Few people will disagree that financial compliance isn’t the most exciting topic within the cannabis industry. But compliance is, and always will be, the engine grease to the legal cannabis market. Cannabis operators have the arduous task of dealing with multiple layers of compliance, both operational (maintaining and adhering to regulations enforced by the state licensing board) and financial. These compliance measures include managing everything from seed-to-sale systems for all plant-related activity to on-site requirements like facility access points and alarms systems to name a few.

With complex compliance requirements for the business, the last thing cannabis operators want to think about is financial compliance. We created Confia on this notion. Just as cannabis regulators impose the tracking of plants through the supply chain via a seed-to-sale system, we have developed a storyboard similarly designed to follow the money, which is the equivalent of a transaction-to-deposit system.

Having experience in regulatory technology, artificial intelligence and machine learning, we’ve been fortunate enough to work with some of the world’s largest banks across multiple countries. This experience has afforded us the luxury of working alongside regulators, chief compliance officers and chief risk officers, understanding how risk is perceived by financial institutions and how it ought to be mitigated. It was this access and knowledge that allowed us to effectively reform, enhance and improve the antiquated BSA programs with a technology-enabled process. Leveraging technology is a necessity, almost a requirement, for the cannabis industry as legalization nears and banking access begins to broaden.

Jamming cannabis requirements into an existing BSA program doesn’t scale well. BSA programs are very manual, descriptive and process oriented. So, we’ve taken our prior experience and success in banking to form Confia, distilling the complexities and simplifying the deliverables surrounding cannabis banking compliance. To best articulate cannabis banking requirements, I break it down into three pillars.

Pillar One: KYC-Enhanced Due Diligence

The first pillar is the client-onboarding bucket or KYC – Know Your Customer. In the complex world of cannabis banking, banks must know and understand their clients to great depths. It’s not enough to simply know that the client exists; you also have to understand whether or not that client could be a potential risk to the bank, and one step further, the financial system. Cannabis is a high-risk industry, so the KYC requirement is escalated to a deeper diligence and review, called Enhanced Due Diligence (EDD).

Cannabis is a high-risk industry so extra due diligence is needed

Banks need to know and understand their customers’ story, and all the key parties (officers, directors, and those with key decision-making powers or access to the bank accounts) within that organization. This includes reviewing personal, business, and legal history – not to mention watchlists and negative news presence. An initial onboarding review must then be followed with daily screening and monitoring of all watchlists and adverse media. Typically, banks do KYC refreshes every three years. In cannabis, a full refresh should be done annually with the daily monitoring systems in place.

The high-risk nature of the industry also requires a level of diligence on all parties to a transaction, even if one of the parties, whether a payer or recipient, is not a client of your bank. Unlike traditional banking sectors, reliance on other banks’ KYC programs is far less defensible in the cannabis industry.

Pillar Two: Transactional Monitoring & Detection

Tracking and monitoring the actual financial transactions comprises the second pillar required for cannabis banking. At Confia, we have focused on streamlining processes, so the cannabis operator can seamlessly support the compliance obligation for every transaction. A bank must demonstrate supporting documentation for every cannabis transaction, and gathering such information is a large undertaking in and of itself and can pose future issues if not done properly, see the pitfalls for lack of compliance. Banks are obligated to understand the nature and reason for each transaction, the source of funds, ensure cannabis licenses are in good standing for all parties, and collect evidence such as accounting records and seed-to-sale data.

Core to transaction monitoring in the traditional sense, is the overarching support through anomaly detection. Relying on information is important, but testing those inputs keeps everyone honest. It is important to evaluate transactions from a holistic point of view relative to peers and relative to the general contents of a transaction. This anomaly detection layer is your last line of defense, and as new information is collected, it continues to refine itself.

Pillar Three: Filing and Reporting Requirements

The third component to compliant cannabis banking is regulatory filing and reporting. Once a client is onboarded, the account requires an initial suspicious activity report or SAR-Initial within 30 days of that client being approved by the bank. Then, a report must be filed every 90 days after that for all the transactions of that cannabis operator. Banks must file the SAR-Initial and the Continuing-SAR reports for each cannabis client they have.

The high-risk nature of the industry requires a level of diligence on all parties to a transaction

Solutions like Confia automate the filing process and support the filing with transactional data evidenced on our distributed ledger of record. This provides immutable audibility and simplifies the process for all parties involved.

Compliance Requirements After US Legalization

The anticipation of federal legalization and banking reform bills has many operators hoping for easier banking. Yet, in my opinion, regulatory oversight and audits will likely increase after such reform or legalization. As other financial institutions start to support cannabis, it will inadvertently create greater opportunity and expose the financial system to nefarious or illegitimate transaction activity. This is why cannabis banking will be carefully monitored by regulators, and more so, why banks will be slow and pragmatic in standing up their internal cannabis banking programs. Some banks may forever avoid the cannabis industry due to the known pitfalls of an industry specific program, while others may simply mitigate the possible exposure to reputational risk.

Choose Wisely: Pitfalls for Lack of Compliance

Financial compliance is the responsibility and duty of the banks, but the real losers and result of non-compliance always fall on the cannabis operators. Regulatory action against an institution may result in the bank shutting down its cannabis program or may require them to complete a remediation of all their cannabis transactions for a certain period from its clients. At the end of the day, regardless of action, the cannabis operator is the one being punished. Operators either lose their bank account and have business massively disrupted, or they are asked to provide all the compliance docs for a historic period, which is a huge undertaking and operational distraction, ultimately impacting business and productivity. So, choose your banking partner wisely.

Summarizing Key Banking Requirements

In summary, banking in the cannabis industry will undoubtedly remain a high-risk industry, with or without legalization. Although banking opportunities may expand as US policies change, there will be continued compliance and regulatory requirements for the foreseeable future.

Onboarding and ongoing screening are critical

Evidence for every transaction is a significant portion of compliance and must not be dismissed

Evaluating activity with broader strokes is essential in mitigating against money laundering

Managing the staggered filing timelines and due dates for each client

Compliance is the most crucial factor in cannabis banking at this point. It cannot be overlooked or taken for granted. Cannabis operators must take an active role in evaluating the compliance programs of their financial providers. To open a bank account is one thing, but the consideration and effort that goes into keeping a bank account is the difference that will protect your business in the long run.

Cannabis is still federally illegal and is included on Schedule 1 of the Controlled Substances Act (CSA), along with such other substances as heroin, fentanyl and methamphetamines.1 It is a federal crime to grow, possess or sell cannabis.

Despite being federally illegal, 36 U.S. states and the District of Columbia have legalized the sale and use of cannabis for medical and/or adult use purposes,2 and both direct and indirect cannabis-related businesses (CRBs) are growing at a rapid rate. Revenue from medical and adult use cannabis sales in the US in 2019 is estimated to have reached $10.6B-$13B and is on track to reach nearly $37B in 2024.3

Because the sale of cannabis is federally illegal, financial institutions face a dilemma when deciding to provide services to CRBs. Should they take a significant legal risk or stay out of the market and miss out on a significant revenue opportunity? So far, the vast majority of financial institutions have been unwilling to take the risk, resulting in a dearth of options for CRB’s. Until recently, cannabis business operators had few options for financial services, but times are changing.

This piece will discuss current trends in banking for cannabis-related businesses. We will cover differences in legality at state and federal levels, complexities in dealing in cash versus digital currencies, Congressional actions impacting banking and CRBs and how banking is changing. The explosion of state legalization of cannabis over the past several years has had a strong ripple effect across the US economy, touching many industries both directly and indirectly. Understanding the implications of doing business with a CRB is both challenging and necessary.

Feds Versus States

Money laundering is the process used to conceal the existence, illegal source or illegal application of funds.4 In 1986 Congress enacted the Money Laundering Control Act (MLCA), which makes it a federal crime to engage in certain financial and monetary transactions with the proceeds of “specified unlawful activity.”5 Therefore, CRB transactions are technically illegal transactions under the MLCA.

