By Seth Mailhot, Steve Levine, Emily Lyons, Leah Kaiser, Marshall Custer No Comments

The U.S. Food and Drug Administration (FDA) issued warning letters this month to two companies concerning the marketing and sale of over-the-counter (OTC) drug products containing cannabidiol (CBD) as an inactive ingredient. The letters allege violations of the Federal Food, Drug, and Cosmetic (FD&C) Act related to current good manufacturing practice requirements and marketing of new drugs without FDA approval.

At issue: labeling, NDAs and active ingredients

The companies subject to the warning letters market OTC drug products that contain CBD as an inactive ingredient. In the warning letters, the FDA states that it has not approved any OTC drugs containing CBD. According to the FDA, an approved new drug application (NDA) is required to legally market nonprescription or OTC drug products containing CBD, regardless of whether the CBD is an active or inactive ingredient. The FDA notes that CBD has known pharmacological effects and demonstrated risks, and that CBD has not been shown to be safe and suitable for use, even as an inactive ingredient. As a result, the FDA states that CBD cannot be marketed in OTC drug products.

Further, the warning letters noted the marketing of several CBD products that highlighted the benefits of CBD for a range of conditions in such a manner that, according to the FDA, “misleadingly suggests that [their] . . . products are approved or endorsed by FDA in some way when this is not true.” The FDA also took issue with the way products were labeled, which included callouts on the front label regarding the CBD content of the product (a requirement under most state laws that permit CBD as an ingredient). Similarly, the FDA also noted that some of the products advertised CBD as an active ingredient in a topical pain reliever product. According to the FDA, no company may legally market such a product, since there are no OTC monographs or NDAs that allow the use of CBD in an OTC drug.

What this means for you

These warning letters highlight the FDA’s vigilance regarding OTC CBD products. Regardless of whether the CBD is labeled as an active or inactive ingredient, the FDA has taken the position that nonprescription CBD drugs are in violation of the FD&C Act. Companies marketing CBD products should be careful to ensure their marketing practices, as well as their product formulations, do not present a heightened risk of FDA enforcement.

