By Abraham Finberg, Rachel Wright, Simon Menkes No Comments

In Part 1, we examined the current status of adult use cannabis in Minnesota, paying particular attention to the licensing framework, taxation and social equity considerations. In this article, we’ll cover some important need-to-know info if you’re considering opening an adult use business in the “Land of 10,000 Lakes.”

Starting a Cannabis Business in Minnesota: Important Considerations

As the state does not expect to begin issuing licenses before the first quarter of 2025, now is the time to plan a licensing campaign. With a population of 5,714,000, 64% of which live in the Twin Cities of Minneapolis-Saint Paul, Minnesota is close in population to Colorado, with 5,774,000 residents. Colorado currently has around $1.8 billion in yearly retail cannabis sales. This may suggest a similar possible level of sales for Minnesota once its retail cannabis market matures.

In a recent op-ed piece for Marijuana Moment, the New York cannabis consulting firm of Bridge West Consulting suggested three reasons, in addition to low cannabis excise taxes and reasonable license fees, why entrepreneurs should consider investing in a retail cannabis business in Minnesota:

Minnesota legislation prohibits localities from banning cannabis businesses. This avoids serious problems that have plagued cannabis businesses in other states including California and Montana in which access for cannabis companies has been denied and, in Montana’s case, even reversed. (Minnesota’s new legislation does allow local governments to limit the number of cannabis retailers to one for every 12,500 residents, however.)

Minnesota has allocated funds to assist social equity cannabis businesses, including $6 million to the CanStartup which will fund non-profits to make loans to budding cannabis businesses.

Bridge West makes the interesting observation that Minnesota is bordered by four states—Wisconsin, Iowa, South Dakota and North Dakota—none of which have legalized adult use cannabis. Moreover, an estimated 1.9 million people live outside of Minnesota within a 50-mile radius. That means that not only will Minnesotans not have to compete with out-of-state cannabis dispensaries but will benefit from the purchases of out-of-state residents that live within a comfortable distance.

How a License Application is Scored

HF100 gives some guidance as to how the Office of Cannabis Management (OCM) will score license applications, awarding points for the following 9 categories: social equity status, veteran status, security and record keeping, employee training plan, business plan and financial situation, diversity plan, labor and employment practices, knowledge and experience and environmental plan.

The OCM may award additional points if the applicant would expand service to an underrepresented market. Points may also be awarded to those applicants who can demonstrate a negative impact from cannabis prohibition such as arrest or imprisonment of the applicant or their immediate family. This is different from social equity status and the law says points may be awarded to the applicants “in the same manner as points are awarded to social equity applicants.”

Emphasis on Market Stability; Prohibition of Vertical Integration

Minnesota is taking measures to ensure “market stability,” which it doesn’t specifically define, but which it says involves:

Ensuring an adequate supply of cannabis, but not a glut.

Eliminating the illicit cannabis market.

Promoting a craft cannabis industry.

Prioritizing growth and recovery in communities that have experienced a disproportionate, negative impact from cannabis prohibition.

HF100 states, “The office shall issue the necessary number of licenses in order to ensure the sufficient supply of cannabis flower and cannabinoid products to meet demand, provide market stability, and limit the sale of unregulated cannabis flower and cannabinoid products.”

Continuing its emphasis on “smaller is better,” HF100 says, “Unless the office determines that the issuance of bulk cultivator licenses is necessary to ensure a sufficient supply of cannabis flower and cannabinoid products, the office shall not issue a bulk cultivator license before July 1, 2028.”

Vertical integration is also prohibited. “The office shall not issue licenses to a single applicant that would result in the applicant being vertically integrated.” HF100 goes on to state that microbusinesses are exempted, and that if the OCM determines that vertical integration is necessary to ensure a sufficient supply of cannabis and cannabis products during the first year of such products being sold to customers, it may authorize one or more applicants to be vertically integrated. However, such a group of licenses are very temporary and will expire at the end of that first year period.

An entity holding a cannabis retailer license may also hold a delivery license, a medical retailer license and an event organizer license. But no retailer may hold any other license. Also, no entity may own or operate more than one retail business in one city or county.

Interestingly, Minnesota is also allowing cities or counties to own and operate a municipal cannabis store, possibly similar to the way Utah has government liquor stores which compete with private bars, breweries, wineries and distilleries.

In Summary

Minnesota is just beginning to define and establish its adult use cannabis market. Like other states before it, it is attempting to promote social equity aims at the same time as it’s working to avoid the serious problems of a competitive illegal market and an over-or-under supply of cannabis to its citizens.

With low license fees and excise taxes and a good-sized population, 420CPA believes cannabis entrepreneurs should seriously consider Minnesota for possible investment. The first cannabis retail businesses are not expected to open for another 18 months, so now is the time for businesspeople to lay the groundwork for their applications and future locations.

Cannabis cultivators across the U.S. are confronting plummeting wholesale prices and tighter profit margins. Operators in Pennsylvania say flower prices have fallen from around $4,000 a pound to around $3,000, on average, and prices in the more mature markets of California, Oregon and Colorado have experienced extreme volatility. Prices in those states are averaging around $700 per pound but of course, that’s an average. There are whispers that prices are as low as $150, revealing how bad the situation really is.

Oversaturation of legal cannabis affects commercial growers everywhere. For example, when Oklahoma opened its free-wheeling medical cannabis program with unlimited business licenses, the pipeline of cannabis from legacy markets in California was disrupted and a glut of flower from the gray market began to influence pricing within the state’s legal market. Although cannabis is not federally legal and interstate commerce is banned, what happens in one state definitely affects what happens in another.

Competition in legal markets has also increased dramatically in recent years as multistate operators expand their footprint and consolidation proliferates. Vertically integrated cultivation, manufacturing and retail is becoming unsustainable for many mom-and-pop businesses, while MSOs can leverage their cash and resources to weather the current storm.

Economic Viability Meets High Quality Production

All of this news is not necessarily negative, but it’s a definite cautionary tale: Being complacent opens opportunities for others. Growing cannabis is complex. It is working with a living and breathing machine. Some businesses fail because operators are not able to find the perfect blend of horticulture, plant science and manufacturing efficiency necessary for success. Some see it simply as a manufacturing concern, others a scientific endeavor, and still others as an artform. An understanding of growing cannabis as a blend of all three is paramount.

Just like the LED evolution, other new cultivation technology is here to stay and should not be brushed off as just experimental

Squeezing more high-quality product out of existing facilities is essential. Costs for labor and electricity are relatively fixed, so operators must turn to technology to improve yield, quality, consistency and plant health without increasing operating expenses.

Over the years, growers have often resisted change surrounding what they view as “the way” or “the best,” but with the industry in such distress, the time is now to address facility inefficiencies.

Much like the evolution of LED use, there might be an initial skepticism at the cost and real value of new cultivation technology, but the economics are too compelling to ignore. The majority of all indoor grows now use LED. The progression from single-ended bulbs, to double-ended HPS, to LED is analogous to plants on the floor of a grow facility, to rolltop benches, and now to vertical farming using racks.

Vertical Cultivation Science

Crop steering applies plant science directly to commercial production. The methodology is based on the idea that plants can be manipulated to grow and perform a certain way. For cannabis plants, the science really comes into play with inter-canopy airflow.

When airflow occurs under the surface of the leaf of the plant, the stomata opens and gas exchange increases as water vapor and oxygen are released and carbon dioxide is absorbed. The micro-barrier of air trapped against the leaves is broken and the exchange of gasses and energy in the cultivation environment is improved, enabling the entire grow to increase its yield. And while CO2 supplementation is widely used and has been for years with positive effect, the under-canopy airflow provides greater efficiency relative to the operating expense of pumping CO2 into the grow room. Money can be saved by applying science to encourage the plant to uptake the extra CO2 that has been naturally released.