Financial institutions therefore face a risk of violating the MLCA if they choose to do business with CRBs, even in states where cannabis operations are permitted. In addition, financial institutions could also face criminal liability under the Bank Secrecy Act (BSA) for failing to identify or report financial transactions that involve the proceeds of cannabis businesses operating legally under state law.6

Federal authorities continued to aggressively enforce federal cannabis laws

In short, because cannabis is illegal at the federal level, processing funds derived from CRBs could be considered aiding and abetting criminal activity or money laundering. States, however, began legalizing cannabis in 1996, and by 2009, thirteen states had laws allowing cannabis possession and use.7 Despite this legislation, federal authorities continued to aggressively enforce federal cannabis laws.8 That changed under the Obama administration when, shortly after being elected, President Obama stated that his administration would not target legal CRB’s who were abiding by state laws.[9] In an attempt to provide clarity in this murky environment, beginning in 2009, the Department of Justice (DOJ) issued three memos designed to guide federal prosecutors in this area. However, none of the DOJ memos issued from 2009 through 2013 addressed potential financial crime related to the legal sale or distribution of cannabis in states allowing the use of medicinal or recreational cannabis.

To assist financial institutions in navigating potential financial crime implications of banking CRBs, the Financial Crimes Enforcement Network (FinCen) issued guidance in 2014 that clarified how financial institutions could conduct business with CRBs and maintain compliance with their Bank Secrecy Act requirements (2014 Guidance).9 According to the 2014 Guidance, financial institutions may choose to interact with CRBs based on factors specific to each institution, including the institution’s business objectives, the evaluated risks associated with offering such services, and its ability to manage those risks effectively.

The 2014 Guidance requires those who choose to provide services to CRBs to design and implement a thorough customer due diligence review that includes, in part, analyzing the licensing of the entity, developing an understanding of the business operations of the entity, and ongoing monitoring of the entity.9 In addition, financial institutions are required to file a Suspicious Activity Report (SAR) for every transaction they process for a CRB, should they choose to accept the business.

Although the 2014 Guidance does outline a path for financial institutions to engage with CRBs, it does not change federal law and, therefore, does not eliminate the legal risk to financial institutions.10 By its very nature, the 2014 Guidance was a temporary fix, subject to changing views of different administrations, evidenced by the fact that all three of the DOJ guidance documents noted above were rescinded by then Attorney General Jeff Sessions on January 4, 2018.12 The DOJ enforcement posture could change once again in a Biden administration. Biden is on record as favoring decriminalization, and Attorney General candidate Merrick Garland has stated that if confirmed he will deprioritize enforcement of low-level cannabis crimes. Garland also believes using limited government resources to pursue prosecution of cannabis crimes states where cannabis is legal does not make sense.12

Because of the uncertainty and high risk, most banks remain unwilling to serve CRBs. Those that do serve CRBs charge exorbitant fees (fees of $750-$1,000 or more per account per month are not uncommon), pricing many smaller operators out of the financial services market.

Cash is King – Or Is It?

Cannabis operators have discovered the old adage “cash is king” is not necessarily true when it comes to the cannabis space. Bank-less CRBs are forced to utilize cash to pay business expenses, which can be particularly difficult. Utility companies, payroll companies, and taxing authorities are just some of the providers that are difficult, if not impossible, to pay in cash. For example, cannabis operators have been turned away from IRS offices when attempting to pay large federal tax obligations in cash. Likewise, cannabis operators have been unable to utilize payroll processing companies to administer payroll and benefits for their businesses because the processors won’t take cash. CRBs can’t use Amazon or other online retailers because online providers cannot accept cash.

Because dealing in cash is so difficult, CRB operators look for workarounds such as using personal credit/debit cards to purchase business equipment and supplies. This doesn’t eliminate the cash problem, however, because the credit card holder will likely have to accept cash as reimbursement. Such transactions could be considered an attempt to hide the source of the cash, which is, by definition, money laundering.

CRBs often have large sums of money onsite

Some bank-less CRBs try to skirt the system by obtaining bank accounts in the name of management companies or other entities one step removed from the actual business. While operators often choose this route in an effort to streamline business and operate out of the shadows, it again runs afoul of banking laws. Transferring cannabis related financial transactions to another entity is actually the very definition of money laundering – which, as noted above, is defined as the process used to conceal the existence or source of “illegal” funds.

In addition to the difficulties in making payments or purchasing business supplies, operating in a cash-heavy environment poses significant safety risks for cannabis operators. CRBs often have large sums of money onsite and transport large sums of cash when purchasing product or paying bills, making them a target for robbery. In 2017, there was a spate of dispensary robberies across the Phoenix Metro area, including one at Bloom Dispensary that took place during operating hours.13

Managing all that cash increases the cost of doing business as well, in the form of increased labor, insurance, and security costs. Cash must be counted and double counted, which can be time consuming for staff, not to mention the time it takes to deliver physical cash payments to hither and yon. Ironically, lack of banking significantly decreases transparency and clouds the waters of compliance, as operating strictly in cash makes it easier to manipulate reported financial results.

Potential Congressional Solutions

In recent years Congress has undertaken several efforts to pass legislation designed to address the state/federal divide on cannabis, which would likely clear the way for financial institutions to provide services to CRBs, including:

R. 1595 – Secure and Fair Enforcement Banking Act of 2019 (“SAFE Act”);

1028 & H.R. 2093 – Strengthening the Tenth Amendment Through Entrusting States Act (STATES Act); and

2227 – Marijuana Opportunity Reinvestment and Expungement Act of 2019 (MORE Act).

The climate in Washington DC, however, did not allow any of these initiatives to pass both houses of congress. Had any been sent to the White House, President Trump was unlikely to sign them into law.

The cannabis industry has new reason to believe reform is on the horizon with shift in political leadership in the White House and Senate. Newly anointed Senate Majority Leader Chuck Schumer recently committed to making federal cannabis reform a priority, and President Biden appears committed to decriminalization, reviving the hope of passage of one of these pieces of legislation.

The Changing Banking Landscape

Even though there is little in the way of formal protections for financial institutions, and with the timeline for a legislative fix unknown, an increasing number of banks are working with cannabis operators.

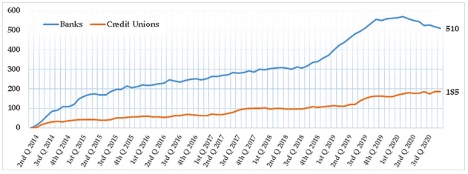

According to FinCen statistics, there were approximately 695 financial institutions actively involved with CRBs as of June 30, 2020. It is important to note that these statistics are based on SAR filings, which banks are required to file when an account or transaction is suspected of being affiliated with a cannabis business. However, some of these SARs may have been generated on genuine suspicious activity rather than on a transaction with a known cannabis customer.

Number of Depository Institutions Actively Banking Cannabis-Related Businesses in the United States (Reported in SARS)14

There are arguably more banking institutions offering services to CRBs than ever before. The challenges for CRBs are (1) finding an institution that is willing to offer services; (2) building/maintaining a compliance regime that will be acceptable to that institution; and (3) cost, given the high fees associated with these types of accounts.

How CRBs Get Accepted by Banks

The gap between CRBs’ need for banking and the financial services providers’ sparse and expensive offerings to the sector has created an opportunity for third-party firms to intervene and provide a compliance structure that will satisfy the needs of the financial institutions, making it easier for the CRB to find a bank.

These third-party firms perform extensive BSA-compliant due diligence on applicants to ensure potential customers are following FinCen guidance required to receive banking services. After the completion of due diligence, they connect the CRBs with financial institutions that are willing to do business with CRBs and provide checking/savings accounts, check writing capability, and merchant processor accounts. These firms often provide additional services such as armored car and cash vaulting services. Some of these firms also offer vendor screening, pre-approving vendors before any payments can be made.

One such firm, Safe Harbor Private Banking, started as a project implemented by the CEO of Partners Credit Union in Denver, Colorado, who set out to design a cannabis banking program that would allow Partners to do business with Colorado CRBs.15 The program was successful and has since expanded into other states who have legalized cannabis. Other operators include Dama Financial and NaturePay.

While these services offer hope for many CRBs, the downside is cost. These services perform the operations necessary to find, open, and maintain a compliant bank account; however, the costs of compliance are still high, pricing some small operators out of the market.

Is Digital Currency an Answer?

