By Melissa Kuipers Blake, Osiris Morel No Comments

After nearly a decade of conversation and education on the Hill, the Senate Banking, Housing and Urban Affairs Committee finally held a markup on the Secure and Fair Regulation (SAFER) Banking Act. Previously known as the SAFE Banking Act, the “R” was included to account for Sen. Jack Reed’s (D-RI) concerns with Section 10. The senator shared his concerns publicly on May 11 during the “Examining Cannabis Banking Challenges of Small Businesses and Workers” hearing. Sen. Reed said that Section 10’s language “would make it more difficult for federal regulators to raise the alarm about relationships with any customer that presents significant risks to the bank” and shared that such a provision is “not limited to the marijuana industry or the cannabis industry,” but that it “could allow pyramid schemes or all sorts of other interesting activity to go on without an effective response by the regulator.” Since then, he and a group of bipartisan members, including Majority Leader Chuck Schumer (D-NY), Senate Banking Committee Chair Sherrod Brown (D-OH), and Sens. Steve Daines (R-MT), Cynthia Lummis (R-WY), Kevin Cramer (R-ND) and Kyrsten Sinema (I-AZ), have worked endlessly to develop language to resolve such concerns while maintaining GOP support, leading to the SAFER Banking Act.

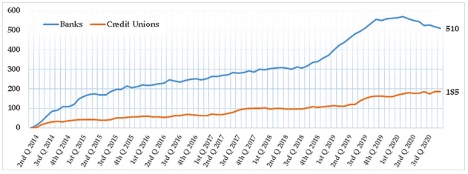

Number of Depository Institutions Actively Banking Cannabis-Related Businesses in the United States (Reported in SARS)

The difference between the SAFE Banking Act and the SAFER Banking Act can mainly be found in Section 10. Changes focus on and determines:

How regulators terminate bank accounts;

How the Federal Deposit Insurance Corporation (FDIC) develops guidance for financial institutions serving state-licensed cannabis businesses;

How income derived from state-legal cannabis business activity is managed;

That personal and political beliefs cannot impact a financial regulator’s decision making;

That federal banking regulators and state banking supervisors and their secretaries of Commerce and Treasury would create rules to increase access to deposit accounts and how such individuals would enhance customer relationships with rural, low- and moderate-income, unbanked and tribal communities; and

How the FDIC would conduct a biennial survey and report on barriers for small- and medium-sized businesses.

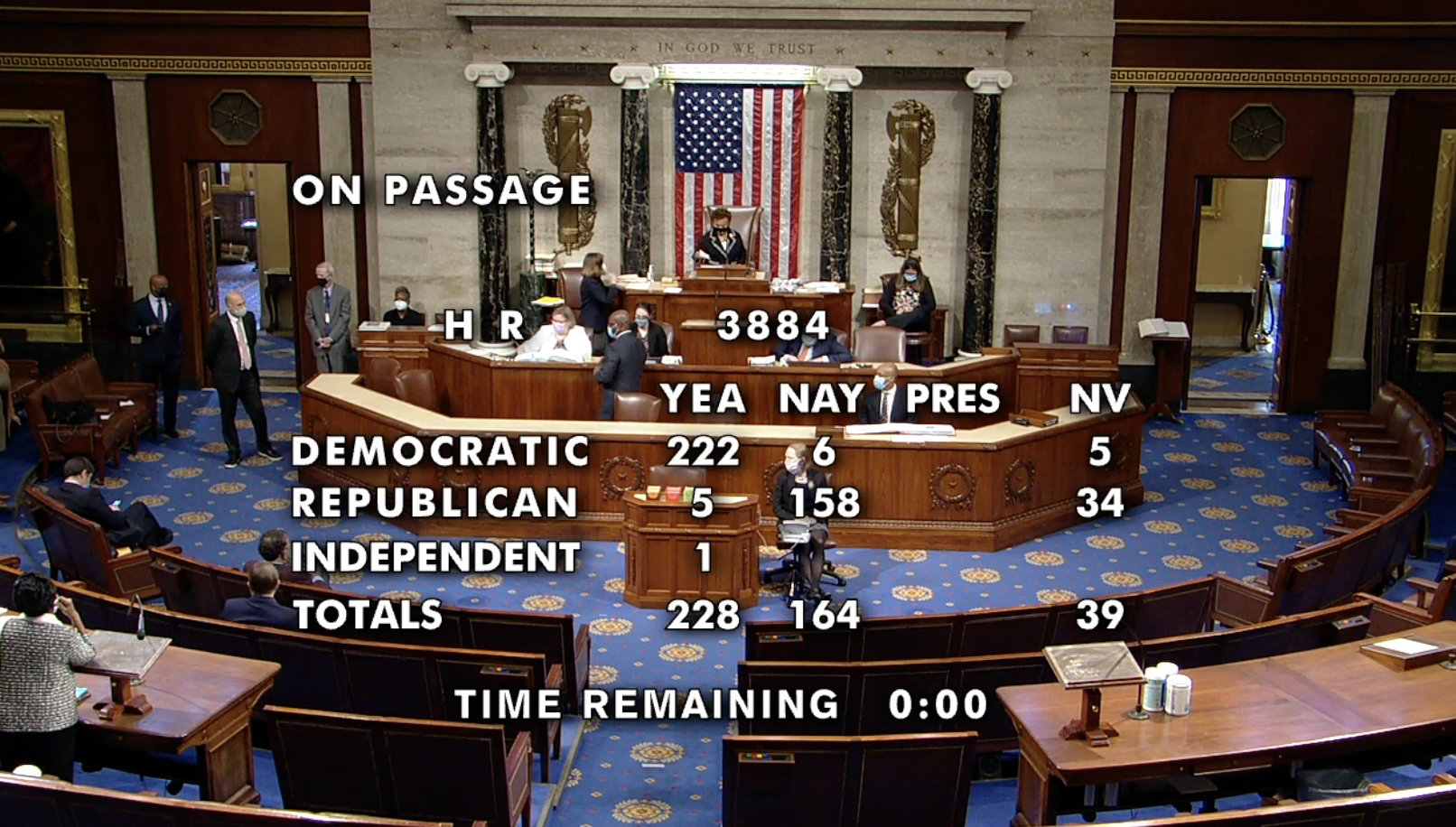

During the markup on Wednesday, members introduced and discussed a range of amendments related to criminal justice reform, the racial wealth gap, federal regulators and their processes, rescheduling and the opioid epidemic. In total, there were six amendments, one by Chairman Brown, as well as Sens. Mike Crapo (R-ID), Bill Hagerty (R-TN), Mike Rounds (R-SD) and two by Sen. Raphael Warnock (D-GA). Sen. Brown’s amendment, which would make technical changes to the bill, was the only amendment to prevail on a 17-6 vote.

Senate Majority Leader Chuck Schumer (center), Senate Finance Committee Chair Ron Wyden (right) and Senator Cory Booker (left)

To begin the markup, Chair Brown said that propelling this legislation is a critical step in reversing the damage done by the war on drugs and clarified that the SAFER Banking Act would create a better financial system for small and medium-sized cannabis businesses that lack access to such traditional banking services. Sen. Daines, who served as the committee ranking member in place of Sen. Tim Scott (R-SC), who was in California preparing for the Republican presidential debate, shared that although he opposes legalization or decriminalization, he agreed to sponsor and support the SAFER Banking Act because it would fix the current banking system for cannabis businesses nationwide. After hearing remarks from Sens. Lummis, Catherine Cortez Masto (D-NV) and Sinema, the committee voted on the bill, and approved its passage to the Senate floor on a 14-9 vote. Senators voting in favor of the bill were Brown, Tester, Warren, Reed, Menendez (by proxy), Smith (by proxy), Warner, Fetterman, Cortez-Masto, Sinema, Van Hollen, Lummis, Cramer and Daines, and voting against the measure were Sens. Warnock, Scott (by proxy), Crapo, Tillis, Kennedy, Haggerty, Vance and Britt.

