions about cannabis: Cannabis cures cancer!1 Smoking cannabis causes cancer!2 Sativas help you sleep; Indicas make you creative!3,4 CBD is not psychoactive!5 But are these ‘facts’ backed by science? Have they been experimentally tested and validated?

I postulated a theory, designed experiments to validate it and evaluated the results. Simply putting “cannabis backed by science” on your label does not solve the problem. Science is not a marketing term. It’s not even a fixed term. The practice of science is multifaceted and sometimes confusing. It evolved from the traditional model of Inductivism, where observations are used in an iterative process to refine a law/theory that can generalize such observations.6 Closely related is Empiricism, which posits that knowledge can only come from observation. Rationalism, on the other hand, believes that certain truths can be directly grasped by one’s intellect.7 In the last century, the definition of science was changed from the method by which we study something, such as Inductivism or Rationalism, and refocused on the way we explain phenomena. It states that a theory should be considered scientific if, and only if, it is falsifiable.8 All that means is that not the way we study something is what makes it scientific, but the way we explain it.

I wonder how can we use empirical observations and rational deliberations to solve the questions surrounding cannabis? And more importantly, how can we form scientific theories that are falsifiable? Cannabis, the plant, the drug, has long been withheld from society by its legal status. As a result, much of what we know, in fact, the entire industry has thrived in the shadows away from rigorous research. It’s time for this to change. I am particularly concerned by the lack of fundamental research in the field. I am not even talking about large questions, like the potential medical benefit of the plant and its constituents. Those are for later. I’m talking about fundamental, mundane questions like how many lumens per square centimetre does the plant need for optimal THC production? What are the kinetics of cannabis extraction in different solvents? What are the thermodynamics of decarboxylation? Where do major cannabinoids differ or align in terms of water solubility and viscosity?

The lack of knowledge and data in the cannabis field puts us in the precarious position of potentially chasing the wrong goals, not to mention wasting enormous amounts of time and money. Here’s a recent example drawn from personal experience:Certainly, I cannot be the only one who has made an incorrect assumption based on anecdotes and incomplete data?

Some of the most common steps in cannabis oil production involve ethanol solutions. Ethanol is commonly removed from extraction material under reduced pressure and elevated heat in a rotary evaporator. I expected that this process would endanger the terpenes in the oil – a key component of product quality. My theory was that volatile terpenes9 would be lost in the rotary evaporator during ethanol10 removal. The close values of vapor pressure for terpenes and ethanol make this a reasonably assumed possibility.11 In the summer of 2018, I finally got the chance to test it. I designed experiments at different temperatures and pressures, neat and in solution, to quantify the terpene lost in ethanol evaporation. I also considered real life conditions and limitations of cannabis oil manufacturers. After all the experiments were done, the results unequivocally showed that terpenes do not evaporate in a rotary evaporator when ethanol is removed from cannabis extracts.12 As it turns out, I was wrong.

We, as an industry, need to start putting money and effort into fundamental cannabis research programs. But, at least I ran the experiments! I postulated a theory, designed experiments to validate it and evaluated the results. At this point, and only this point, can I conclude anything about my hypothesis, even if that is that my working theory needs to be revised. Certainly, I cannot be the only one who has made an incorrect assumption based on anecdotes and incomplete data?

There is a particular danger when using incomplete data to form conclusions. There are many striking examples in the medical literature and even the casual observer might know them. The case of hormone replacement therapy for menopause and the associated risks of cardiovascular diseases showed how observational studies and well-designed clinical trials can lead to contradicting results.13 In the thirties of the last century, lobotomy became a cure-all technique for mental health issues.14 Dr. Moniz even won the Nobel Prize in Medicine for it.15 And it must come as no surprise when WIRED states “that one generation’s Nobel Prize-winning cure is another generation’s worst nightmare.”16 And with today’s knowledge is impossible to consider mercury as a treatment for syphilis, but that is exactly what it was used as for many centuries.17 All those examples, but the last one in particular should “be a good example of the weight of tradition or habit in the medical practice, […] of the necessity and the difficulties to evaluate the treatments without error.”18 There is the danger that we as cannabis professionals fall into the same trap and believe the old stories and become dogmatic about cannabis’ potential.

We, as an industry, need to start putting money and effort into fundamental cannabis research programs. That might be by sponsoring academic research,19 building in-house research divisions,20 or even building research networks.21 I fully believe in the need for fundamental cannabis research, even the non-sexy aspects.22 Therefore, I set up just that: an independent research laboratory, focused on fundamental cannabis research where we can test our assumptions and validate our theories. Although, I alone cannot do it all. I likely will be wrong somewhere (again). So, please join me in this effort. Let’s make sure cannabis science progresses.

References

No, it does not. There are preliminary in-situ studies that point at anti-cancer effects, but its more complicated. The therapeutic effects of Cannabis and cannabinoids: An update from the National Academies of Sciences, Engineering and Medicine report, Abrams, Donald I., European Journal of Internal Medicine, Volume 49, 7 – 11

No, it does not. National Academies of Sciences, Engineering, and Medicine. 2017. The Health Effects of Cannabis and Cannabinoids: The Current State of Evidence and Recommendations for Research. Washington, DC: The National Academies Press. https://doi.org/10.17226/24625.