Digital currency is also making its way into the cannabis world. Digital currency, or cryptocurrency, is a medium of exchange that utilizes a decentralized ledger to record transactions, otherwise known as a blockchain. One of the largest benefits of blockchain is that it is a secure, incorruptible digital ledger used for, among other things, financial transactions.16 Blockchain technology offers CRBs a transparent and immutable audit trail for business and financial transactions. Several cannabis-specific cryptocurrencies have sprung up in the past several years, including PotCoin, CannabisCoin, and DopeCoin, to name a few.

In July 2019, Arizona approved cryptocurrency startup ALTA to offer services to the state’s medical cannabis operators.17 ALTA describes itself as a “digital payment club where cash-intensive businesses pay each other using digital tokens instead of cash.”18 ALTA members purchase digital tokens that are used to pay other members using a proprietary blockchain based system. The tokens are redeemable for US dollars at a stable rate of 1:1, and CRBs do not need a bank account to participate in the ALTA program.

ALTA proposes to pick up members’ cash and exchanges it for tokens, which are then used to pay other members for goods and services. Tokens may be redeemed for cash at any time.18 The company has been approved by the Arizona State Attorney General, and one of the first members they hope to enlist is the Arizona Department of Revenue (ADOR). Enlisting ADOR into the program would allow dispensary members to pay state taxes digitally rather than hauling large amounts of cash to ADOR offices.

Similarly, Nevada recently contracted with Multichain Ventures to supply a digital currency solution to the Nevada cannabis industry. Nevada Assembly Bill 466 requires the state create a pilot program to design a “closed loop” system like Venmo in an effort to reduce cash transactions in the cannabis sector. Like ALTA, Nevada’s proposed system will convert cash to tokens which can then be transacted between system participants.19

While both proposals are promising for Arizona and Nevada CRBs, the timeline as to when, or if, these offerings will come online is unknown. Action on cannabis reform at the federal level may render these options moot.

Looking to the Future

Although states are legalizing cannabis in one form or another in growing numbers, the fact that cannabis is still federally illegal poses a significant barrier to accessing the financial services market for CRBs. While most banks are still reluctant to offer services to this rapidly growing industry, there are more banks than ever before willing to participate in the cannabis industry. Recent changes in leadership in Washington DC offer a positive outlook for cannabis reform at the federal level.

As the “green rush” continues to envelop the country, financial services options available to CRBs are slowly growing. Many new options are now available to help CRBs find a bank, develop compliance programs, and manage the cash related problems encountered by most CRBs. However, these solutions may be out of reach for the budget-conscious small operator. Also, there are a number of cryptocurrency solutions designed specifically for CRBs; however, when, or if, these solutions will gain significant traction is still unknown.

References

Controlled Substances Act, 21 U.S.C., Subchapter I, Part B, §812.

“State Marijuana Laws”; National Conference of State Legislatures, February 19, 2021.

“Exclusive: US Retail Marijuana Sales On Pace to Rise 40% in 2020, near $37B by 2024”. Marijuana Business Daily, June 30, 2020.

Kaufman, Irving. “The Cash Connection: Organized Crime, Financial Institutions, and Money Laundering”. Interim Report to the President, October 1984.

S. Code § 1956 – Laundering of Monetary Instruments.

Rowe, Robert. “Compliance and the Cannabis Conundrum.” ABA Banking Journal, September 11, 2016.

“History of Marijuana as a Medicine – 2900 BC to Present”. ProCon.org, December 4, 2020.

Truble, Sarah and Kasai, Nathan. “The Past – and Future – of Federal Marijuana Enforcement”. org, May 12, 2017.

Sessions, Jefferson B. “Memorandum for All United States Attorneys”. January 4, 2018.

“Attorney General Nominee Garland Signals Friendlier Marijuana Stance”. Marijuana Business Daily, February 22, 2021.

Stern, Ray. “Robbers Hitting Phoenix Medical Marijuana Dispensaries: Is Bank Reform Needed?” The Phoenix New Times, April 11, 2017.

FinCen Marijuana Banking Update, June 30, 2020.

Mandelbaum, Robb. “Where Pot Entrepreneurs Go When the Banks Just Say No.” The New York Times, January 4, 2018.

Rosic, Ameer. “What is Blockchain Technology? A Step-by-Step Guide for Beginners.” com, 2016.

Emem, Mark. “Marijuana Stablecoin Asked to Play in Arizona Fintech Sandbox.” CCN.com, October 25, 2019.

http:\\Whatisalta.com\

Wagner, Michael, CFA. “Multichain Ventures Secures Public Sector Contract with Nevada to Supply Tokenized Financial Ecosystem for the Legal Cannabis Industry”, January 26, 2021.

The cannabis industry in the United States represents about a $50 billion asset class making it one of the largest new asset classes in the country. Commercial real estate lending is a key enabler for companies seeking to expand and scale. Pelorus Equity Group is one of the largest commercial lenders in cannabis with over $170 million deployed since its first cannabis transaction in 2016.

Since 1991, Pelorus principals have participated in more than $1 billion of real estate investment transactions using both debt and equity solutions. Pelorus offers a range of transactional solutions addressing the diverse needs of cannabis related business operators. While most cannabis private equity lenders focus on real estate acquisition and refinancing, Pelorus has leveraged its experience in more than 5,000 transactions of varying size and complexity to offer value-add loans, a rarity in the industry.

We spoke with Rob Sechrist, president of Pelorus Equity Group and manager of the Pelorus Fund. Rob joined Pelorus in 2010 after several years in the California real estate market. In 2018, Pelorus launched the Pelorus Fund where Rob is currently the manager. The Fund converted to an REIT in 2020.

Aaron Green: How did you get involved in the cannabis industry?

Rob Sechrist: Pelorus is a value-add bridge lender. We’ve been lending for a long time, originally in the non-cannabis space. We’ve done 5000 transactions for over a billion dollars – more than a lot of banks.

In 2014, our local congressman Dana Rohrabacher passed the Rohrabacher-Blumenauer Amendment that defunded the Department of Justice from prosecuting any cannabis related business in a medically licensed state. We were a supporter of that legislation and once that passed, we took a serious look at utilizing our expertise in being a value-add lender and applying it to the largest asset class of real estate that is newly coming about today. That cannabis related asset class is about $50 billion.

Rob Sechrist, president of Pelorus Equity Group and manager of the Pelorus Fund

We decided that we had the expertise to move into this space and to build these facilities out for our borrowers so that the cannabis use tenants would have a fully stabilized facility and make it operate. After the amendment passed in 2014, by 2016 we had originated our first transaction. Since that time, we’ve originated 51 transactions in the cannabis space for over $177 million so far. It wasn’t that big of a pivot when you’re just providing the value-add loan.

“Value-add” in the loan business means that a portion of the loan amount, let’s just say is a million dollars, maybe 250,000 of that, is a pre-approved budget to go back into the property. In cannabis property those are typically tenant improvements and/or equipment to fully stabilize that tenant. So, we’re the first fully dedicated lender in the nation exclusively to cannabis and we’ve done more transactions than anybody else in the nation.

Green: What are some challenges of cannabis lending compared to traditional lending?

Sechrist: The number one challenge in cannabis is that you must disclose to your investors that you’re originating the loans to cannabis use tenants. Many people have concerns that lending indirectly might be federally illegal. If you did not disclose that to your investors when you form that capital stack to fund these transactions, you’re going to run into issues. So, you would need to create a vehicle where you disclose to your investors that you’re intending to lend into cannabis and it’s still federally illegal. Doing one-off stand-alone transactions deal by deal is not sustainable if you’re going to be a large lender.

There are other challenges. Because cannabis is still federally illegal, it gives insurers and other third parties the ability to deny a claim, or certain lender protections. Some examples include errors and omissions insurance, title insurance, property insurance, etc. and all of them say in those policies that if you’re doing something federally illegal, then the policy is null and void. So, you must think your way through very carefully all the things that could potentially be an issue. You also have to disclose to those third parties and find a way to get them to acknowledge it to make sure you have the coverage if you ever have to make a claim. That’s a very difficult process.

Green: How has the investor profile in cannabis lending changed over time?

Sechrist: Our fund was structured to allow for institutional capital from the inception. We were able to do that because we are completely non-plant touching. Our fund only lends to the owners of commercial real estate. We do not lend to any cannabis licensed operator directly whatsoever. Our borrowers – the owners of the properties – would then have a lease agreement with the cannabis use tenant. Even if it’s an owner-operator, those are separate entities. That’s how we’ve distinguished ourselves.