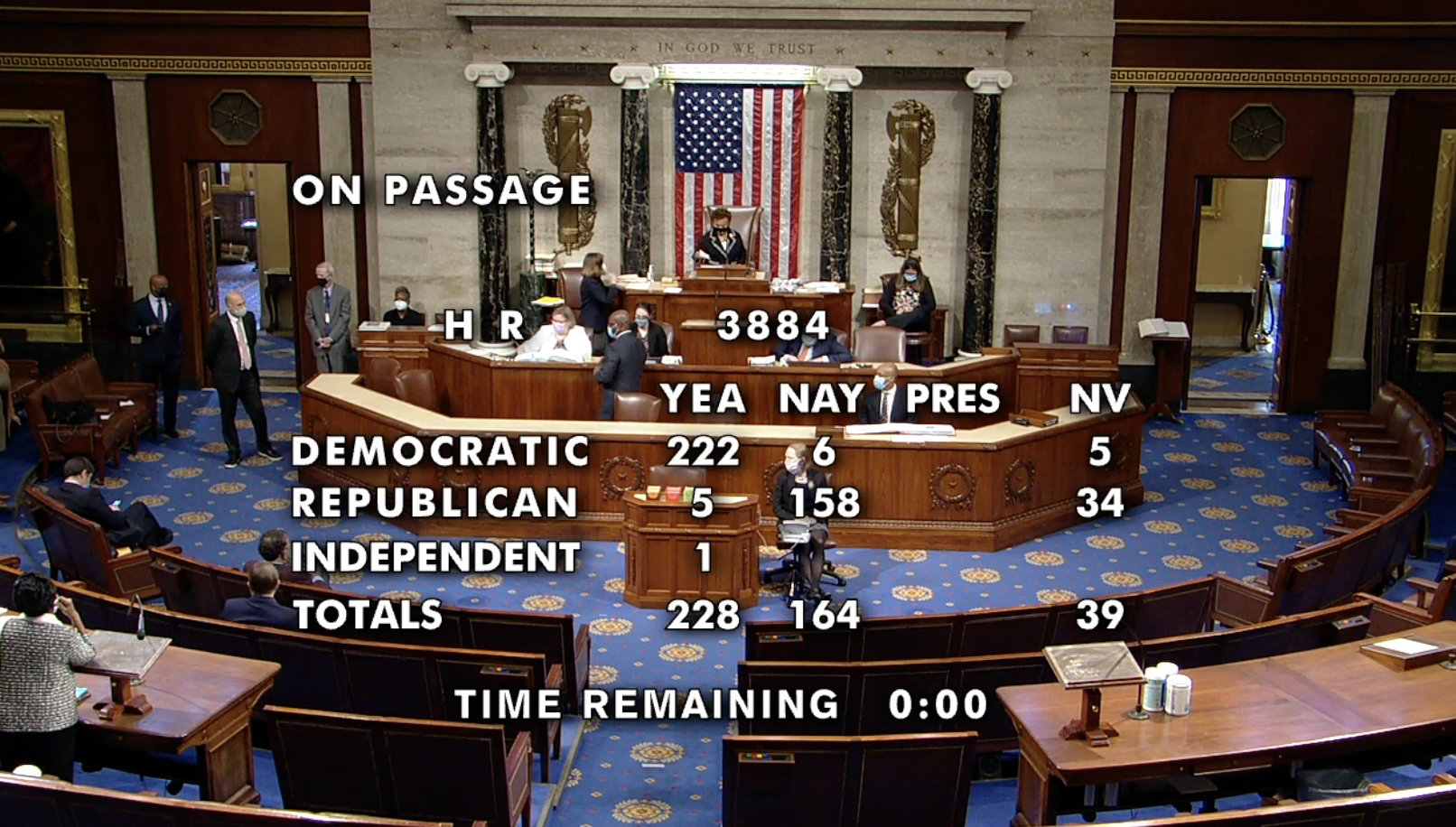

On Friday, December 4, 2020, the US House of Representatives passed the Marijuana Opportunity Reinvestment and Expungement Act of 2019 (the MORE Act), which would effectively legalize cannabis by removing it from the Controlled Substances Act. The bill (H.R. 3884) has several key components:

Most importantly, the bill would remove cannabis from the list of controlled substances in the Controlled Substances Act, as well as other federal legislation such as the National Forest System Drug Control Act of 1986. This would effectively end many of the obstacles created by the federal illegality of cannabis such as the lack of access to banking, tax consequences such as 280E, adverse immigration impacts and threats of federal criminal enforcement.

Rep. Earl Blumenauer (D-OR) donning his cannabis mask as he presides over the Congress

Second, not only does the bill preclude future prosecution for cannabis-related crimes, the bill is designed to be retroactive and would provide for the expungement of past non-violent cannabis offenses.

The bill creates a prescribed excise tax on cannabis and cannabis products. The funds collected from the taxes would be channeled into opportunity and reinvestment programs.

A Community Reinvestment Grant Program would be established aimed at the provision of services for “individuals most adversely impacted by the War on Drugs,” such as job training, education, literacy programs, mentoring, and substance use treatment programs;

A Cannabis Opportunity Program would be established providing state funds for small business loans in the cannabis industry targeted at social equity candidates; and

An Equitable Licensing Grant Program providing funds for states to implement equitable cannabis licensing programs aimed at minimizing “barriers to cannabis licensing and employment for individuals most adversely impacted by the War on Drugs.”

The bill would require all cannabis producers to obtain a federal permit. Cannabis businesses would need to be licensed at the state, local, and federal levels to operate.

This MORE Act is a substantial step in cannabis legislation. Reactions to the proposed legislation have been mixed. While the bill does include some measures aimed at social equity, critics of the bill claim it does not go far enough. Similarly, while the bill includes a federal permitting provision, this would be the beginning of a nascent federal regulatory scheme.

What does this mean for your business?

While this bill passed in the US House of Representatives, it would still need to pass in the U.S. Senate this term, which by most accounts does not seem likely. However, the passage of this bill signifies the progress that has been made and provides insight on what further legislation may look like.

By Seth Mailhot, Steve Levine, Emily Lyons, Megan Herr 1 Comment

On August 20, 2020, the Drug Enforcement Administration (DEA) published an Interim Final Rule on industrial hemp and hemp derivatives (the interim rule), which immediately went into effect, to conform DEA regulations with the Agriculture Improvement Act of 2018 (the 2018 Farm Bill).

The 2018 Farm Bill effectively removed industrial hemp from the definition of “marijuana” in the Controlled Substances Act (CSA). Additionally, tetrahydrocannabinols contained in industrial hemp, such as cannabidiol (commonly known as CBD), were also removed from the purview of the CSA.

The 2018 Farm Bill defines hemp as:

the plant Cannabis Sativa L. and any part of that plant, including the seeds thereof and all derivatives, extracts, cannabinoids, isomers, acids, salts, and salts of isomers, whether growing or not, with a delta-9 tetrahydrocannabinol concentration of not more than 0.3 percent on a dry weight basis.

Accordingly, because cannabis and its “derivatives, extracts, [and] cannabinoids” are not considered “marihuana,” so long as their delta-9 tetrahydrocannabinol (THC) concentration is at or below 0.3% on a dry weight basis, the regulation of hemp fell outside the authority of the DEA. However, the DEA’s interim rule attempts to draw a hard line in the sand as to when the plant, and any products derived therefrom, are considered “marihuana,” thereby still subject to the DEA’s purview.

