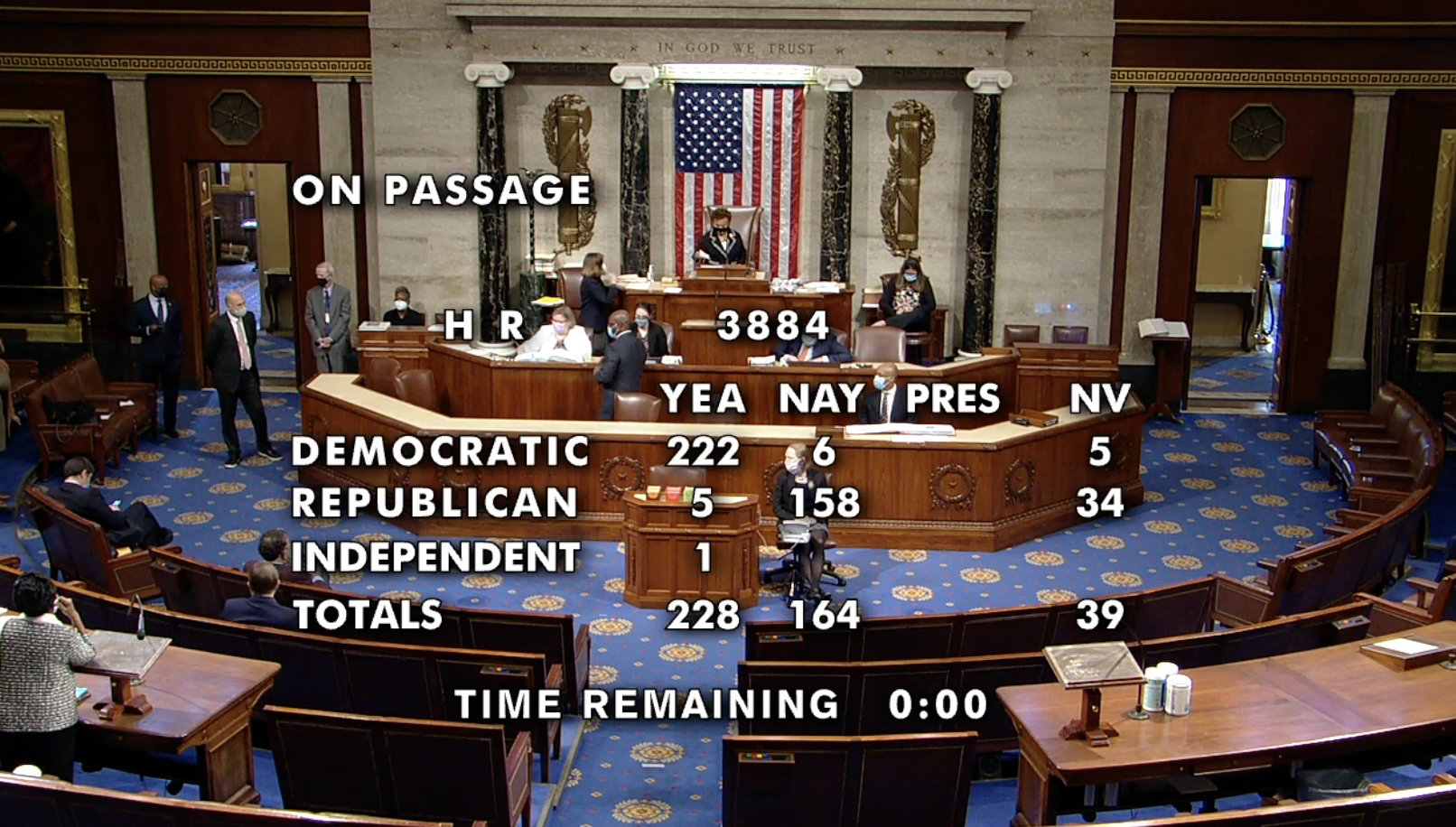

Late last month, Mastercard decided to halt their debit card transactions with cannabis dispensaries, notifying financial institutions and payment processors to stop processing purchases. This isn’t the first digital payment solution to swiftly exit the industry – late last year, vendors turned off services to their cashless ATMs. These abrupt decisions have made major headlines, shocking cannabis dispensary owners, operators and consumers as they scramble to shift focus back to the remaining legal payment tools.

For the cannabis industry veterans like myself, these exits aren’t a surprise at all. Why? Cannabis is federally illegal and federal regulations restrict banks and other financial services companies from working with cannabis businesses – even if it is legal at a state level. Due to this massive legal hurdle, cannabis dispensaries often lack access to typical banking services and have limited payment options for consumers, making it challenging to manage and facilitate payments.

Some believe that this decision by Mastercard, the second largest payments provider in the world, and by other payment vendors, coupled with the political pressure to legalize cannabis could help push legalization or the Secure and Fair Enforcement (SAFE) Banking Act to help mitigate the lack of access to banking services in the longer term. Even though cannabis represents an economic opportunity – MJBizDailyestimates that combined medical and adult use cannabis sales could reach $33.6 billion by the end of 2023, and $53.5 billion by 2027 – hurdles to legalization mean that, for now, cash will be the most prevalent payments option.

Let’s Talk About Cash

Physical cash is difficult to manage for dispensaries

Cash remains the longstanding and most prevalent payment option in cannabis. However, it presents difficulties for businesses. Physical cash is difficult to manage for dispensaries for several reasons, primarily due to the costs to count, track and manage cash volumes and the labor required to count the cash. In fact, in most dispensaries, associates count cash an average of six times a day. Each time cash is manually counted, dispensaries risk miscounts, shrinkage, security and safety concerns due to robberies.

This manual labor required to oversee a business’s balance sheet and keep dispensaries operating is inefficient and unsustainable, and many have attempted to incorporate debit payments or cashless ATM transactions to help mitigate the costs associated with cash. However, while cash presents logistical and operational challenges for dispensary owners, it remains one of the more dependable payment options consumers and dispensaries have for cannabis transactions. Dispensaries can integrate simple strategies to improve their cash handling and operate more efficiently.

Best practices with cash management for dispensaries

The biggest and most impactful strategy is incorporating cash automation tools to help secure, count and manage their payments. The largest and oldest dispensary in Washington D.C. incorporated sophisticated automation tools into their cash handling practices, which have alleviated massive headaches and burdens from store associates, managers and its accounting team, who previously relied on manual cash processes to count, sort and manage their cash.

Mastercard halted debit card transactions with cannabis dispensaries just weeks ago

This cash-handling technology has improved count accuracy, saved time for staff, improved visibility and enabled real-time reporting. These tools have transformed the day-to-day duties of staff. The dispensary’s accounting team and associates no longer get overwhelmed when anticipating increased cash flow on 4/20 or other holidays because they have tools that eliminate the extreme costs of handling cash. Additionally, they now confidently support audits as they have complete reports of each transaction by user, date and time. Before automation, audits were next to impossible to execute confidently.

The greatest benefit of cash automation tools is the near elimination of shrinkage, a term referring to the cash lost due to employee theft or miscounts. With cash automation, cash is as affordable as digital payment options, with the added confidence that cash won’t disappear as a payment option for consumers.

Have a Cash Strategy

While Mastercard’s decision to leave the cannabis industry leaves dispensaries in the lurch, the cannabis payments ecosystem continues to evolve and transition quickly. Dispensaries must be agile and incorporate strategies for the payment options, both inbound from consumers and outbound to their vendors, that they can rely on.

As the cannabis industry continues to evolve, embracing cash automation will be crucial for sustainable growth and success. Cash automation is a transformative solution for cannabis reducing the cost of managing cash while addressing the unique challenges associated with high cash volume operations. Embracing cash automation allows dispensaries to thrive in an evolving industry while maintaining control over their cash ecosystem, no matter who enters or exits the payments space.

By Tamara L. Kolb, Amy Bean, Caitlin Strelioff No Comments

As the legal cannabis market expands, banks and nonbank financial institutions (NBFIs) across the United States continue to explore how to safely provide banking and other financial services to cannabis-related businesses (CRBs) and other CRB ecosystem players. At the same time, these organizations are taking into account changes they might need to consider relative to their Bank Secrecy Act ( BSA), anti-money laundering (AML) and related compliance programs.

Regulatory conundrum

The Controlled Substances Act (CSA) identifies the cannabis plant and all its derivatives as a Schedule 1 controlled substance. Schedule 1 controlled substances have a “high abuse potential with no accepted medical use,” and they cannot be “prescribed, dispensed, or administered.” Because cannabis remains classified as a Schedule 1 controlled substance, the CSA “imposes strict controls on possession, manufacturing, distribution, and dispensing” of cannabis.