Pelorus Equity Group, Inc. Logo

Regarding the investor profile, the first $100 million plus we raised was primarily from retail investors who were individuals writing checks up to a million dollars. Once we had three years of audited track record and our fund was $100 million, we then pivoted over to family offices and institutional investors and pension funds. We’re now working primarily with those types of investors.

The reason that we started with retail investors is that it’s very easy for me to explain our model to a single decision maker and answer their questions. Once I move into family offices or institutional investors, the opportunity goes to a credit committee where I’m relying on some other party to educate the investor about our investment. It’s enormously challenging at that point if it’s not me doing the talking. I know the answers, but I’m having to rely on somebody else to answer questions. We’ve tried to educate everybody we speak with and craft our documentation in such a way that even when it’s not myself answering the questions directly, people can understand how we thread the needle through some of the legal hurdles.

Green: How do you prioritize deal flow, and what are the qualities of a successful loan applicant?

Sechrist: We typically maintain a pipeline of around $150 million in transactions at any one time.

Applicants must have real estate. We’re not doing business loans or operator loans directly to tenants or business operations. So, that’s the starting point. We want a real estate piece of collateral where we feel more than comfortable with the loan-to-value and ratios and the loan to cost and other figures, that we feel that this transaction is going to be a success for our borrower and ultimately the tenant.

Next, we will only work with very experienced operators who have a proven track record where this is not their first transaction. Ideally, we are working someone who is looking to expand their operations and who is ready to either move from being a tenant of their previous facility and buying their next facility.

The next aspect that we’re looking for is the strength of the borrower’s guarantor. They must be able to qualify to support that transaction. Many of our transactions are millions or 10s of millions of dollars. You must have a sponsor that can support that size of a transaction.

Green: What sort of value-adds should a cannabis property owner look for in their lender?

Sechrist: Most people that are looking for loans are only familiar with getting loans for themselves on their owner-occupied house. Most loans have points, they have a rate and a term, loan-to-value and things like that.

“We wanted to make sure that when we underwrite the transaction, that every single piece of capital is necessary to get that facility all the way to where that tenant can start generating their first crops and make their lease payments.”When you move into construction loans or value-add lending, there are other elements that are more important than the pricing of the loan. The number one thing is to get that property fully stabilized and built as quickly as possible. Cannabis tenants are generating 10 to 15 times more revenue per month than non-cannabis tenants.

If you go to a bank and borrow money it may be a third of what it costs to borrow from us, but they process draws maybe once a month. So, if you’re having to advance the money for improvements of the property, and then the bank reimburses once a month, at a certain point you’re not going to be able to advance any more money until you get reimbursed. The project comes to a stop. So, in your mind, you might have saved an enormous amount on the pricing of the rate, but it’s costing you dearly in revenue and opportunity costs. We typically process 50 to 100 draws post-closing on transactions, and we get that facility built and the money reimbursed to all the contractors on a multiple-times-a-week basis. It’s happening in real flow all the time.

A typical problem for a tenant is that the tenant improvements are orders of magnitude higher than a non-cannabis tenant – anywhere from $150 to $250 per square foot. In addition, the equipment is often enormously expensive as well. It’s tough to put money into a buildout for a building that you may not own. Our vision at Pelorus was, let’s not force these tenants – the cannabis operators – to raise equity at the worst possible time when they’re not generating revenue through the facility. Let’s shift that capital balance for those tenant improvements and equipment from the from the tenant to the owner of the building, which is where it’s secured and adds value to that building anyway. Our vision was to shift that money from the balance sheet of the tenant over to the owner of the real estate so the tenant didn’t have to sell equity to come up with that money. Then the tenant is paying for the improvements in the lease rate and the borrower is paying for improvements in the note rate. And so we’ve shifted tenant improvements from being an equity component to now it’s just priced in the debt. This way you know what the terms are and you know what your total exposure is there.

We wanted to make sure that when we underwrite the transaction, that every single piece of capital is necessary to get that facility all the way to where that tenant can start generating their first crops and make their lease payments. Most of our peers in the space don’t look at it that way. They just do the acquisition or the refinance. They don’t do anything for the tenant improvements. They don’t do anything for the equipment. The tenant is left out there to either raise that equity or the borrower – the owner of the real estate – is having to come up with that additional capital on their own. We think you’re set up for failure in that circumstance. So, we blend all that into one capital stack. It’s important that the tenants can get all the way up to being able to cash flow and support that facility and be fully stabilized so they can refinance into a lower cost bank or credit union transaction.

Green: What federal policies and trends are you monitoring?

Sechrist: First, I think that it’s important to remind people that the Rohrabacher-Blumenauer Amendment has protected everybody from any prosecution. So, there’s no jeopardy out there that exists. The second thing I like to tell people is there are 695 banks on FinCEN’s website of cannabis Tier 1 depositors, and of those, we’re tracking numerous FDIC insured state banks and credit unions that are lending directly. We’ve been paid off by banks.

So, there’s this massive misconception that there’s no banking at all and that everything is happening by cash. The only cash buildup that happens is at the retail dispensary level because credit cards aren’t allowed for retail sales at the dispensaries. Out of the 2,000 transactions that we’ve either processed or reviewed, not one has ever not had banking set up. So, it is a big misnomer that there’s no depositor relations for Tier 1 banking, which is plant touching.

Tier 2/3 depositors are ancillary, which is what we are at Pelorus. There are 100 private lenders and dozens and dozens of state and federal credit unions or state banks and credit unions, not federal, that are FDIC insured and lending. Those banks are difficult to get loans from because they only want to do urban environments. They want to do fully stabilized companies and they want to use alternative views and the facility has to have seasoning for cash flow. It’s difficult to qualify for them. So, banking and lending exists out there, and most people are not aware of that.

Green: What are you most interested in learning about? This could be either in cannabis or in your personal life.

Sechrist: My two passions are snowboarding and racetrack driving. I just came back from the Mille Miglia race in Italy, and I do a lot of driving on the racetracks. I’m always looking to learn from those experiences.

In the cannabis sector, social equity programs are happening across the nation and cannabis licenses are being issued to operators. We would like to help participate in some system of educating these applicants that win the awards. Lending to an owner of a property who just won a license but has no experience is going to be problematic. Somebody needs to be thinking that out and making sure that these people that win have enough experience and education to set them up for success. Cannabis is one of the most complicated businesses ever, and they’ve got this license as their ticket, but they need to know how to make sure they’re going to be successful.

Things are about to change for cannabis and cannabis-related businesses, as landmark legislation to reform federal cannabis banking and insurance laws is just around the corner with the SAFE and CLAIM Acts now making their way through Congress.

The Secure and Fair Enforcement (SAFE) Banking Act, which already passed in the House, would allow financial institutions to do business with cannabis companies without facing federal penalties. There are high expectations the proposal will make its way through the Senate and onto President Biden’s desk.

The Clarifying Law Around Insurance of Marijuana (CLAIM) Act was introduced in Congress in March and is in the first stage of the legislative process. If it passed, it would allow insurance companies to service cannabis businesses without the threat of federal penalties.

For years, fear of sanctions kept banks and credit unions from working with the cannabis industry, forcing cannabis businesses to operate on a cash basis which made them targets of crime and created complications for financial regulators. This is a significant first step for cannabis businesses toward conducting more legitimate and safe operations.

The SAFE Banking Act: Providing a Legitimate Avenue to Banking and Loans

With 37 states and D.C. having taken action to legalize cannabis in some way, it is clear the federal cannabis regulatory model has shifted and the path forward for the SAFE Banking Act shows promise.

The bill creates a safe harbor for banks and credit unions to the extent they would not be liable or subject to federal forfeiture action for providing financial services to a cannabis-related business.More competition means greater capacity and lower premiums for all.

The bill would prohibit a federal banking regulator from:

Recommending, incentivizing or encouraging a depository institution not to offer financial services to an account holder affiliated with a cannabis-related business or prohibit or otherwise discouraging a depository institution from offering services to such a business

Terminating or limiting the deposit insurance or share insurance of a depository institution solely because the institution provides services to a cannabis-related business

Taking any adverse or corrective supervisory action on a loan made to a person solely because the person either owns such a business or owns real estate or equipment leased to such a business.