After the vote, Sen. Jeff Merkley (D-OR) thanked Sen. Rand Paul (R-KY) and former Republican Sen. Cory Gardner (CO) for their early efforts and for bringing the legislation and issue to the chamber’s attention and concluded that he hopes to have a robust discussion with the full Senate chamber.

With the bill out of committee, it heads to the Senate floor for additional input, discussion and potentially a vote. Majority Leader Schumer has said he intends to bring the SAFER Banking Act to the floor “with all due speed” and noted that he is committed to attaching Rep. Dave Joyce’s (R-OH) Harnessing Opportunities by Pursuing Expungement (HOPE) Act and Rep. Brian Mast’s (R-FL) Gun Rights and Marijuana (GRAM) Act to the final legislation. Sen. Schumer also shared that such provisions would address the war on drugs, bolster social equity and criminal justice reform and protect Second Amendment rights for medical cannabis patients.

When the SAFER Banking Act will receive floor time remains unclear, but Leader Schumer has made numerous representations that he would like to see it done this year.

As the cannabis industry grows, companies are faced with more labor related compliance and regulatory issues, which require time and expertise. Rather than hire internal staff to manage human resources (HR) and compliance, many companies choose to outsource nearly 85% of HR functions. These functions include payroll administration, HR tasks and other employment liabilities, like insurance, to a third-party Managed Service Provider (MSP). This model frees up internal resources to grow and develop the company’s core business, while also offsetting risks associated with employment, taxes and insurance.

Nicholas Murer formed WECO in 2014 to provide human capital financial services to the legal cannabis industry, offering services like payroll management, workforce management, human resource implementation, accounting solutions, recruiting and staffing. The company has since expanded to providing consulting services, financial product representation, investor asset development, wholesale trading and advising emerging market development projects worldwide.

With markets across the country maturing at a rapid rate, change is a constant. Cannabis companies operating in new markets need to maintain compliance while focusing on their business plan, which can be a difficult task. We sat down with Nick Murer to learn more about compliance issues that cannabis businesses face, like workers comp, payroll taxes, insurance and how outsourcing some HR functions can help.

Q: What are some of the major labor compliance issues faced by employers in the cannabis industry?

Nicholas Murer: Like other industries, the cannabis industry is subject to labor related regulations like paid time off, harassment prevention training, workers compensation requirements, payroll taxes, pay transparency, unemployment insurance and reporting. Unless companies have an expert, or a team of experts, monitoring and managing compliance on both the employer and employee side, they may quickly find themselves in hot water with state regulatory agencies, or even with an employee for labor law violations.

Another issue continues to be access to banking and payment processing. Many cannabis companies continue to pay employees and vendors in cash, which creates not only problems in accurate accounting, but safety concerns for employees as well. There are banks and credit unions that will work with cannabis companies, but without a partner who has relationships with and access to a proven and trusted network of banks and processors, monthly account and transaction fees can be expensive and out of reach. With the SAFE Banking Act stalled once again in Congress, this will continue to be an issue.

Q: How can cannabis companies mitigate their risk by outsourcing HR functions?

Murer: By utilizing a Managed Service Provider (MSP), cannabis companies enter a labor contract model for payroll and HR administration. An MSP is a professional workforce management company that provides comprehensive employment services for businesses.Nick Murer and the WECO team will be at the CQC this October 16-18. Click here to learn more.

This model provides the client company with the best labor practices, risk mitigation and claims management with access to national workers compensation and unemployment insurance. The MSP is the employer of record, so is responsible for most aspects of the employee/employer relationship. The day-to-day management of the employee continues with the client company, but the company’s liability and risk are reduced. MSP compliance risk reducing services include:

Background screening and reporting

Labor related compliance management at state and local levels

Handbook and policy management and distribution to employees

A central location for employee onboarding, time and assignment tracking, payroll administration and reporting

Separation of labor cost for each location/company for 280E tax mitigation

All federal, state and local tax filings

Employment verification

Employee access to health insurance

Employee access to banking for payroll direct deposit

Outsourcing to an MSP provides cost savings to the company, including:

Reduced staff

More efficient payroll processing and legal compliance

Streamlined recruitment

Utilizing WECO to manage the employer of record process allows client companies to look beyond traditional payroll to a full workforce management solution that ensures a smooth payroll and provides the tools that can support the growth and development of a workforce including compliant banking, human resources management and employee services.

About Nicholas Murer

Nicholas Murer formed WECO in 2014 to provide human capital financial services to the legal cannabis industry, offering services like payroll management, workforce management, human resource implementation, accounting solutions, recruiting and staffing. Nick Murer has more than twenty years of professional and technical sales experience working globally in the energy, engineering and scientific industries, including a substantial background in industrial technical sales, account development, marketing, human resources, acquisitions and project management. He studied accounting and business management at the University of Pittsburgh and organization development and human resource management from Colorado State University.

By Abraham Finberg, Rachel Wright, Simon Menkes No Comments

Cannabis companies representing 45% of California’s cannabis sales are pushing a bill that will crack down on non-paying customers. Well known operators, including Kiva, Lowell Farms, Nabis and Sunderstorm, recently formed Financial Stability for California Cannabis (FSCC) and moved to support Assembly Bill 766.”

The bill, nicknamed “The Cannabis Credit Protection Act,” would require a cannabis licensee to pay for goods and services sold or transferred by another licensee no later than 15 days following the final date set forth in the invoice. If full payment is not received by that date, the seller would be required to report this to the Department of Cannabis Control (DCC), which in turn would notify the delinquent buyer and begin disciplinary proceedings. The buyer would be prohibited from purchasing any other cannabis products on credit until the delinquent invoice was paid. In addition, the DCC would be empowered to issue a penalty (unspecified), taking into account “the frequency and gravity of the licensee’s [past] failure to pay outstanding invoices”.

In a letter of support for AB 766, the FSCC stated, “This culture of nonpayment that has emerged in California’s cannabis market leaves businesses across the entire industry and supply chain – as well as ancillary businesses that support legal cannabis operators – with outstanding balances and unpaid invoices sometimes totaling hundreds of thousands of dollars…This ballooning debt bubble in the cannabis industry will only continue to grow without proper oversight, putting the entirety of the state’s supply chain at risk of collapse and impacting state revenue decline even further.”

Opponents of the bill acknowledge the problem of non-payment in the industry, but feel AB 766 is too heavy handed and is “ripe for abuse.” In a blog post for the international legal firm Harris Bricken, cannabis attorney Griffen Thorne writes, “[L]icensees who are reported would be legally prohibited from buying goods or services on credit from other licensees until they pay the invoices for which they were reported in full … The person making the report has to give the DCC almost no information in order to make the report. There is no hearing. There does not even seem to be an opportunity to contest the report. The second a report is made, the other side loses its rights to buy goods on credit – presumably even under preexisting contractual arrangements with third parties. This seems like an obvious due process concern and ripe for abuse.”

The number and amounts of unpaid cannabis product invoices have ballooned over time and have driven California cannabis vendors to take such extreme measures. Collections and outstanding receivables are a symptom of an industry struggling under heavy taxes and competition from illegal operations that pay no taxes whatsoever, and which now account for over 60% of all cannabis sales within the state.

In order to ascertain the current status of AB 766, 420CPA reached out to Assemblymember Phil Ting (D-San Francisco), co-sponsor of the bill along with FSCC, the Cannabis Distribution Association, California Cannabis Industry Association and the California Cannabis Manufacturers Association. We corresponded with Tania Dikho, Ting’s Legislative Director. Ms. Dikho informed us that the bill was heard in the Assembly Appropriations Committee on May 18, but it was not passed.

“It’s a 2-year bill meaning we can’t act on it until this legislative year is over, so the bill will not have another hearing [and we] can’t make any changes to it until next year,” explained Ms. Dikho.

The 2-year status is a tenuous one. The bill must be approved by the Assembly and make its way to the Senate between early January 2024 and January 31, 2024 or it may no longer be acted upon and will die a legislative death.