Under the Money Laundering Control Act of 1986 (MLCA) and the BSA as amended, covered banks and NBFIs are prohibited from providing financial services to businesses that are engaged in illicit activities. Because federal law prohibits the distribution and sale of cannabis, financial transactions involving CRBs are therefore deemed to be transactions that involve funds derived from illegal activities.

As of Feb. 3, 2022, 18 states, two territories, and the District of Columbia have enacted legislation to regulate cannabis for adult use. Thirty-seven states, the District of Columbia and four territories have approved comprehensive, publicly available medical and cannabis programs. Eleven states allow for the use of low-THC, high-CBD substances for medical reasons in limited situations or as a legal defense.

The growing divide between federal prohibition and state legalization of the cannabis industry creates a precarious position for federally regulated banks and NBFIs with the main concern involving exposure to legal, operational and regulatory risk. The situation begs the question: How might the federal government and regulators pursue and prosecute players in the legal cannabis industry?

The current economic trajectory predicts that retail sales of legal cannabis products in the U.S. will surpass an estimated $41.5 billion annually by 2025, and many banks and NBFIs are eagerly awaiting the federal green light to do business with CRBs without fear of prosecution or legal ramifications.

From 2018 forward, Congress has made several attempts to pass legislation that would protect CRBs when cultivating, distributing, marketing, and selling cannabis products in their state-legalized form. These efforts to declassify cannabis-related activity as a specified unlawful activity have thus far been unsuccessful.

The House passing the MORE Act back in 2020

Passage of the Secure and Fair Enforcement Banking Act of 2021 (SAFE Banking Act) and the Marijuana Opportunity Reinvestment and Expungement Act of 2021 (MORE Act) would enable banks and NBFIs to provide financial services to CRBs. The SAFE Banking Act would provide a safe harbor for banks and NBFIs that provide financial services to CRBs. The MORE Act would deschedule cannabis from the CSA entirely.

Questions to ask

Banks and NBFIs interested in providing financial services to CRBs should ask these questions:

Do we adequately understand our risk, and what are the implications for our organization? How should we augment our risk assessment process and our controls?

To what extent are we willing to accept the risk of banking CRBs? Do we have the ability to identify CRB customers, and if so, do we have any?

How should we advise the board of directors about setting risk appetite?

What customer due diligence (CDD) and enhanced due diligence (EDD) will we need to safely continue with existing customers and onboard new ones?

How will we monitor for unusual and suspicious activity? What will be the alerting and judgmental criteria?

How will our resource needs change so that we stay abreast of new processes and controls?

Risk appetite considerations

In order to determine whether to accept or prohibit CRBs, banks and NBFIs should identify the level of acceptable risk they are willing to take on. Several key components need to be considered, such as:

The board of directors’ stance on legal cannabis, given that good governance recommends and regulators expect that the board sets risk appetite

Cannabis laws in states within the customer footprint and the impact on customers’ communities

Risk profile, customer base, geographic location, products, and services

Relationship with regulators and any recent deficiencies or weaknesses in the BSA and associated compliance programs

Ability to implement appropriate controls and staffing

Developing a strategic road map

If the decision is made to bank CRBs, banks and NBFIs should perform an assessment of compliance maturity for existing BSA/AML program processes and controls to identify potential gaps and develop a strategic road map that helps the organization achieve its vision for future state compliance and sustainable operations.

A well-developed and well-articulated strategic road map visualizes what actions or key outcomes are needed to help organizations achieve their long-term goals. When creating the road map, banks and NBFIs need to demonstrate a keen understanding of their desired strategy, outcomes, markets, and products for onboarding and banking CRB customers. Specifically, banks and NBFIs need to define and explain how desired outcomes and business strategies create risk and exposure.

In addition to a road map, banks and NBFIs should develop and document a detailed risk-based approach that is aligned to the organization’s risk tolerance to determine necessary compliance steps when banking CRB customers.

Specifically, the following activities should be considered when developing a CRB banking program that meets regulatory expectations:

Identifying BSA/AML control gaps related to CRB risk identification and mitigation and formulating a plan to address them

Updating a board-approved policy framework

Updating detailed operating policies and procedures

Planning for capacity, developing job descriptions, and onboarding new personnel

Training for all three lines of defense, senior management, and the board

Developing and documenting a phased or full approach to acceptance of CRB customers

Developing and documenting a CRB program oversight policy

This framework is intended to help banks and NBFIs differentiate types of CRBs and their corresponding risks, and it separates CRBs into three tiers and details risks for each tier. The following exhibit summarizes the approach:

Risk framework by tier

Level

Risk

Tier 1

Direct

Tier 2

Indirect with substantial revenue from Tier 1

Tier 3

Indirect with incidental revenue from Tier 1

Source: CRB Monitor

Even the most conservative of risk appetites equivalent to outright prohibition is not devoid of significant risk considerations. Residual risk frequently encompasses a large number of indirect connections in the total CRB ecosystem. Common examples are printers, lawyers, accountants, landlords, and even utilities and taxing authorities, and all of these are subject to regulatory scrutiny and, importantly, visibility to law enforcement. Also, policies to prohibit or restrict will be audited and examined for compliance, and exceptions will require explanations.

This panorama necessitates expertise and prudence in identifying and evaluating risks within the many layers of CRBs. For example, consider a bank or NBFI that banks a CRB’s employee or vendor. If a bank fails to properly implement controls that would allow it to identify and mitigate risk associated with banking CRBs, it will be susceptible to severe violations of the BSA, including civil money penalties, criminal penalties, and regulatory enforcement actions.

Implementing necessary precautions

A well-developed road map should consider and implement the following activities:

Understanding the most current state and federal cannabis laws and regulations to ensure the bank or NBFI’s compliance

Understanding the local, state, or tribal program to ensure CRB customers are compliant with the program

Implementing a CRB risk assessment

Implementing executive approval practices for direct CRBs

Developing adequate risk ratings (possibly through a risk-based, tiered approach) and corresponding monitoring for CRB customers that includes:

Integrating various customer onboarding and AML solutions at both onboarding and periodic levels

Scheduling regular reviews to include recurring enhanced due diligence, site visits, and transaction monitoring

Monitoring for suspicious activity, including red flags, via open sources for adverse information about the CRB customers and related parties such as beneficial owners

Performing adequate CDD and EDD that will validate that the CRB-offered products, services, and programs are compliant with most current state laws and regulations by:

Collecting appropriate documentation as evidence of compliance, perhaps including a comprehensive onboarding questionnaire, beneficial ownership information, and contracts for the growing, harvesting, transporting and processing of the product

Reviewing applications and supporting documentation used to obtain a legal cannabis state license

Understanding the normal and expected activity of the organization’s CRB customers and their product usage

Developing adequate training programs and governance and oversight programs to address this customer type by:

Updating existing policies and procedures to review inherent risk presented by banking CRB customers

Updating annual training for employees

Auditing initial program design and periodic operational effectiveness

Moving forward cautiously

The ins, outs, and unknowns of cannabis banking are complex, and they require banks and NBFIs to be extremely vigilant with current policy and aware of new developments. Overall, the idea of creating a cannabis program might seem like a daunting task, but with appropriate guidance and care, organizations can provide services in compliance with laws and regulations.

Crowe disclaimer: Qualified organizations only. Independence and regulatory restrictions may apply. Some firm services may not be available to all clients. Given the continued evolution and inconsistency of various state and federal cannabis-related laws, any company should seek competent legal advice relating to its involvement in the cannabis industry, including when considering a potential public offering as a cannabis-related company.

Federal regulations have made compliant credit processing in the cannabis industry difficult to achieve. As a result, most cannabis retailers operate a cash-only model, limiting their ability to upsell customers and placing a burden on customers who might rather use credit. While some dispensaries offer debit, credit or cashless ATM transactions, regulators and traditional payment processors have been cracking down on these offerings as they are often non-compliant with regulations and policies.

Two companies, KindTap Technologies and Aeropay, are addressing the cannabis industry’s payment processing challenges with innovative digital solutions geared towards retailers and consumers.

We interviewed both Cathy Corby Iannuzzelli, president at KindTap Technologies and Daniel Muller, CEO at Aeropay. Cathy co-founded KindTap in 2019 after a career in the banking and payments industries where she launched multiple financial and credit products. Daniel founded AeroPay in 2017 after a career in digital product innovation, most recently at GPShopper (acquired by Financial), where he oversaw the design and development of over 300 web and mobile applications for large scale Fortune 500 companies.

Green: What is the biggest challenge your customers are facing?

