The cannabis industry isn’t a level playing field. It’s disheartening to say. But as someone who has been building a soon-to-open dispensary for the last three years, I’ve experienced this lack of equity firsthand.

It starts with the industry’s foundation. We’re in an era where anyone can start a business. Create a logo, launch a website and upload promotional content on social media. A few clicks and…boom, you’re a business owner. Lovely, but absolutely not the case for the cannabis industry.

Getting started is no easy feat.

Budding cannabis entrepreneurs (pun very much intended) need a ton of capital in order to get started. And as cannabis isn’t federally legalized, entrepreneurs don’t have access to traditional banking loans. They either need to fund their cannabis venture with their life savings or turn to family, friends and their community to fundraise. Unfortunately, not everyone has such privilege or access. This reality contributes to the industry’s unequal playing field – and due to a lack of legalization, shows no signs of letting up.

Jessica Gonzalez

Jessica Gonzalez, a Jersey City-based attorney and cannabis advocate, spoke to this challenge in a recent NJBiz interview. “It’s extremely expensive to enter and survive in this industry, and given the limited capital options, you are forced to seek private investors – which opens a whole can of racial and gender bias. The need to stay capitalized, coupled with constantly changing regulatory environments, expensive service professionals, lack of real estate, a social stigma and IRS tax code 280E, creates high barriers to entry and high survival barriers.”

As Gonzales notes, funding is just one piece of the puzzle. Once you’ve secured said funding and have decided to start a cannabis venture, you’re navigating a minefield of ever-changing regulations. This demands the help of pricey service professionals–attorneys, operators, marketers and more–who remain abreast of current laws and have the subject matter expertise to properly guide you.

The issues with the cannabis industry are clear – funding is difficult to secure, marketing is nearly impossible and pricey consultants are table stakes. On the bright side, operating in cannabis isn’t all doom and gloom. Solutions are ahead–and they’ve been baked into the operating strategy of many fantastic, social-equity led dispensaries, includingSocíale, the soon-to-open Park Ridge, IL dispensary. While getting started is no easy feat, as leaders, we should each take it upon ourselves to empower those wanting to work with this life-changing plant by developing an industry that’s ripe with endless opportunities.

Economically empowering employees should remain top-of-mind.

The lack of equitable wealth creation in the cannabis industry bolsters its inaccessibility. It’s unfair that if a dispensary or cannabis business succeeds, only the entrepreneur wins financially. Yes, employees may get a small discretionary bonus at the end of the year – but they’re not woven into the fabric of the business’s profitability. Employees – and those earlier in the value chain, like growers – are left out in the cold, while dispensary owners seek to profit immensely.

Personally, when I started in the cannabis industry, I thought this dichotomy was blatantly unfair – and vowed to be a powerful force in changing that. At Socíale, profit sharing is a part of our DNA. Employees will take part in dispensary profits from the day they start. This way, everyone wins–and if employees decide to start a cannabis venture of their own, that ambition is more in reach. This is a massive piece of what the cannabis industry preaches when it has conversations surrounding social equity. It’s time the industry and its leaders back up this ideology with a plan of action. Embracing the concept of ownership not only among founders and senior leaders, but among employees at all levels, can provide a valuable taste of entrepreneurship. Situations like these often empower employees economically to create lasting changes for not just the company they’re working for, but for themselves and their families at home.

Social equity license holders should pay it forward.

Social equity dispensaries should embrace the pay-it-forward mentality among the communities of which they serve, especially those disproportionately impacted by the War on Drugs. It’s unfortunate to see dispensaries falsely advertise with a “social equity” label, merely for the vanity of it all.

Socíale is beholden to certain promises we made to the state of Illinois, who granted us our social equity license. This includes employing people from under-represented communities and advocating for cannabis social justice – two causes that we’re deeply committed to. As we look to shape the future, let’s remain hopeful about what it holds. Collaboration over competition needs to be the motto. If we all partner together to think beyond profits and aim to better the greater cannabis community, we’ll all be better off.