Businesses that would like to voice their opinion for or against AB 766 should contact their state legislative representatives.

2022 brought more change and visibility to the cannabis industry than nearly any year before. Two of five legalization ballot measures passed, bringing the total number of states with legal medical or medical and recreational laws to 39. President Biden issued an executive order pardoning nonviolent offenders and directing a review into rescheduling cannabis. The Medical Marijuana and Cannabidiol Research Expansion Act was enacted. Cannabis arose prominently in legislatures across the country, with over 50 federal bills and hundreds of state-level measures introduced.

We’ve yet to see the full impact from Biden’s October 6 announcement

But as 2022 came to a close, only a handful of actions are being carried into the new year, and the industry faces more hardship and turmoil than it has since the inception of legalization. Legal cannabis retailers and cultivators in markets across the country continue to struggle with onerous regulations and competition from the illicit market, and oversupply in these markets is driving down prices as West Coast growers and manufacturers anxiously await interstate commerce.

Looking ahead to the coming year, industry watchers can anticipate certain issues and legislation: further investigation into cannabis’ classification on the Controlled Substances Act (CSA) from federal agencies, federal cannabis pardons coming to fruition, a follow-up from the Department of Justice’s technical report, and the reintroduction of high-profile federal legislation, like the Cannabis Opportunity Act (CAOA), the States Reform Act, Marijuana Opportunity Reinvestment and Expungement (MORE) Act, Harnessing Opportunities by Pursuing Expungement (HOPE) Act and the Secure and Fair (SAFE) Banking Act.

Below, we recap some of the big moments of 2022 and what to expect in 2023.

A Presidential Pardon for Simple Possession

On Oct. 6, President Biden made a historic announcement to “grant a full, complete, and unconditional pardon to all current United States citizens and lawful permanent residents who committed the offense of simple possession of marijuana in violation of the Controlled Substances Act” and “all current United States citizens and lawful permanent residents who have been convicted of the offense of simple possession of marijuana in violation of the Controlled Substances Act.” His executive order also encouraged governors to follow suit for cases regarding state offenses and requested that the secretary of Health and Human Services and the attorney general “expeditiously” review how cannabis is scheduled under federal law.

Biden signing his executive order back in October of 2022

The president’s strategic plan attempts to at least partly address some of the adverse impacts of the United States’ war on drugs on certain populations like low-income and Black and Latinx Americans. While an admirable and important effort, certain portions of his executive order will take much longer than others to yield tangible impact. A federal pardoning can take anywhere between two to five years, and the laws and duration of state-level pardoning vary—depending on the state and its governing practices. Additionally, since governors are not required to pardon individuals following the president’s executive order, some convicted persons may never see or be able to seek justice. And the most uncertain timeline relates to the review of cannabis’ classification on the CSA. Rescheduling or descheduling a substance under the CSA can be tedious and grueling, and, as seen with other substances, the process can range from four to ten years. However, the exercise is ongoing, and although results may not be shared in time for the 118th Congress, it is to be expected that the issue will be discussed at length in 2023 and beyond.

When it comes to legislation, there is no question that Majority Leader Chuck Schumer (D-NY) and Sens. Ron Wyden (D-OR) and Cory Booker (D-NJ) will reintroduce the CAOA in 2023. The comprehensive legislation aims to decriminalize cannabis by removing the drug from the CSA and tackles issues related to research, public safety, restorative justice and equity, taxation and regulation, public health and industry practices.

2. States Reform Act.

Sen. Schumer unveiling the Cannabis Administration and Opportunity Act

Another piece of legislation we anticipate seeing in the 118th Congress is Rep. Nancy Mace’s (R-SC) States Reform Act. Coming from a state without any cannabis laws, the freshman congresswoman introduced a measure that would federally decriminalize cannabis by fully deferring to state powers over prohibition and commercial regulation and regulate cannabis products like alcohol. In 2022, the bill received positive feedback from the industry and dominated the discussions during the Developments in State Cannabis Laws and Bipartisan Cannabis Reforms congressional hearing. With its bold cannabis sponsor, who will now serve as the House Oversight Subcommittee on Civil Rights and Civil Liberties chair, the States Reform Act will undoubtedly take center stage in 2023.

3. MORE Act.

Sponsored by Rep. Jerry Nadler (D-NY), the MORE Act will also be reintroduced in 2023; however, it remains to be seen how much attention the bill will receive. The MORE Act aims to decriminalize cannabis by removing the drug from the CSA and eliminating criminal penalties for anyone who manufactures, distributes or possesses cannabis. In the 117th Congress, Rep. Nadler served as the chair to the House Judiciary Committee and was able to advance his measure through the chamber with ease. But since the House majority has flipped, and Rep. Jim Jordan (R-OH) is likely to serve as the chair, getting the MORE Act to the floor for a vote may be challenging—especially given Rep. Jordan’s opposition to the cannabis sector.

The House passing the MORE Act back in 2020

4. HOPE Act.

The HOPE Act often flies under the radar, but this Republican-sponsored bill made headlines during the 117th Congress. Sponsored by Co-Chair of the Congressional Cannabis Caucus (CCC), Rep. Dave Joyce (OH), the bipartisan legislation aims to help states with expunging cannabis offenses by reducing the financial and administrative burden of such efforts through federal grants. Although it was not considered in the House, the language of the bill was heavily debated by the Senate, particularly toward the end of the year when the chamber was negotiating the final text for end-of-year must-pass packages, like the National Defense Authorization Act (NDAA), the Omnibus and the Continuing Resolution (CR). Alongside the SAFE Banking Act, the HOPE Act was one of the only cannabis bills that had a realistic chance of advancing as part of a larger legislative vehicle, so there is no question that the congressman will reintroduce the measure in the upcoming congressional session.

5. SAFE Banking Act.

And last, but certainly not least, is the most discussed cannabis bill this year: the SAFE Banking Act. The legislation aims to create a safe harbor for financial institutions to provide traditional banking services to cannabis businesses in states that have legalized the drug. It also allows cannabis businesses to access lines of credit, loans and wealth management. It has now passed in the House seven times, with bipartisan support. And although the SAFE Banking Act was debated by the House several times throughout the year, the Senate did not tackle the bill until November. By the time discussions for the bill’s language had taken off, Sen. Booker remained firm that he would only support a cannabis bill if it included criminal justice and social equity reform language. In an attempt to satisfy the senator’s demands, Majority Leader Schumer considered marrying the SAFE Banking Act and the HOPE Act as part of a larger package.

However, and much to the cannabis industry’s detriment, not only was the timeline for those bills a little too late, but Democrats were, unfortunately, unable to fix the money laundering and cash legacy concerns of Sen. Chuck Grassley (R-IA) and other Republicans.

Sen. Cory Booker (D-NJ) Photo: Nick Fisher, Flickr

After attempting to attach the SAFE Banking Act to multiple vehicles, retiring Congressman Ed Perlmutter (D-CO), sponsor of the legislation, and Sen. Schumer were unsuccessful in getting the bill over the finish line. In a final Hail Mary, Sen. Schumer attempted to include the language to the Omnibus, but compounded with the technical assistance report from the Department of Justice (DOJ) and ongoing media flurry, he and the Democratic party yet again came up empty-handed.

The question now is: who will carry the SAFE Banking Act and Rep. Perlmutter’s legacy in 2023? Many will look toward cannabis industry champions like Reps. Joyce, Mace, Earl Blumenauer (D-OR) and Brian Mast (R-FL). However, it would be worth considering other members of the CCC and some of the incoming freshmen, particularly those from a state with legal cannabis laws. It is also entirely possible that Sen. Jeff Merkley (D-OR) finds his own sponsor to carry his companion bill in the House since he has already announced that he looks forward to working on the legislation in the upcoming year. Regardless, it is highly likely that the SAFE Banking Act will be reintroduced in 2023 and considered throughout the year.