Cathy Corby Iannuzzelli, co-founder and president at KindTap Technologies

Iannuzzelli: Our customers include both cannabis retailers and their end consumers. As long as cannabis is illegal at the federal level, normal payment solutions such as debit and credit cards cannot be accepted for cannabis purchases. This has resulted in heavy cash-based sales and unstable, transient work-around ATM payment solutions that can be ripped out with little notice, disrupting the entire business. The lack of a mature payment network to support retail payments for cannabis purchases is a huge challenge for all stakeholders. Cannabis retailers bear the high cost and safety issues of operating a heavily cash-based retail business. Consumers encounter several friction points that require them to change their behavior when purchasing cannabis relative to how they purchase everything else.

Muller: Our cannabis business customers have faced a constantly changing and, frankly, exhausting financial services environment. From the need to move and manage large amounts of cash, to card workarounds, added to the disappointment from legislation around the SAFE Banking Act, these inconsistencies have acted as a roadblock to their potential growth and profitability. Aeropay is in the position to be a stable, long-term, reliable payments partner ready to help them scale their businesses. We believe these opportunities are limitless.

Green: What geographies have got your attention and why?

Daniel Muller, CEO and founder of Aeropay

Iannuzzelli: KindTap’s focus is on the U.S. market where federal policy has created the need for alternatives to traditional payment networks. KindTap is available in every U.S. state where cannabis is legally sold. In terms of our distribution channels, KindTap’s digital payment solution was brought to market during the COVID-19 pandemic when curbside pick-up and delivery became critically important. These channels are where the exchange of cash at pick-up posed the greatest security risk to employees and customers. Our early integrations were with e-commerce platforms focused on delivery and pick-up orders, and our integration partners have strong customer bases in California and the northeast. So, while KindTap can provide its “Pay Later” lines of credit and “Pay Now” bank account solutions anywhere, we have heavier penetration in those regions.

Muller: California, for its established tech culture and how it plays into the cannabis industry – your product simply has to live up to their tech standards to be heard. Also, Chicago, our headquarters, with its newly emerged commitment to financing the cannabis industry and bringing with it a more traditional business approach. In Chicago, you have to have elevated standards of professional practices in any industry you enter. And of course, we love to watch emerging markets like New York and Florida as they head towards adult-use and what shape cannabis and payments will take.

Green: What are the broader industry trends you are following?

Iannuzzelli: We continue to see a strong transition from cash and ATM transactions over to digital payments. Since KindTap has a fully-integrated payment “button” on e-commerce checkout screens, the adoption rate of end consumers to that one-click experience is quite strong. We are also seeing trends of more “express lines” in the retail environment – for those KindTap users who paid online/ahead – and faster/safer delivery experiences to people’s homes since there is no longer the need to collect any payment upon delivery. We are firm believers in the delivery/digital payments combination and a strong increase of that trend as more states allow for delivery.

Muller: The cannabis industry is starting to normalize payments and mirror traditional online and brick-and-mortar. With bank-to-bank (ACH) payments, cannabis businesses can now offer modern customer shopping experiences including pre-payment for delivery orders without the need for a cash exchange at the door, offering the option to buy online pickup in-store and contactless in-store QR scan-to-pay customer experiences. With these familiar and customer-driven options now available, we are seeing widespread adoption, as well as meaningful increases in spend and returning customers.

Green: Thank you both. That concludes the interview!

About KindTap: KindTap Technologies, LLC operates a financial technology platform that offers credit and loyalty-enabled payment solutions for highly-regulated industries typically driven by cash and ATM-based transactions. KindTap offers payment processing and related consumer applications for e-commerce and brick-and-mortar retailers. Founded in 2019, the company is backed by KreditForce LLC plus several strategic investors, with debt capital provided by U.S.-based institutions. Learn more at kindtaptech.com.

About AeroPay: AeroPay is a financial technology company reimagining the way money is moved in exchange for goods and services. Frustrated with the current, antiquated payments landscape, we believe there is a better way to pay and a better way to get paid. AeroPay set out to build a payments platform that works for all- businesses, consumers, and their communities. Learn more at aeropay.com.

Federal regulations have made compliant credit processing in the cannabis industry difficult to achieve. As a result, most cannabis retailers operate a cash-only model, limiting their ability to upsell customers and placing a burden on customers who might rather use credit. While some dispensaries offer debit, credit or cashless ATM transactions, regulators and payment processors have recently been cracking down on these offerings as they are often non-compliant with regulations and policies.

KindTap Technologies, LLC operates a financial technology platform that offers credit and loyalty-enabled payment solutions for highly regulated industries typically driven by cash and ATM-based transactions. KindTap offers payment processing and related consumer applications for e-commerce and brick-and-mortar retailers. Founded in 2019, the company is backed by KreditForce LLC plus several strategic investors, with debt capital provided by U.S.-based institutions.

We interviewed Cathy Corby Iannuzzelli, co-founder and chief payments officer at KindTap Technologies. Cathy co-founded KindTap after a career in the banking and payments industries where she launched multiple financial and credit products.

Aaron Green: Cathy, thanks for taking the time today. How did you get involved in the cannabis industry?

Cathy Corby Iannuzzelli, co-founder and chief payments officer at KindTap Technologies

Cathy Corby Iannuzzelli: I’ve been in the payments industry for a long time. I was doing some consulting a few years ago for a client in Colorado and that gave me exposure to the issues in cannabis like the fact that you couldn’t have real payments in cannabis. Then, a close family member with health issues turned to medical cannabis when nothing else seemed to work. I was amazed by the difference it made in her life. At that point, I put those two things together and I said, I need to focus on helping this industry get a real cannabis payments solution because I thought it was ridiculous that you had an industry of this size and importance that had been abandoned by the payments industry.

Aaron Green: Can you highlight some of your background prior to entering cannabis?

Corby Iannuzzelli: Throughout my career, I’ve been a banker, I’ve been a payment processing executive and I’ve been a consultant. So, I’ve kind of done it all in the payments and financial services space.

Aaron Green: Why is it that most dispensaries only take cash?

Corby Iannuzzelli: In the US, even though cannabis is legal in many states, it’s still illegal federally. There are big banks and card networks like Visa, MasterCard, etc., who are national, even global companies and frankly, the executives of those companies don’t want to end up in jail for violating national laws. So, they have put cannabis dispensaries on what’s called a “prohibited merchants” list. This means you cannot accept Visa, MasterCard, Discover, American Express, or similar payments as a cannabis business and so it’s forcing the industry to a cash-based solution.

About the only thing you’re seeing that’s not cash in dispensaries are ATMs. But if you think about it, ATMs are machines where the consumer goes and pulls cash out and pays upwards of $5 or more in fees for doing that. They then hand that cash back to the dispensary who then has the costs of having to deal with that cash. The industry is just stuck in a cash-based business until federal legislation changes.

Aaron Green: I’ve been to some dispensaries where they accept credit cards or debit cards. What is going on there?

Corby Iannuzzelli: I’ve heard reports of consumers who’ve been able to use a credit card or a debit card in a dispensary. Sometimes the processor who sold that solution to the dispensary says, “Oh, it’s compliant, I guarantee you it’s compliant.” But if you dig in, that’s not the case. And eventually, Visa or MasterCard figures it out and shuts it down. In some cases, it’s outright fraud where the processor who sold the payment terminal to the dispensary is misrepresenting it as say a doctor’s office rather than a dispensary. There’s no merchant category code in the payment networks that says this is for processing dispensary payments, so they pretend it’s something else until they get shut down.

When they do get shut down, I’ve heard of cases in Las Vegas where it was basically 100% Visa or MasterCard one day and 100% cash the next day. It completely disrupted the whole business. It’s not just the retail store, but the inventories and everything else throughout the business.

“About the only thing you’re seeing that’s not cash in dispensaries are ATMs”

There have also been some cases where you’ll see something called a cashless ATM. In a store, they call it a debit card transaction. It’s really a cashless ATM where the consumer is making what looks to the ATM network like a cash withdrawal in $10 or $20 increments, but the consumer is getting a receipt instead of cash, and they’re turning around and handing that receipt back to the dispensary who then makes a change because the cashless ATM only dispensed in $10 or $20 increments.

Now ATM networks are looking at these cashless ATM transactions to see if they are compliant. Do consumers know the fees that they’re paying? Are these transactions coming in and looking to the network like real cash when it’s not? Cashless ATM transactions are probably the most common thing you see, but that’s being called into question after the Eaze incident where a large company was misrepresenting its terminals. The federal government stepped in and called it bank fraud and the individuals behind it, the executives, are in jail. Since then, the networks are looking at this and saying, what about these cashless ATMs? Are those transactions within our rules, or is there something funny going on here?