Specifically, the interim rule promulgates the DEA’s position that hemp processors can convert otherwise legal hemp into illegal “marihuana,” thereby bringing it back under the DEA’s authority, if such processing and extraction increases the THC content above the 0.3% THC threshold, even momentarily. Specifically, the interim rule states:

[T]he definition of hemp does not automatically exempt any product derived from a hemp plant, regardless of the Δ9-THC content of the derivative. In order to meet the definition of ‘hemp,’ and thus qualify for the exemption from [S]chedule I, the derivative must not exceed the 0.3% Δ9-THC limit. The definition of ‘marihuana’ continues to state that ‘all parts of the plant Cannabis sativa L.,’ and ‘‘every compound, manufacture, salt, derivative, mixture, or preparation of such plant,’ are [S]chedule I controlled substances unless they meet the definition of ‘hemp’ (by falling below the 0.3% Δ9-THC limit on a dry weight basis) or are from exempt parts of the plant (such as mature stalks or non-germinating seeds) . . . As a result, a cannabis derivative, extract, or product that exceeds the 0.3% Δ9-THC limit is a [S]chedule I controlled substance, even if the plant from which it was derived contained 0.3% or less Δ9-THC on a dry weight basis.

Accordingly, the DEA’s stance creates a substantial risk for processors who will be considered to be in possession of a Schedule I controlled substance during the extraction process if the THC content exceeds the 0.3% THC threshold at any point during processing, an almost inevitable result of the extraction process. Nevertheless, the interim rule states:

the definition of hemp does not automatically exempt any product derived from a hemp plant, regardless of the Δ9-THC content of the derivative. In order to meet the definition of ‘hemp,’ and thus qualify for the exemption from [S]chedule I, the derivative must not exceed the 0.3% Δ9-THC limit.

Although the DEA impliedly recognizes the fact that hemp processing can result in a temporary increase in THC content, it still took the position that, should the THC content exceed 0.3% THC at any point during the extraction process, processors will be considered to be in possession of a Schedule I controlled substance, regardless of whether the finished product complies with federal law.

Just some of the many hemp-derived CBD products on the market today.

Consequently, the interim rule creates significant criminal risk for anyone processing industrial hemp, as the DEA has asserted that the processing of hemp into extracts, derivatives and isolated cannabinoids (which are arguably legal under the 2018 Farm Bill) can result in unintentional violation of federal law, thereby subjecting processors to the risk of significant criminal liability. That said, the interim final rule does not appear to be a shift in DEA policy since the passage of the 2018 Farm Bill in December 2018, nor has DEA issued any warnings to industrial hemp manufacturers or otherwise signaled a change in enforcement policy by issuing the Interim Final Rule.

In addition, the DEA took several other steps in the interim final rule towards the deregulation of hemp products:

Adding language stating that the definition of “tetrahydrocannabinols” does not include “any material, compound, mixture, or preparation that falls within the definition of hemp set forth in 7 U.S.C. § 1639o”.

Removing from Schedule V a “drug product” in an FDA-approved finished dosage formulation that contains cannabidiol (CBD) and no more than 0.1 percent (w/w) residual tetrahydrocannabinols (e.g. Epidiolex).

Removing DEA import and export controls for hemp extract that does not exceed the statutory 0.3% THC limit.

In our previous posts, we discussed why state-legal medical and recreational cannabis businesses are likely not eligible to receive federal financial assistance under the Paycheck Protection Program due to the fact that these businesses are inherently engaged in federally illegal activities.

While our view has not necessarily changed, this post is intended to highlight the implications of a recent temporary restraining order prohibiting the U.S. Small Business Administration (SBA) from excluding strip clubs from receiving financial relief under the Coronavirus Aid, Relief, and Economic Security Act (CARES Act or the “Act”).

The Case for Strip Clubs to Receive SBA Assistance

The Facts

Last month, DV Diamond Club of Flint LLC (dba Little Darlings) sued the SBA in the U.S. District Court for the Eastern District of Michigan claiming, among other things, that the agency exceeded its authority under the CARES Act by excluding otherwise eligible strip clubs from receiving Paycheck Protection Program (PPP) loans.

Little Darlings Night Club in Flint, Michigan

On April 6, 2020, Little Darlings, an adult entertainment establishment licensed in Flint, Michigan, applied for a PPP loan to mitigate its business losses as a result of the COVID-19 pandemic.

Due to rapidly diminishing PPP funds and the rejection of applications submitted by other seemingly eligible adult entertainment establishments, Little Darlings filed a claim against the SBA alleging that the agency’s April 15, 2020 “Business Loan Program Temporary Changes; Paycheck Protection Program “ Rule (the Interim Rule) exceeded the SBA and Department of Treasury’s regulatory authority under the CARES Act.

The Interim Rule, in part, provided that:

“Businesses that are not eligible for PPP loans are identified in 13 CFR 120.110 and described further in SBA’s Standard Operating Procedure (SOP) 50 10, Subpart B, Chapter 2, except that nonprofit organizations authorized under the Act are eligible.” 1

The Interim Rule effectively clarified that those businesses that “are identified” in 13 C.F.R. § 120.110 (the Ineligibility Rule) and “described further” in Standard Operating Procedure 50 10 5(K) are “not eligible for PPP loans.”