6. Other Measures

Other measures that are likely to reappear in 2023 are the Capital Lending and Investment for Marijuana Businesses (CLIMB) Act, Veterans Equal Access Act, the GRAM Act, Common Sense Cannabis Reform for Veterans, Small Businesses and Medical Professionals Act, VA Medicinal Cannabis Research Act and the Homegrown Act. Additionally, the passage of the Medical Marijuana and Cannabidiol Research Expansion Act and the advancement of many of these federal bills have opened the gates for new legislation related to medical and recreational cannabis, research, veterans’ access, financial services, criminal justice reform and social equity, and public health and safety to emerge.

For states with legal cannabis laws, bills related to enhancing the state’s medical or medical and recreational programs, preventing industry oversaturation and price gouging, expanding licensing opportunities, criminal justice reform, youth and advertising protections and impaired driving are likely to be introduced. States where cannabis ballot measures failed will likely see those measures resurface.

The continued growth of legalization across the country is all but inevitable. In the nearer term, the industry will focus on how to remain viable in the face of high taxes and oversupply in 2023. New Congressional leadership could lead to bipartisan cannabis legalization if enough members are willing to rally behind their colleagues who are pushing for cannabis legislation. While the road is long before we will see the full impact from President Biden’s Oct. 6 announcement, the action proves those in power cannot ignore the ever-growing numbers of Americans across party lines and demographics who agree that cannabis use should be legal and regulated.

Senate Majority Leader Chuck Shumer (D-NY), Sen. Cory Booker (D-NJ) and Sen. Ron Wyden (D-OR) introduced the Cannabis Administration and Opportunity Act (CAOA), a bill that seeks to decriminalize cannabis and end prohibition as we know it. About a year ago, the same lawmakers held a press conference where they unveiled their first draft of the CAOA, calling on the public for comments and input.

In that press conference last year, Sen. Booker emphasized the need to address social equity and restorative justice, laying out the foundation for what would soon be called the most comprehensive piece of cannabis legislation so far.

Sen. Schumer unveiling the Cannabis Administration and Opportunity Act last year.

According to the Minority Cannabis Business Association (MCBA), the bill succeeds in doing that, offering a number of provisions that would help those most impacted by cannabis prohibition, offer funding for equity programs, support for minorities in the cannabis market and more. “The CAO Act represents a giant leap forward in federal cannabis policy by outlining the most meaningful solutions to address issues facing minority cannabis businesses we’ve seen in a federal legalization bill to-date,” says Kaliko Castille, president of MCBA.

Notable provisions in the bill also include:

Removes cannabis from the Controlled Substances Act scheduling entirely.

Allows states to implement their own policies without the federal government interfering.

Allows cannabis businesses access to financial services, removes the threat of 280E tax code impacting normal business deductions.

Regulatory responsibility would fall under the authority of the Alcohol and Tobacco Tax and Trade Bureau (TTB), the Food and Drug Administration (FDA).

Immediate expungement for prior cannabis convictions and cancellation of any sentencing for those incarcerated for cannabis.

Raise allowable THC content in hemp from 0.3% to 0.7%.

Sets up a pilot program with the Small Business Administration (SBA) for minority-owned and economically disadvantaged cannabis businesses.

High taxes: Up to a 25% federal excise tax on top of state cannabis taxes.

Like this article and want to see more? Subscribe to our free newsletter here The cannabis industry could receive a significant boost if the recently introduced Capital Lending and Investment for Marijuana Businesses (CLIMB) Act passes Congress. The bipartisan bill was introduced by Rep. Troy A. Carter, Sr., a Democrat from Louisiana, and Rep. Guy Reschenthaler, a Republican from Pennsylvania. It is intended to boost the cannabis industry by creating greater access to capital, banking insurance and other business services. Unlike the SAFE Banking Act (which specifically addresses banking services for the cannabis industry), the CLIMB Act was introduced “to permit access to community development, small business, minority development and any other public or private financial capital sources for investment in and financing or cannabis-related legitimate businesses.”

Rep. Troy A. Carter, Sr.

Currently, the cannabis industry faces a serious dilemma with regard to accessing not only traditional banking services, but also essential capital and financing sources. The latest member of the cannabis bill alphabet soup attempts to remedy this by addressing two key issues.

First, the CLIMB Act would permit access to key “business assistance” programs from various financial institutions by prohibiting any federal agency from bringing any civil, criminal, regulatory or administrative actions against a business or a person simply because they provide “business assistance” to a cannabis state-legal company. The CLIMB Act defines “business assistance” broadly to include, among other things, management consulting work, accounting, real estate services, insurance or surety products, advertising, IT and other communication services, debt or equity capital services, banking or credit card services and other financial services.

This provision of the CLIMB Act would immediately create more access to traditional insurance, lending and credit. This broad protection would not only apply to private entities providing “business assistance,” but arguably means that the U.S. Small Business Administration (SBA) could not be penalized by Congress or another government agency for providing loans to state-legal cannabis companies. Moreover, currently the cannabis industry does not have access to use credit cards, as major credit card companies refuse to permit such transactions. The CLIMB Act could pave the way for major credit card providers to begin permitting cannabis transactions. Permitting the use of major credit cards like American Express, Mastercard and Visa could result in an increase in sales for cannabis retailers.

The second, and possibly the most important, aspect of the CLIMB Act is that it would amend the Securities and Exchange Act of 1934 to create a “safe harbor” for national securities exchanges like Nasdaq and the New York Stock Exchange (NYSE) to list cannabis companies and would permit the trading of these cannabis businesses stock. Currently, plant-touching cannabis companies with operations in the U.S. can only be listed on a Canadian-based exchange and can also only be traded in the U.S. via the over-the-counter (OTC) markets. Trading securities on the OTC markets does not provide the same level of security as securities traded on a national exchange like Nasdaq or NYSE. Specifically, the CLIMB Act delineates that the federal illegality of cannabis is not a bar to listing or trading of securities for legitimate cannabis-related businesses.

Rep. Guy Reschenthaler

This provision of the CLIMB Act has two immediate effects. First, the CLIMB Act would allow for U.S. cannabis companies currently listed in Canada to list on the Nasdaq or NYSE. Second, this provision would allow more traditional, “blue-chip” industry companies currently listed on Nasdaq or the NYSE who haven’t been able to operate within the cannabis industry as a plant-touching entity, to enter the cannabis industry as an active participant.

In announcing the CLIMB Act, Representative Reschenthaler stated that “American cannabis companies are currently restricted from receiving traditional lending and financing, making it difficult to compete with larger, global competitors. The CLIMB Act will eliminate these barriers to entry, and provide state-legal American cannabis companies, including small, minority, and veteran-owned businesses, with access to the financial tools necessary for success.”

It is important to note that the CLIMB Act, like the SAFE Banking Act, only represents one small, but important step toward cannabis reforms. Neither proposal would legalize, de-schedule or reschedule cannabis. Rather, the CLIMB Act addresses very real-world, operational issues facing the cannabis industry. With that in mind, the CLIMB Act would certainly provide much needed clarity for issues facing all cannabis companies.

Passage of the CLIMB Act is not a forgone conclusion, but rather is quite uncertain. Other pieces of cannabis-related legislation, like the SAFE Banking Act, have passed the House of Representatives multiple times without the U.S. Senate taking any action. Moreover, the CLIMB Act was introduced with only two legislative supporters.

By Tamara L. Kolb, Amy Bean, Caitlin Strelioff No Comments

As the legal cannabis market expands, banks and nonbank financial institutions (NBFIs) across the United States continue to explore how to safely provide banking and other financial services to cannabis-related businesses (CRBs) and other CRB ecosystem players. At the same time, these organizations are taking into account changes they might need to consider relative to their Bank Secrecy Act ( BSA), anti-money laundering (AML) and related compliance programs.

Regulatory conundrum

The Controlled Substances Act (CSA) identifies the cannabis plant and all its derivatives as a Schedule 1 controlled substance. Schedule 1 controlled substances have a “high abuse potential with no accepted medical use,” and they cannot be “prescribed, dispensed, or administered.” Because cannabis remains classified as a Schedule 1 controlled substance, the CSA “imposes strict controls on possession, manufacturing, distribution, and dispensing” of cannabis.

