Businesses often require outside capital to finance operating activities and to enable scaling and growth. Financing in the cannabis industry is notoriously challenging with regulatory obstacles at the local, state and federal levels. Recent market dynamics pose additional challenges for both financiers and cannabis operators.

We sat down with Matt Hawkins, Founder and Managing Partner of Entourage Effect Capital (EEC) to learn more about EEC and to get his perspective on recent market trends.

Aaron Green: In a nutshell, what is your investment/lending philosophy?

Matt Hawkins, Founder & Managing Partner at Entourage Effect Capital

Matt Hawkins: Entourage Effect Capital’s long history and experienced leadership allow us to access and construct high potential later-stage growth investments with sought-after industry leaders. We want to get ahead of what is happening on the regulatory and federal level to build scale with our investments.

Green: What types of companies are you primarily financing? What qualities do you look for in a cannabis industry operator or operating group?

Hawkins: Essentially, we are focused on investing in companies that will benefit the most when legalization occurs. We are currently working on multiple such deals, and separately, we are excited by how our newly minted, early-stage focused Arcview Ventures Seed Fund will provide a pipeline to the next generation of leading growth opportunities. When evaluating opportunities, we always look for the potential for scale and a strong management team.

Green: Capital market dynamics have led to significant public cannabis company revaluations in 2022. How has this affected your business?

Hawkins: As an industry, we all want companies to be valued for what they are worth, and right now, there are a lot of companies where that’s not the case due to the downturn in valuation. For us, it works the other way, because we are now able to invest at lower valuations with the hope of more upside when valuations reset.

Green: Debt on cannabis companies balance sheets have increased significantly in recent years. What is your perspective on that?

Hawkins: Debt is at its highest in industry. Operators don’t want to take equity capital at this point because valuations have come way down. However, we are lucky to have been in this business for a long time so that we can create our own deals. Our reputation precedes us — as a result, combined with the strength of our portfolio, people want us in their capital stack.

Green: How does the lack of institutional investor participation in the cannabis industry affect your business?

Hawkins: The lack of institutional capital in the industry makes it difficult for a large chunk of companies to grow and scale. For the industry to grow, there needs to be a different type of investor, investors who are not scared to go through the peaks and valleys we go through as an industry, whereas retail investors take their losses and move on. Everybody’s competing for the same small pool of money; managing cash is the most important factor for operators, whether private or public, big or small.

Green: What would you like to see in either state or federal legalization?

Hawkins: The illicit market still has a strong presence, and until we get regulatory reform, it’s going to continue. Reducing the tax burden on legalized markets would bring more revenue to both operators and the government because they’d reduce the market share of the illicit market, with the price offset trickling down to the retail customer.

Passing the SAFE Banking Act would create consequential changes for the cannabis industry. There is also a small chance that the New York Stock Exchange and the Nasdaq could start listing legal plant-touching businesses. If that happens, more institutional capital would enter the market and flush the industry with cash, with market caps going way up. There is a lot of unease and uncertainty with retail investors that prop up the stocks in the space, and it will continue until there is regulatory movement, even on the private side.

Green: What trends are you following closely as we head towards the end of 2022?

Hawkins: I don’t see anything happening unless the SAFE Banking Act passes. Otherwise, things are status quo, especially with public companies. For private companies, we’re going to see a lot more consolidation, especially in California.

Mergers and acquisition activity in the cannabis space tripled from 2020 to 2021, and that pace is on track to continue in 2022. With big players entering the global cannabis market, we’re fielding more questions about mergers and acquisitions of cannabis businesses.

In this guide, we look at the evolution of the U.S. cannabis industry and some best practices and considerations for M&A deals in this environment.

The New Reality of Cannabis M&A Activity

The industry has evolved since adult use cannabis was first legalized in some U.S. states in 2012. More cannabis companies have a professional infrastructure—legal, financial and operational—with executive teams and board members ensuring the organization establishes proper governance procedures. Investors and private equity firms are showing more interest, and some cannabis companies have celebrated their first IPOs on the Canadian Securities Exchange (CSE).

At the same time, we are seeing a kind of “market grab” by multistate operators (MSOs) looking to acquire various licenses and expand their market share. MSOs tend to understand the current state of the market. For example, in California and some other states, there is a surplus of cannabis on the market for various reasons, partially due to so-called “burner distribution”—rogue distributors using licenses to buy vast amounts of legally grown cannabis at wholesale prices and selling the product on the black market, thereby undercutting retailers and other legal cannabis businesses. Another reason for the surplus is simply the entrance of many legal cultivators into the market over the past year.

Due to these trends, MSOs are interested in acquiring the outlets to be able to sell the surplus cannabis within California and other new markets.