The CLAIM Act: Backing Cannabis Businesses with the Right Insurance Coverage

Should the CLAIM Act pass, it will protect insurance companies that provide coverage to a state-sanctioned and regulated cannabis business. It would also prohibit the federal government from terminating an insurance policy issued to a cannabis business and protect employees of an insurer from liability due to backing a cannabis-related business.

The CLAIM Act will be a boost for the insurance market and drive more underwriters to write cannabis policies. More competition means greater capacity and lower premiums for all. The act would also have a notable impact on currently hard-to-source policies like Cyber coverage, Directors & Officers (D&O) insurance, Errors & Omissions (E&O) and other management liability policies that have been extremely limited to cannabis businesses.

Cannabis Sales Still Growing Strong Globally

The cannabis market is not slowing down in the United States or globally. Recent forecasts have U.S. sales reaching $28 billion in 2022.

As was the case in Canada where cannabis was made federally legal in 2018, there’s going to be a steep learning curve industry-wide for financial services and insurance vendors who don’t yet understand the risks and liabilities of cannabis operations, even if the SAFE and CLAIM Acts pass this year. And yet this is one giant step in the right direction toward the safe and equitable sales of cannabis country-wide.

All major industries took a hit during the COVID-19 pandemic, but in many states, cannabis dispensaries were labeled as essential, which has allowed the industry to continue with some alterations. The impact now will come from what innovations and improvements the industry can leverage going forward.

From changes to protocols and buyer behaviors to supply chain disruptions, there were many new hurdles for the industry in addition to the ones cannabis businesses already faced, such as funding. But the silver lining could be that businesses within the cannabis industry become less of a specialty and more ‘every day’ than ever before.

The effects of the pandemic on the cannabis industry

Overall, the industry has fared well, in part thanks to its distinction as an essential service in states where cannabis is legal. It’s possible states made this decision for the same reason that alcohol businesses were deemed essential in most places: hospitals are not equipped during pandemic times to take care of people who are being forced to detox or those suffering from anxiety because they don’t have access to their legal drug of choice.

In a multitude of ways, cannabis businesses have adapted to bring calm in a storm while at the same time making manufacturing adjustments to meet the CDC guidelines. For example, there is more attention placed on individually pre-packaged products for single use; something that is less sharable as an experience but eminently practical.

Another area that has shifted a little is in the limiting of the exchange and interaction between business owners and staff relative to the customers. It’s all in the aim of mitigating the risk of exposure, but it has changed the dynamic in many cannabis businesses. This is the new normal for the time being and the industry has adapted well.

Ultimately, retail cannabis businesses today are no different than the retail of candy, cigarettes or alcohol. Certainly, segments of the industry have still struggled. Lack of tourism and the curbside/take out circumstances at dispensaries took their toll. But without the opportunity to still conduct business in some capacity, 50-60% of all operators would have gone out of business. Plus, as many people use cannabis to offset medical symptoms, including pain management, there is a legitimate need for cannabis to be available. The pandemic has provided the opportunity for many who might not have tried it before to give it a chance to help them medicinally.

Behaviors have changed, including those of buyers

Driven by consumer interests, many dispensaries have adapted to provide curbside pickup options, delivery of online orders and more. That has meant that the customer also needs to be more knowledgeable about cannabis: the experienced consumer knows what they like and want and can make their choices at a distance. Someone who is new to cannabis use might find navigating the choices and options a little more difficult, without the help of experienced staff. The breadth of material online and the ability of some dispensaries to share content that helps the consumer to make choices, in the absence of walking around the dispensary, have been additional tools at the disposal of businesses.

That said, the cannabis industry today is not a vastly different one: it is adapting to the new rules and new reality. Whether this way of doing business—at a distance—is a temporary or permanent solution will be dependent upon what federal and state regulators dictate in the months ahead, but there is likely to be ongoing demand for being able to order online and keep social distance protocols in place.

An interesting example is the Ontario Cannabis Store (OCS) in Ontario, Canada. This is a government run shop that has retail as well as a robust online presence, with free delivery during the pandemic. This has facilitated an increase in new customers, which had already jumped, post legalization. People who might have felt uncomfortable going into a dispensary can still learn about cannabis online and order it, from the relative comfort and safety of their sofa.

Supply chain disruptions and the cannabis industry

The industry has long been focused on overseas suppliers. With the arrival of the pandemic and restrictions on obtaining products from other countries, supply chains have been disrupted for many cannabis businesses. That has forced many to shift their supply chains to more local manufacturers, in North and South America.

In the long run, this should have a positive impact for the industry, so that despite the short-term disruption to the supply chain, which is having an impact on the industry as a whole, there could be an upside for local producers, growers and manufacturers. It will take time to know how this will all play out.

Funding and other issues for the cannabis industry

For a new cannabis startup in these times, the key will be what it has always been for any business, just to a greater degree: due diligence. Companies that want to open a cannabis business, whether during the pandemic or not, need to evaluate the opportunity as one would any investment. It’s all about the numbers: data for the industry as a whole and specifically from competition. These days, that data is widely available and more and more consultants and investors have expertise in this industry. “Overall, there is more interest in the industry than ever before”

It’s vital to be extremely well versed, particularly for businesses that are relatively new in the industry, because the single biggest issue for many has and will continue to be funding and investment. The cannabis industry is no different than any other business, except for the fact that it is a specialty business. With that comes the need to look for funding among investors who have some knowledge or appreciation for the industry.

Some of the key concerns traditional investors will have include:

Regulatory differences from state to state: since cannabis is still illegal at the federal level, there can be an array of hurdles at state and local level that make cannabis businesses trickier to work with.

There are religious based/morality issues for some lenders in dealing with the industry. These aren’t dissimilar from issues with other industries such as adult entertainment and gaming. It’s also fair to point out that, morality aside, these industries have thrived in the last several decades.

So, while traditional banking institutions will often deal with the proceeds from the cannabis industry, including allowing bank accounts for these businesses, there is far less of a chance that they would invest in a cannabis business, for fear of risking their license. They can even go so far as to refuse to include income from a cannabis business in the determination of a loan application.

There are more unique lending or investing groups that either specialize in cannabis or are starting to open their books to specialize in cannabis. Overall, there is more interest in the industry than ever before, as it becomes normalized in American society: more participants and more insiders of the industries that are willing to invest in the right idea.

Will legalization be more likely in the future?

The fact that cannabis businesses and dispensaries have been deemed essential services during the pandemic, where they legally operate, has shed new light on the relevance of these businesses and the advantages of more widespread legalization.“Consumers will help drive the innovations as they demand clean consumption methods”

In fact, the pandemic has normalized a lot of new behaviors, including the acceptable use of cannabis to help with stress and anxiety. People are, perhaps thanks to staying at home more, doing the legwork to understand how cannabis could be useful to them in managing their stress. The medicinal benefits of cannabis have long been researched and understood: consumers are coming into the fray to express their interest in it, which can only fuel the possibility of more widespread legalization.

Add to this the fact that the cannabis industry is a growth industry. There are companies and jobs that aren’t coming back, post-pandemic. There is an opportunity to grow the cannabis industry to the general benefit of many, both as business owners and employees. The revenue generated from taxation following legalization would also benefit many state coffers. Federal level legalization would be the panacea to eliminate the mixed message, state by state regulation that currently exists.

Opportunities for innovation, moving forward

As more and more people become interested in the industry, and as cannabis use is normalized within society through legalization, the opportunities for the industry can only expand.

For an industry that started on the simple concept of smoking cannabis, the advances have already been legion: edibles, nanotechnology-based formulations for effective, clean consumption and many more innovations.

In a world that increasingly sees smoking as a negative, for the obvious impact to lung health, there are so many opportunities to grow the industry to find consumption methods that are safe and still deliver the impact of the inhaled version.

Here again, consumers will help drive the innovations as they demand clean consumption methods. The technology is available to make this possible; it only takes innovation and education to find the best ways to move this industry forward.

As legalization expands—and particularly if it is dealt with at the federal level—the industry will be able to capitalize on existing infrastructure for manufacturing and distribution, allowing new businesses to grow, get funded and thrive in the new normal.