The problems facing the cannabis industry arising from its ongoing status as a federally illegal enterprise are numerous and well documented: 280E tax burdens, limited access to banking, exclusion from capital markets, uneven access to federal intellectual property right protections and the inability to access the stream of interstate commerce. The recent woes faced by cannabis companies operating in mature markets reveal another key legal hurdle for cannabis companies, their investors and their creditors: the inability to access federal bankruptcy protection. However, cannabis companies may have access to a number of contractual and state law remedies to deal with insolvency and other financial woes.

Background

Bankruptcy laws in the United States are unique in the world; nowhere else is access to bankruptcy so available or forgiving for ordinary citizens and companies alike, allowing debtors a fresh start by either liquidating their assets or reorganizing their debt. Commentators have observed that such favorable bankruptcy laws encourage entrepreneurship and have been at least partially responsible for American innovation. Indeed, the ability of Congress to enact bankruptcy laws is enshrined in the United States Constitution. Like almost all laws in the U.S. at the time, bankruptcy was originally the domain of the various states; it was not until the late 18th century that Congress saw the importance of a uniform set of protections for debtors and passed the first federal bankruptcy law in 1800; since then, bankruptcy has been exclusively the purview of federal law, with current bankruptcy law governed by the United States Bankruptcy Code.

Yuefan Wang, attorney at Husch Blackwell

This exclusivity, however, poses a problem for state-regulated cannabis businesses: because cannabis is federally illegal, in the eyes of the United States Trustee Program, a division of the United States Department of Justice responsible for overseeing the administration of bankruptcy proceedings, the reorganization of any cannabis business amounts to “supervis[ing] an ongoing criminal enterprise regardless of its status under state law.” Therefore, since there is no such thing as state law bankruptcy, even cannabis companies operating in full compliance with state laws do not have access to any bankruptcy protections.1

All financing transactions, whether debt or equity, occur in the shadow of bankruptcy. The basic distinction between debt and equity is predicated on the favorable treatment of holders of the former compared to holders of the latter (within debt, the favorable treatment of secured debt over unsecured debt), and this is true, especially in bankruptcy. Even beyond distribution priorities, the Bankruptcy Code’s provisions on automatic stays, avoiding powers, and discharge fundamentally shape the relationship between debtors and creditors: a bankruptcy judge has the power to impose the Bankruptcy Code on the relationship between a debtor and its creditors, no matter their previous contractual relationships. Just as the possibility of litigation is a Sword of Damocles hanging over any legal disputes, the prospect of a bankruptcy filing affects any negotiations between a debtor and its creditors ab initio. Therefore, when financial problems arise and a cannabis company must begin the difficult task of approaching its lenders for relief, it does so without an effective incentive for creditors to come to the table available to other companies in otherwise similar situations.

Alternatives to Bankruptcy

Just as disputants often prefer the contractual certainty of a settlement agreement to the capriciousness of a jury, debtors and creditors may choose extra-judicial solutions for insolvency. The downward trend in bankruptcies over the last few decades may partially be the product of such out-of-court arrangements, and debtors and creditors are increasingly comfortable with them as an alternative to voluntary or involuntary bankruptcy filing. While the effectiveness of these solutions is, in industries other than cannabis, ultimately evaluated with bankruptcy in mind, these solutions may also be preferable for a creditor of a cannabis company that is defaulting on its obligations.

Contractual Remedies: Lender Workouts, Exchange Offers and Composition Agreements

Given that the relationship between a debtor and its creditors is essentially contractual, the parties may choose to modify their relationship in any manner to which they can mutually agree. A lender workout is an agreement for a financially distressed company to adjust its debt obligations with a creditor (or often multiple creditors given that a lender’s payment obligations to one creditor necessarily affect its obligations to its other creditors). These contractual adjustments are tailored to the particular situation and can take the form of deferrals of payments of interest or principal, extensions of maturity dates, covenant relief (e.g., adjustment of the lender’s debt-to-asset ratio or other financial covenants which would otherwise trigger an event of default), and/or debt-for-equity swaps. This last option (including its related concepts, such as grants of options or warrants) is especially prevalent in the cannabis industry, given that cannabis companies often do not have traditional bank debt (though, at the same time, such solutions may be increasingly unattractive to creditors given lower valuations and the prevalence of equity as a form of consideration in cannabis mergers and acquisitions transactions).