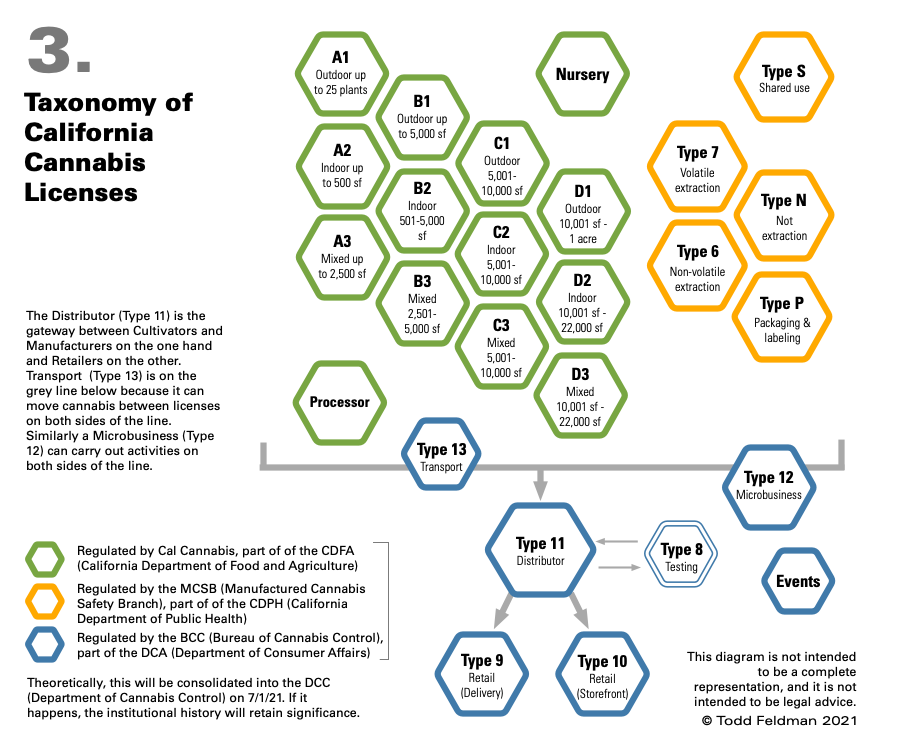

Transferring Cannabis License Rights

One of the biggest challenges to M&A activity in the cannabis sector is the difficulty of transferring or selling a cannabis license.

Different types of cannabis licenses in California

Cannabis licenses are not expressly transferable or assignable under California law and many other states. However, the parties involved aren’t without options. For example, a business that is sold to a new owner may be able to retain its existing cannabis license while the new owner’s license application is pending, as long as at least one existing owner is staying on board. At the state license level, a change of up to 20% financial interest does not constitute a change in ownership, although the Bureau of Cannabis Control (BCC) must be notified and approve the change.

This process can take a while—often a year or more—since licensing involves overcoming hurdles at the local level as well as the state level with the BCC. It’s crucial to talk with legal counsel about the particulars of the license and location early in the process to best structure the terms of the agreement while complying with state and local requirements.

Seeking a Tax-Free Reorganization in the Cannabis Space

In many cannabis mergers and acquisitions, the goal is to accomplish a tax-free reorganization, where the parties involved acquire or dispose of the assets of a business without generating the income tax consequences that would result from a straight sale or purchase of those assets.

IRC Section 368(a) defines various types of tax-free reorganizations, including:

In a stock-for-stock reorganization, all of the target company’s stock is traded for a portion of the stock of the acquiring parent corporation, and target company shareholders become minority shareholders of the acquiring company.

Often, it’s tough to meet the requirements to qualify for this type of tax-free reorganization because at least 80% of the target stock must be paid for in voting stock of the acquirer.

Additionally, companies may be saddled with too much debt. If the acquirer assumes that debt, it may be classified as consideration paid to the seller and therefore disqualify the transaction as a tax-free reorganization.

In other M&A deals, the acquiring corporation may be unwilling to assume the debt of the target corporation—perhaps because showing these items on its balance sheet would impact its debt-to-equity and other financial ratios.

Rather than acquiring the target company’s stock, the acquirer may purchase its assets. In a stock-for assets exchange, the buyer must purchase “substantially all” of the target’s assets in exchange for voting stock of the acquiring corporation.

A stock-for-assets format offers the buyer the benefit of not having to assume the unknown or contingent liabilities of the target. However, it’s only feasible if the acquirer purchases at least 80% of the fair market value of the target’s assets AND all or virtually all of the deal consideration will be stock of the acquirer.

Tax Consequences Arising from Sale of Assets

If the sale price doesn’t consist primarily of the buyer’s stock, the transaction may be a standard asset sale. This leads to very different tax results.

If the seller is a C corporation, it will typically face double taxation—paying tax once on the sale of assets within the corporation and again when those profits are distributed to shareholders. If the target company has net operating losses (NOLs), it can use those NOLs to offset the tax hit.

If the seller is an S corporation, it won’t have to pay corporate tax on the transaction at the federal level. Instead, shareholders will pay tax on the gain on their individual returns.