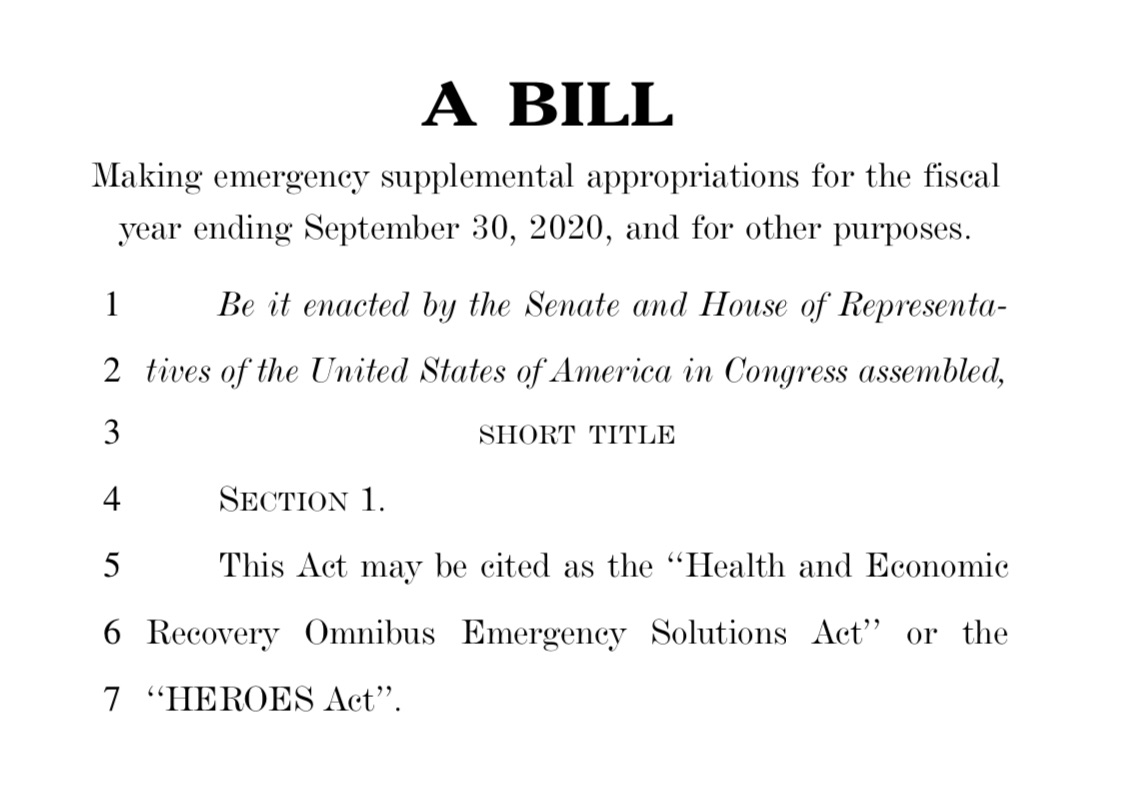

UPDATE: Late in the evening on May 15, the House of Representatives passed the HEROES package, voting 208-199 (with 23 abstentions). The bill now now heads to the Senate where its fate is more uncertain.

Earlier today, Speaker Nancy Pelosi debuted the latest piece of legislation to help Americans impacted by the coronavirus pandemic. The Health and Economic Recovery Omnibus Emergency Solutions Act (HEROES Act) is a large bill containing emergency supplemental appropriations more than 1,800 pages long.

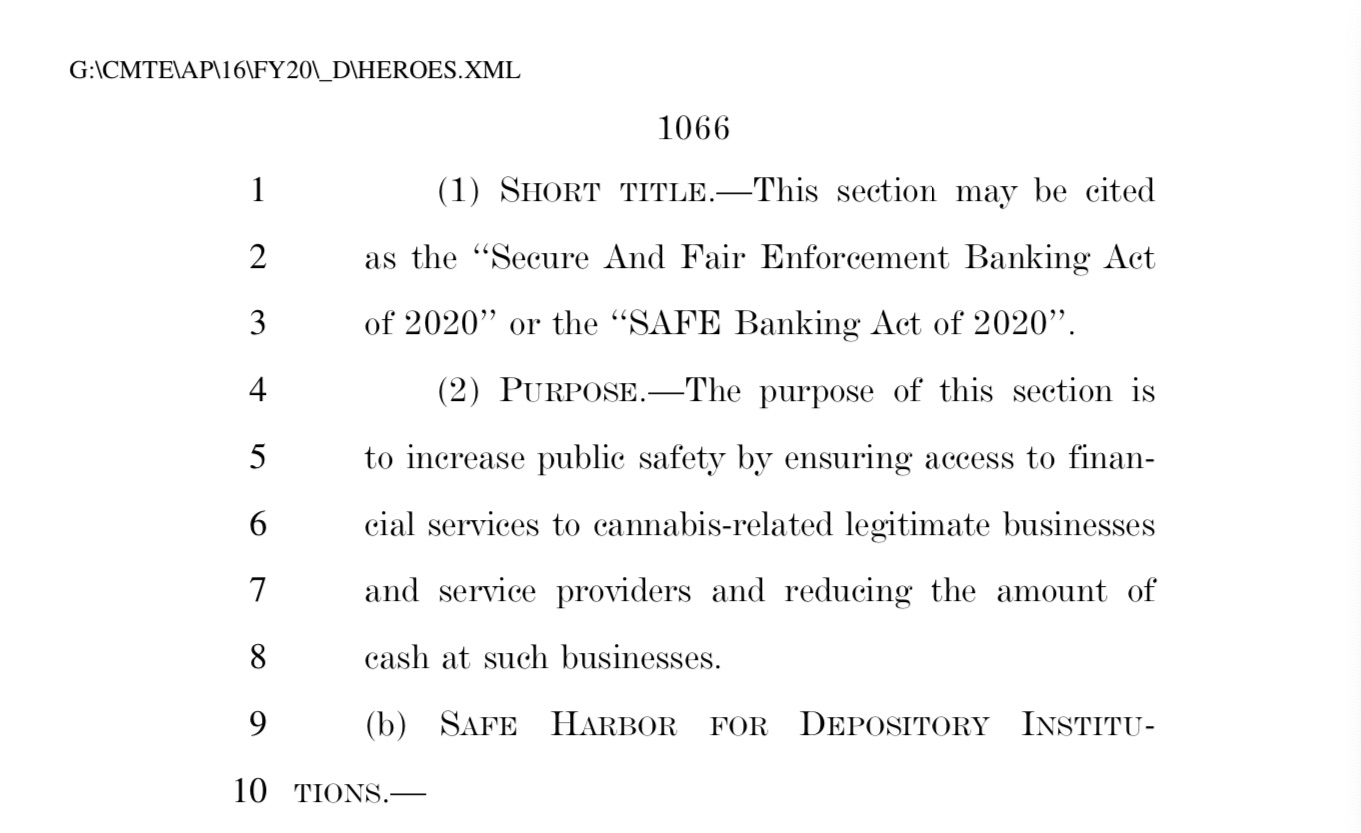

On page 1,066, those in the cannabis industry will find a very exciting addition: the Secure and Fair Enforcement (SAFE) Banking Act. For the uninitiated, the SAFE Banking Act would ensure access to financial services for cannabis-related businesses and service providers.

Currently, federally regulated financial institutions face penalties for dealing with cannabis companies due to the Controlled Substances Act. The bill, if passed, would eliminate the possibility of any repercussions for doing business with cannabis companies.

The impact of this bill becoming law would be widespread and immediate for both the cannabis market and banks looking to invest in the cannabis industry. With banks given the green light to conduct business with the cannabis industry, there is no doubt that many financial institutions will rush to the opportunity. Cannabis businesses will benefit greatly, no longer having to deal with massive quantities of cash and gain access to things like loans, bank accounts and credit lines. Furthermore, cannabis companies will benefit from the rush of banks getting in the game, leading to a competitive and affordable banking market.

It is no secret that cannabis businesses have had a cash problem for decades now. Given the coronavirus pandemic, CDC guidelines dictate minimizing the handling of cash and encourage payment options like credit cards. Cannabis businesses dealing with large quantities of cash puts them, their employees, their customers and even regulators at risk.