Proper Drainage Is Also Key

Controlling the space with proper drainage will keep a host of problems at bay

Drainage issues like the puddling of water in vertical farming are detrimental to the efficiency of a cultivation facility. Even when growers use precision irrigation techniques to give the plants pinpointed irrigation volumes over different time periods, rack systems can still suffer from drainage issues. That means that affected plants are not receiving the precision irrigation strategy and the entire purpose of the scientific application is defeated.

Precise drainage is critical because standing water opens the door to root born disease, pests, and microbial issues. Spray regimes can address this problem, but they cost money. The key is to reduce dependency on mitigation efforts by better controlling the agricultural space and improving outcomes with a scientifically approached plan.

Greenhouses, warehouses and vertical farming facilities all have potential environmental issues that reduce their economic viability, but with proper vertical air movement, drainage equipment and an understanding of microclimates and how to address them scientifically, efficiency and product quality are enhanced.

Time to Embrace Change

As with any industry, there is resistance to adopting new technology in cannabis cultivation. The original and legacy players will always claim they know how to best grow their plants, but the reality is that the business needs must be addressed.

As canopies increase within a facility, advancements like robotics, LEDs and advanced airflow technology define how the industry operates and continues to improve. Efficiency keeps business alive—cannabis growers must continually assess their operations and make the capital investments that will pay off as wholesale prices continue to decline.

In the cannabis industry, it’s crucial to be able to predict the future, to adapt and survive in a competitive industry that is arguably regulated more closely than any other.

From licensing to buildout, there are a growing number of barriers to entering the cannabis industry as a cultivator. Those who are lucky to successfully establish a grow operation are well aware that one of the crucial hurdles is managing space to maximize facility efficiency and capacity.

To stay profitable, the more plants you can grow and harvest at a time in a continuous cycle, the better. From an economic and environmental perspective, managing cost, space and time comes down to automation and efficiencies. One of the most efficient ways we optimize is through the practice of vertical farming.

Vertical farming maximizes canopy square footage while minimizing Cost of Goods Sold (COGs) to produce high-quality cannabis at scale year-round, and the industry is slowly finding that this method is an incredibly efficient and profitable way to maximize cannabis output.

Yellow Dream Farm is our family-owned cannabis cultivation, manufacturing and distribution company based in San Bernardino County, California, often known as the Silicon Valley of cannabis. Our craft, boutique-style cannabis is grown from floor to ceiling in the 30,000-square-foot facility. We’re using cutting-edge technology that’s only come to market in the last five years and using a variety of sustainable practices. With environmental and feeding efficiencies, we’re able to harvest 300 pounds per week when compared to 150 pounds per week from a facility of the same size.

Vertical Farming for Space Optimization

Like any medical field, cannabis has seen large numbers of outside investments into the space, bringing ideologies and efficiencies from other time-tested industries. One such efficiency is vertical farming – a practice already seen in large-scale agriculture.

The Yellow Dream Farm vertical cultivation facility

We choose vertical farming to maximize our canopy square footage and minimize COGs to produce high-quality cannabis at scale. The barrier to entry into the cannabis industry is expensive, and you must utilize every square inch to stay profitable. We believe vertical farming is the most efficient and most profitable way to maximize output and our numbers can back that up; for example, we can produce double the amount of flower than the average single-tier room with the same square footage, without doubling the cost.

Our rooms contain double stacks to double room capacity by using ceiling heights instead of square footage. Even though vertical farming has larger start-up costs, we can maximize square footage and output, allowing us to get a better and faster ROI. Vertical farming can be done in many different ways but the way we built our facility was always with a sustainable outlook. We also look to improve and remove human error; with full irrigation control and crop steering technologies, we can recalibrate sensors, irrigation media and environmental sensors when needed based on successes, challenges or environmental constraints. Additionally, we have a few other sustainable practices that make a difference.

Water Conservation, Lighting and Automation

Being a California-based grower, water conservation is a key part of our operations. With San Bernardino County being located in the heart of the high desert, conserving water is not only a requirement but a competitive advantage. Our practices provide cost savings which we then pass along to our customers. Each cannabis plant on average requires between a half gallon and one gallon of water per day, which we then recirculate through condensate water from our A/C and dehumidifiers. All runoff nutrient water is re-filtered and reused to get the most out of our nutrients before discarding waste. Our freezer panel walls hold temperatures at consistent rates, and we have a fully automated system to dial in specific needs at any given time.

LED lights above a crop at Yellow Dream Farm

Lighting is another major environmental and capital cost. Our primary lighting system is LED technology, and we use LED spectrums to find which spectrum benefits the plant most. With LEDs, our energy consumption is 30 percent less.

Vertical Farming Is the Future of Cannabis and Agriculture

Vertical farming has been hailed as the future of many agricultural industries and cannabis is no different. We already see large vertical farms in most legal states, but surprisingly it’s still not a common style of growing. As the price per pound steadily declines in California, being able to keep COGs down will allow vertical farmers to sustain and thrive in this volatile industry.

In order to adapt, grow and leave a positive mark on the industry, we must pave the way for new styles of growing and utilizing new technology and science that was not available to growers in the past. We can use these advanced new technologies to make real-time changes to each sector of our facility and optimize both people power, and energy efficiency. And most importantly, we’ll be able to produce top-quality cannabis for adults to enjoy at affordable prices.

As an experiential marketer that works with a lot of vice-oriented brands, I’ve always been fascinated by the story of the rise of spirits in the US – a history marked by ingenuity in the face of heavy restrictions, clashing social norms, crime and political ideals. Since then, those same qualities have emerged in the story of cannabis and how, against all odds, it has recently begun to push its way into the mainstream. But on the path to legalization, cannabis can also learn a lot from the spirits industry about what not to do.

For example, when laws governing the spirits industry were written in the post-Prohibition 1930s, the federal government wanted to create an equitable landscape. So, they created a 3-tier system – manufacturers or importers must sell to wholesalers, wholesalers must then sell to retailers and retailers sell to us. They figured that keeping manufacturing interests separate from wholesale and retail interests would keep any large company from owning an entire supply chain, muscling out smaller competitors.

In theory, it’s not a bad idea. Imagine the consequences of massive companies like Diageo or AB InBev using their money to pay bars and liquor stores to only stock their brands and not competitors. Add on the Tied House Laws, which basically says an entity in one of the three categories cannot have an ownership stake in any of the others, and you get a seemingly even-handed marketplace.

Tied House Laws theoretically limit one entity from monopolizing a supply chain

In truth, it makes it almost impossible to be disruptive or for new brands to break through. Other industries have innovated by cutting out the middleman and selling direct-to-consumer – something that simply cannot happen in alcohol (minus the wineries and distilleries that can sell direct out of their tasting rooms). Also, now distributors are so consolidated that there are only one or two big distribution companies in each state. So, as a company trying to bring a new product to market, you have to get into one of these highly selective and competitive distributors if you are going to be successful – a challenging ask for a small, independent brand.

Protection racket

Now, imagine that same challenge coming to the cannabis space. With legalization around the corner, the adult use (as opposed to medical use) cannabis industry could easily look like alcohol in the rules that will be set up.

The demand for high quality cannabis continues to increase, but the prices need to level out to stave off the black market.

Right now, adult use manufacturers can sell their products to dispensaries directly. Some use a distributor, but there is no nationwide mandate to – which is probably for the best. If a distributor isn’t a requirement, it forces brands to offer something new to differentiate themselves. It will spark innovation, rather than add an extra profit margin that will get rolled into the final price – a price that is already higher than it should be due to the murky federal legal status. Adding complexity and cost will only make it harder to compete with the illicit market. For the industry to grow, costs for illicit cannabis can’t be lower than its legal counterpart.