For the buyer, the benefit of an asset sale is that the assets acquired get a “step-up basis” to their purchase price. This is beneficial from a tax perspective, as the buyer can depreciate the assets and may be able to claim accelerated or bonus depreciation to help offset acquisition costs.

The subsidiary merges into the target company before liquidating,

The target company then becomes a subsidiary of the acquirer, and

The target company’s shareholders receive cash.

Structuring the deal this way may work to overcome the hurdle of transferring the license but may not qualify as a tax-free reorganization.

Bottom Line

The circumstances and motivations for mergers and acquisitions in the cannabis industry are diverse. As a result, there is no one-size-fits-all approach to structuring the transaction. In any event, it’s crucial to start the process early and seek advice from legal counsel and tax advisors to minimize the tax burden and ensure that both parties to the transaction get the best deal possible. If you need assistance, contact your 420CPA strategic financial advisor.

Village Farms International (NASDAQ: VFF) manages and operates greenhouse facilities in North America. They’ve worked with growers for over 30 years and started supporting cannabis growers in 2017. The company was founded by Michael A. DeGiglio and Albert W. Vanzeyst in 1987 and is headquartered in Delta, Canada. But is Village Farms stock a strong buy?

What is Village Farms International?

Village Farms International has a long history of managing and operating energy efficient grow facilities for agricultural crops. This includes cannabis, recently, and vegetables which bring in over $200 million in revenue annually.

Their 2021 acquisition of Pure SunFarms, one of Canada’s best known cannabis brands, gave them around $17 million in extra revenue and a large opportunity in the flower competition in Canada. Current goals have them taking 20% of the flower market share. They also deal in vapes, oils and infused edibles.

Bottom Line: Is Village Farms Stock a Strong Buy?

Village Farms stock shows plenty of promise. They have a large footprint in Texas as well, supporting hemp cultivation and processing into CBD products for distribution in the USA. With a small stake in Altum International, they also have a presence in Asia.

Excitingly, their subsidiary Balanced Health Botanicals, has come out with their Synergy Collections of SKUs (cannabinoids such as CBDA, CBG, and CBG with non-hallucinogenic mushrooms and Kava roots). These products will come as tinctures, capsules and drinks (around 31 SKUs pending) and should diversify their product offerings even more.

Their revenue remains strong, with adjusted EBITDA up 49% YoY and Pure SunFarms reporting 12 straight quarters of positive adjusted EBITDA. They have a lot of cash and are paying off their debt and recent acquisition costs quickly. With really low P/S, Price/Book and EV/Revenue ratios (all under 4) we see a bargain price now for a company that should slowly grow for the next six quarters.

Village Farms stock presents a longer buy and hold opportunity but the recent price drop (37% in 1 year?!) is making much more of an enticing deal now.

For all these reasons we rate VFF as Strong.

83% of Cannin’s fundamentals prove true within 30 days or less on 100+ recommendations over the past 3 years.

On October 14, Canopy Growth announced their plans to acquire Wana Brands, the number one cannabis edibles brand based on market share in North America. The two companies entered into an agreement that gives Canopy the right to acquire 100% of the membership interests of Wana Brands (a call option to acquire 100% of each Wana entity) once a “triggering event,” such as when plant-touching companies begin trading on major US stock exchanges or full federal legalization, occurs.

As part of the agreement, Canopy Growth makes an upfront payment of $297.5 million to Wana Brands. Until the United States moves on cannabis legalization or companies can start trading on U.S. exchanges and Canopy uses the call option to acquire Wana Brands, they don’t get any voting or economic interest in Wana Brands. The two companies are essentially operating completely independently of each other until the US legalizes cannabis.

Nancy Whiteman co-founded Wana Brands in 2010 and since then the company has expanded significantly. Following the legalization of adult-use cannabis in Colorado, their sales skyrocketed. Over the next few years, Whiteman oversaw the company’s expansion into a number of new states. In 2016, they moved into Oregon’s market and quickly grew their brand presence, seemingly overnight. Then they expanded into Nevada, Arizona and Illinois in 2017. After that the company made a major East Coast push, expanding into Maryland, Florida and Massachusetts, with other major northeast markets expected to be added soon. The brand now has products available in twelve US states and nine Canadian provinces, with plans to add four additional states by the end of the year.

Nancy Whiteman, CEO & Co-Founder of Wana Brands

Shortly after the announcement, we sat down together over coffee in Las Vegas to discuss Whiteman’s journey to success, her plans for the company’s expansion and what the future might hold for Wana Brands.

Aaron G. Biros: First of all, congratulations on the acquisition. As a co-founder and CEO, it must be amazing to see the success of your company and all you’ve accomplished. How do you feel?

Nancy Whiteman: I feel ecstatic. I am so excited and so proud of what Wana has accomplished. Just all around a great feeling.

Biros: What was it like leading up to this moment? From the inception of the business, did you ever have any doubts you’d make it this far?