Under the Money Laundering Control Act of 1986 (MLCA) and the BSA as amended, covered banks and NBFIs are prohibited from providing financial services to businesses that are engaged in illicit activities. Because federal law prohibits the distribution and sale of cannabis, financial transactions involving CRBs are therefore deemed to be transactions that involve funds derived from illegal activities.

As of Feb. 3, 2022, 18 states, two territories, and the District of Columbia have enacted legislation to regulate cannabis for adult use. Thirty-seven states, the District of Columbia and four territories have approved comprehensive, publicly available medical and cannabis programs. Eleven states allow for the use of low-THC, high-CBD substances for medical reasons in limited situations or as a legal defense.

The growing divide between federal prohibition and state legalization of the cannabis industry creates a precarious position for federally regulated banks and NBFIs with the main concern involving exposure to legal, operational and regulatory risk. The situation begs the question: How might the federal government and regulators pursue and prosecute players in the legal cannabis industry?

The current economic trajectory predicts that retail sales of legal cannabis products in the U.S. will surpass an estimated $41.5 billion annually by 2025, and many banks and NBFIs are eagerly awaiting the federal green light to do business with CRBs without fear of prosecution or legal ramifications.

From 2018 forward, Congress has made several attempts to pass legislation that would protect CRBs when cultivating, distributing, marketing, and selling cannabis products in their state-legalized form. These efforts to declassify cannabis-related activity as a specified unlawful activity have thus far been unsuccessful.

The House passing the MORE Act back in 2020

Passage of the Secure and Fair Enforcement Banking Act of 2021 (SAFE Banking Act) and the Marijuana Opportunity Reinvestment and Expungement Act of 2021 (MORE Act) would enable banks and NBFIs to provide financial services to CRBs. The SAFE Banking Act would provide a safe harbor for banks and NBFIs that provide financial services to CRBs. The MORE Act would deschedule cannabis from the CSA entirely.

Questions to ask

Banks and NBFIs interested in providing financial services to CRBs should ask these questions:

Do we adequately understand our risk, and what are the implications for our organization? How should we augment our risk assessment process and our controls?

To what extent are we willing to accept the risk of banking CRBs? Do we have the ability to identify CRB customers, and if so, do we have any?

How should we advise the board of directors about setting risk appetite?

What customer due diligence (CDD) and enhanced due diligence (EDD) will we need to safely continue with existing customers and onboard new ones?

How will we monitor for unusual and suspicious activity? What will be the alerting and judgmental criteria?

How will our resource needs change so that we stay abreast of new processes and controls?

Risk appetite considerations

In order to determine whether to accept or prohibit CRBs, banks and NBFIs should identify the level of acceptable risk they are willing to take on. Several key components need to be considered, such as:

The board of directors’ stance on legal cannabis, given that good governance recommends and regulators expect that the board sets risk appetite

Cannabis laws in states within the customer footprint and the impact on customers’ communities

Risk profile, customer base, geographic location, products, and services

Relationship with regulators and any recent deficiencies or weaknesses in the BSA and associated compliance programs

Ability to implement appropriate controls and staffing

Developing a strategic road map

If the decision is made to bank CRBs, banks and NBFIs should perform an assessment of compliance maturity for existing BSA/AML program processes and controls to identify potential gaps and develop a strategic road map that helps the organization achieve its vision for future state compliance and sustainable operations.

A well-developed and well-articulated strategic road map visualizes what actions or key outcomes are needed to help organizations achieve their long-term goals. When creating the road map, banks and NBFIs need to demonstrate a keen understanding of their desired strategy, outcomes, markets, and products for onboarding and banking CRB customers. Specifically, banks and NBFIs need to define and explain how desired outcomes and business strategies create risk and exposure.

In addition to a road map, banks and NBFIs should develop and document a detailed risk-based approach that is aligned to the organization’s risk tolerance to determine necessary compliance steps when banking CRB customers.

Specifically, the following activities should be considered when developing a CRB banking program that meets regulatory expectations:

Identifying BSA/AML control gaps related to CRB risk identification and mitigation and formulating a plan to address them

Updating a board-approved policy framework

Updating detailed operating policies and procedures

Planning for capacity, developing job descriptions, and onboarding new personnel

Training for all three lines of defense, senior management, and the board

Developing and documenting a phased or full approach to acceptance of CRB customers

Developing and documenting a CRB program oversight policy

This framework is intended to help banks and NBFIs differentiate types of CRBs and their corresponding risks, and it separates CRBs into three tiers and details risks for each tier. The following exhibit summarizes the approach:

Risk framework by tier

Level

Risk

Tier 1

Direct

Tier 2

Indirect with substantial revenue from Tier 1

Tier 3

Indirect with incidental revenue from Tier 1

Source: CRB Monitor

Even the most conservative of risk appetites equivalent to outright prohibition is not devoid of significant risk considerations. Residual risk frequently encompasses a large number of indirect connections in the total CRB ecosystem. Common examples are printers, lawyers, accountants, landlords, and even utilities and taxing authorities, and all of these are subject to regulatory scrutiny and, importantly, visibility to law enforcement. Also, policies to prohibit or restrict will be audited and examined for compliance, and exceptions will require explanations.

This panorama necessitates expertise and prudence in identifying and evaluating risks within the many layers of CRBs. For example, consider a bank or NBFI that banks a CRB’s employee or vendor. If a bank fails to properly implement controls that would allow it to identify and mitigate risk associated with banking CRBs, it will be susceptible to severe violations of the BSA, including civil money penalties, criminal penalties, and regulatory enforcement actions.

Implementing necessary precautions

A well-developed road map should consider and implement the following activities:

Understanding the most current state and federal cannabis laws and regulations to ensure the bank or NBFI’s compliance

Understanding the local, state, or tribal program to ensure CRB customers are compliant with the program

Implementing a CRB risk assessment

Implementing executive approval practices for direct CRBs

Developing adequate risk ratings (possibly through a risk-based, tiered approach) and corresponding monitoring for CRB customers that includes:

Integrating various customer onboarding and AML solutions at both onboarding and periodic levels

Scheduling regular reviews to include recurring enhanced due diligence, site visits, and transaction monitoring

Monitoring for suspicious activity, including red flags, via open sources for adverse information about the CRB customers and related parties such as beneficial owners

Performing adequate CDD and EDD that will validate that the CRB-offered products, services, and programs are compliant with most current state laws and regulations by:

Collecting appropriate documentation as evidence of compliance, perhaps including a comprehensive onboarding questionnaire, beneficial ownership information, and contracts for the growing, harvesting, transporting and processing of the product

Reviewing applications and supporting documentation used to obtain a legal cannabis state license

Understanding the normal and expected activity of the organization’s CRB customers and their product usage

Developing adequate training programs and governance and oversight programs to address this customer type by:

Updating existing policies and procedures to review inherent risk presented by banking CRB customers

Updating annual training for employees

Auditing initial program design and periodic operational effectiveness

Moving forward cautiously

The ins, outs, and unknowns of cannabis banking are complex, and they require banks and NBFIs to be extremely vigilant with current policy and aware of new developments. Overall, the idea of creating a cannabis program might seem like a daunting task, but with appropriate guidance and care, organizations can provide services in compliance with laws and regulations.

Crowe disclaimer: Qualified organizations only. Independence and regulatory restrictions may apply. Some firm services may not be available to all clients. Given the continued evolution and inconsistency of various state and federal cannabis-related laws, any company should seek competent legal advice relating to its involvement in the cannabis industry, including when considering a potential public offering as a cannabis-related company.

Federal regulations have made compliant credit processing in the cannabis industry difficult to achieve. As a result, most cannabis retailers operate a cash-only model, limiting their ability to upsell customers and placing a burden on customers who might rather use credit. While some dispensaries offer debit, credit or cashless ATM transactions, regulators and traditional payment processors have been cracking down on these offerings as they are often non-compliant with regulations and policies.