Of course, we are in the nascent stages of legalization here and we’ve come a long way culturally and technologically since the 30s. But remember, the rules governing alcohol were written nearly 100 years ago along with the passage of the 21st amendment repealing prohibition. Startlingly, those laws haven’t changed that much since they were written, so any mistakes made now in dealing with the cannabis industry could last for a long time.

A new way forward

What the cannabis industry needs is a new model for the adult use/recreational space, keeping some of what exists in the alcohol industry but without ever mandating use of a distributor – the middle tier. This would mean keeping Tied House Laws in place and applying them to cannabis so that a manufacturer could never hold an interest in a retailer, while still allowing them to sell directly to dispensaries and to consumers. Currently, some states allow for vertical integration, which would change under Tied House Laws.

This should be pretty simple, since most states are already separating licenses by type of activity (manufacturer, retailer, etc.) and it would promote competition while bringing the widest array of products possible to each consumer. Also, it would prevent any behemoths from squeezing out the up and comers.

Constant innovation is a hallmark of the cannabis market and a key factor in continuous growth.

Of course, some retail license allowances could be considered on a case-by-case basis. For example, I would carve out an exception that growers/manufacturers could sell direct to consumers through a single “tasting room” at their brand home. This is similar to the operations of microbreweries, distilleries and wineries. It would encourage education for consumers, and provide great opportunities for brands to show why their products are better or unique.

Given the technology and logistics solutions available to businesses in a 21st century economy, mandated distributors create a sometimes-unnecessary barrier to an already efficient supply chain. If mandated, prices will inflate to cover added margin, thus making it harder to bring consumers over from the legacy market to the legal one. I’m not against the idea of a distributor – they can add tremendous value, but the mandate would seriously curtail industry growth.

Direct-to-retail and direct-to-consumer sales are necessary for the economic health and growth of the industry. Without this, using alcohol as a cautionary tale, at some point the middle tier cannabis brands will inevitably begin to wield an outsized amount of power. We are living at a time where innovation is going to be the key to explosive growth in the cannabis industry, so it’s important to do everything possible to let the market find its way without falling into a century-old trap.

By Gregory S. Kaufman, Jessica R. Rodgers No Comments

With the signing of the Cannabis Control Act (the Act) on April 21, 2021, Virginia became the first southern state to legalize adult use cannabis and just the fourth state to do so through the legislature. Legalizing adult use cannabis through the legislature, as opposed to through the ballot box, is not the typical route states have followed up to now. Eleven of the sixteen states and the District of Columbia have legalized adult use cannabis through the use of ballot measures. Virginia joins Vermont, Illinois, New York and New Mexico (which legalized after Virginia) as one of the few states that have gone the legislative route. Under Governor Northam’s administration, the path to legalization was swift, taking less than four months from introduction to passage.

Governor Northam added amendments to the already passed Senate Bill 1406 and the General Assembly voted to approve those amendments, with the Lieutenant Governor breaking the tie in the Senate’s vote. Upon signing, Governor Northam called the law a step towards “building a more equitable and just Virginia and reforming our criminal justice system to make it more fair.” This message and the opportunities to promote social equity through a legal cannabis industry have been consistent points of advocacy made by supporters as the bill advanced to becoming law.

Prior to the Governor’s amendments, the Act under consideration set July 1, 2024 as the date on which both legal possession and adult use sales would begin. The Governor decided to accelerate the date for legal possession to July 1 of this year, a decision believed to have been influenced by data showing that Black Virginians were more than three times as likely to be cited for possession, even after simple possession was decriminalized in the state a year prior. The regulated adult use market is still set to begin making sales on July 1, 2024; however, it remains possible that this date could be advanced through the legislature in the meantime. Nevertheless, Virginia is on track to becoming the first southern state with an operating regulated commercial cannabis market.

Creating an Administrative Structure for the Adult Use Program

Virginia became the first state in the South to legalize adult use cannabis

This sweeping fifty-page law creates the Cannabis Control Authority to regulate the cultivation, manufacture, wholesale and retail sale of cannabis and cannabis product. The Act further lays the groundwork for licensing market participants and regulating appropriate use of cannabis; defining local control; testing, labeling, packaging and advertising of cannabis and cannabis products; and taxation. The Act also contains changes to the criminal laws of the Commonwealth. Companion to the Act are new laws addressing the testing, labeling and packaging of smokable hemp products and manufacturing of edible cannabis products. Additionally, the Cannabis Equity Reinvestment Board was created to address the impact of economic divestment, violence and criminal justice responses to community and individual needs through scholarships and grants.

While persons 21 years or older may possess up to one ounce of cannabis and cultivate up to four plants for personal use per household beginning on July 1, 2021, there are a host of regulations to be written in order to regulate the adult use market. These regulations will be the devil in the details of how the regulated market will work. Regardless, the Cannabis Control Act does establish the framework for adult use cannabis that is unique to Virginia and designed to promote and encourage participation from people and communities disproportionately impacted by cannabis prohibition and enforcement.

The Cannabis Control Authority (CCA) will consist of a Board of Directors, the Cannabis Public Health Advisory Council, the Chief Executive Officer and employees. The Board will have five members appointed by the Governor and confirmed by the legislature, each with the possibility of serving two consecutive five-year terms. The Board is tasked with creating and enforcing regulations under which retail cannabis and cannabis products are possessed, sold, transported, distributed, and delivered. It is expected that the Board will begin discussing regulations next year and that applications for licenses for cannabis cultivation facilities, manufacturing facilities, cannabis testing facilities, wholesalers, and retail stores will begin to be accepted in 2023. Importantly, a Business Equity and Diversity Support Team, led by a Social Equity Liaison, and the Equity Reinvestment Board, led by the Director of Diversity, Equity and Inclusion, are to contribute to a plan to promote and encourage participation in the industry by people from disproportionately impacted communities.

Regulating Participation in the Market

The Act empowers the Board to establish a robust and diverse marketplace with many entry opportunities for market participants. Up to 450 cultivation licenses, 60 manufacturing licenses for the production of retail cannabis products, 25 wholesaler licenses and 400 licenses for retail stores can be granted. These numbers do not include the four permits granted to pharmaceutical processors (entities that cultivate and dispense medical cannabis) under the Commonwealth’s medical program.

Virginia Governor Ralph Northam Image: Craig, Flickr

In addition to the sheer number of licenses that can be granted, the Act devises a unique approach to addressing concerns of a concentration of licenses in too few hands and a market dominated by large multi-state operators. At the same time, it sets up a mechanism to capitalize two cannabis equity funds intended to benefit persons, families and communities historically and disproportionately targeted and affected by drug enforcement through grants, scholarships and loans. Over-concentration and market dominance concerns are addressed by limiting a person to holding an equity interest in no more than one cultivation, manufacturing, wholesaler, retail or testing facility license. This eliminates the ability of companies to be vertically integrated from cultivation through retail sales operations. However, there are two exceptions to the impediment to vertical integration. First, the Board is authorized to develop regulations that permit small businesses to be vertically integrated and ensure that all licensees have an equal and meaningful opportunity to participate in the market. These regulations will be closely scrutinized by those looking to enter Virginia’s regulated market once they are proposed. Qualifying small businesses could benefit substantially from the economic advantages commensurate with being vertically integrated, assuming they have the access to the capital needed to achieve integration and operate successfully. The second exception allows permitted pharmaceutical processors and registered industrial hemp processors to hold multiple licenses if they pay $1 million to the Board (to be allocated to job training, the equity loan fund or equity reinvestment fund) and submit a diversity, equity and inclusion plan for approval and implementation. Consequently, Virginia is attempting to fund, in part, its ambitious social equity programs by monetizing the opportunity for these processors to participate vertically in the adult use market.