Whiteman: A thousand times. Absolutely. Anyone in cannabis that tells you they didn’t have any doubts is probably not being very honest. I had been thinking about partnership for a while. I felt the timing was right because of a variety of reasons, but also the possibility of federal legalization. I wanted to make sure that Wana was really going to be well positioned for future growth. One of the things that I said in our employee meeting – I quoted the old proverb of ‘If you want to go fast, go alone, but if you want to go far, go together.’ We’ve been going it alone for eleven years and we’ve gone very fast. But I want Wana to continue to be a major player in the industry and to go far. I really felt that this was the time in the industry to strike a partnership.

So that’s a little bit of the thinking behind it. I think when there is federal legalization, there is going to be a host of competitors entering the industry that are going to be unlike anything we’ve faced before. I think it’s going to be challenging for independent brands to scale as rapidly as they’re going to need to scale to compete against all of this new competition on their own. So that’s the why behind the timing of it.

In terms of why Canopy, I’ve known Canopy for quite a while. I met them when we were looking for partners about three and a half years ago. We did not end up putting together a deal at that point in time, but I did get to know the company quite a bit. Since then that company has changed significantly with leadership changes and became a very different company with the Constellation Brands investment behind them.

When I think about the future of the industry and particularly post-legalization, I have certain things that I am looking for in partners. Of course, I am looking for financial strength in a partner. I was really looking for a company that has a very long-term perspective on the industry, with both the proper resources and the proper mindset to make long-term investments for the future. And then my belief is that post-legalization, we’re going to see radical changes in the industry including where products are cultivated in a global market, more distribution outside of dispensaries – and I think liquor stores could be a likely form of distribution at some point in time, so the relationship with Constellation was very interesting and appealing to me. But all of those things wouldn’t mean as much to me if I didn’t feel we didn’t have a good fit in terms of our shared values and how we saw the industry. We spent a lot of time talking about that and I think one of the aspects that really attracted me to Canopy was that we are very aligned on how we see the future of the industry shaping up. Certainly, I think there is a wonderfully viable position for cannabis as an alcohol replacement, however we also have a lot of focus on innovation and the health and wellness aspects of cannabis. I was really looking for a partner that felt the same, and it ended up that we really were aligned on those values.

Biros: What does it look like going forward? Since you’re staying on board, how will your new role change?

Whiteman: My new role doesn’t change at all actually. I woke up last Monday—the week after the big announcement–and it felt very normal getting back to work and having my usual meetings. This was my fifteen minutes of fame and thankfully its diminishing so now it’s just back to work as usual.

But moving forward, we have big plans. Wana is launching in four new markets over the next couple of months, we’re in discussions to launch in an additional six markets, and we have very robust innovation pipeline. So, we’re just really busy right now just executing on our strategy. I am looking forward to getting to know our new colleagues at Canopy better and exploring different collaboration possibilities.

I feel very optimistic. I was thrilled our employees were delighted with the news and morale is very high. The feedback from the rest of the industry has been really positive and overall, I am feeling very good about this decision.

Biros: So you mentioned some expansion plans for four new markets in the next few months. How does the acquisition help Wana Brands expand?

Whiteman: You know we haven’t announced the new states so I can’t speak to those publicly yet. They were all in the works before this deal and are currently in the process of being onboarded. Where it will get interesting is how this deal impacts new states that we move into. Until Canopy decides to exercise the call option [to acquire 100% of membership interests in each Wana entity], we are still an independently owned and run company. So we are still going to be looking for the best partners that we can find in new markets, and the Canopy connection will certainly be helpful to us. But to your point about the plans, we’ll be announcing those new market expansions in the coming weeks.

Biros: As a woman leader with an extremely significant position in the cannabis industry, do you have any advice for young aspiring entrepreneurs, women leaders or other women in the cannabis space?

Whiteman: I do. I posted something on LinkedIn the other day and I’m going to make the same comment to you as I made in that post because I think it’s important and particularly important for young women. People have said a lot of nice things about me in the past couple of weeks and of course everybody loves to hear nice things about themselves. But the truth is, some of them are not true. And one of them that is definitely not true is that I am somehow fearless. And I guess what I would say to women and young entrepreneurs is that fearlessness is a myth.

Being an entrepreneur is hard. You’re putting your money on the line, you’re putting your time on the line, you’re putting your reputation, you’re potentially putting your family’s, your friends’ and your investors’ money on the line. Who would not be afraid against that backdrop? We all have times of feeling fearful, of feeling anxious, of having sleepless nights. So, what I would say is don’t aspire to be fearless. There are other aspirations that are much more useful. For example, aspire to be resilient, aspire to be persistent, aspire to be of service to other people, aspire to be very true to your values and your strategy. Don’t let this mythology of what a “leader” is supposed to look like make you feel bad about your emotions. It’s not about having those emotions, it’s what you do with them.

That’s what I would say to young entrepreneurs and especially to women. Because I do believe that women hold themselves to a very high standard a lot of the time and have a lot of misconceptions of what they’re supposed to be living up to when it comes to leadership.