The Ineligibility Rule – 13 C.F.R. §120.110

In 1996, the SBA declared that certain types of businesses are not eligible to participate in SBA lending programs. Under the Ineligibility Rule (codified at 13 CFR § 120.110), certain sexually oriented businesses2 and “businesses engaged in any illegal activity,”3 in addition to other enumerated businesses, were barred from receiving SBA financial assistance.

The SOP

In 2019, the SBA issued “Standard Operating Procedure for Lender and Development Company Loan Programs 50 10 5(K)” (the SOP) providing guidance to lenders regarding how to administer the Ineligibility Rule. The SOP explained that certain business types such as “Businesses Providing Prurient Sexual Material”i and “Businesses Engaged in any Illegal Activity,ii” among others, may be “ineligible” to participate in SBA programs.4

The Argument

In addition to arguing that the SBA’s regulations violated Little Darlings’ Constitutional rights under the First and Fifth Amendments, Little Darlings alleged that the SBA lacked authority to promulgate regulations clarifying what businesses were eligible for PPP loans, as Congress intended to “increase eligibility” for PPP loans under the CARES Act by establishing only two criteria for PPP eligibility. Moreover, Little Darlings relied on the fact that Congress explicitly provided that “any business concern . . . shall be eligible” for a PPP loan if it met the criteria identified in 15 U.S.C. § 636(a)(36)(D)(i) of the CARES Act.

As a result, Little Darlings sought a Temporary Restraining Order (TRO), Preliminary and Permanent Injunction enjoining the SBA from enforcing or utilizing the Ineligibility Rule or SOP to exclude otherwise eligible PPP loan applicants. As part of the orders, the SBA would be required to immediately notify all SBA lending banks to immediately discontinue utilizing 13 CFR § 120.110 or the SOP as criteria for determining PPP eligibility and to process all PPP loan applications without reference to such regulations and procedures.

On May 11, 2020, U.S. District Judge Matthew Leitman granted Little Darlings’ TRO blocking the SBA from enforcing the Ineligibility Rule and SOP finding that Congress intended to provide temporary paycheck support to “all Americans employed by all small businesses that satisfied the two eligibility requirements – even businesses that may have been disfavored during normal times.”5

Notably, the Sixth Circuit refused to overturn the TRO reasoning that withholding loans from previously “ineligible” businesses, such as strip clubs, conflicts with the broad interpretation of the CARES Act.

Similar cases have also been brought in Illinois and Wisconsin on behalf of adult entertainment businesses that have been denied PPP relief. Notably, on April 23, 2020, the U.S. District Court for the Eastern District of Wisconsin issued a comparable injunction blocking the SBA from denying federal financial assistance to multiple Wisconsin gentlemen clubs.

Implications for Cannabis Businesses

As we previously discussed, one of the largest hurdles for cannabis businesses to receive federal financial assistance from the SBA is that applicants must make a good faith certification that they are not engaged in any federally illegal activity.6

The SBA has historically relied on both the Ineligibility Rule and SOP to uphold its position that “illegal activities” include both Direct Marijuana Businessesiii and Indirect Marijuana Businessesiv that “make, sell, service, or distribute products or services used in connection with illegal activity.”7

However, should Judge Leitman’s interpretation hold true and continue to prohibit the SBA from utilizing the Ineligibility Rule or the SOP as criteria for determining PPP eligibility, cannabis businesses (namely Indirect Marijuana Businesses8) may be eligible to receive PPP loans so long as they satisfy the eligibility requirements identified in the CARES Act.

Although it would ordinarily be absurd to conclude that Congress intended to provide financial assistance to businesses operating in clear violation of federal law (such as Direct Marijuana Businesses), the U.S. District Court for the Eastern District of Michigan and the Sixth Circuit have concluded that the expansive definition of “any business concern” in the CARES Act is not subject to SBA limitations.

U.S. District Judge Matthew Leitman

As Judge Leitman elaborated in his May 11, 2020 order:

“Congress’s decision to expand funding to previously ineligible businesses is not an endorsement or approval of those businesses. Instead, it is a recognition that in the midst of this crisis, the workers at those businesses have no viable alternative options for employment in other, favored lines of work and desperately need help. It is not absurd to conclude that in order to support these workers, Congress temporarily permitted previously excluded businesses to obtain SBA financial assistance.”

Therefore, although we believe it to be highly unlikely that cannabis businesses will actually receive PPP loans due to their continued violation of the Controlled Substances Act (CSA) and need to make a good faith certification that they are not engaged in any federally illegal activity, the door has been opened for certain types of cannabis businesses to potentially receive PPP loans should the SBA remain prohibited from relying on the Ineligibility Rule or SOP to disqualify otherwise eligible applicants.