Those devilish details of how this market will function, and how onerous compliance obligations will be, will emanate from those yet to be proposed regulations covering many areas and subject matters including:

Outdoor cultivation by cultivation facilities;

Security requirements;

Sanitary standards;

A testing program;

An application process;

Packaging and labeling requirements;

Maximum THC level for retail products (not to exceed 5 mg per serving or 50 mg per package for edible products);

Record retention requirements;

Criteria for evaluating social equity license applications based on certain ownership standards;

Licensing preferences for qualified social equity applicants;

Low interest loan program standards;

Personal cultivation guidelines; and

Outdoor advertising restrictions.

Needless to say, the CCA Board has a lot work ahead in order to issue reasonable regulations that will carry out the dictates in the Act and encourage the development of a well-functioning marketplace delivering meaningful social equity opportunities.

Much work needs to be done before July 1, 2024 to prepare for its debutThe application process for the five categories of licenses will be developed by the Board, along with application fee and annual license fee amounts. It is not clear how substantial these fees will be and what effect they will have on the ability of less-well-capitalized companies and individuals to compete in the market. The Act dictates that licenses are deemed nontransferable from person to person or location to location. However, it is not entirely clear that changes in ownership will be prohibited. The Act contemplates that changes in ownership will be permitted, at least as to retail store licensees, through a reapplication process. Perhaps the forthcoming regulations will add clarity to the transferability of licenses and address the use of management services agreements as a potential workaround to the limitations in license ownership.

Certain requirements particular to certain license-types are worthy of highlighting. For example, there are two classes of cultivation licenses. Class A cultivation licenses authorize cultivation of a certain number of plants within a certain number of square feet to be determined by the Board. Interestingly, Class B licenses are for cultivation of low total THC (no more than 1%) cannabis. Several requirements specific to retail stores are noteworthy. Stores cannot exceed 1,500 square feet, or make sales through drive-through windows, internet-based sales platforms or delivery services. Prohibitive local ordinances are not allowed; however, localities can petition for a referendum on the question of whether retail stores should be prohibited in their locality. Retail stores are allowed to sell immature plants and seek to support the home growers, an allowance that is fairly unique among the existing legal adult-use states.

Taxing Cannabis Sales

Given the perception that regulated cannabis markets add to state coffers, it is little surprise that Virginia’s retail market will be subject to significant taxes. The taxing system is straightforward and not complicated by a taxing regime related to product weight or THC content, for example. There is a 21% tax on retail sales by stores, in addition to the current sales tax rates. In addition, localities may, by ordinance, impose a 3% tax on retail sales. These taxes could result in a retail tax of approximately 30%.

Changes to Criminal Laws

Changes to the criminality of cannabis will have long lasting effects for many Virginians. These changes include:

Fines of no more than $25 and participation in substance abuse or education programs for illegal purchases by juveniles or persons 18 years or older;

Prohibition of warrantless searches based solely on the odor of cannabis;

Automatic expungement of records for certain former cannabis offenses;

Prohibition of “gifting” cannabis in exchange for nominal purchases of some other product;

Prohibition of consuming cannabis or cannabis products in public; and

Prohibition of consumption by drivers or passengers in a motor vehicle being driven, with consumption being presumed if cannabis in the passenger compartment is not in the original sealed manufacturer’s container.

These changes, and others, represent a balancing of public safety with lessons learned from the effects of the war on drugs.

Potpourri

The Act contains myriad other noteworthy provisions. For example, the Board must develop, implement and maintain a seed-to-sale tracking system for the industry. Plants being grown at home must be tagged with the grower’s name and driver’s license or state ID number. Licenses may be stripped from businesses that do not remain neutral while workers attempt to unionize. However, this provision will not become effective unless approved again by the legislature next year. Banks and credit unions are protected under state law for providing financial services to licensed businesses or for investing any income derived from the providing of such services. This provision is intended to address the lack of access to banking for cannabis businesses due to the federal illegality of cannabis by removing any perceived state law barriers for banks and credit unions to do business with licensed cannabis companies.

The adult use cannabis industry is coming to Virginia. Much work needs to be done before July 1, 2024 to prepare for its debut. However, the criminal justice reforms and commitment to repairing harms related to past prohibition of cannabis are soon to be a present-day reality. Virginia is the first Southern state to take the path towards legal adult use cannabis. It is unlikely to be the last.

At Raw Garden, we have a ‘Farming First’ philosophy because we understand that the process of farming is the process of managing the plant’s life and the management of the land those plants grow on – this is when the plantgets its chance to thrive but requires that it is properly nurtured in order to provide resources such as high-quality terpenes and cannabinoids.

Our cannabis plants are sun-grown in Santa Barbara county soil just like other California crops. From the seed to the shelf, we are vertically integrated and maintain quality control at every step in the process. We grow our own seeds, farm and harvest our own plants, and process our own products while employing sustainable and regenerative farming practices – only organic and natural fertilizers, soil amendments and pest control methods are used on thefarm.

As farmers we have a responsibility to care for the land and the soil to ensure it is fertile and healthy well into the future. We take care of the soil and it takes care of our plants. The result is premium quality products that our customers love and trust. Our success and commitment to quality is proof that the economics of clean, sustainable operations are achievable. We’re farmers and scientists on a mission to make clean, high quality cannabis that is affordable and accessible.

A few of the sustainable agriculture practices we employ at Raw Garden include:

The Clean Green Certified logo

Clean Green Certification – Since our inception, we have been certified and licensed members of Clean Green, the #1 globally-recognized organic and sustainable cannabis certification program. The program was created in 2004 as a way to standardize legal cannabis products and the result was a program to help farms and brands obtain organic-like certification based on the USDA National Organic program. Clean Green-certified growers and processors regularly win awards for their high-quality products, including our award-winning extracts.

Water Conservation – Our farm team waters at the right time of day to reduce evaporative water loss; we also use drip irrigation and mulch to reduce water waste and runoff. Last year, we used about 8,000 gallons of water per acre on average, which is significantly less than standard outdoor grown crops.

Natural Fertilizer and Pest Control – We apply only organic fertilizers and foliar feeds and we spray only organic pathogen-free inoculants to keep our plants healthy and disease-free, which consistently results in high yields. To naturally deter pests, we recruit beneficial predatory insects like ladybugs and parasitic wasps, in addition to botanical oils and diatomaceous earth.

Precision Agriculture (PA) and Site-Specific Crop Management (SSCM) – We utilize technology to manage crops and increase farm efficiency, such as machine learning for fertilizer optimization and digital sensors in the field to monitor crops.

Author Khalid Al-Naser next at Raw Garden’s farm. Image by Brian Walker

Soil Health and Terroir – Like grapes for wine, cannabis plants grown in the soil have terroir that affects the flower’s qualities, characteristics, terpene profile, aroma and taste, based on temperature, climate, soil composition and topography, as well as other environmental influences. Micro-climates matter – the same strain of cannabis grown along the coast likely has a different taste and potency than one grown inland. We grow in Santa Barbara wine country for the combination of fertile soil, hot sun, and cool nights which yield an incredibly diverse, potent and flavorful crop of cannabis flowers. Between growing seasons, we employ regenerative agriculture by planting cover crops including oat, beans, peas and buckwheat to add nitrogen and organic matter naturally back in the soil. This method of cover crops also helps reduce pests and soil-borne diseases in preparation for the next growing season. We know that an ideal environment in combination with healthy soil and good land management results in healthier, more vigorous plants, which translates to higher-quality products.