Aaron Smith, executive director of NCIA

According to Aaron Smith, executive director of the National Cannabis Industry Association (NCIA), the cash problem is a serious, unnecessary health risk. “On behalf of the legal cannabis industry, we commend the congressional leadership for prioritizing public health and safety by including sensible cannabis banking policy in this legislation,” says Smith. “Our industry employs hundreds of thousands of Americans and has been deemed ‘essential’ in most states. It’s critically important that essential cannabis workers are not exposed to unnecessary health risks due to outdated federal banking regulations.”

In fact, it was the NCIA and a handful of other industry organizations that lobbied Congress last week to include language from the SAFE Banking Act in the HEROES Act, citing the known fact that cash can harbor coronavirus and other pathogens, along with the “personal proximity required by cash transactions as reasons for urgency in addition to the other safety and transparency concerns addressed by the legislation.”

The SAFE Banking Act was already approved by the House of Representatives. In September of 2019, the bill made a lot of progress through Congress, but stalled once it made it to the Senate Banking Committee.

The HEROES Act will be debated by the House of Representatives prior to a floor vote. If it passes the House, it moves to the Senate, which is about as far as it made it the last go around. However, because the banking reform is included in coronavirus relief legislation, there is a newborn sense of hope that the bill could be signed into law.

On Wednesday, March 25, the United States Senate approved an estimated $2-trillion stimulus package in response to the economic impact of the COVID-19 outbreak. The legislation, formally known as the “Coronavirus Aid, Relief, and Economic Security Act” (or the CARES Act), was approved by the Senate 96-0 following days of negotiations. One of the most highly anticipated provisions of the CARES Act, the “recovery rebates” for individuals, will provide a one-time cash payment up to $1,200 per qualifying individual ($2,400 in the case of eligible individuals filing a joint return) plus an additional $500 for qualifying children (§6428.2020(a)). The CARES Act, which remains subject to House approval, also prescribes an additional $500 billon in corporate aid, $100 billion to health-care providers, $150 billion to state and local governments and $349 billion in small business loans in an effort to provide continued employment and stabilize the economy. The legislation further provides billions of dollars in debt relief on existing loans.

CARES Act – Paycheck Protection Program

Under the CARES Act, small businesses who participate in the “Paycheck Protection Program” can receive loans to cover payroll expenses, group health care benefits, employee salaries, interest on mortgage obligations, rent, and utilities (§1102(F)(i)). To qualify for these small business loans, businesses must employ 500 employees or less, including all full-time and part-time employees (§1102(D)). Eligible recipients must also submit the following as part of their loan application: (i) documentation verifying the number of full-time equivalent employees on payroll and applicable pay rates; (ii) documentation verifying payments on covered mortgage obligations, payments on covered lease obligations, and covered utility payments; and (iii) a certification that the documentation presented is true and the amounts requested will be used to retain employees and make necessary payments (§1106(e)). The CARES Act delegates authority to depository institutions, insured credit unions, institutions of the Farm Credit System and other lenders to provide loans under this program (§1109(b)). The Treasury Department will be tasked with establishing all interest rates, loan maturity dates, and all other necessary terms and conditions. Prior to issuing these loans, lenders will consider whether the business (i) was in operation as of February 15, 2020, (ii) had employees for whom the business paid salaries and payroll, or (iii) aid independent contractors as reported on a Form 1099-MISC (§1102(F)(ii)(II)).

What Does This Mean for Cannabis Businesses?

Due to the continued Schedule I status of cannabis (excluding hemp) under the Controlled Substances Act (CSA), cannabis businesses are not eligible to participate in the Paycheck Protection Program intended to keep “small businesses” afloat during the current economic crisis. Because federal law still prohibits banks from supporting marijuana businesses, financial institutions remain hesitant to service the industry, as anti-money laundering concerns and Bank Secrecy Act requirements (31 U.S.C. 5311 et seq.) are ever-present. As a result, even if cannabis businesses technically qualify to receive federal assistance under the Paycheck Protection Program, they will face an uphill battle in actually obtaining such loans.

Cannabis Businesses Are Also Precluded from “Disaster” Assistance

Moreover, the conflict between state and federal law continues to prevent cannabis business from receiving assistance from the U.S. Small Business Administration (SBA) under the Coronavirus Preparedness and Response Supplemental Appropriations Act (H.R. 6201). In light of the COVID-19 outbreak, the SBA revised its “Disaster Loan” process to provide low-interest “Disaster Loans” to eligible small businesses. To qualify for these loans, a state must submit documented business losses for at least five businesses per county. The problem, however, is that the SBA still refuses to assist state-legal cannabis businesses in equal need of small business loans. Specifically, in a 2018 Policy Notice, the SBA reaffirmed that cannabis businesses – and even some non “plant-touching” firms who service the cannabis industry – cannot receive aid in the form of federally backed loans, as “financial transactions involving a marijuana-related business would generally involve funds derived from illegal activity.” The 2018 Policy Notice clarified that the following business are ineligible to receive SBA loans:

(a) “Direct Marijuana Business” — a business that grows, produces, processes, distributes, or sells marijuana or marijuana products, edibles, or derivatives, regardless of the amount of such activity. This applies to personal use and medical use even if the business is legal under local or state law where the applicant business is or will be located.

(b) “Indirect Marijuana Business” — a business that derived any of its gross revenue for the previous year (or, if a start-up, projects to derive any of its gross revenue for the next year) from sales to Direct Marijuana Businesses of products or services that could reasonably be determined to support the use, growth, enhancement or other development of marijuana. Examples include businesses that provide testing services, or sell grow lights or hydroponic equipment, to one or more Direct Marijuana Businesses. In addition, businesses that sell smoking devices, pipes, bongs, inhalants, or other products that may be used in connection with marijuana are ineligible if the products are primarily intended or designed for such use or if the business markets the products for such use.

More recently, the SBA provided further clarification that cannabis businesses are not entitled to receive a cut of the federal dollars being appropriated for disaster relief because of the CSA’s continued prohibition of the sale and distribution of cannabis. Last week, the SBA reiterated that:

“With the exception of businesses that produce or sell hemp and hemp-derived products [federally legalized under the 2018 Farm Bill], marijuana related businesses are not eligible for SBA-funded services.” (@SBAPacificNW)

Consequently, because of the continued Schedule I status of cannabis under federal law, cannabis businesses will not be entitled to receive Disaster Loans from the SBA, regardless of whether they qualify as a struggling small business.

Resolving the Issue

While the federal government has been considering legislation, such as SAFE Banking and the STATES Act, to create a more rational federal cannabis policy, neither of these bills are likely to pass any time soon given the current COVID-19 pandemic.

At the end of the day, until Congress passes some form of federal cannabis legalization, these small businesses will remain plagued by the inability to receive financial assistance, as evinced by the Paycheck Protection Program.

The hemp industry has experienced and continues to see a surge of growth and awareness nationwide. Following the passage of the 2018 Farm Bill, permanently legalizing the crop and removing hemp from its classification as a controlled substance, consumer demand for hemp and hemp products like CBD have skyrocketed.

Unfortunately, there remain many challenges. Confusion about hemp’s legal status – and the differences between hemp and its intoxicating cousin, marijuana – has too often stymied commerce in the industry, particularly with traditional banking products and merchant services being limited in their availability to those trying to grow their businesses.

This month, we witnessed a breakthrough development. Upon the bipartisan urging of Senate Majority Leader Mitch McConnell and Senator Ron Wyden, four federal banking regulatory agencies – Federal Deposit Insurance Corporation, Office of the Comptroller of the Currency, the Federal Reserve, Financial Crimes Enforcement Network – joined by the Conference of State Bank Supervisors – issued joint guidance confirming the legal status of hemp and the requirements for banks providing financial services to businesses.

Just some of the many CBD products on the market today.

The new guidance achieves many necessary benchmarks integrating hemp and banking, such as no longer requiring banks to file suspicious activity reports for customers solely because they are engaged in the growth or cultivation of hemp in accordance with applicable laws and regulations. Further, the guidance clarifies the difference between hemp businesses and marijuana businesses – adding yet another point of relief to banks concerned with national and state legality.

The hope is that the joint guidance should alleviate any fear of audits or regulatory crackdowns that have slowed financial institution integration with the hemp industry. However, this does not require banks or financial entities to participate in business with hemp companies. Nor does this guidance directly address the legality of hemp-derived CBD commerce.