References

See Interim Rule, p. 2812

12 C.F.R. § 120.110(p) Businesses which: (1) Present live performances of a prurient sexual nature; or (2) Derive directly or indirectly more than de minimis gross revenue though the sale of products or services, or the presentation of any depictions or displays, of a prurient sexual nature

12 C.F.R. § 120.110(h) Businesses engaged in any illegal activity.

See the 2019 SOP, ECF No. 12-11, PageID.570

Specifically, U.S. District Judge Matthew F. Leitman reasoned that: “While Congress may have once been willing to permit the SBA to exclude these businesses from its … lending programs, that willingness evaporated when the COVID-19 pandemic destroyed the economy and threw tens of millions of Americans out of work…” In response to the SBA’s argument that such an interpretation would lead to “absurd results,” Judge Leitman stated: “[T]hese are no ordinary times, and the PPP is no ordinary legislation. The COVID-19 pandemic has decimated the country’s economy, and the PPP is an unprecedented effort to undo that financial ruin.”

It is our position that Indirect Marijuana Businesses (or non plant-touching businesses that service state licensed marijuana establishments) will have an easier time alleging that they are not operating in violation of federal law than those businesses whose existence is inherently premised on cultivating and distributing marijuana in violation of the Controlled Substances Act

i Businesses Providing Prurient Sexual Material (13 CFR § 120.110(p))

A business is not eligible for SBA assistance if:

It presents live or recorded performances of a prurient sexual nature; or

It derives more than 5% of its gross revenue, directly or indirectly, through the sale of products, services or the presentation of any depictions or displays of a prurient sexual nature.

SBA has determined that financing lawful activities of a prurient sexual nature is not in the public interest. The Lender must consider whether the nature and extent of the sexual component causes the business activity to be prurient.

ii Businesses Engaged in any Illegal Activity (13 CFR § 120.110(h))

SBA must not approve loans to Applicants that are engaged in illegal activity under federal, state, or local law. This includes Applicants that make, sell, service, or distribute products or services used in connection with illegal activity, unless such use can be shown to be completely outside of the Applicant’s intended market.

Marijuana-Related Businesses:

Because federal law prohibits the distribution and sale of marijuana, financial transactions involving a marijuana-related business would generally involve funds derived from illegal activity. Therefore, businesses that derive revenue from marijuana-related activities or that support the end-use of marijuana may be ineligible for SBA financial assistance.

iii “Direct Marijuana Business” mean “a business that grows, produces, processes, distributes, or sells marijuana or marijuana products, edibles, or derivatives, regardless of the amount of such activity. This applies to recreational use and medical use even if the business is legal under local or state law where the applicant business is or will be located.”

iv “Indirect Marijuana Business” means “a business that derived any of its gross revenue for the previous year (or, if a start-up, projects to derive any of its gross revenue for the next year) from sales to Direct Marijuana Businesses of products or services that could reasonably be determined to aid in the use, growth, enhancement or other development of marijuana. Examples of Indirect Marijuana Businesses include businesses that provide testing services, or sell or install grow lights, hydroponic or other specialized equipment, to one or more Direct Marijuana Businesses; and businesses that advise or counsel Direct Marijuana Businesses on the specific legal, financial/ accounting, policy, regulatory or other issues associated with establishing, promoting, or operating a Direct Marijuana Business. However … [the] SBA does not consider a plumber who fixes a sink for a Direct Marijuana Business or a tech support company that repairs a laptop for such a business to be aiding in the use, growth, enhancement or other development of marijuana. Indirect Marijuana Businesses also include businesses that sell smoking devices, pipes, bongs, inhalants, or other products if the products are primarily intended or designed for marijuana use or if the business markets the products for such use.”

By Steve Levine, Megan Herr, Meghan Brennan No Comments

On Thursday April 23, 2020, Representatives Earl Blumenauer (D-OR) and Ed Perlmutter (D-CO) introduced the “Emergency Cannabis Small Business Health and Safety Act” in the House. Blumenauer and Perlmutter have been influential in protecting state-legal cannabis businesses from federal interference, most recently under the 2020 federal appropriations rider.

If passed, the Act would allow state-legal medical and recreational cannabis businesses to take advantage of the multi-trillion dollar stimulus packages designed to help small businesses harmed by COVID-19.

As we previously discussed, cannabis businesses harmed by COVID-19 remain ineligible to receive federal financial assistance due to their engagement in “federally illegal” activities. Consequently, cannabis businesses cannot receive assistance from the Small Business Administration (SBA) thereby making them ineligible to receive Paycheck Protection Program (PPP) loans and other SBA financial assistance, including Economic Injury Disaster Loans (EIDLs), traditional 7(a) loans, 504 loans, and microloans.

To provide the industry with much needed economic relief, the legislation states that cannabis businesses would no longer be prohibited from (i) participating in the PPP, (ii) receiving EIDL loans, or (iii) receiving emergency EIDL grants purely on the basis that the business is a “cannabis-related legitimate business”1 or “service provider.”2

Additionally, the Act clarifies that the SBA and its officers, directors and employees would “not be held liable pursuant to any Federal law or regulation solely for providing a loan or a loan guarantee to a cannabis-related legitimate business or a service provider.”

Even though states have varied in their approach to continue medical and retail cannabis operations amid the coronavirus outbreak, a majority of states that allow some form of sale and consumption of cannabis have designated the cannabis industry as “essential” and open for operation.3 Some states have gone as far as allowing home delivery, curbside pick-up, and telemedicine consultations.