As farmers, it is our responsibility to care of the land with good management decisions today so that we grow the best quality products while better preserving the land for the future. It takes careful planning, knowledge of the land, a commitment to sustainable practices and a desire to put farming first.

Update: On April 21, 2021, Virginia Governor Ralph Northam signed the legislation into law, making Virginia the first state int he American South to legalize adult use cannabis.

On April 7, 2021, legislators in Virginia finally came to an agreement for their adult use cannabis legalization plan. Back in February of this year, lawmakers passed a bill to legalize adult use cannabis with a launch date of 2024, but Governor Ralph Northam wanted to move quicker than that.

Virginia Governor Ralph Northam Image: Craig, Flickr

Last week, Gov. Northam issued a number of amendments to the legalization bills (Senate Bill 1406 and House Bill 2312) that essentially tapers the time frame of legalization to July of this year. With the legislature approving those amendments yesterday, the state of Virginia has now finalized their legalization plans, setting in motion the launch of the very first legal adult use cannabis market in the American South.

Beginning July 1, 2021, Virginia will allow adults to possess up to an ounce of cannabis and up to four plants per household. The commercial cannabis market, and the regulatory framework accompanying it, will be set to legalize sales July 1, 2024.

The bill establishes the Virginia Cannabis Control Authority as the regulatory body overseeing the legal cannabis market. A five-member Board of Directors in that agency will develop and issue regulations and licenses. According to the bill, the Board can set the number of licenses, with a maximum of 400 retailers, 25 wholesalers, 450 cultivators and 60 manufacturers, aside from any medical cannabis and hemp processing license already issued. The Board is also in charge of licensing testing labs.

Vertical integration is not permitted under Virginia’s new legalization plan, but all of the medical cannabis licensees in the state are already vertically integrated. According to the bill, they can keep their vertical integration for a small fee of $1 million and after they submit a diversity, equity and inclusion plan.

In addition to Virginia’s normal 6% sales tax, a state tax of 21% is added to retail sales of adult use cannabis, excluding medical dispensaries. Local municipalities are allowed to issue up to 3% in additional taxes.

The cannabis industry saw close to $15.5B in deals across VC, private equity, M&A and IPOs in 2020 according to PitchBook data. Early and growth stage capital has been a key enabler in deal activity as companies seek to innovate and scale, taking advantage of trends towards national legalization and consolidation. Entourage Effect Capital is one of the largest VC firms in cannabis with over $150MM deployed since its inception in 2014. Some of their notable investments include GTI, CANN, Harborside (CNQ: HBOR), Acreage Holdings, Ebbu, TerrAscend and Sunderstorm.

We spoke with Matt Hawkins, co-founder and managing partner at Entourage Effect Capital. Matt started Entourage in 2014 after exiting his previous company. He has 20+ years of private equity experience and serves on the Boards of numerous cannabis companies. Matt’s thought leadership has been on Fox Business in the past and he has also recently featured on CNBC, Bloomberg, Yahoo! Finance, Cheddar and more.

Aaron Green: How did you get involved in the cannabis industry?

Matt Hawkins: We’ve been making investments in the cannabis industry since 2014. We’ve made 65 investments to date. We have a full team of investment professionals, and we invest up and down the value chain of the industry.

I had been in private equity for 25 years and I kind of just fell into the industry after I’d had an exit. I started lending to warehouse owners in Denver that were looking to refinance their mortgages out of commercial debt into private debt, which would then give them the ability to lease their facilities to growers. I realized there would be a significant opportunity to place capital in the private equity side of the cannabis business. So, I just started raising money for that project and I haven’t looked back. It’s been a great run and we’ve built a fantastic portfolio. We look forward to continuing to deploy capital up to and through legalization.

Green: Do you consider Entourage Effect Capital a VC fund or private equity firm? How do you talk about yourself?

Hawkins: In the early stages of the industry, we were more purely venture capital because there was hardly any revenue. We’re probably still considered a venture capital firm, by definition, just because of the risk factors. As the industry has matured, the investments we make are going to be larger. The reality is that the checks we write now will go to companies that have a track record of not only 12 months of revenue, but EBITDA as well. We can calculate a multiple on those, and that makes it more like lower/middle-market private equity investing.

Green: What’s your investment mandate?

Matt Hawkins, Co-Founder and Managing Partner at Entourage Effect Capital

Hawkins: From here forward our mandate is to build scale in as many verticals as we can ahead of legalization. In the early days, we were focused on giving high net worth individuals and family offices access to the industry using a very diversified approach, meaning we invested up and down the value chain. We’ll continue to do that, but now we’re going to be really laser focused on combining companies and building scale within companies to where they’re going to be more attractive for exit partners upon legalization.

Green: Are there any particular segments of the industry that you focus on whether it’s cultivation, extraction or MSOs?

Hawkins: We tend to focus on everything above cultivation. We feel like cultivation by itself is a commodity, but when vertically integrated, for example with a single-state operator or multi-state operator, that makes it intrinsically more valuable. When you look at the value chain, right after cultivation is where we start to get involved.

Green: Are you also doing investments in tech and e-commerce?

Hawkins: We’ve made some investments in supply chain, management software, ERP solutions, things like that. We’re not really focused on e-commerce with the exception of the only CBD company we are invested in.

Green: How does Entourage’s investment philosophy differ from other VC and private equity firms in cannabis?

Hawkins: We really don’t pay attention to other people’s philosophies. We have co-invested with others in the past and will continue to do so. There’s not a lot of us in the industry, so it’s good that we all work together. Until legalization occurs, or institutional capital comes into play, we’re really the only game in town. So, it behooves us all to have good working relationships.

Green: Across the states, there’s a variety of markets in various stages of development. Do you tend to prefer investing in more sophisticated markets? Say California or Colorado where they’ve been legalized for longer, or are you looking more at new growth opportunities like New York and New Jersey?

Hawkins: Historically, we’ve focused on the most populous states. California is obviously where we’ve placed a lot of bets going forward. We’ll continue to build out our portfolio in California, but we will also exploit the other large population states like New Jersey, New York, Arizona, Massachusetts, Michigan, Ohio and Illinois. All of those are big targets for us.

Green: Do you think legalization will happen this Congress?

Hawkins: My personal opinion is that it will not happen this year. It could be the latter part of next year or the year after. I think there’s just too much wood to chop. I was encouraged to see the SAFE Banking Act reappear. I think that will hopefully encourage institutional capital to take another look at the game, especially with the NASDAQ and the New York Stock Exchange open up. So that’s a positive.

I think with the election of President Biden and with the Senate runoffs in Georgia going Democrat, the timeline to legalization has sped up, but I don’t think it’s an overnight situation. I certainly don’t think it’ll be easy to start crossing state lines immediately, either.

Green: Can you explain more about your thoughts on interstate commerce?

Hawkins: I think it’s pretty simple. The states don’t want to give up all the tax revenue that they get from their cultivation companies that are in the state. For example, if you allow Mexico and Colombia to start importing product, we can’t compete with that cost structure. States that are neighbors to California, but need to grow indoors which is more expensive, are not going to want to lose their tax revenues either. So, I just think there’s going to be a lot of butting heads at the state level.

The federal government is going to have to outline what the tax implications will be, because at the end of the day the industry is currently taxed as high as it ever will be or should be. Anything North of current tax levels will prohibit businesses from thriving further, effectively meaning not being able to tamp down the illicit market. One of the biggest goals of legalization in my opinion should be reducing the tax burden on the companies and thereby allowing them to be able to compete more directly with the illicit market, which obviously has all the benefits of reduced crime, etc.