Aaron Green: So, to summarize here: you’ve got federal regulations at the national level that says that cannabis banking is not allowed so major institutions are not offering it. Yet you found a way through the regulations and compliance issues. I’m curious can you pull back the curtains a little bit and tell us how you came up with a solutionhere?

Corby Iannuzzelli: Well, we came up with the solution by stubbornly refusing to believe that cannabis payment processing could not be done in a compliant manner. We just said, “there is a compliant way to do this, let’s figure it out.” We took the same components that are out there for the financial services and payments industry and reassembled them in such a way that we do not violate any rules. We do not use any of the Visa, MasterCard, Discover or Amex rails, we built our own network. We have direct contracts with the merchants and direct contracts with the consumers. We control everything and all the funds flow through regulated financial institutions. So, we designed something that looks and acts to consumers and retailers the way Visa and MasterCard look and act when a consumer goes to make a purchase, but they run on a separate set of payment rails and in compliance with banking regulations and state regulations. When you’re looking at the problem from a different perspective, sometimes you can come up with a better answer.

Green: On the consumer side, what does that user experience look like?

Corby Iannuzzelli: Our product is completely digital. The consumer experience starts with integration at the online checkout. When it’s an e-commerce shopping cart and somebody is placing an order, they will see a button called “Pay with KindTap.” The first time they click that button they’re automatically brought to our integrated web app where they do a quick and easy application for our digital revolving line of credit product. If approved, they instantly go back to the checkout screen and their first purchase will just happen immediately, with flexible payment options over time. If the consumer decides they don’t want our KindTap credit and would rather have a pay now-product where we pull the funds from their bank account, then the consumer can do so. So, there is no physical card per se, it’s integrated like PayPal or Affirm at the point of checkout online. For the consumers who use KindTap credit, there is a mobile app where they can see their transactions, view statements, pay their bills, etc.

Additionally, there is a loyalty program for all purchases – KindTap credit or through the consumer’s bank, because we feel very strongly that a lot of the reasons consumers choose to pay with one card over another is the points and the rewards that they get. So, we’re providing loyalty rewards with KindTap so that consumers can get rewarded for that spending with KindTap and it’s better for the retailers.

Green: On the retailer side, what does that experience look like and what is your business model?

Corby Iannuzzelli: We are not going store by store doing integrations, rather, we’re integrating with various software, delivery and e-commerce providers. That gives us broad reach and ability to expand rapidly in various state markets where cannabis is legal. Once a merchant says “yes, I want to be a member of the KindTap Merchant Network,” then we work to get them set up on our platform in a matter of days. The merchants receive continuous support from our success team, marketing co-investment and a depth of analytics reporting. We made the entire process and ongoing operations streamlined and frictionless for both merchants and consumers.

Aaron Green: What are the benefits of moving from cash to credit type of payments?

Corby Iannuzzelli: On the retail side, there are the obvious benefits of not having all the security, safety and theft issues associated with operating a physical cash business. Consumers very often don’t carry cash anymore, except when they’re making a cannabis purchase. There are a lot of hidden costs to retailers because payments are not just about moving money from the consumer to the business.

“I really am optimistic that with so many scientific breakthroughs we’ve had that we’re going to be able to figure this out.”Payment options – or lack thereof – can shape where people shop, how much they spend and what they buy. It’s a proven science how consumers make impulse purchases. If you’re a cash-based business in cannabis, and you’re trying to get somebody to make an impulse purchase, and they walked in with $100, then you can’t get them to spend more than $100, no matter how creative your marketing is! The consumer is limited by how much cash they have in their bank account or in their pocket at that point in time. So, it’s really about the upsell that comes with the bigger basket sizes that retailers experience when you move from a cash-based business to credit and suddenly, the merchant doesn’t have to deal with long lines of consumers on payday when the store was beyond slow two days before. Now the consumer can spread purchases with the thinking, “I’d rather not be the one standing in that line on payday. I’m going to go Wednesday [instead of Friday] because I have KindTap credit so I can budget and manage my cash flow throughout the month rather than around my paydays.”

So, we think that the lack of an efficient and effective payment system for cannabis is holding back sales. We all focus on how much the industry is growing. KindTap thinks about how much faster it could be growing if it was supported by a decent payment system.

Aaron Green: What are some other cash-only markets you are looking at?

Corby Iannuzzelli: We are laser-focused on the cannabis ecosystem and bringing a compliant credit and loyalty-based digital payments solution to cannabis merchants and customers and rewarding those stakeholders for accepting/using KindTap. Additionally, we are planning to extend the KindTap Merchant Network so that consumers can use/earn our loyalty points with other goods and services they’re purchasing that are adjacent to cannabis or that are important to the cannabis consumer. That’s the direction we’re going.

Aaron Green: Today people can receive gas points for spending with their credit card. Now with KindTap, you can spend to get cannabis points?

Corby Iannuzzelli: That’s exactly right.

Aaron Green: What in either cannabis or your personal life are you most interested in learning about?

Corby Iannuzzelli: Personally, I am most interested in seeing breakthrough technologies in climate change. We’re going to need to correct this situation and I’m reading about collecting carbon dioxide from the air and burying it in the earth and things like that. I really am optimistic that with so many scientific breakthroughs we’ve had that we’re going to be able to figure this out. Certainly, it’s going to take a lot of smart people and a lot of investment, but I really look forward to watching them do their stuff and hopefully taking us out of this nightmare situation that we’re heading into if we don’t make some changes.

Aaron Green: Thanks Cathy, that concludes the interview.

Few people will disagree that financial compliance isn’t the most exciting topic within the cannabis industry. But compliance is, and always will be, the engine grease to the legal cannabis market. Cannabis operators have the arduous task of dealing with multiple layers of compliance, both operational (maintaining and adhering to regulations enforced by the state licensing board) and financial. These compliance measures include managing everything from seed-to-sale systems for all plant-related activity to on-site requirements like facility access points and alarms systems to name a few.

With complex compliance requirements for the business, the last thing cannabis operators want to think about is financial compliance. We created Confia on this notion. Just as cannabis regulators impose the tracking of plants through the supply chain via a seed-to-sale system, we have developed a storyboard similarly designed to follow the money, which is the equivalent of a transaction-to-deposit system.

Having experience in regulatory technology, artificial intelligence and machine learning, we’ve been fortunate enough to work with some of the world’s largest banks across multiple countries. This experience has afforded us the luxury of working alongside regulators, chief compliance officers and chief risk officers, understanding how risk is perceived by financial institutions and how it ought to be mitigated. It was this access and knowledge that allowed us to effectively reform, enhance and improve the antiquated BSA programs with a technology-enabled process. Leveraging technology is a necessity, almost a requirement, for the cannabis industry as legalization nears and banking access begins to broaden.

Jamming cannabis requirements into an existing BSA program doesn’t scale well. BSA programs are very manual, descriptive and process oriented. So, we’ve taken our prior experience and success in banking to form Confia, distilling the complexities and simplifying the deliverables surrounding cannabis banking compliance. To best articulate cannabis banking requirements, I break it down into three pillars.

Pillar One: KYC-Enhanced Due Diligence

The first pillar is the client-onboarding bucket or KYC – Know Your Customer. In the complex world of cannabis banking, banks must know and understand their clients to great depths. It’s not enough to simply know that the client exists; you also have to understand whether or not that client could be a potential risk to the bank, and one step further, the financial system. Cannabis is a high-risk industry, so the KYC requirement is escalated to a deeper diligence and review, called Enhanced Due Diligence (EDD).

Cannabis is a high-risk industry so extra due diligence is needed

Banks need to know and understand their customers’ story, and all the key parties (officers, directors, and those with key decision-making powers or access to the bank accounts) within that organization. This includes reviewing personal, business, and legal history – not to mention watchlists and negative news presence. An initial onboarding review must then be followed with daily screening and monitoring of all watchlists and adverse media. Typically, banks do KYC refreshes every three years. In cannabis, a full refresh should be done annually with the daily monitoring systems in place.

The high-risk nature of the industry also requires a level of diligence on all parties to a transaction, even if one of the parties, whether a payer or recipient, is not a client of your bank. Unlike traditional banking sectors, reliance on other banks’ KYC programs is far less defensible in the cannabis industry.

Pillar Two: Transactional Monitoring & Detection

Tracking and monitoring the actual financial transactions comprises the second pillar required for cannabis banking. At Confia, we have focused on streamlining processes, so the cannabis operator can seamlessly support the compliance obligation for every transaction. A bank must demonstrate supporting documentation for every cannabis transaction, and gathering such information is a large undertaking in and of itself and can pose future issues if not done properly, see the pitfalls for lack of compliance. Banks are obligated to understand the nature and reason for each transaction, the source of funds, ensure cannabis licenses are in good standing for all parties, and collect evidence such as accounting records and seed-to-sale data.