Nonetheless, despite the cannabis industry’s designation as “essential,” cannabis businesses (including those who service the cannabis industry) will continue to be precluded from receiving federal financial assistance until the Emergency Cannabis Small Business Health and Safety Act, or similar legislation, is passed. It is important to note that, even if passed, the Emergency Cannabis Small Business Health and Safety Act would likely provide little relief, as the majority of the funds to be administered by the SBA have already been accounted for.

What does this mean to you?

Although the COVID-19 pandemic has highlighted the need for the heavily-taxed and financially burdened cannabis industry to receive assistance under the stimulus packages, the Act, even if passed by Congress, faces an uphill battle in the Republican-held Senate.

References

The term “cannabis-related legitimate business” means a manufacturer, producer, or any person that – (A) engages in any activity described in subparagraph (B) pursuant to a law established by a State or a political subdivision of a State, as determined by such State or political subdivision; and (B) participates in any business or organized activity that involves handling cannabis or cannabis products, including cultivating, producing, manufacturing, selling, transporting, displaying, dispensing, distributing, or purchasing cannabis or cannabis products.”

The term “service provider” (A) means a business, organization, or other person that – (i) sells goods or services to a cannabis-related legitimate business; or (ii) provides any business services, including the sale or lease of real or any other property, legal or other licensed services, or any other ancillary service, relating to cannabis; and (B) does not include a business, organization, or other person that participates in any business or organized activity that involves handling cannabis or cannabis products, including cultivating, producing, manufacturing, selling, transporting, displaying, dispensing, distributing, or purchasing cannabis or cannabis products.”

In our previous post, we touched on the fact that state-legal medical and recreational cannabis businesses (including indirect cannabis businesses) could not receive federal financial assistance due to the continued Schedule I status of cannabis under the Controlled Substances Act (CSA). While state-legal medical and recreational cannabis businesses have been adversely affected due to government imposed shelter-in-place restrictions across the United States, they are unable to take advantage of the multi-trillion dollar stimulus packages that are designed to help small businesses because they are engaged in “federally illegal” activities. As described below, applicants applying for federal loans must certify, under penalty of perjury, that they are not engaged in “illegal” activity.

While it is our view that state-legal medical and recreational cannabis businesses should be entitled to assistance as they are hurting like every other business, we explain why such businesses cannot receive financial assistance under the Paycheck Protection Program and the SBA’s Economic Injury Disaster Loan Program due to the facts that these businesses do not comply with federal law.

CARES Act

As previously discussed, Section 1102 of the Coronavirus Aid, Relief, and Economic Security Act (CARES Act or the “Act”) directed $349 billion to the Small Business Administration (SBA) to administer to small businesses harmed by COVID-19. As a result, businesses can apply for Paycheck Protection Program (PPP) loans and other SBA financial assistance, including Economic Injury Disaster Loans (EIDLs), traditional 7(a) loans, 504 loans, and microloans, and can also receive investment capital from the Small Business Investment Company program.

Paycheck Protection Program (PPP)

Generally, the following businesses are eligible to receive loans under the PPP:

Any business, 501(c)(3) nonprofit organization, 501(c)(19) veterans organization or Tribal business with not more than 500 employees whose principal place of residence is in the United States;

Any business that meets the SBA employee-basedsize standards for the industry in which it operates (if applicable);

Any business that is a “small business concern” as defined in Section 3 of the Small Business Act, 15 U.S.C. 632, and meets the SBA employee-based or revenue-basedsize standards corresponding to its primary industry; or

Any business that is a “small business concern” under the SBA’s “alternative size standard” as of March 27, 2020, which standard is met if the business has not more than:

(i) maximum tangible net worth of $15 million, and

(ii) an average net income of $5 million (after Federal income taxes, excluding any carry-over losses) for 2 full fiscal years before the date of application.

Importantly, to apply for PPP, an applicant must make a good faith certification that the applicant is eligible to receive a PPP loan. An applicant must certify, under penalty of perjury, that it “is not engaged in any activity that is illegal under federal, state or local law.” (Borrower Application Form, page 2).

Consequently, because state-legal marijuana businesses (including indirect marijuana businesses) are operating in violation of federal law, applicants cannot make such certification, they remain ineligible to participate in the PPP.

Economic Injury Disaster Loans (EIDLs)

The CARES Act also provided a slew of changes to the SBA’s pre-existing EIDL program, which provides small businesses with working capital loans of up to $2 million to assist to help overcome the temporary loss of revenue as the result of a declared disaster.

The Act set out new rules making it easier for small businesses harmed by COVID-19 to receive loans quickly and efficiently; the Act added $30 billion to the EIDL loan fund, with an additional $10 billion added for the EIDL Grants connected to the EIDL loans.