Biros: What an incredible perspective to have. Okay, one last question for you: what are you doing to celebrate?

Whiteman: So far, I’ve been too busy to celebrate! This just happened so recently. I would like to take a great trip with my kids. I don’t really know I have not had time to figure that out. People tell me I need to go to Disney. But right now, it’s still taking a little while to let it all sink in.

Biros: Wonderful! And Nancy, thank you so much for your time I really appreciate it.

Whiteman: And thank you! So nice to see you in person.

As an experiential marketer that works with a lot of vice-oriented brands, I’ve always been fascinated by the story of the rise of spirits in the US – a history marked by ingenuity in the face of heavy restrictions, clashing social norms, crime and political ideals. Since then, those same qualities have emerged in the story of cannabis and how, against all odds, it has recently begun to push its way into the mainstream. But on the path to legalization, cannabis can also learn a lot from the spirits industry about what not to do.

For example, when laws governing the spirits industry were written in the post-Prohibition 1930s, the federal government wanted to create an equitable landscape. So, they created a 3-tier system – manufacturers or importers must sell to wholesalers, wholesalers must then sell to retailers and retailers sell to us. They figured that keeping manufacturing interests separate from wholesale and retail interests would keep any large company from owning an entire supply chain, muscling out smaller competitors.

In theory, it’s not a bad idea. Imagine the consequences of massive companies like Diageo or AB InBev using their money to pay bars and liquor stores to only stock their brands and not competitors. Add on the Tied House Laws, which basically says an entity in one of the three categories cannot have an ownership stake in any of the others, and you get a seemingly even-handed marketplace.

Tied House Laws theoretically limit one entity from monopolizing a supply chain

In truth, it makes it almost impossible to be disruptive or for new brands to break through. Other industries have innovated by cutting out the middleman and selling direct-to-consumer – something that simply cannot happen in alcohol (minus the wineries and distilleries that can sell direct out of their tasting rooms). Also, now distributors are so consolidated that there are only one or two big distribution companies in each state. So, as a company trying to bring a new product to market, you have to get into one of these highly selective and competitive distributors if you are going to be successful – a challenging ask for a small, independent brand.

Protection racket

Now, imagine that same challenge coming to the cannabis space. With legalization around the corner, the adult use (as opposed to medical use) cannabis industry could easily look like alcohol in the rules that will be set up.

The demand for high quality cannabis continues to increase, but the prices need to level out to stave off the black market.

Right now, adult use manufacturers can sell their products to dispensaries directly. Some use a distributor, but there is no nationwide mandate to – which is probably for the best. If a distributor isn’t a requirement, it forces brands to offer something new to differentiate themselves. It will spark innovation, rather than add an extra profit margin that will get rolled into the final price – a price that is already higher than it should be due to the murky federal legal status. Adding complexity and cost will only make it harder to compete with the illicit market. For the industry to grow, costs for illicit cannabis can’t be lower than its legal counterpart.

Of course, we are in the nascent stages of legalization here and we’ve come a long way culturally and technologically since the 30s. But remember, the rules governing alcohol were written nearly 100 years ago along with the passage of the 21st amendment repealing prohibition. Startlingly, those laws haven’t changed that much since they were written, so any mistakes made now in dealing with the cannabis industry could last for a long time.

A new way forward

What the cannabis industry needs is a new model for the adult use/recreational space, keeping some of what exists in the alcohol industry but without ever mandating use of a distributor – the middle tier. This would mean keeping Tied House Laws in place and applying them to cannabis so that a manufacturer could never hold an interest in a retailer, while still allowing them to sell directly to dispensaries and to consumers. Currently, some states allow for vertical integration, which would change under Tied House Laws.

This should be pretty simple, since most states are already separating licenses by type of activity (manufacturer, retailer, etc.) and it would promote competition while bringing the widest array of products possible to each consumer. Also, it would prevent any behemoths from squeezing out the up and comers.

Constant innovation is a hallmark of the cannabis market and a key factor in continuous growth.

Of course, some retail license allowances could be considered on a case-by-case basis. For example, I would carve out an exception that growers/manufacturers could sell direct to consumers through a single “tasting room” at their brand home. This is similar to the operations of microbreweries, distilleries and wineries. It would encourage education for consumers, and provide great opportunities for brands to show why their products are better or unique.

Given the technology and logistics solutions available to businesses in a 21st century economy, mandated distributors create a sometimes-unnecessary barrier to an already efficient supply chain. If mandated, prices will inflate to cover added margin, thus making it harder to bring consumers over from the legacy market to the legal one. I’m not against the idea of a distributor – they can add tremendous value, but the mandate would seriously curtail industry growth.

Direct-to-retail and direct-to-consumer sales are necessary for the economic health and growth of the industry. Without this, using alcohol as a cautionary tale, at some point the middle tier cannabis brands will inevitably begin to wield an outsized amount of power. We are living at a time where innovation is going to be the key to explosive growth in the cannabis industry, so it’s important to do everything possible to let the market find its way without falling into a century-old trap.