Core to transaction monitoring in the traditional sense, is the overarching support through anomaly detection. Relying on information is important, but testing those inputs keeps everyone honest. It is important to evaluate transactions from a holistic point of view relative to peers and relative to the general contents of a transaction. This anomaly detection layer is your last line of defense, and as new information is collected, it continues to refine itself.

Pillar Three: Filing and Reporting Requirements

The third component to compliant cannabis banking is regulatory filing and reporting. Once a client is onboarded, the account requires an initial suspicious activity report or SAR-Initial within 30 days of that client being approved by the bank. Then, a report must be filed every 90 days after that for all the transactions of that cannabis operator. Banks must file the SAR-Initial and the Continuing-SAR reports for each cannabis client they have.

The high-risk nature of the industry requires a level of diligence on all parties to a transaction

Solutions like Confia automate the filing process and support the filing with transactional data evidenced on our distributed ledger of record. This provides immutable audibility and simplifies the process for all parties involved.

Compliance Requirements After US Legalization

The anticipation of federal legalization and banking reform bills has many operators hoping for easier banking. Yet, in my opinion, regulatory oversight and audits will likely increase after such reform or legalization. As other financial institutions start to support cannabis, it will inadvertently create greater opportunity and expose the financial system to nefarious or illegitimate transaction activity. This is why cannabis banking will be carefully monitored by regulators, and more so, why banks will be slow and pragmatic in standing up their internal cannabis banking programs. Some banks may forever avoid the cannabis industry due to the known pitfalls of an industry specific program, while others may simply mitigate the possible exposure to reputational risk.

Choose Wisely: Pitfalls for Lack of Compliance

Financial compliance is the responsibility and duty of the banks, but the real losers and result of non-compliance always fall on the cannabis operators. Regulatory action against an institution may result in the bank shutting down its cannabis program or may require them to complete a remediation of all their cannabis transactions for a certain period from its clients. At the end of the day, regardless of action, the cannabis operator is the one being punished. Operators either lose their bank account and have business massively disrupted, or they are asked to provide all the compliance docs for a historic period, which is a huge undertaking and operational distraction, ultimately impacting business and productivity. So, choose your banking partner wisely.

Summarizing Key Banking Requirements

In summary, banking in the cannabis industry will undoubtedly remain a high-risk industry, with or without legalization. Although banking opportunities may expand as US policies change, there will be continued compliance and regulatory requirements for the foreseeable future.

Onboarding and ongoing screening are critical

Evidence for every transaction is a significant portion of compliance and must not be dismissed

Evaluating activity with broader strokes is essential in mitigating against money laundering

Managing the staggered filing timelines and due dates for each client

Compliance is the most crucial factor in cannabis banking at this point. It cannot be overlooked or taken for granted. Cannabis operators must take an active role in evaluating the compliance programs of their financial providers. To open a bank account is one thing, but the consideration and effort that goes into keeping a bank account is the difference that will protect your business in the long run.

Before jumping into what cannabis businesses can do amid this pandemic, it is crucial to explore the specifics behind how the virus impacted the industry as a whole. From a surface level, it seems obvious what happened: dispensaries had to implement social distancing protocols, require both customers and employees to wear masks and limited the number of customers that can be present on the point-of-sale floor room. But COVID-19 did not merely make shopping experiences a tab bit inconvenient.

Cannabis producers, and especially those involved in manufacturing cannabis goods, experienced an apparent disruption in their production schedules. If the metals and plastics were sourced from Wuhan, Shenzhen or any other dense industrial area in China, supplies suddenly stopped coming, and producers were left with limited production options. Businesses did not consider the value of having various vendors and instead put all their stock in one source. A disruption in production inherently impacts dispensaries.

COVID-19 impacted more than just supply chains, however. For instance, investors are now less likely than before the pandemic to invest in early-stage cannabis companies. Competition for capital now far outweighs the supply for cannabis companies, and we have seen (and will continue to see) a drop in company valuations. Indeed, COVID-19 is affecting more than just currently existing operators but those yet struggling to create cannabis businesses of their own.

Vendors & Supplies

A broad survey conducted by the Institute for Supply Management (ISM) between February 22, 2020 and March 5, 2020 found that 75% of U.S. companies had experienced supply chain disruption as a result of the COVID-19 outbreak. An estimated 90-95% of all components utilized in cannabis vaporizer pens were sourced from manufacturers in Shenzhen, China. In contrast, very few companies used domestic manufacturers. While this is just one example, it is equally important to note that cannabis-specific equipment and supply shortages were not the only factors that disrupted cannabis businesses. Shortages of personal protective equipment (PPE) presented challenges for cannabis dispensaries, producers and manufacturers that continued to operate during the “shelter in place” orders.

Operators must establish a resilient supply chain. Do not simply limit your options to one specific region, as this can be a costly mistake. Operators must cultivate an in-depth understanding of their supply chain beyond critical suppliers and their stress points; they need to develop and follow a systematic supply process that takes potential disruptions and stress points into account. When vetting potential vendors, always ask detailed questions that elicit evidence-backed responses. Ask vendors where they source their materials from, whether they have any history of experiencing disruptions in their supply chain and what kind of setbacks they have suffered as a result of COVID-19.

Investing in Your Core Business

In light of COVID-19, operators must invest in solutions that increase efficiency and improve the customer’s experience. This entails ensuring your customer safely enters and leaves your dispensary with a product they are satisfied with—the essence of any retail operation. Your operation should focus on enhancing customer flow as opposed to encouraging aimless roaming. Having an open-space, Apple store style dispensaries might have been a popular option before, but times have changed, and dispensaries must adapt.

Guided purchases offer not just more efficient transactions, but also serve to ensure that your waiting room isn’t backed up with an endless stream of unmanageable customers. Depending on your locally-mandated COVID-19 protocols, your dispensary will likely not be permitted to hold a high number of customers in the store, nor should it during this pandemic. Each customer service representative must be active as opposed to passive, directly asking customers what they are interested in, offering product or strain choices when customers seem unsure and answering questions as thoroughly as possible to avoid confusion and inherently delays. Be sure to emphasize the value of guided purchases to your employees and how they can promote the safety of both themselves and their customers.

Maintaining Urgency

The uncertainty of COVID-19 and its impact on the general economy has left many individuals “clocked out.” Simply put, many people feel that they should wait until things go back to normal before making any critical decisions. As essential businesses, cannabis operators cannot afford to make this same mistake. Now is not the time to sit back, reflect and wait for the vaccine. Instead, operators must work to precisely assess how COVID-19 impacted their business and execute a clear plan of action to address foreseeable problems.

Execution is far more important than perfection; you’ll need to make changes on a dime and avoid spending excessive hours obsessing over debating specific actions rather than taking them. It is far more essential to get tasks done versus ensuring they are perfect. If something is not working in your business, it must be readdressed or removed entirely from the protocol. It is far better to make necessary changes now amid the pandemic as opposed to reactively waiting and seeing what may come next following it.

Stay nimble by cutting out any factors that may be slowing down your company’s efficiency. Is your point-of-sale system causing issues? Can you use a better payment processing tool? Are any employees underperforming? Are there any internal policies that may be hindering your employees’ ability to work as optimally as possible? These are some of the many factors that must be considered to ensure your business stays agile and adaptable. Determine what is working against you and execute a plan of action to address. Do not wait and do not take shortcuts around regulations.

Understanding the Shift in Purchasing Behavior

Regardless of whether or not a vaccine for COVID-19 is completed anytime soon, operators must know that there is no “returning to normal.” People’s habits and behaviors have changed due to this virus, whereas slow browsing of items might have been preferable for some individuals before COVID-19; this is likely not the case today. Furthermore, research groups like Accenture have found that most customers expect their shopping habits to change permanently.

Source: Accenture COVID-19 Consumer Research, conducted April 2–6. Proportion of consumers that agree or significantly agree.

In the study mentioned above, shopping more consciously is one of the two top priorities for customers during this pandemic. According to Accenture, “[c]onsumers are more mindful of what they’re buying. They are striving to limit food waste, shop more cost consciously and buy more sustainable options. Brands will need to make this a key part of their offer (e.g., by exploring new business models).” Furthermore, customers are now more likely to shop locally; this is why community engagement would be especially important to ensure you develop transparency and trust between your brand and your customers. Understanding this shift in purchasing behavior will remain one of the more crucial tasks of any cannabis operator.