The CARES Act also expanded eligibility to include businesses with no more than 500 employees, any individual operating as a sole proprietor or an independent contractor, and tribal businesses, cooperatives and ESOPs with no more than 500 employees. Small business concerns and small agricultural cooperatives who meet the SBA’s applicable size standards are also eligible, as well as most nonprofits.

However, to receive an EIDL loan, applicants must make a good faith certification that the applicant is eligible to receive an EIDL. An applicant must certify, under penalty of perjury, that it “is not engaged in any illegal activity (as defined by Federal guidelines).” (COVID-19 Economic Injury Disaster Loan Application).

The SBA has clarified that the limitation on applicants “engaged in any illegal activity” (13 CFR § 120.110 (h)) refers to all applicants engaged in “illegal activity under federal, state, or local law.”

In a Statement of Position issued on April 1, 2019 (the SOP), the SBA clarified that “illegal activity” includes “[a]pplicants that make, sell, service, or distribute products or services used in connection with illegal activity, unless such use can be shown to be completely outside of the Applicant’s intended market.” (SOP 50 10 5(K))

The SOP indicated that both (i) Direct Marijuana Businesses1 and (ii) Indirect Marijuana Businesses2 cannot receive SBA assistance due to the limitation on applicants “engaged in any illegal activity.”

It is the SBA’s position that, “because federal law prohibits the distribution and sale of marijuana, financial transactions involving a marijuana-related business would generally involve funds derived from illegal activity.”

Consequently, because state-legal cannabis businesses (including indirect marijuana businesses) are operating in violation of federal law, applicants cannot certify that they are “not engaged in any illegal activity,” they are not eligible to receive EIDLs.

“Direct Marijuana Business” mean “a business that grows, produces, processes, distributes, or sells marijuana or marijuana products, edibles, or derivatives, regardless of the amount of such activity. This applies to recreational use and medical use even if the business is legal under local or state law where the applicant business is or will be located.”

“Indirect Marijuana Business” means “a business that derived any of its gross revenue for the previous year (or, if a start-up, projects to derive any of its gross revenue for the next year) from sales to Direct Marijuana Businesses of products or services that could reasonably be determined to aid in the use, growth, enhancement or other development of marijuana. Examples of Indirect Marijuana Businesses include businesses that provide testing services, or sell or install grow lights, hydroponic or other specialized equipment, to one or more Direct Marijuana Businesses; and businesses that advise or counsel Direct Marijuana Businesses on the specific legal, financial/ accounting, policy, regulatory or other issues associated with establishing, promoting, or operating a Direct Marijuana Business. However … [the] SBA does not consider a plumber who fixes a sink for a Direct Marijuana Business or a tech support company that repairs a laptop for such a business to be aiding in the use, growth, enhancement or other development of marijuana. Indirect Marijuana Businesses also include businesses that sell smoking devices, pipes, bongs, inhalants, or other products if the products are primarily intended or designed for marijuana use or if the business markets the products for such use.”

On Wednesday, March 25, the United States Senate approved an estimated $2-trillion stimulus package in response to the economic impact of the COVID-19 outbreak. The legislation, formally known as the “Coronavirus Aid, Relief, and Economic Security Act” (or the CARES Act), was approved by the Senate 96-0 following days of negotiations. One of the most highly anticipated provisions of the CARES Act, the “recovery rebates” for individuals, will provide a one-time cash payment up to $1,200 per qualifying individual ($2,400 in the case of eligible individuals filing a joint return) plus an additional $500 for qualifying children (§6428.2020(a)). The CARES Act, which remains subject to House approval, also prescribes an additional $500 billon in corporate aid, $100 billion to health-care providers, $150 billion to state and local governments and $349 billion in small business loans in an effort to provide continued employment and stabilize the economy. The legislation further provides billions of dollars in debt relief on existing loans.

CARES Act – Paycheck Protection Program

Under the CARES Act, small businesses who participate in the “Paycheck Protection Program” can receive loans to cover payroll expenses, group health care benefits, employee salaries, interest on mortgage obligations, rent, and utilities (§1102(F)(i)). To qualify for these small business loans, businesses must employ 500 employees or less, including all full-time and part-time employees (§1102(D)). Eligible recipients must also submit the following as part of their loan application: (i) documentation verifying the number of full-time equivalent employees on payroll and applicable pay rates; (ii) documentation verifying payments on covered mortgage obligations, payments on covered lease obligations, and covered utility payments; and (iii) a certification that the documentation presented is true and the amounts requested will be used to retain employees and make necessary payments (§1106(e)). The CARES Act delegates authority to depository institutions, insured credit unions, institutions of the Farm Credit System and other lenders to provide loans under this program (§1109(b)). The Treasury Department will be tasked with establishing all interest rates, loan maturity dates, and all other necessary terms and conditions. Prior to issuing these loans, lenders will consider whether the business (i) was in operation as of February 15, 2020, (ii) had employees for whom the business paid salaries and payroll, or (iii) aid independent contractors as reported on a Form 1099-MISC (§1102(F)(ii)(II)).

What Does This Mean for Cannabis Businesses?