Green: Do you foresee 280E changes coming in the future?

Hawkins: For sure. If the federal illegality veil is removed – which means there’ll be some type of rescheduling – cannabis would be removed from the 280E category. I think 280E by definition is about just illegal drugs and manufacturing and selling of that. As long as cannabis isn’t part of that, then it won’t be subject to it.

Green: What have been some of the winners in your portfolio in terms of successful exits?

Hawkins: When the CSC started allowing companies in Canada to own U.S. assets, the whole landscape changed. We were fortunate to be early investors in Acreage and companies that sold to Curaleaf and GTI before they were public. We are big investors in TerrAscend. We were early investors in Ebbu which sold to Canopy Growth. Those were huge wins for us in Fund I. We also have some interesting plays in Fund II that are on the precipice of having similar-type exits.

You read about the big ones, but at the end of the day, the ones that kind of fall under the radar – the private deals – actually have even greater multiples than what we see on some of the public M&A activity.

Green: Governor Cuomo has been hinting recently at being “very close” on a deal for opening up the cannabis market in New York. What do you think are the biggest opportunities in New York right now?

Hawkins: If it can get done, that’s great. I’m just concerned that distractions in the state house right now in New York may get in the way of progress there. But if it doesn’t, and it is able to come to fruition, then there isn’t a sector that doesn’t have a chance to thrive and thrive extremely well in the state of New York.

Green: Looking at other markets, Curaleaf recently announced a big investment in Europe. How do you look at Europe in general as an investment opportunity?

Hawkins: We have a pretty interesting play in Europe right now through a company called Relief Europe. It’s poised to be one of the first entrants to Germany. We think it could be a big win for us. But let’s face it, Europe is still a little behind, in fact, a lot behind the United States in terms of where they are as an industry. Most of the capital that we’re going to be deploying is going to be done domestically in advance of legalization.

Green: What industry trends are you seeing in the year ahead?“We’re constantly learning from other industries that are steps ahead of us to figure out how to use those lessons as we continue to invest in cannabis.”

Hawkins: Well, I think you’ll see a lot of consolidation and a lot of ramping up in advance of legalization. I think that’s going to apply in all sectors. I just don’t see a scenario wherein mom and pops or smaller players are going to be successful exit partners with some of the new capital that’s coming in. They’re going to have to get to a point where they’re either selling to somebody bigger than them right now or joining forces with companies around the same size as them and creating mass. That’s the only way you’re going to compete with companies coming in with billions of dollars to deploy.

Green: How do you see this shaking out?

Hawkins: That’s where you start to look into the crystal ball. It’s really difficult to say because I think until we get to where we truly have a national footprint of brands, which would require crossing state lines, it’s going be really difficult to tell where things go. I do know that liquor, tobacco, beer, the distribution companies, they all are standing in line. Big Pharma, big CPG, nutraceuticals, they all want access to this, too.

In some form or fashion, these bigger players will dictate how they want to go about attacking the market on their own. So, that part remains to be seen. We’ll just have to wait and see where this goes and how quickly it goes there.

Green: Are you looking at other geographies to deploy capital such as APAC or Latin America regions?

Hawkins: Not at this point. It’s not a focus at all. What recently transpired here in the elections just really makes us want to focus here and generate positive returns for investors.

Green: As cannabis goes more and more mainstream, federal legalization is maybe more likely. How do you think the institutional investor scene is evolving around that? And is it a good thing to bring in new capital to the cannabis market?

Hawkins: I don’t see a downside to it. Some people are saying that it could damage the collegial and cottage-like nature of the industry. At the end of the day, if you’ve got tens of billions of dollars that are waiting to pour into companies listed on the CSC and up-listing to the NASDAQ or New York Stock Exchange, that’s only going to increase their market caps and give them more cash to acquire other companies. The trickle-down effect of that will be so great to the industry that I just don’t know how you can look the other way and say we don’t want it.

Green: Last question: What’s got your attention these days? What’s the thing you’re most interested in learning about?

Hawkins: We’re constantly learning about just where this industry is headed. We’re constantly learning from other industries that are steps ahead of us to figure out how to use those lessons as we continue to invest in cannabis. We all saw the correlation between cannabis and alcohol prohibition. The reality is that the industry is mature enough now where you can see similarities to industries that have gone from infancy to their adolescent years. That’s kind of where we are now and so we spend a lot of time studying industries that have been down this path before and see what lessons we can apply here.

Green: Okay, great. So that concludes the interview!

Flower continues to be the dominant product category in US cannabis sales. In this “Flower-Side Chats” series of articles Green interviews integrated cannabis companies and flower brands that are bringing unique business models to the industry. Particular attention is focused on how these businesses navigate a rapidly changing landscape of regulatory, supply chain and consumer demand.

Connected is a vertically-integrated cannabis company based out of Sacramento, CA and one of the most sought-after brands in California and Arizona. Having formed as a legacy operation in 2009, Connected has created a cult-like following over more than a decade in business. According to BDS Analytics, Connected Cannabis and their acquired brand Alien Labs now boasts the highest wholesale flower price in any major legal market – their average indoor flower wholesale price is 2x the CA average – yet also has the highest flower retail revenue.

We spoke with Sam Ghods, CEO of Connected to learn more about his transition from tech to cannabis, how Connected thinks about product and his vision for future growth. Sam joined Connected in 2018 after getting to know the founders. Prior to Connected, Sam was a co-founder at Box where he stayed on for 3 years after their successful IPO.

Aaron Green: How did you get involved in the cannabis industry?

Sam Ghods: I originally came from the tech industry. I co-founded Box, a cloud sharing and storage company, in the mid 2000s with three other friends. We grew that from the four of us to eventually a multi-billion-dollar public offering in 2015. I stayed on a few more years after that until I took some time off trying to decide what I wanted to do next. I looked at a number of different industries and companies, but personally I always had a real passion for artisan and craft consumer goods. It’s a really big hobby of mine. Whether it’s going to Napa or learning about different kinds of premium consumer goods, I really had a deep love and never knew cannabis could be like that.

When I first met Caleb, the co-founder of Connected, he instantly got my attention by telling me that they had been selling out of their product in the volume of millions of dollars a year at more than two times what everybody else was selling for. That really piqued my interest because creating a product that has that level of consumer passion and demand is maybe the single hardest thing about building a consumer goods business. For them to have been so successful in what was a very difficult and gray market to operate in at the time – this was mid 2018 that I was speaking with him and he had been building this company since 2009 – is a really big challenge, and really impressive.

Sam Ghods, CEO of Connected

So, I started spending time with Caleb and the Connected team and learned a lot about the business. Everything I learned got me more interested and more excited. The way that they thought about the product, the way they treated it was with a reverence and level of sophistication I had no idea was possible.

I was so excited to just learn about the space. I mean, honestly, it feels like the internet in the 90’s- The sheer possibility and excitement. The only difference here is that the market already has existed for 100 years plus: the gray and underground markets for this product are actually phenomenally mature. And now we’re lifting up billions of dollars in commerce that’s already occurring and attempting to legalize all of it in one fell swoop, which creates such an interesting set of challenges.

I first got involved as an advisor on fundraising and strategy. And then a few months later, they were looking for a CEO and I joined full time as CEO in September 2018.

Aaron: What trends in the industry are you focused on?

Sam: It may seem basic, but I think product quality in the broader cannabis markets nationally and internationally is really underrated. Because of the extreme weight of the regulatory frameworks in so many different markets, it’s resulting in a lot of product being grown and sold just because it can be by the operators that are doing it. In many markets, they count the number of producers by the handful, instead of being measured in hundreds or thousands like in California or Oregon. And in that kind of environment, you’re not really having competition, and you’re not really able to see the quality that has existed in this category for years and years and years.