Two companies, KindTap Technologies and Aeropay, are addressing the cannabis industry’s payment processing challenges with innovative digital solutions geared towards retailers and consumers.

We interviewed both Cathy Corby Iannuzzelli, president at KindTap Technologies and Daniel Muller, CEO at Aeropay. Cathy co-founded KindTap in 2019 after a career in the banking and payments industries where she launched multiple financial and credit products. Daniel founded AeroPay in 2017 after a career in digital product innovation, most recently at GPShopper (acquired by Financial), where he oversaw the design and development of over 300 web and mobile applications for large scale Fortune 500 companies.

Green: What is the biggest challenge your customers are facing?

Cathy Corby Iannuzzelli, co-founder and president at KindTap Technologies

Iannuzzelli: Our customers include both cannabis retailers and their end consumers. As long as cannabis is illegal at the federal level, normal payment solutions such as debit and credit cards cannot be accepted for cannabis purchases. This has resulted in heavy cash-based sales and unstable, transient work-around ATM payment solutions that can be ripped out with little notice, disrupting the entire business. The lack of a mature payment network to support retail payments for cannabis purchases is a huge challenge for all stakeholders. Cannabis retailers bear the high cost and safety issues of operating a heavily cash-based retail business. Consumers encounter several friction points that require them to change their behavior when purchasing cannabis relative to how they purchase everything else.

Muller: Our cannabis business customers have faced a constantly changing and, frankly, exhausting financial services environment. From the need to move and manage large amounts of cash, to card workarounds, added to the disappointment from legislation around the SAFE Banking Act, these inconsistencies have acted as a roadblock to their potential growth and profitability. Aeropay is in the position to be a stable, long-term, reliable payments partner ready to help them scale their businesses. We believe these opportunities are limitless.

Green: What geographies have got your attention and why?

Daniel Muller, CEO and founder of Aeropay

Iannuzzelli: KindTap’s focus is on the U.S. market where federal policy has created the need for alternatives to traditional payment networks. KindTap is available in every U.S. state where cannabis is legally sold. In terms of our distribution channels, KindTap’s digital payment solution was brought to market during the COVID-19 pandemic when curbside pick-up and delivery became critically important. These channels are where the exchange of cash at pick-up posed the greatest security risk to employees and customers. Our early integrations were with e-commerce platforms focused on delivery and pick-up orders, and our integration partners have strong customer bases in California and the northeast. So, while KindTap can provide its “Pay Later” lines of credit and “Pay Now” bank account solutions anywhere, we have heavier penetration in those regions.

Muller: California, for its established tech culture and how it plays into the cannabis industry – your product simply has to live up to their tech standards to be heard. Also, Chicago, our headquarters, with its newly emerged commitment to financing the cannabis industry and bringing with it a more traditional business approach. In Chicago, you have to have elevated standards of professional practices in any industry you enter. And of course, we love to watch emerging markets like New York and Florida as they head towards adult-use and what shape cannabis and payments will take.

Green: What are the broader industry trends you are following?

Iannuzzelli: We continue to see a strong transition from cash and ATM transactions over to digital payments. Since KindTap has a fully-integrated payment “button” on e-commerce checkout screens, the adoption rate of end consumers to that one-click experience is quite strong. We are also seeing trends of more “express lines” in the retail environment – for those KindTap users who paid online/ahead – and faster/safer delivery experiences to people’s homes since there is no longer the need to collect any payment upon delivery. We are firm believers in the delivery/digital payments combination and a strong increase of that trend as more states allow for delivery.

Muller: The cannabis industry is starting to normalize payments and mirror traditional online and brick-and-mortar. With bank-to-bank (ACH) payments, cannabis businesses can now offer modern customer shopping experiences including pre-payment for delivery orders without the need for a cash exchange at the door, offering the option to buy online pickup in-store and contactless in-store QR scan-to-pay customer experiences. With these familiar and customer-driven options now available, we are seeing widespread adoption, as well as meaningful increases in spend and returning customers.

Green: Thank you both. That concludes the interview!

About KindTap: KindTap Technologies, LLC operates a financial technology platform that offers credit and loyalty-enabled payment solutions for highly-regulated industries typically driven by cash and ATM-based transactions. KindTap offers payment processing and related consumer applications for e-commerce and brick-and-mortar retailers. Founded in 2019, the company is backed by KreditForce LLC plus several strategic investors, with debt capital provided by U.S.-based institutions. Learn more at kindtaptech.com.

About AeroPay: AeroPay is a financial technology company reimagining the way money is moved in exchange for goods and services. Frustrated with the current, antiquated payments landscape, we believe there is a better way to pay and a better way to get paid. AeroPay set out to build a payments platform that works for all- businesses, consumers, and their communities. Learn more at aeropay.com.

The cannabis industry is an unprecedented industry and one under constant review and control. Following the November 2020 elections, fifteen states and Washington DC have legalized adult use cannabis, a number that will continue to grow as legalization slowly becomes more widely adopted in other states. Beyond that, a continuously growing number of states allow residents to purchase legal medicinal cannabis, and many have also decriminalized adult use. However, it still remains a Schedule I substance under the Controlled Substances Act and is therefore illegal on all accounts at the U.S. federal level, which creates a number of issues for businesses in the cannabis industry duly operating in states where it has been legalized.

Not only is it difficult for cannabis companies to avail themselves of alternative banking solutions, but there are also obstacles in place preventing these companies from taking advantage of notable tax deductions. The primary obstacle being Internal Revenue Code (IRC) Section 280E.

What is Section 280E?

Section 280E is a relatively short code section, only 77 words to be exact, but it carries significant weight and can have a debilitating effect on the taxable income of marijuana [sic] related businesses (MRB). Section 280E of the IRC prohibits taxpayers who are engaged in the business of trafficking certain controlled substances, including cannabis, from deducting typical business expenses associated those activities. Section 280E, which was enacted in 1982 during the “War on Drugs” era, has become increasingly relevant for cannabis businesses. The cannabis industry has grown substantially in recent years with annual market values expected to reach $30 billion by 2025.

However, while Section 280E greatly restricts the tax deductions of state-legal cannabis businesses, there is some reprieve. Current IRC provisions permit state-legal cannabis businesses, including growers, producers, wholesalers or retailers, to deduct the Cost of Goods Sold (COGS) in computing their US federal income tax liability, despite the application of Section 280E.

Impact of Section 280E on Businesses

What does Section 280E mean for cannabis businesses today? It is intended to prevent dealers from claiming tax deductions for their business expenses, interpreted to include state-legal cannabis businesses, reduced deductions that result in increased taxable income and MRBs will face higher federal tax rates.

The IRC disallows any deductions or credits paid or incurred during a tax year if those deductions or credits relate to trafficking controlled substances. The courts have taken the position that the term “trafficking” in this case means “engaging in a commercial activity – that is, to buy and sell regularly.” Simply, the law denies cannabis businesses any U.S. federal income tax deduction for ordinary and necessary business expenses, despite being duly licensed as a legal business in their state of operation.

Typically, the ability to deduct ordinary business expenses means that a business is subject to federal tax on its net income (i.e., gross receipts minus expenses). However, the definition of Section 280E and the classification of cannabis as a Schedule I substance severely hinders legal cannabis companies from taking advantage of tax deductions for actual economic expenses incurred in the ordinary course of business, which results in a significantly higher effective tax rate as compared to other businesses.