With all of this in mind, there is still work to be done. Priority #1 is passage of the SAFE Banking Act. This bipartisan legislation, initially focused on providing a green light to marijuana banking in states where pot is legal, was amended to ensure a separate safe harbor for hemp, with far fewer hoops since it is not a controlled substance. It also directs federal financial agencies to provide clear guidance to both banks and other financial institutions – such as credit card companies – that hemp and CBD commerce are legal. The bill was passed overwhelmingly by the House in September and we are hopeful to see full Senate consideration soon.

Banking is one of the key targets that the hemp industry is aiming to secure, as this will allow for an increase in legal hemp business growth and practices. The goal of the U.S. Hemp Roundtable is to provide consumers with safe and legal hemp products along with the knowledge that the companies are meeting the highest standards and complying with national and state law.

While you may not have heard of CannTrust Holdings so far, that is now about to change. A summer spectacle of double dealing and corporate greed has put this Canadian cannabis company on the global map.

Unfortunately, the current meltdown underway is indicative of more to come.

A Summary Of The Story So Far

CannTrust, a company which serves 72,000 Canadian patients and got into the game early, decided to do what it saw other companies doing all around them. That covers a lot of ground (good and bad at this point). Regardless, the most relevant recent twist to the saga came when the company hired a new CEO, Peter Aceto last October.

Aceto however, along with the now also fired co-founder and chair of the board Eric Paul, decided to continue growing and harvesting unlicensed product. Worse, this occurred while boasting in public of their productivity gains on the way to securing a hefty investment of capital this spring. $170 million. The grow rooms finally got their certification in April.

What is even more embarrassing however, is that this was a round led by the much-vaunted investors the industry has been courting assiduously for the past several years. Specifically, in this case? Institutional banks like Bank of America, Merrill Lynch, Citigroup, Credit Suisse Securities and RBC Capital Markets.

But that is “just” the North American hemisphere. The rather unfortunately named CannTrust (certainly at this point) also had a European footprint – notably Denmark. Unlicensed cannabis ended up there too, of course. Stenocare A/S, the company at the receiving end of the same, reported receipt of product from the unlicensed rooms on July 4.

As far as such things go, however, you have to give it to CannTrust company executives. In terms of setting standards if not benchmarks and “records”, they certainly seemed to have set a few, although probably not the ones they aspired to. If not, with certainty, their investors.

A Surprise Or Inevitability?

That said, for many who have been sounding warnings for at least a year, the 2019 Summer of Canadian Cannascandal is certainly starting to confirm what many have been saying for quite some time. This is not the first time a securities exchange, for one, has sounded the alarm. Deutsche Börse delisted the entire North American public cannabis industry last summer briefly. Then they revised their policy, reluctantly, after Luxembourg changed its stance on medical use. That said, they are still watching with a standing policy of bouncing any company that runs afoul of their rules.

The problems, issues and more bubbling at the center of this cannameltdown, in other words, are not limited to just one company or country.

And everyone knows it.

Accounting For Past Mistakes

For those who are counting, the value of all of that illegally grown CannTrust product is not insignificant. Estimates are floating in the CA$50-70 million range. The problem is, of course, nobody is sure what numbers to rely on. CannTrust employees knowingly provided inaccurate information to the new CEO if not regulatory body until a whistle-blower provided a few more details.

That said, for all of the hullabaloo, one thing this story also does is point a bright spotlight on the lax enforcement of even this pretty easy-to-understand regulation.

The question, however is, if CannTrust thought it could get away with this kind of blatent flouting of the rules, if not lax oversight, are there any other companies who might have also done similiar things?

After all, even the pesticide scandal of 2016 did not occur at just one company either.

Where Are The Proceedings?

This is a rolling story, which began to break at the beginning of last month when Health Canada issued a non-compliance order to CannTrust and impounded 5,200 kg of dried cannabis that was apparently grown in unlicensed grow rooms on July 3.

There have already been some jaw dropping revelations so far (beyond the executive decision to even go down this road in the first place) no matter how attractive pimping numbers was. Starting with things like fake walls being erected to hide the grow. And then of course pictures that have been all over social media of late, of the now departed CEO Aceto being photographed directly in front of said unlicensed rooms too.

As a result, the drama has continued to unfold in a highly predictable way.

By August 1, CannTrust Holdings, a Canadian cannabis company listed on both the New York and Toronto stock exchanges, was facing a “quasi-criminal investigation” by the Canadian Joint Serious Offenses Team. This is a coalition of law enforcement agencies including the Ontario Securities Commission, the Royal Canadian Mounted Police Financial Crimes Unit, and the Ontario Provincial Police Anti-Rackets Branch.

But CannTrust’s issues don’t end there. This is an international story that is just beginning. Government regulators in Europe if not elsewhere are paying attention.So are shareholders, and their lawyers.

For all of today’s growing acceptance and legitimacy with cannabis, the reality is that today’s operators – whether growers/producers or dispensary operators – still face risks in running their businesses. If, in the old days, a customer got deathly ill from cannabis contaminated with something from somewhere during the distribution chain, oh, well. But now that there’s a legal system of checks and balances; there’s recourse when issues arise.

The problem is that the business is so new that most people don’t know what they don’t know about mitigating those risks. And that, unfortunately, extends to many in the insurance business who need to be doing a better job helping put the right protections in place.

One grower bemoaned to me at a cannabis trade show, “I sure wish I could insure my crops.” What? “You can,” I told him. His old-school ag broker didn’t know any better and didn’t do him any favors with his ignorance. But it brought home the point: We have to start treating cannabis like the real business it is.

Reviewing the existing insurance policies of today’s cannabis businesses uncovers some serious gaps in coverage that could be financially crippling if not downright dangerous should a claim be triggered. Retail dispensaries, for example, are high-cash businesses, making banking and trusted employees a must-have.Today’s cannabis businesses need to understand there will be risks but they are a lot more manageable than in the old days.

And a close eye must be cast to lease agreements for hidden exposures, too. We know a Washington state grower that had no property insurance on its large, leased indoor growing facility. The company’s lease made its owners, not their landlord, responsible for any required building improvements. It was one of a variety of serious exposures that had to be fixed.

Today’s cannabis businesses need to understand there will be risks but they are a lot more manageable than in the old days. Rather than find themselves under-insured, they can start by learning what they probably have wrong about insurance. Dispelling three of the most common myths is a good place to start.

Myth #1: Nobody will insure a cannabis business.

Not remotely true. You can and should get coverage. Think property and casualty, product liability, EPLI and directors and officers, employee benefits and workers comp. Additionally, you should be educated on what crop coverage does and doesn’t cover. Depending on your business’ role in production and distribution, you might also consider cargo, stock throughput, auto, as noted, crime and cyber coverage. It pays to protect yourself.

Myth #2: If my business isn’t doing edibles, I don’t have to worry about product liability insurance.

The reality is that product liability may be the biggest risk the cannabis industry faces, at every level on the supply chain. There’s a liability “trickle down” effect that starts with production and distribution and sales and goes down to labeling and even how the product is branded. Especially when a product is an edible, inhalable or ingestible with many people behind it, the contractual risk transfer of product liability is an important consideration. That means the liability is pushed to all those who play any role in the supply chain, whether as a producer or a retailer or an extractor. And all your vendors must show their certificates of insurance and adequate coverage amounts. Don’t make the mistake of being so excited about this new product that you don’t check out the vendors you partner with for this protection.

Myth #3: Any loss at my operation will be covered by my landlord’s policy.

As the example I cited early illustrated, that’s unlikely. Moreover, your loss might even cause your landlord’s insurance to be nullified for having rented to a cannabis business. It’s another reason to examine your lease agreement very carefully. You want to comply with your landlord’s requirements. But you also need to be aware of any potential liabilities that may or may not be covered. Incidentally, even if your landlord’s policy offers you some protection, your interests are going to be best served through a separate, stand-alone policy for overall coverage.

These are interesting times for the burgeoning legal cannabis business. Getting smart – fast – about the risks and how to manage them will be important as the industry grows into its potential.

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

We use tracking pixels that set your arrival time at our website, this is used as part of our anti-spam and security measures. Disabling this tracking pixel would disable some of our security measures, and is therefore considered necessary for the safe operation of the website. This tracking pixel is cleared from your system when you delete files in your history.

We also use cookies to store your preferences regarding the setting of 3rd Party Cookies.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.