That’s one of the things that really sets us apart – the quality is first above all else, as well as the innovation and time that has gone into it, and not many existing brands in the legal market can say that. With some of the “premium” brands on the market, it would be comparable to just jumping into the wine industry one day and thinking that you can become a premium brand, without having any knowledge of the history of the product or the industry itself. At Connected, we have a team that’s been doing this for over a decade. We did a back of the envelope calculation: there’s over one thousand lifetime harvests between our team. We’ve also brought in specialists from Big Ag and other industries to complement that experience.

Cannabis is a very, very difficult plant to grow at a very high level. It’s much more like high-end wine or spirits than other fruit or produce. I think in the cannabis community, that’s extremely acknowledged, and appreciation for that is the reason we get by with the highest prices in the legal market. I think in the broader investor and financial community, this point hasn’t really hit home, because the limited license markets aren’t mature enough, and there isn’t enough competition in many of them.

Our focus is continuing to make the best product we can, which has fed and developed our brands [Connected and Alien Labs] into what they are today. That is our number one focus, and we think it’s pretty unique to the space of not just cultivating a great quality product, but also as far as breeding, pushing the bar higher and higher on what can be done with the genetics of the plant.

Aaron: How do you think about choosing testing labs?

Sam: So, the number one criterion is responsibility and compliance. We must be completely confident that they’re testing accurately, safely and exactly to the specifications of the state. Then from there, it is really cultivating about a partnership. There’s a lot of nuance in the relationship with a testing lab. We note things like: Are they responsive? Are they sensitive to our needs in terms of either timelines or requirements we have? It does come down to timelines and costs to a certain extent, like who’s able to deliver the best service for the best cost, but it really is a partnership where you’re working together to deliver a great product. Reliability and consistency are big pieces as well.

Aaron: Industry estimates for illicit market activities are something like 60% of the California market. From your perspective, how do we fix that?

Sam: I think it probably comes down to funding for the efforts to discontinue those activities and opening up the barrier to entry, incentivizing “illegal” operators to make the investment in the cross-over. I think the most successful attempts to tamp it down was when there were initiatives that were well-orchestrated and well-funded, allowing for legacy growers to actually cross over to the “legal” industry. You can’t launch an industry with such an extreme amount of regulation, set a miles-high barrier to entry, and then penalize legacy growers for continuing their business as-is. If the illicit market continues to be fueled by rejection, you’re not going to achieve the tax revenue that you’re expecting to see, that we all want to see. There needs to be an attitude that every dollar put into transitioning illicit markets into regulated markets is returned many times over in tax revenue to the state’s citizens.

Aaron: So, I understand you sell wholesale. Do you sell direct to consumer?“Once they hit the shelves, we blow people away again, beyond their expectations of what they had before.”

Sam: We own and operate three retail stores, so we do sell direct to our consumers, but at this point the majority of our product is sold through third party dispensaries.

Aaron: Do you make fresh frozen?

Sam: We do. On the cultivation side we have indoor, mixed light and outdoor. We fresh freeze a portion of our outdoor harvest every year, and then we use that fresh frozen for our live resin products, for example, our recent live resin cartridge. It creates a vape experience really unlike any other because we are using our regular market-ready flower, but instead we’re taking that flower and actually extracting, not just using the distillate and mixing a batch of terpenes with it. We extract the entire plant’s content across the board, from cannabinoids to terpenoids and everything in between, and then you have our live resin cartridges.

Aaron: How do you think about brand identity and leveraging the brand to command higher prices?

Sam: The cycle we’ve effectively created is that every time we do a release of a new strain or a new batch or harvest, the quality is generally going up. That quality is released under our brands, and then the customer is able to associate that increase in quality and reputation with those brands. Then for our next launch, we have an even bigger platform to talk about the products and to ship and distribute and sell the products. Once they hit the shelves, we blow people away again, beyond their expectations of what they had before. That continuous cycle keeps fortifying the brand and fortifying the product. From our perspective the brand is built 100% on the quality of the product. The product will always be our highest priority and the brand will come downstream from that.

Aaron: Tell me about Alien Labs.

Sam: Alien Labs was an acquisition. It was a company that had built their brand really successfully in the gray market through 2017 and Prop 215 in California and had an incredible level of quality, a really loyal and dedicated fan base, not to mention a tremendous Instagram presence and following, which is where 98% of cannabis marketing happens today. We really loved the spirit of what the founders were bringing to the table. In 2018, we decided basically to join forces with them and bring them on board, creating a partnership where they leverage our infrastructure and the systems and processes we’ve built, but still keep their way of cultivation and their product vision. To this day, Ted Lidie, one of the founders, continues as the lead brand director for Alien Labs.

Aaron: In what geographies do you currently operate?

Sam: Our primary offices and facilities are based out of Sacramento, California, but we have facilities throughout the state. Last year, for the first time we launched operations in a new state, Arizona. As you may know, you’re not allowed to take cannabis products across state lines at all, so if you want consistent product in multiple markets you really have no choice but to rebuild your entire infrastructure in each state you want to open up.

There are many brands that are expanding and launching in more markets more quickly, but they’re doing so by taking product that’s already existing and putting their brand name on it. That is something we’ve decided strategically that we will not do. We’ve spent years building a high level of trust with our customers, so we’re only going to put our brand name on products that are our genetics, our cultivation, our style, our quality of product. When we launched in Arizona, we did it with a facility that we leased and took over and now operate with our staff. We’re replicating the same exact product that you can get in California in Arizona, which is really exciting.

We launched just this past November, which has been incredibly successful. Our dispensary partner Harvest saw lines of dozens of people out the door.“We consider ourselves a flower company first and foremost, so for us, that was a very calculated strategic move.”

Aaron: Any new geographies on the horizon that you can talk about?

Sam: We’re constantly evaluating new opportunities. I don’t have anything particularly specific to announce right now, but I will say we look for states where we believe there’s a competitive environment where the product quality is going to really stand out and be appreciated.

Aaron: Do you notice any differences in consumer trends between California and Arizona that stand out?

Sam: Not too many yet. We don’t have a retail location in Arizona, so we don’t have as much direct contact. However, we have heard consistently that the Connected customer demographics – as you would imagine most interested in our product – are those looking for something special, unique, different and have a really superior quality to everything else out there. We ended up launching in Arizona with the highest price point for flower in the state, and we say that’s just the beginning. The market is still so young and immature, both nationally and internationally, that this category is going to develop into one that’s really taste-driven.

Aaron: What’s next in California?

Sam: Continued growth and product development. We want to keep blowing away our customers with more and more incredible products, different product types and categories. For example, the cartridges were a really big launch for us because we don’t really consider ourselves a vape company. We consider ourselves a flower company first and foremost, so for us, that was a very calculated strategic move. We were only going to launch the product if we could fully replicate what the consumer gets from the flower experience. We are very unlikely to ever release a distillate pen, for example.

Aaron: What are you personally interested in learning more about?

Sam: We, as a society, really don’t know very much about the cannabis plant. Pretty much all meaningful research around cannabis stopped in the early 1900’s with prohibition. In the meantime, we’ve performed millions of dollars of studies and research on almost every other plant that we grow commercially. We understand these plants extraordinarily well. Cannabis science is stuck back in agriculture of early 1900s. The most interesting conversations I have are around how the plant works, how it doesn’t work and the ways in which it is so different from all other plants with which we are familiar. Our head of cultivation comes from Driscolls, the largest berry company in the world, and even he is frequently surprised by the way the cannabis plant reacts to things that are commonly understood in other plants. So, the way the actual plant responds to different environments is truly fascinating and something I think we’ll be learning about for decades and decades to come.