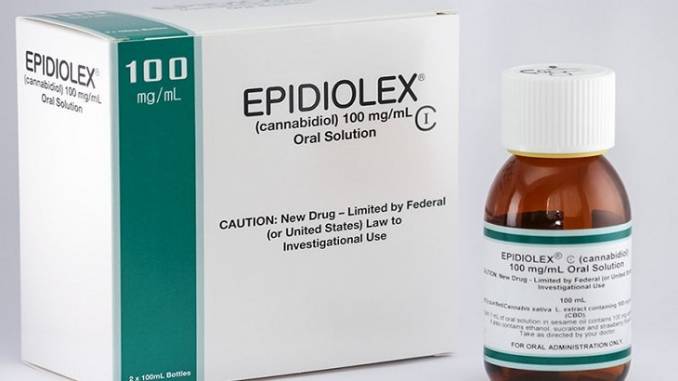

Last week, GW Pharmaceuticals (Nasdaq: GWPH) announced they have entered into an agreement with Jazz Pharmaceuticals (Nasdaq: JAZZ) for Jazz to acquire GW Pharma. Both boards of directors for the two companies have approved the deal and they expect the acquisition to close in the second quarter of 2021.

GW Pharma is well-known in the cannabis industry as producing the first and only FDA-approved drug containing CBD, Epidiolex. Epidiolex is approved for the treatment of seizures in rare diseases like severe forms of epilepsy. GW is also currently in phase 3 trials seeking FDA approval for a similar drug, Nabiximols, that treats spasms from conditions like multiple sclerosis and spinal cord injuries.

Jazz Pharmaceuticals is a biopharmaceutical company based in Ireland that is known for its drug Xyrem, which is approved by the FDA to treat narcolepsy.

Bruce Cozadd, chairman and CEO of Jazz, says the acquisition will bring together two companies that have a track record of developing “differentiated therapies,” adding to their portfolio of sleep medicine and their growing oncology business. “We are excited to add GW’s industry-leading cannabinoid platform, innovative pipeline and products, which will strengthen and broaden our neuroscience portfolio, further diversify our revenue and drive sustainable, long-term value creation opportunities,” says Cozadd.

Justin Gover, CEO of GW Pharma, says the two companies share a vision for developing and commercializing innovative medicines, with a focus on neuroscience. “Over the last two decades, GW has built an unparalleled global leadership position in cannabinoid science, including the successful launch of Epidiolex, a breakthrough product within the field of epilepsy, and a diverse and robust neuroscience pipeline,” says Gover. “We believe that Jazz is an ideal growth partner that is committed to supporting our commercial efforts, as well as ongoing clinical and research programs.”

Editor’s Note: This is an excerpt from chapter ten of From Seed to Success: How to Launch a Great Cannabis Cultivation Business in Record Time by Ryan Douglas. Douglas is founder of Ryan Douglas Cultivation, a cannabis cultivation consulting firm. He was Master Grower from 2013-2016 for Tweed, Inc., Canada’s largest licensed producer of medical cannabis and the flagship subsidiary of Canopy Growth Corporation.

Cultivation businesses should consider specializing in just one stage of the cannabis cultivation process. The industry has focused heavily on vertical integration, and some regulating bodies require licensees to control the entire cannabis value chain from cultivation and processing to retail. This requirement is not always in the best interest of the consumer or the business, and will likely change as the industry evolves. Not only will companies specialize in each step of the value chain, but we’ll see even further segmentation among growers that choose to focus on just one step of the cultivation process. Cannabis businesses that want to position themselves for future success should identify their strengths in the crop production process and consider specializing in just one part.

Ryan Douglas, former Master Grower for Tweed and author of From Seed to Success: How to Launch a Great Cannabis Cultivation Business in Record Time

Elsewhere in commercial horticulture, specialization is the norm. It is unlikely that the begonias you bought at your local garden shop spent their entire life inside that greenhouse. More likely, the plant spent time hopping between specialists in the production chain before landing on the retail shelf. One grower typically handles stock plant production and serves as a rooting station for vegetative cuttings. From there, rooted cuttings are shipped to a grower that cares for the plants during the vegetative stage. Once they’re an appropriate height for flowering, they’re shipped to the last grower to flower out and sell to retailers.

Cannabis businesses should consider imitating this model as a way to ensure competitiveness in the future. In the US, federal law does not yet allow for the interstate transport of plants containing THC, but the process can be segmented within states where vertical integration is not a requirement. As we look ahead to full federal legalization in the US, we should anticipate companies abandoning the vertical integration model in favor of specialization. In countries where cannabis cultivation is federally legal, entrepreneurs should consider specialization from the moment they begin planning their business.