Expanding Sales Avenues

More and more customers are now relying on online and curbside purchases than ever before. Dispensaries must look to their current sales avenues and determine where key focuses should be made. Use your sales data to determine where customers are making their purchases the most, be it through third-party delivery services such as Eaze, standard home delivery, online ordering or curbside pickup. Focus on identifying friction and streamlining the user experience on all customer-facing platforms and services. Equally, consider which platform your customers are using the most to make purchases; are they making more online purchases, or do most still prefer direct shopping at the store? Remember that having more products doesn’t necessarily mean more revenue. You must also identify which products are performing well and which have low margins.

These considerations can help strengthen your highest performing platform while working to fix any more inferior performing platforms. As stated before, stay nimble; if something is not working out, cut it out from your business model, and move forward. Do not be afraid to cut poor-performing platforms to hone your focus on the successful ones. Since post-COVID-19 shopping behavior is likely to stay permanent, these changes may still be applicable following a slowdown or cessation of the virus.

Delighting Your Customers

Virus or not, customer satisfaction remains one of the most crucially defining points for the future of your business. Your customers must be safe and must be happy with their purchase. To ensure this outcome, you need to maintain adequate safety policies while equally promoting streamlined purchases. Although a limited number of individuals may be annoyed with over-the-top safety precautions, most customers will enjoy the heightened security that comes alongside these types of measures.

Contactless service, such as having customers scan their identification upon entry or encouraging more credit card versus cash transactions, can increase customer satisfaction, as they will feel a stronger sense of security when shopping at your dispensary. Focus on streamlining curbside pickup. Things such as requiring vehicle descriptions (e.g., license plate numbers, color, make) for curbside pickup purchases can go a long way in helping employees quickly identify customers.

Equally, be sure there is hand sanitizer available near the entrance of your dispensary. This adds a further sense of security for your shoppers. Delivery should be consistent; delays and setbacks must be minimal to win the confidence of your customers. Take the extra steps to ensure your dispensary is clean and products hygienic. All these factors work to increase customer satisfaction while maintaining their safety, and more importantly, impact the level of trust your customers have in association with your brand.

Scaling Operations Taking Advantage of Limited Competition in Emerging Markets

As stated before, several individuals—including existing and emerging cannabis businesses—are clocked out following COVID-19. This mindset is not only detrimental for operations but can also impact how you scale your business. New markets are coming online and will continue to do so as regulators are increasingly incentivized to replenish government coffers. Riverside County in California, for instance, is now allowing for capless licenses for all cannabis business types. However, what remains the key focus for regulators is expanding the number of delivery and distribution operators. In Massachusetts, delivery endorsements for dispensaries are available without a set deadline to social equity applicants and do not have a defined cap. In Illinois, the cap for transporters was equally removed, and each applicant who scores above 75% will receive a license.

These types of licenses are now more valuable than ever before for two reasons. The first reason is that regulators are keener to award delivery and transporter licenses than other types. Secondly, customers now prefer home delivery over shopping in stores due to COVID-19. With more people clocked out during these times, you have far more opportunities and far fewer competitors during application processes. Use this time to truly develop a strategy for expansion, as the chance might not come so quickly again.

Conclusion

As a final point, be sure to expand your online presence during this time. Although you may not have the capacity to reflect your company’s personality and value through quick in-store transactions, you can use social media to encourage product reviews, social interactions, and recommendations. Invest in marketing through social media platforms. Platforms such as TikTok have helped form communities of like-minded individuals. Use platforms such as that to highlight your company’s personality and values, avoid being “salesy” and focus more on being funny, entertaining and just alive. Character adds value to your business.

People want to laugh, to feel safe and they want to live. Create social interactions and immersion and always prioritize being honest and transparent with your customers. This final point stands as equally as important as the rest of the considerations highlighted throughout this article. Stay nimble, stay active and stay alert! Do not view the chaos behind this pandemic as a pit, and instead see it as a ladder. Track down opportunities, do not be afraid of change, and, more importantly, do not wait for an answer to COVID-19, be the answer.

As state and local jurisdictions rake in millions of dollars in tax revenue from the state’s legal cannabis industry, new states, counties and cities are piling onto the cannabis tax bandwagon. There are currently hundreds of local cannabis business taxes in place in California. On the November ballots, there are 47 new local cannabis tax measures. In fact, even some local jurisdictions that outlaw cannabis operations want a piece of the green pie and are asking voters to impose cannabis business taxes.

More cannabis tax measures being passed means more regulations and compliance responsibilities for cannabis businesses. This is especially taxing (pun intended) for multi-licensed and multi-location cannabis businesses. With hefty monetary penalties and even revocation of business licenses as consequences of noncompliance, adherence to state and local tax regulations is of paramount concern to cannabis businesses. Below is a list that Taxnexus has put together showing all of the cannabis tax measures on the November 6 ballots in California:

Taxnexus is an automated transaction-to-treasury cannabis tax compliance solution for the entire cannabis supply chain that provides point-of-sale state and local cannabis sales and use tax calculation, tax data management as the authority of record, and timely filing of returns with all applicable taxing authorities.

California City and County Cannabis Tax Measures November 6, 2018 Ballots

City

County

Measure

Name

Proposal

Adelanto

San Bernardino

S

Adelanto Marijuana Tax

To authorize the city to impose a tax on marijuana businesses of up to $5.00 per square foot on nurseries and up to 5% on other businesses.

Atascadero

San Luis Obispo

E-18

Atascadero Cannabis Business Tax

To impose a tax on cannabis businesses at annual rates not to exceed $10.00 per canopy square foot for cultivation, 10% of gross receipts for retail cannabis businesses, 2.5% for testing laboratories, 3% for distribution businesses, and 6% of gross receipts for all other cannabis businesses.

Atwater

Merced

A

Atwater Marijuana Tax

To authorize the city to impose a 15% tax on marijuana businesses.

Benicia

Solano

E

Benicia Marijuana Business Tax

To authorize the city to impose a tax of up to $10 per square foot for marijuana nurseries and 6% of gross receipts for other marijuana businesses.

Capitola

Santa Cruz

I

Capitola Marijuana Business Tax

To authorize the city to tax marijuana businesses at a rate of up to 7% with no expiration date to fund general city purposes.

Chula Vista

San Diego

Q

Chula Vista Marijuana Business Tax

To authorize the city to tax marijuana businesses at the following rates: 5% to 15% of gross receipts or $5 to $25 per square foot for cultivation.

Colfax

Placer

C

City of Colfax Cannabis Business Tax

To tax cannabis businesses at annual rates not to exceed $10.00 per canopy square foot for cultivation (adjustable for inflation), 6% of gross receipts for retail cannabis businesses, and 4% for all other cannabis businesses.

Colton

San Bernardino

U

Colton Marijuana Tax

To authorize the city to impose a tax on marijuana businesses of up to $25.00 per square foot on nurseries and up to 10% on other businesses.

Emeryville

Alameda

S

Emeryville Marijuana Business Tax

To enact a marijuana business tax at a rate of up to 6% of gross receipts to fund general city purposes.

Fresno

Fresno

A

Fresno Marijuana Business Tax

To tax marijuana businesses at rates of up to $12 per canopy square foot and up to 10% of gross receipts for medical dispensaries and other marijuana businesses, with revenue dedicated to the city’s general fund an a community benefit fund.

Goleta

Santa Barbara

Z2018

Goleta Marijuana Business Tax

To authorize the city to tax marijuana businesses at the following initial rates with a cap at 10% of sales: 5% for retailers; 4% for cultivators; 2% for manufacturers; and 1% for distributors/nurseries.

Hanford

Kings

C

Hanford Cannabis Business Tax

To tax cannabis businesses at an annual maximum rate of $7 per square foot of canopy for cultivation businesses using artificial lighting only, $4 per square foot of canopy for cultivation businesses using a combination of artificial and natural lighting, $2 per square foot of canopy for cultivation businesses using natural lighting only, and $1 per square foot of canopy for nurseries, 1% of gross receipts of laboratories, 4% of gross receipts of retail sales, 2% of gross receipts of distribution and 2.5% of gross receipts of all other types of cannabis businesses.

Hesperia

San Bernardino

T

Hesperia Marijuana Tax

To authorize the city to impose a tax on marijuana businesses of up to $15.00 per square foot on nurseries and up to 6% on other businesses.

La Mesa

San Diego

V

La Mesa Marijuana Business Tax

To authorize the city to tax marijuana businesses at rates of up to 6% gross receipts and up to $10 per square foot of cultivation.

Lassen

Lassen

M

Lassen County Commercial Marijuana Business Tax

To authorize the county to enact a tax on commercial marijuana at rates of between $0.50 to $3.00 per square foot for cultivation and 2.5% to 8% on gross receipts for other businesses, such as retail, distribution, manufacturing, processing, and testing.