Legal Actions and Challenges to Section 280E

There have been court challenges and concessions made to Section 280E. Specifically, the 2007 court case Californians Helping to Alleviate Medical Problems, Inc., v. Commissioner. This court case reinforced the precedence that Section 280E does not apply to cost of goods sold. The Internal Revenue Service (IRS) defines cost of goods sold to be “expenditures necessary to acquire, construct or extract a physical product which is to be sold.” Generally, for a retail MRB, this means that the direct cost of acquiring cannabis products for resale. Deductions for rent, utilities, wages, insurance and other operating costs common to ordinary businesses are generally disallowed. New York State has specifically indicated that it intends to follow Section 280E for its own income tax calculations, disallowing these same deductions against New York taxable income

Tax Court and Section 280E

The Tax Court has also been aggressive in tamping down efforts by MRBs to separate cannabis related and non-cannabis related activities. The courts argue that these separate activities constitute a single trade or business when they share a close and inseparable organizational and economic relationship. In addition, the risk of cannabis related activities tainting a taxpayer’s other business concerns exists if services or employees are shared between an MRB and a non-MRB. Allocation of expenditures to cost of goods sold, as well as any allocations of costs between MRB and non-MRB entities, need to be well thought out and supported by defensible tax and accounting positions.

The Future of MRBs and Section 280E

All indications point to an increased frequency of IRS audits of MRBs compared to audits of non-cannabis related businesses. Therefore, documenting the methodology behind the calculation of costs of goods sold is even more important for MRBs. It is vital to consult with a tax advisor to ensure you are maximizing your cost of goods sold deductions and preparing the best documentation possible to support your 280E tax positions.

Disclaimer: The information presented in this article should not be considered legal advice or counsel and does not create an attorney-client relationship between the author and the reader. If the reader of this has legal or accounting questions, it is recommended they consult with their attorney or accountant.

Cannabis is still federally illegal and is included on Schedule 1 of the Controlled Substances Act (CSA), along with such other substances as heroin, fentanyl and methamphetamines.1 It is a federal crime to grow, possess or sell cannabis.

Despite being federally illegal, 36 U.S. states and the District of Columbia have legalized the sale and use of cannabis for medical and/or adult use purposes,2 and both direct and indirect cannabis-related businesses (CRBs) are growing at a rapid rate. Revenue from medical and adult use cannabis sales in the US in 2019 is estimated to have reached $10.6B-$13B and is on track to reach nearly $37B in 2024.3

Because the sale of cannabis is federally illegal, financial institutions face a dilemma when deciding to provide services to CRBs. Should they take a significant legal risk or stay out of the market and miss out on a significant revenue opportunity? So far, the vast majority of financial institutions have been unwilling to take the risk, resulting in a dearth of options for CRB’s. Until recently, cannabis business operators had few options for financial services, but times are changing.

This piece will discuss current trends in banking for cannabis-related businesses. We will cover differences in legality at state and federal levels, complexities in dealing in cash versus digital currencies, Congressional actions impacting banking and CRBs and how banking is changing. The explosion of state legalization of cannabis over the past several years has had a strong ripple effect across the US economy, touching many industries both directly and indirectly. Understanding the implications of doing business with a CRB is both challenging and necessary.

Feds Versus States

Money laundering is the process used to conceal the existence, illegal source or illegal application of funds.4 In 1986 Congress enacted the Money Laundering Control Act (MLCA), which makes it a federal crime to engage in certain financial and monetary transactions with the proceeds of “specified unlawful activity.”5 Therefore, CRB transactions are technically illegal transactions under the MLCA.

Financial institutions therefore face a risk of violating the MLCA if they choose to do business with CRBs, even in states where cannabis operations are permitted. In addition, financial institutions could also face criminal liability under the Bank Secrecy Act (BSA) for failing to identify or report financial transactions that involve the proceeds of cannabis businesses operating legally under state law.6

Federal authorities continued to aggressively enforce federal cannabis laws

In short, because cannabis is illegal at the federal level, processing funds derived from CRBs could be considered aiding and abetting criminal activity or money laundering. States, however, began legalizing cannabis in 1996, and by 2009, thirteen states had laws allowing cannabis possession and use.7 Despite this legislation, federal authorities continued to aggressively enforce federal cannabis laws.8 That changed under the Obama administration when, shortly after being elected, President Obama stated that his administration would not target legal CRB’s who were abiding by state laws.[9] In an attempt to provide clarity in this murky environment, beginning in 2009, the Department of Justice (DOJ) issued three memos designed to guide federal prosecutors in this area. However, none of the DOJ memos issued from 2009 through 2013 addressed potential financial crime related to the legal sale or distribution of cannabis in states allowing the use of medicinal or recreational cannabis.

To assist financial institutions in navigating potential financial crime implications of banking CRBs, the Financial Crimes Enforcement Network (FinCen) issued guidance in 2014 that clarified how financial institutions could conduct business with CRBs and maintain compliance with their Bank Secrecy Act requirements (2014 Guidance).9 According to the 2014 Guidance, financial institutions may choose to interact with CRBs based on factors specific to each institution, including the institution’s business objectives, the evaluated risks associated with offering such services, and its ability to manage those risks effectively.

The 2014 Guidance requires those who choose to provide services to CRBs to design and implement a thorough customer due diligence review that includes, in part, analyzing the licensing of the entity, developing an understanding of the business operations of the entity, and ongoing monitoring of the entity.9 In addition, financial institutions are required to file a Suspicious Activity Report (SAR) for every transaction they process for a CRB, should they choose to accept the business.

Although the 2014 Guidance does outline a path for financial institutions to engage with CRBs, it does not change federal law and, therefore, does not eliminate the legal risk to financial institutions.10 By its very nature, the 2014 Guidance was a temporary fix, subject to changing views of different administrations, evidenced by the fact that all three of the DOJ guidance documents noted above were rescinded by then Attorney General Jeff Sessions on January 4, 2018.12 The DOJ enforcement posture could change once again in a Biden administration. Biden is on record as favoring decriminalization, and Attorney General candidate Merrick Garland has stated that if confirmed he will deprioritize enforcement of low-level cannabis crimes. Garland also believes using limited government resources to pursue prosecution of cannabis crimes states where cannabis is legal does not make sense.12

Because of the uncertainty and high risk, most banks remain unwilling to serve CRBs. Those that do serve CRBs charge exorbitant fees (fees of $750-$1,000 or more per account per month are not uncommon), pricing many smaller operators out of the financial services market.

Cash is King – Or Is It?

Cannabis operators have discovered the old adage “cash is king” is not necessarily true when it comes to the cannabis space. Bank-less CRBs are forced to utilize cash to pay business expenses, which can be particularly difficult. Utility companies, payroll companies, and taxing authorities are just some of the providers that are difficult, if not impossible, to pay in cash. For example, cannabis operators have been turned away from IRS offices when attempting to pay large federal tax obligations in cash. Likewise, cannabis operators have been unable to utilize payroll processing companies to administer payroll and benefits for their businesses because the processors won’t take cash. CRBs can’t use Amazon or other online retailers because online providers cannot accept cash.

Because dealing in cash is so difficult, CRB operators look for workarounds such as using personal credit/debit cards to purchase business equipment and supplies. This doesn’t eliminate the cash problem, however, because the credit card holder will likely have to accept cash as reimbursement. Such transactions could be considered an attempt to hide the source of the cash, which is, by definition, money laundering.

CRBs often have large sums of money onsite

Some bank-less CRBs try to skirt the system by obtaining bank accounts in the name of management companies or other entities one step removed from the actual business. While operators often choose this route in an effort to streamline business and operate out of the shadows, it again runs afoul of banking laws. Transferring cannabis related financial transactions to another entity is actually the very definition of money laundering – which, as noted above, is defined as the process used to conceal the existence or source of “illegal” funds.

In addition to the difficulties in making payments or purchasing business supplies, operating in a cash-heavy environment poses significant safety risks for cannabis operators. CRBs often have large sums of money onsite and transport large sums of cash when purchasing product or paying bills, making them a target for robbery. In 2017, there was a spate of dispensary robberies across the Phoenix Metro area, including one at Bloom Dispensary that took place during operating hours.13

Managing all that cash increases the cost of doing business as well, in the form of increased labor, insurance, and security costs. Cash must be counted and double counted, which can be time consuming for staff, not to mention the time it takes to deliver physical cash payments to hither and yon. Ironically, lack of banking significantly decreases transparency and clouds the waters of compliance, as operating strictly in cash makes it easier to manipulate reported financial results.