Cultivators that specialize in breeding and genetics could sell seeds, rooted cuttings, and tissue culture services to commercial growers. Royalties could provide a recurring source of income after the initial sale of seeds or young plants. Contracting propagation activities to a specialist can result in consistently clean rooted cuttings that arrive certified disease-free at roughly ¼ the cost of producing them in-house. This not only frees up space at the recipient’s greenhouse and saves them money, but it eliminates the risks inherent in traditional mother plant and cloning processes. If a mother plant becomes infected, all future generations will exhibit that disease, and the time, money, energy, labor, and space required to maintain healthy stock plants is substantial. Growers that focus on large scale cultivation would do well to outsource this critical step.

From Seed to Success: How to Launch a Great Cannabis Cultivation Business in Record Time

Intermediary growers could specialize in growing out seeds and rooted cuttings into mature plants that are ready to flower. These growers would develop this starter material into healthy plants with a strong, vigorous root system. They would also treat the plants with beneficial insects and inoculate the crop with various biological agents to decrease the plant’s susceptibility to pest and disease infestations. Plants would stay with this grower until they are about six to 18 inches in height—the appropriate size to initiate flowering.

The final stage in the process would be the flower grower. Monetarily, this is the most valuable stage in the cultivation process, but it’s also the most expensive. This facility would have the proper lighting, plant support infrastructure, and environmental controls to ensure that critical grow parameters can be tightly maintained throughout the flowering cycle. The grower would be an expert in managing late-stage insect and disease outbreaks, and they would be cautious not to apply anything to the flower that would later show up on a certificate of analysis (COA), rendering the crop unsaleable. This last stage would also handle all harvest and post-harvest activities—since shipping a finished crop to another location is inefficient and could potentially damage the plants.

As the cannabis cultivation industry normalizes, so, too, will the process by which the product is produced. Entrepreneurs keen on carving out a future in the industry should focus on one stage of the cultivation process, and excel at it.

On December 16, 2020, Aphria Inc. (TSX: APHA and Nasdaq: APHA) announced a merger with Tilray, Inc. (Nasdaq: TLRY), creating the world’s largest cannabis company. The two Canadian companies combined have an equity value of $3.9 billion.

Following the news of the merger, Tilray’s stock rose more than 21% the same day. Once the reverse-merger is finalized, Aphria shareholders will own 62% of the outstanding Tilray shares. That is a premium of 23% based on share price at market close on the 15th. Based on the past twelve months of reports, the two companies’ revenue totals more than $685 million.

Both of the companies have had international expansion strategies in place well beyond the Canadian market, with an eye focused on the European and United States markets. In Germany, Aphria already has a well-established footprint for distribution and Tilray owns a production facility in Portugal.

About two weeks ago, Aphria closed on their $300 million acquisition of Sweetwater Brewing Company, one of the largest independent craft brewers in the United States. Sweetwater is well known for their 420 Extra Pale Ale, their cannabis-curious lifestyle brands and their music festivals.

Once the Aphria/Tilray merger is finalized, the company will have offices in New York, Seattle, Toronto, Leamington, Vancouver Island, Portugal and in Germany. The new combined company will do business under the Tilray name with shares trading on NASDAQ under ticker symbol “TLRY”.

Aphria’s current chairman and CEO, Irwin Simon, will be the chairman and CEO of the combined company, Tilray. “We are bringing together two world-class companies that share a culture of innovation, brand development and cultivation to enhance our Canadian, U.S., and international scale as we pursue opportunities for accelerated growth with the strength and flexibility of our balance sheet and access to capital,” says Simon. “Our highly complementary businesses create a combined company with a leading branded product portfolio, including the most comprehensive Cannabis 2.0 product offerings for patients and consumers, along with significant synergies across our operations in Canada, Europe and the United States. Our business combination with Tilray aligns with our strategic focus and emphasis on our highest return priorities as we strive to generate value for all stakeholders.”

Here is the headliner: As of the second week in January, there will be a cannabis related exchange-traded fund (ETF), trading on the Frankfurt Stock Exchange (or Deutsche Börse), the third largest stock exchange in the world and the meeting point between equities and the vast majority of institutional investment globally.

The Medical Cannabis and Wellness UCITS ETF (CBSX G) will trade on Deutsche Börse’s Xetra.

London-based ETF provider HANetf is the creator of the fund.

The idea is to create a fund with targeted exposure to the European market. And as a result, it is bound to be interesting. Especially as the companies included must go through a due diligence process that will only include equities traded on stock exchanges like the NYSE, Nasdaq and TSX.

This of course is no guarantee, particularly given the scandals of the major Canadians last year (who are listed on all or an assortment of the above).

Indeed, in the eyes of German authorities, this is not necessarily all that significant. And that in and of itself is a watchword of caution here. Namely the Deutsche Börse put the entire North American cannabis equity market under special watch two years ago and that has not changed since then. That said, with legalization now clearly in Europe, things in general look a lot different on the ground.

What will be really intriguing is when the fund (or the ones inevitably to follow) that look at the discussion from a European market perspective.

Purpose Investments, the Canadian partner involved, has over CA $8 billion in assets under management as of last month and across a range of ETFs.