Lompoc

Santa Barbara

D2018

Lompoc Marijuana Business Tax

To authorize the city tax marijuana businesses at the following rates: $0.06 per $1 of non-medical retail sales proceeds; $0.01 per $1 of cultivation proceeds; $15,000 for net income less than $2 million of manufacturing/distribution proceeds; $30,000 for net income $2 Million or more of manufacturing/distribution proceeds; a total aggregate tax of $0.06 per $1.00 of microbusinesses proceeds; and no tax on testing.

Malibu

Los Angeles

G

Malibu Marijuana Business Authorization and Tax

To authorize the sale of recreational marijuana in the city and imposing a general tax at the rate of 2.5% of gross receipts on the sale of recreational marijuana.

Marina

Monterey

V

Marina Marijuana Business Tax

To authorize marijuana businesses to operate in the city and authorizing the city to tax marijuana businesses at rates of up to 5% of gross receipts, with revenue funding general city purposes.

Maywood

Los Angeles

CT

Maywood Marijuana Business Tax

To authorize the city to tax marijuana businesses at a maximum rate of 10% of gross receipts to fund general city purposes.

Moreno Valley

Riverside

M

City of Moreno Valley Commercial Cannabis Activity Tax

To enact a tax on cannabis sales and cultivation, not exceeding 8% of gross receipts and $15 per square foot of cultivation.

Morgan Hill

Santa Clara

I

Morgan Hill Marijuana Business Tax

To authorize the city to tax marijuana businesses at annual rates up to $15.00 per canopy square foot for cultivation and up to 10% of gross receipts for all other marijuana businesses.

Mountain View

Santa Clara

Q

Mountain View Marijuana Business Tax

To enact a tax on marijuana businesses of up to 9% of gross receipts to fund general city purposes.

Oakland

Alameda

V

Oakland Marijuana Business Tax Amendments

To amend the marijuana business tax law to: allow marijuana business to deduct the cost of raw materials from their gross receipts and to pay taxes on a quarterly basis; and allow the city council to amend the law in any manner that does not increase the tax rate.

Oroville

Butte

T

Oroville Marijuana Tax

To authorize an annual gross receipts tax on cannabis businesses at rate not to exceed 1%, with initial rates of 5% on retailers and manufacturers; 4% on cultivators; 3% on distributors; 2% on nurseries; 0% on testing laboratories; and 7% on microbusiness to generate approximately $300,000 to $600,000 in annual revenue.

Paso Robles

San Luis Obispo

I-18

Paso Robles Cannabis Business Tax

To impose a maximum tax rate on every person or entity operating or conducting a cannabis business within the City a cultivation tax of up to$20.00 per square foot of space utilized in connection with the cultivation and processing of cannabis; a gross receipts tax of up to 10% for all cannabis transportation; a gross receipts tax of up to 15% for all cannabis manufacturing, testing, and distribution; and a gross receipts tax of up to 10% for dispensaries.

Pomona

Los Angeles

PC

Pomona Marijuana Business Tax

To authorize the city to tax marijuana businesses at rates of $10.00 per canopy square foot for cultivation and up to 6% of gross receipts for all other marijuana businesses to fund general city purposes.

Riverbank

Stanislaus

B

City of Riverbank Cannabis Business License Tax

To authorize the City Council of the City to impose a business license tax at a rate of up to 10% of gross receipts on cannabis businesses and dispensaries, to help fund general municipal services.

San Bernardino

San Bernardino

W

San Bernardino Marijuana Tax

To authorize the city to impose a tax on marijuana businesses of up to $10.00 per square foot on nurseries and up to 6% on other businesses.

San Diego

San Diego

AA

City Council Marijuana Business Tax Measure

To authorize the city to tax marijuana businesses at the following rates: $14 per square foot; up to 8% on manufacturing and distribution; up to 10% on medicinal retail; up to 12% on adult-use retail; and up to 3.5% on testing.

San Francisco

San Francisco

D

San Francisco Marijuana Business Tax Increase

To tax marijuana businesses with gross receipts over $500,000 at a rate between 1% and 5%, exempting retail sales of medical marijuana, and expanding the marijuana business tax to businesses not physically located in San Francisco.

Santa Ana

Orange

Y

Santa Ana Recreational Marijuana Business Tax

To authorize the city to tax marijuana businesses at rates of $0.25 to $35.00 for gross square footage and up to 10 percent for cultivating, manufacturing, distributing, selling, or testing.

Santa Clara

Santa Clara

M

Santa Clara Marijuana Business Tax

To authorize the city to tax commercial marijuana businesses up to 10% of gross receipts and up to $25 per square foot for cultivation.

Simi Valley

Ventura

Q

Cannabis Business Tax

To enact a maximum tax on gross receipts of cannabis businesses in the City after January 1, 2019, as follows: for testing, 2.5%; for retail sales, retail delivery, or microbusiness retail, 6%; for distribution not to consumers, 3%; for manufacturing, processing or nonretail microbusiness, and any other type of business not otherwise specified, 4%; and for cultivation, a tax per square foot of canopy ranging from $2.00 per square foot of canopy to $10.00 per square foot of canopy, depending on the type of lighting (artificial or natural) used.

Solvang

Santa Barbara

F2018

Solvang Marijuana Business Tax

To authorize the city to tax marijuana businesses at an initial rate of 5 percent of gross receipts with a cap of 10 percent and a maximum annual increase of 1 percent.

Sonora

Tuolumne

N

City of Sonora Cannabis Business License Tax

To enact a business license tax at a rate of up to 15% of gross receipts on cannabis businesses, to help fund general municipal services; and increasing the City’s appropriations limit for the Fiscal Years 2019-2023 by the amount of tax proceeds received.

Suisun

Solano

C

Suisun Marijuana Business Tax

To authorize the city to impose a tax of up to $25 per square foot and 15% gross receipts for marijuana businesses.

Union City

Alameda

DD

Union City Marijuana Business Tax

To authorize the city to tax marijuana businesses at rates of $12.00 per square foot for cultivation and 6 percent of gross receipts for other businesses to fund general municipal services.

Vista

San Diego

Z

Vista Retail Medical Marijuana Sales and Tax Initiative (November 2018)

To authorize commercial retails sales of medicinal marijuana for up to 11 retailers and enacting a 7% tax on the business’ gross receipts.

Contra Costa

R

Contra Costa County Marijuana Business Tax

To authorize Contra Costa County to tax commercial marijuana businesses in the unincorporated area in the amount of up to $7.00 per canopy square foot for cultivation and up to 4 percent gross receipts for all other cannabis businesses to fund general County expenses.

El Dorado

N, P, Q, R, S

Commercial Cannabis Tax Measures

To impose a general tax on any independently authorized commercial cannabis activity in the unincorporated areas of El Dorado County at rates up to: $30 per square foot or 15% for cultivation; 10% for distribution, manufacturing, and retail; and 5% for testing laboratories, effective until amended or repealed, with estimated annual revenue of $1,900,000 to $52,800,000.

To authorize outdoor and mixed-light (greenhouse) commercial cannabis cultivation for medicinal use on parcels of at least 10 acres zoned Rural Lands, Planned Agricultural, Limited Agricultural, and Agricultural Grazing that are restricted in canopy size, required to pay a County commercial cannabis tax, and subject to a site-specific review and discretionary permitting process with notification to surrounding property owners and environmental regulation.

To authorize outdoor and mixed-light (greenhouse) commercial cannabis cultivation for recreational adult use on parcels of at least 10 acres zoned Rural Lands, Planned Agricultural, Limited Agricultural, and Agricultural Grazing that are restricted in canopy size, required to pay a County commercial cannabis tax, and subject to a site-specific review and discretionary permitting process with notification to surrounding property owners and environmental regulation.

To authorize the retail sale, delivery, distribution, and indoor cultivation of commercial cannabis for medicinal use on parcels zoned Community Commercial, Regional Commercial, General Commercial, Industrial High, and Industrial Low that are restricted in number and concentration, required to pay a County commercial cannabis tax, and subject to a site-specific review and discretionary permitting process with notification to surrounding property owners and environmental regulation.

To authorize the retail sale, delivery, distribution, and indoor cultivation of commercial cannabis for recreational adult use on parcels zoned Community Commercial, Regional Commercial, General Commercial, Industrial High, and Industrial Low that are restricted in number and concentration, required to pay a County commercial cannabis tax, and subject to a site-specific review and discretionary permitting process with notification to surrounding property owners and environmental regulation.