Potential Congressional Solutions

In recent years Congress has undertaken several efforts to pass legislation designed to address the state/federal divide on cannabis, which would likely clear the way for financial institutions to provide services to CRBs, including:

R. 1595 – Secure and Fair Enforcement Banking Act of 2019 (“SAFE Act”);

1028 & H.R. 2093 – Strengthening the Tenth Amendment Through Entrusting States Act (STATES Act); and

2227 – Marijuana Opportunity Reinvestment and Expungement Act of 2019 (MORE Act).

The climate in Washington DC, however, did not allow any of these initiatives to pass both houses of congress. Had any been sent to the White House, President Trump was unlikely to sign them into law.

The cannabis industry has new reason to believe reform is on the horizon with shift in political leadership in the White House and Senate. Newly anointed Senate Majority Leader Chuck Schumer recently committed to making federal cannabis reform a priority, and President Biden appears committed to decriminalization, reviving the hope of passage of one of these pieces of legislation.

The Changing Banking Landscape

Even though there is little in the way of formal protections for financial institutions, and with the timeline for a legislative fix unknown, an increasing number of banks are working with cannabis operators.

According to FinCen statistics, there were approximately 695 financial institutions actively involved with CRBs as of June 30, 2020. It is important to note that these statistics are based on SAR filings, which banks are required to file when an account or transaction is suspected of being affiliated with a cannabis business. However, some of these SARs may have been generated on genuine suspicious activity rather than on a transaction with a known cannabis customer.

Number of Depository Institutions Actively Banking Cannabis-Related Businesses in the United States (Reported in SARS)14

There are arguably more banking institutions offering services to CRBs than ever before. The challenges for CRBs are (1) finding an institution that is willing to offer services; (2) building/maintaining a compliance regime that will be acceptable to that institution; and (3) cost, given the high fees associated with these types of accounts.

How CRBs Get Accepted by Banks

The gap between CRBs’ need for banking and the financial services providers’ sparse and expensive offerings to the sector has created an opportunity for third-party firms to intervene and provide a compliance structure that will satisfy the needs of the financial institutions, making it easier for the CRB to find a bank.

These third-party firms perform extensive BSA-compliant due diligence on applicants to ensure potential customers are following FinCen guidance required to receive banking services. After the completion of due diligence, they connect the CRBs with financial institutions that are willing to do business with CRBs and provide checking/savings accounts, check writing capability, and merchant processor accounts. These firms often provide additional services such as armored car and cash vaulting services. Some of these firms also offer vendor screening, pre-approving vendors before any payments can be made.

One such firm, Safe Harbor Private Banking, started as a project implemented by the CEO of Partners Credit Union in Denver, Colorado, who set out to design a cannabis banking program that would allow Partners to do business with Colorado CRBs.15 The program was successful and has since expanded into other states who have legalized cannabis. Other operators include Dama Financial and NaturePay.

While these services offer hope for many CRBs, the downside is cost. These services perform the operations necessary to find, open, and maintain a compliant bank account; however, the costs of compliance are still high, pricing some small operators out of the market.

Is Digital Currency an Answer?

Digital currency is also making its way into the cannabis world. Digital currency, or cryptocurrency, is a medium of exchange that utilizes a decentralized ledger to record transactions, otherwise known as a blockchain. One of the largest benefits of blockchain is that it is a secure, incorruptible digital ledger used for, among other things, financial transactions.16 Blockchain technology offers CRBs a transparent and immutable audit trail for business and financial transactions. Several cannabis-specific cryptocurrencies have sprung up in the past several years, including PotCoin, CannabisCoin, and DopeCoin, to name a few.

In July 2019, Arizona approved cryptocurrency startup ALTA to offer services to the state’s medical cannabis operators.17 ALTA describes itself as a “digital payment club where cash-intensive businesses pay each other using digital tokens instead of cash.”18 ALTA members purchase digital tokens that are used to pay other members using a proprietary blockchain based system. The tokens are redeemable for US dollars at a stable rate of 1:1, and CRBs do not need a bank account to participate in the ALTA program.

ALTA proposes to pick up members’ cash and exchanges it for tokens, which are then used to pay other members for goods and services. Tokens may be redeemed for cash at any time.18 The company has been approved by the Arizona State Attorney General, and one of the first members they hope to enlist is the Arizona Department of Revenue (ADOR). Enlisting ADOR into the program would allow dispensary members to pay state taxes digitally rather than hauling large amounts of cash to ADOR offices.

Similarly, Nevada recently contracted with Multichain Ventures to supply a digital currency solution to the Nevada cannabis industry. Nevada Assembly Bill 466 requires the state create a pilot program to design a “closed loop” system like Venmo in an effort to reduce cash transactions in the cannabis sector. Like ALTA, Nevada’s proposed system will convert cash to tokens which can then be transacted between system participants.19

While both proposals are promising for Arizona and Nevada CRBs, the timeline as to when, or if, these offerings will come online is unknown. Action on cannabis reform at the federal level may render these options moot.

Looking to the Future

Although states are legalizing cannabis in one form or another in growing numbers, the fact that cannabis is still federally illegal poses a significant barrier to accessing the financial services market for CRBs. While most banks are still reluctant to offer services to this rapidly growing industry, there are more banks than ever before willing to participate in the cannabis industry. Recent changes in leadership in Washington DC offer a positive outlook for cannabis reform at the federal level.

As the “green rush” continues to envelop the country, financial services options available to CRBs are slowly growing. Many new options are now available to help CRBs find a bank, develop compliance programs, and manage the cash related problems encountered by most CRBs. However, these solutions may be out of reach for the budget-conscious small operator. Also, there are a number of cryptocurrency solutions designed specifically for CRBs; however, when, or if, these solutions will gain significant traction is still unknown.

References

Controlled Substances Act, 21 U.S.C., Subchapter I, Part B, §812.

“State Marijuana Laws”; National Conference of State Legislatures, February 19, 2021.

“Exclusive: US Retail Marijuana Sales On Pace to Rise 40% in 2020, near $37B by 2024”. Marijuana Business Daily, June 30, 2020.

Kaufman, Irving. “The Cash Connection: Organized Crime, Financial Institutions, and Money Laundering”. Interim Report to the President, October 1984.

S. Code § 1956 – Laundering of Monetary Instruments.

Rowe, Robert. “Compliance and the Cannabis Conundrum.” ABA Banking Journal, September 11, 2016.

“History of Marijuana as a Medicine – 2900 BC to Present”. ProCon.org, December 4, 2020.

Truble, Sarah and Kasai, Nathan. “The Past – and Future – of Federal Marijuana Enforcement”. org, May 12, 2017.

Sessions, Jefferson B. “Memorandum for All United States Attorneys”. January 4, 2018.

“Attorney General Nominee Garland Signals Friendlier Marijuana Stance”. Marijuana Business Daily, February 22, 2021.

Stern, Ray. “Robbers Hitting Phoenix Medical Marijuana Dispensaries: Is Bank Reform Needed?” The Phoenix New Times, April 11, 2017.

FinCen Marijuana Banking Update, June 30, 2020.

Mandelbaum, Robb. “Where Pot Entrepreneurs Go When the Banks Just Say No.” The New York Times, January 4, 2018.

Rosic, Ameer. “What is Blockchain Technology? A Step-by-Step Guide for Beginners.” com, 2016.

Emem, Mark. “Marijuana Stablecoin Asked to Play in Arizona Fintech Sandbox.” CCN.com, October 25, 2019.

http:\\Whatisalta.com\

Wagner, Michael, CFA. “Multichain Ventures Secures Public Sector Contract with Nevada to Supply Tokenized Financial Ecosystem for the Legal Cannabis Industry”, January 26, 2021.

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

We use tracking pixels that set your arrival time at our website, this is used as part of our anti-spam and security measures. Disabling this tracking pixel would disable some of our security measures, and is therefore considered necessary for the safe operation of the website. This tracking pixel is cleared from your system when you delete files in your history.

We also use cookies to store your preferences regarding the setting of 3rd Party Cookies.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.