Solactive, the German company which independently calculates the index, may also be unknown to North Americans in particular. In Germany, particularly Frankfurt, they have developed, since their founding in 2007, a reputation for being not only quirky, but not risk averse. In other words, decidedly “non-German,” at least by stereotype. And cannabis right now, particularly with this approach, is an inevitable development. This could, in fact, do very well. The problem, however, that is still in the room is the vastly different levels of compliance – but that too is a risk calculation that is to the people at the table, no different than certain kinds of commodities.

That alone makes this ETF intriguing simply because it will indeed be evaluated by German eyes – if not processes.

Significance

Things are clearly normalizing on both the accounting and reform front. The growth of the regulated Canadian market and the increasing focus on regulation of all kinds is only going to make things less risky for investors.

Bottom line: Good development, but won’t be the last. By far.Further, there are not many public European companies, yet. That may also change. However, for the moment, they are still a trickle (and all over the map).

What is intriguing is the timing of the fund. If not what it potentially spells for the public markets. And further the obvious research the Auslander team have done in finding the right European-based partner. Look for interesting things indeed.

This is the first real foray into Europe by anything outside a single stock offering on a European equity market.

For Germans, in particular, who are extremely risk averse, and tend to invest in other kinds of securities if not insurance to build up their pensions, the equity markets sniff a bit too much for most of “North American scam.” Far from cannabis. Yet some Germans do invest in the markets. As do other Europeans.

Bottom line: Good development, but won’t be the last. By far.

The beleaguered CannTrust has been given a way out of the perilous mess that executive management created for the company – but such a salvation comes at a high cost. That said, the company was already in deep water with regulators and clients. Health Canada, in fact, cancelled the company’s license to produce and sell cannabis in September – essentially mandating mass returns two months after a whistleblower instigated what is probably the legal industry’s most egregious scandal to date.

Efforts to regain regulatory approval also include plans by the company to recover cannabis that was not authorized by its license, and improve inventory tracking – the full details of which will be delivered to Health Canada by October 21.

While the beleaguered pot company’s stock predictably surged again on the public markets, the question lingers: can CannTrust ever be trusted again? These were egregious violations.

A Changing Industry

As with most things in business, the issues plaguing CannTrust were not isolated to one company. This has ranged in the past from pesticide use to creative accounting. Not to mention all sorts of creative endeavors on the financial side that are, depending on which stock market you look at this from, less than legit or just this side of shady.

It was easy to throw the book at a company like this – not only for these specific violations, but also as a warning to others tempted to engage in similar tactics (or fail to clean those up that still exist).

CannTrust in other words, was a clarion bell about the change in the weather, driven not only by international treaties but the legitimization of the drug, on the ground. Globally. When large health insurers get involved (see Europe), the conversation begins to change. And it is, fairly drastically.

On the ground in Germany, there are two more cultivation sites underway with one now certified and functional. BfArM (the German equivalent of the FDA) is now on the front lines of a battle that so far, at least in Canada, has not been addressed at a level Europe requires. That said, this reality too is changing. One of the largest distributors in Germany, CC Pharma, now owned by Aphria, has started a supply chain compliance check that is overdue. And further, while focussed on the cannabis industry, in truth, is a problem that plagues pharma far from cannabinoids.

However, as this is the cannabis industry, the scandals that rip through headlines are that much more visceral.

Seed to sale traceability, and further in a model unseen in the industry so far, will also become a watchword that is still rippling through an international industry chafing at any sort of standards, let alone standardization required for pharmaceutical acceptance. The bar, in other words, has just been set much higher. And there are many who will not make the grade.

CannTrust, certainly, was a victim not only of internal mismanagement, but a shifting environment that is rapidly upgrading on a level not seen so far in the entire North American industry – with a few notable exceptions.

Pharmaceutical Grade Is The Standard To Beat

Here is the reality now facing an industry coming into its own and on an international basis. The standards are tightening. The rules are not only being written but being enforced. And while there are sure to be a few more scandals along the way, the kinds of basic problems found at CannTrust are probably, finally, going extinct in the part of the industry that now knows it is being held accountable to far higher standards.

The reason? Medical grade and national food standards are in the room for every exporter now eyeing Europe. And that alone is resetting the debate everywhere. No matter how treacherous the path may be.

So no matter how harsh the penalties are now facing one company, even the regulators know that this is shifting territory. CannTrust, after all, is being given a second chance.

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

We use tracking pixels that set your arrival time at our website, this is used as part of our anti-spam and security measures. Disabling this tracking pixel would disable some of our security measures, and is therefore considered necessary for the safe operation of the website. This tracking pixel is cleared from your system when you delete files in your history.

We also use cookies to store your preferences regarding the setting of 3rd Party Cookies.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.

Green: How does the lack of institutional investor participation in the cannabis industry affect your business?

Green: How does the lack of institutional investor participation in the cannabis industry affect your business?