Lake

K

Lake County Marijuana Business Tax

To authorize the county to enact a marijuana business tax at the rates of $1.00 per square foot for nurseries and cultivators and between 2.5% and 4% for other businesses.

San Joaquin

B

Unincorporated County of San Joaquin Cannabis Business Tax

To impose a special tax on commercial cannabis businesses in unincorporated San Joaquin County at a rate of 3.5% to 8% of gross receipts, with an additional cultivation tax of $2.00 per square foot of cultivation space.

Tuolumne

M

Tuolumne County Commercial Cannabis Business Tax

The County to impose a 0%-15% gross receipts tax on commercial cannabis businesses (but no less than $0-$15 per square foot for cultivation businesses as annually increased by a consumer price index) in the unincorporated area of Tuolumne County, and to authorize the Board of Supervisors to implement and adjust the tax at its discretion, with funds staying local for unrestricted general revenue purposes, including but not limited to public safety, health,environmental protection and addressing industry impacts, unless repealed or amended by voters.

Last week, Hoban Law Group announced a major international expansion, with new offices in Latin America and the European Union. The Denver-based law firm said they will have four new offices across the EU by late fall and two new offices in Latin America by spring of 2018.

Bob Hoban, managing partner

Bob Hoban, managing partner and co-founder of Hoban Law Group, says they have already been working internationally for years. “HLG steps in to global markets quickly as our direct work with government officials on policy and regulation has kept us in this important global curve,” says Hoban. “We have accepted the challenge of being global cannabis industry leaders & experts and will work with strategic industry-leading partners, such as New Frontier Data, to move the industry forward across six countries.”

The press release says the law firm has been advising governments around the world on cannabis policy for several years, as well as working on a handful of international business transactions in the past. These new offices will work mainly with structured finance, mergers and acquisitions, worldwide trade, regulatory law and equity placement in the cannabis (including industrial hemp) industry. “Combining the firm’s corporate practice, with our intellectual property and tax practice groups will position our firm’s client’s to succeed at the highest levels in this international marketplace,” says Hoban.

The press release also announced they have added Andrew Telsey, an experienced securities attorney, to their firm. He has helped take more cannabis businesses public in the U.S. than any other attorney.

Hoban Law Group, founded in 2009, is the nation’s largest cannabis business law firm. They have attorneys in every state that has legalized cannabis in the United States.

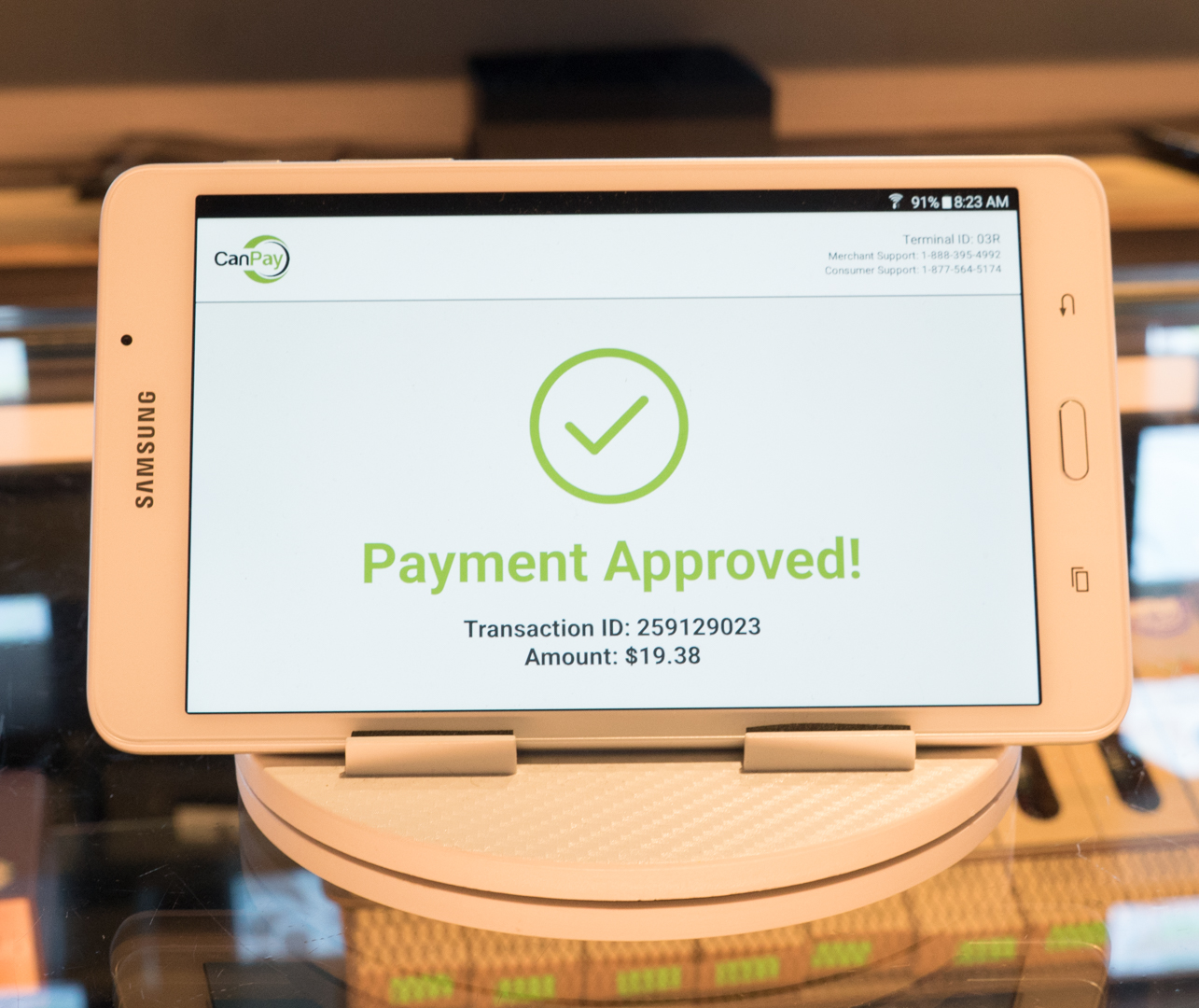

CanPay, a debit payment solution for the cannabis space, announced today their partnership with Harborside, the largest medical dispensary brand in the United States. The partnership will allow Harborside’s more than 200,000 patients to use a mobile debit app when purchasing cannabis through their delivery service, instead of bringing cash.

For deliveries, patients would use the CanPay app on their device “to generate a secure, single-use payment token that includes no personal identifiable information,” according to the press release. A Harborside delivery employee scans the token and the money is transferred from the patient’s checking account to Harborside. This allows for delivery employees to make less cash transactions and affords patients the luxury of not having to take out cash to get their medicine.

Harborside, founded in 2006, is recognized as the largest nonprofit cannabis dispensary in California, and the United States. They were reportedly the first dispensary to lab test their products. Being an advocate for patients and their safety, they offer a variety of free health and wellness services. “It’s important to us that we stay on the forefront of patient care and access to the products our community needs to improve their quality of life,” says dress wedding, co-founder of Harborside. “CanPay enables us to continue delivering on those goals by normalizing the payment process for our patients and staff.”

CanPay launched last year in November and has since expanded to over 50 dispensaries and six different states. The premise of their system is a secure and safe transaction for customers or patients of dispensaries. “To ensure privacy and security, all purchases are made using non-identifiable, single-use, and random payment tokens generated in the CanPay App,” reads the press release. CanPay is currently serving businesses in Washington, California, Colorado, Maine, Florida, and Oregon.

Dustin Eide, CEO of CanPay

“Patients who rely on cannabis for preexisting medical conditions should not have to be inconvenienced or have their safety put at risk by a cash-only model,” says Dustin Eide, chief executive officer of CanPay. “Delivery is a mainstream solution and payments should be able to keep up with the industry. By partnering with Harborside, we are providing their patients the benefits of more secure, transparent transactions.” According to Eide, their service is compliant with federal medical cannabis policy and guidance. “CanPay’s service operates under compliance programs built around the Cole Memo and FinCEN Guidance issued by the Department of Justice and the Treasury, respectively, and updated on Feb. 14, 2014 which provided guidance to financial institutions on the conditions with which they can provide banking services to the state regulated cannabis industry without incurring federal action,” says Eide. “Also, CanPay utilizes the Automated Clearing House (ACH) network to affect our services in full transparency. While Visa and MasterCard have established clear rules prohibiting cannabis transactions on their networks, the ACH network relies on the individual financial institutions to determine what type of transactions may occur.” Because of that, Eide says, there’s no need to hide transactions, unlike services that use Visa or MasterCard that require using an obscure legal entity name or a financial intermediary’s name.