Due to the continued Schedule I status of cannabis (excluding hemp) under the Controlled Substances Act (CSA), cannabis businesses are not eligible to participate in the Paycheck Protection Program intended to keep “small businesses” afloat during the current economic crisis. Because federal law still prohibits banks from supporting marijuana businesses, financial institutions remain hesitant to service the industry, as anti-money laundering concerns and Bank Secrecy Act requirements (31 U.S.C. 5311 et seq.) are ever-present. As a result, even if cannabis businesses technically qualify to receive federal assistance under the Paycheck Protection Program, they will face an uphill battle in actually obtaining such loans.

Cannabis Businesses Are Also Precluded from “Disaster” Assistance

Moreover, the conflict between state and federal law continues to prevent cannabis business from receiving assistance from the U.S. Small Business Administration (SBA) under the Coronavirus Preparedness and Response Supplemental Appropriations Act (H.R. 6201). In light of the COVID-19 outbreak, the SBA revised its “Disaster Loan” process to provide low-interest “Disaster Loans” to eligible small businesses. To qualify for these loans, a state must submit documented business losses for at least five businesses per county. The problem, however, is that the SBA still refuses to assist state-legal cannabis businesses in equal need of small business loans. Specifically, in a 2018 Policy Notice, the SBA reaffirmed that cannabis businesses – and even some non “plant-touching” firms who service the cannabis industry – cannot receive aid in the form of federally backed loans, as “financial transactions involving a marijuana-related business would generally involve funds derived from illegal activity.” The 2018 Policy Notice clarified that the following business are ineligible to receive SBA loans:

(a) “Direct Marijuana Business” — a business that grows, produces, processes, distributes, or sells marijuana or marijuana products, edibles, or derivatives, regardless of the amount of such activity. This applies to personal use and medical use even if the business is legal under local or state law where the applicant business is or will be located.

(b) “Indirect Marijuana Business” — a business that derived any of its gross revenue for the previous year (or, if a start-up, projects to derive any of its gross revenue for the next year) from sales to Direct Marijuana Businesses of products or services that could reasonably be determined to support the use, growth, enhancement or other development of marijuana. Examples include businesses that provide testing services, or sell grow lights or hydroponic equipment, to one or more Direct Marijuana Businesses. In addition, businesses that sell smoking devices, pipes, bongs, inhalants, or other products that may be used in connection with marijuana are ineligible if the products are primarily intended or designed for such use or if the business markets the products for such use.

More recently, the SBA provided further clarification that cannabis businesses are not entitled to receive a cut of the federal dollars being appropriated for disaster relief because of the CSA’s continued prohibition of the sale and distribution of cannabis. Last week, the SBA reiterated that:

“With the exception of businesses that produce or sell hemp and hemp-derived products [federally legalized under the 2018 Farm Bill], marijuana related businesses are not eligible for SBA-funded services.” (@SBAPacificNW)

Consequently, because of the continued Schedule I status of cannabis under federal law, cannabis businesses will not be entitled to receive Disaster Loans from the SBA, regardless of whether they qualify as a struggling small business.

Resolving the Issue

While the federal government has been considering legislation, such as SAFE Banking and the STATES Act, to create a more rational federal cannabis policy, neither of these bills are likely to pass any time soon given the current COVID-19 pandemic.

At the end of the day, until Congress passes some form of federal cannabis legalization, these small businesses will remain plagued by the inability to receive financial assistance, as evinced by the Paycheck Protection Program.

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

We use tracking pixels that set your arrival time at our website, this is used as part of our anti-spam and security measures. Disabling this tracking pixel would disable some of our security measures, and is therefore considered necessary for the safe operation of the website. This tracking pixel is cleared from your system when you delete files in your history.

We also use cookies to store your preferences regarding the setting of 3rd Party Cookies.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.

Further, the warning letters noted the marketing of several CBD products that highlighted the benefits of CBD for a range of conditions in such a manner that, according to the FDA, “misleadingly suggests that [their] . . . products are approved or endorsed by FDA in some way when this is not true.” The FDA also took issue with the way products were labeled, which included callouts on the front label regarding the CBD content of the product (a requirement under most state laws that permit CBD as an ingredient). Similarly, the FDA also noted that some of the products advertised CBD as an active ingredient in a topical pain reliever product. According to the FDA, no company may legally market such a product, since there are no OTC monographs or NDAs that allow the use of CBD in an OTC drug.

Further, the warning letters noted the marketing of several CBD products that highlighted the benefits of CBD for a range of conditions in such a manner that, according to the FDA, “misleadingly suggests that [their] . . . products are approved or endorsed by FDA in some way when this is not true.” The FDA also took issue with the way products were labeled, which included callouts on the front label regarding the CBD content of the product (a requirement under most state laws that permit CBD as an ingredient). Similarly, the FDA also noted that some of the products advertised CBD as an active ingredient in a topical pain reliever product. According to the FDA, no company may legally market such a product, since there are no OTC monographs or NDAs that allow the use of CBD in an OTC drug.