Aaron: Okay, great. That concludes the interview. Thank you, Sam!

Part One of this series took a look at how the regulated cannabis market can only be understood in relation to the previous medical market as well as the ongoing “traditional” market. Part Two of the series describes how regulation defines vertical integration in California cannabis, and conversely, how vertical integration can address some of the problems that the regulations create. But first:

A Grain of Salt

Take the conventional wisdom about vertical integration with a grain of salt. Expected benefits may not materialize under the current circumstances:

Overall, the business environment is highly challenging due to extensive regulation, over taxation, insufficient retail capacity and competition from the “traditional” market. As a result, integrating businesses upstream or downstream may mean capturing losses, not profits.

The three major types of cannabis activity span three major industrial sectors: raw materials (i.e., cultivation), manufacturing and service (distribution, testing and retail). As a result, a vertically integrated company needs to carry out very different types of activity, which require very different types of core competencies, equipment and facilities.

Developing core competencies is especially challenging because each of the major cannabis sectors is still evolving.

Realizing the benefits of vertical integration requires an additional core competency in cross-sector operations.

Regulations Define the Supply Chain

California’s regulations define the cannabis supply chain by defining both the individual links (licensees) and the relationships between those links. Therefore, an understanding of vertical integration must be grounded in an understanding of the underlying regulatory definitions.

The regulatory definition of each link is extensive. For example, each licensee is tied to a specific facility, and must have its own procedures for production, inventory control, security, etc. When the links are strung together, this definition tends to preserve operational redundancies, and impede operational integration.

Overall, the relationships between the links are primarily defined in terms of preserving the chain of cannabis custody. On top of that, regulations define very specific (and very consequential) links between certain licenses, as discussed below.

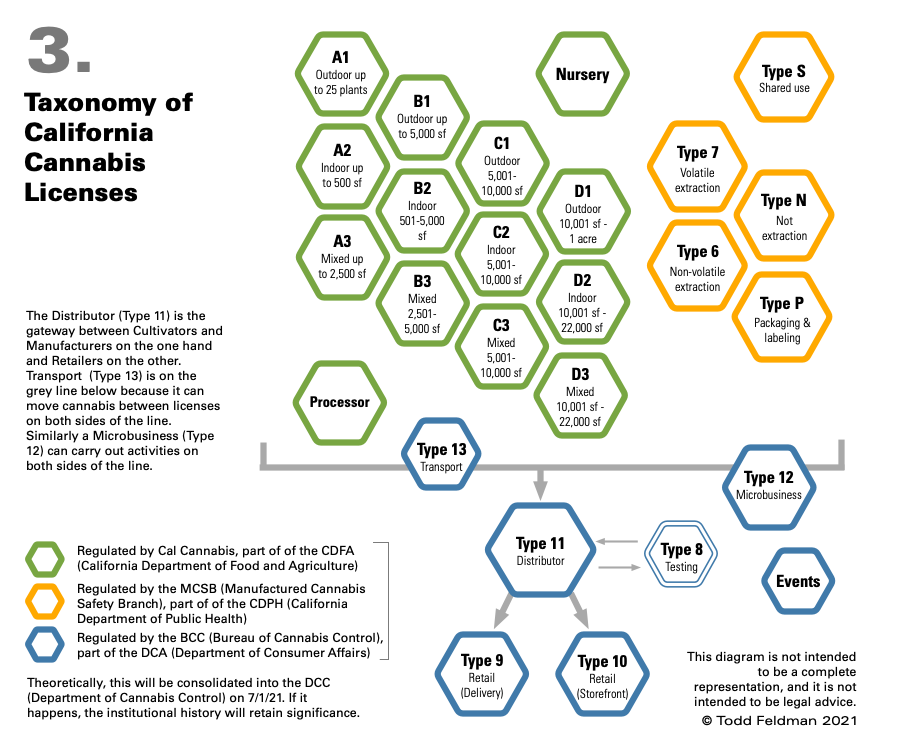

A Taxonomy of Links

There are currently 26 types of cannabis license in California, 25 of which can be vertically integrated:

Cultivation – 14 licenses, including 4 sizes each for Indoor (up to 22,0000 sf), Mixed Light (up to 22,000 sf) and Outdoor (up to 1 acre), as well as Nursery and Processor (drying, trimming and packaging/labeling). Note that cultivation licenses are the only licenses that restrict the scale of activities.

Manufacturing – 5 licenses, including volatile extraction, non-volatile extraction, everything but extraction (i.e., infusion) and packaging/labeling.

Testing (Type 8), for testing cannabis according to state standards prior to sale. The owner of a testing license cannot own any other type of license.

Distribution (Type 11), acts as the gateway between cultivation and manufacturing on the one hand, and retail on the other. The distributor’s gateway status is entirely an artifact of regulation – cannabis must be officially tested before it is sold to a consumer, and only a distributor can order the official test. All products must stay in a “quarantine” area at the distributor until they pass testing. Products that fail testing must be destroyed if they cannot be remediated.

Transport (Type 13), which can move cannabis between licensees (with a narrow exception). This license does not allow for official testing.

Delivery Retail (Type 10), for delivery services that are subject to the vagaries of software platforms and the intransigence of local authorities.

Microbusiness (Type 12), which allows the licensee to carry out cultivation (up to 10,000 square feet), non-volatile manufacturing, distribution and retail.

Event Organizer

Self-Distribution – A Case of Useful Integration

You may gather from the previous section that shoving a gratuitous and mandatory distributor into the middle of the supply chain creates problems for cultivators and manufacturers. Savvy operators solve this problem by getting a distribution license. This allows the cultivator or manufacturer to:

Pick the time and place for the testing of its cannabis products.

Avoid paying someone else for the storage of cannabis products as they await test results or purchase.

Reduce transport costs (particularly if the distributor is near the other operations).

Sell directly to retailers.

The bottom line is that vertical integration in California cannabis is useful as a means to an end, as opposed to an end in itself. Therefore, cannabis operators should carefully consider how vertical integration will benefit their core business before incurring the risks and expenses associated with an additional license.

This article is an opinion only and is not intended to be legal advice.

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

We use tracking pixels that set your arrival time at our website, this is used as part of our anti-spam and security measures. Disabling this tracking pixel would disable some of our security measures, and is therefore considered necessary for the safe operation of the website. This tracking pixel is cleared from your system when you delete files in your history.

We also use cookies to store your preferences regarding the setting of 3rd Party Cookies.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.

In a recent op-ed piece for Marijuana Moment, the New York cannabis consulting firm of Bridge West Consulting suggested three reasons, in addition to low cannabis excise taxes and reasonable license fees, why entrepreneurs should consider investing in a retail cannabis business in Minnesota:

In a recent op-ed piece for Marijuana Moment, the New York cannabis consulting firm of Bridge West Consulting suggested three reasons, in addition to low cannabis excise taxes and reasonable license fees, why entrepreneurs should consider investing in a retail cannabis business in Minnesota: Continuing its emphasis on “smaller is better,” HF100 says, “Unless the office determines that the issuance of bulk cultivator licenses is necessary to ensure a sufficient supply of cannabis flower and cannabinoid products, the office shall not issue a bulk cultivator license before July 1, 2028.”

Continuing its emphasis on “smaller is better,” HF100 says, “Unless the office determines that the issuance of bulk cultivator licenses is necessary to ensure a sufficient supply of cannabis flower and cannabinoid products, the office shall not issue a bulk cultivator license before July 1, 2028.”