Brent Salmons, attorney at Husch Blackwell

Similarly, an exchange offer restructures a faltering company’s capital stack. Typically, a company facing a default will offer its equity-holders new debt or equity securities in exchange for its outstanding debt securities, which new securities have more favorable terms, such as covenants, events of defaults and maturity. Exchange offers have the same goal as lender workouts in that they seek to eliminate a class of securities with an impending maturity date, event of default or breach of a covenant.

Composition agreements are contractual arrangements between a debtor and its creditors whereby the creditors agree to accept less favorable claims in order for the debtor to reorganize its operations so that the debtor’s future inflows can meet its reduced outflows, with the alternative being a complete collapse of the debtor (in which case no one, or perhaps only the most senior secure lenders, is repaid). These agreements often provide for oversight by a committee of the creditors and will often involve contractual promises by creditors to forbear from exercising their previously existing rights until a defined triggering event.

Statutory Remedies: UCC Article 9 Sales and ABCs

If the contractual remedies described above are akin to Chapter 11 bankruptcy proceedings, whereby a company in dire (but ultimately salvageable) straits continues to operate while its debt obligations are reorganized, state law statutory remedies are analogous to Chapter 7 bankruptcy proceedings; the business is a sinking ship and must liquidate its assets to maximize payments to its creditors (in the bankruptcy context, per the rules of absolute priority). Such liquidation is governed by rules under state law which may be available to cannabis companies.

If a creditor has a security interest in the collateral of a debtor, then the most popular option is usually a sale under Article 9 of the Uniform Commercial Code (UCC). The UCC is a standardized set of laws and regulations for conducting business, including lending. The UCC itself is not law; rather it is a codex that has been adopted by most states and incorporated into their statutes as law, usually with some variations. UCC Article 9 deals with secured transactions and, in particular, provides for the sale and disposition of collateral subject to a security interest upon a default by the debtor. Similar to a §363 sale under the Bankruptcy Code, a sale under UCC Article 9 provides for a “friendly foreclosure” whereby a defaulting debtor and its lenders cooperate to facilitate a sale of the secured collateral.

Article 9 imposes certain parameters on such dispositions, including that foreclosure sales be “commercially reasonable”, which the UCC specifies as meaning that the collateral be sold in a reasonable and customary manner on a recognized market, at then-current market prices. If the sale was approved in a judicial proceeding, by a bona fide creditors’ committee, by a representative of creditors or by an assignee for the benefit of creditors, then this creates a presumption of commercial reasonability under the UCC.

A less common option is an assignment for the benefit of creditors (ABCs). Laws governing such assignments vary by state and are generally rare, with California being a notable exception where both ABCs are more common and where cannabis is legal. An ABC is initiated by the debtor, which then enters into an agreement to assign its assets to a third-party assignee, which holds such assets in trust for the benefit of the creditors and is then responsible for their liquidation, similar in principle to a trustee in bankruptcy.

ABCs, however, are generally not suitable for cannabis companies as the third-party assignee would not be able to take possession of a licensed cannabis business, or certain assets such as cannabis plants, distillates and other products, without itself being licensed by the relevant state regulatory agency. A similar problem occurs under Article 9 sales, whereby the purchaser of the collateral must be licensed in order to possess and operate cannabis product and, more importantly, the all-important state-issued licenses which provide a cannabis company with the authority to operate as such; the pool of potential purchasers is therefore limited to those purchasers already licensed or which are willing to undergo the burdensome process of becoming licensed, hence shrinking the market for such assets and reducing their value. These issues may be resolved in some states by the assignor/seller entering into a management services agreement with the assignee/purchaser, pursuant to which the assignee/purchaser effectively manages the operations of the cannabis business. These agreements, however, need to be carefully drafted so that they are not seen as constituting ownership of the business by the assignee/purchaser (until the actual transfer of the licenses occurs), as defined under applicable state law.

While absolutely true for “plant-touching” companies, recent cases in the federal Ninth Circuit Court of Appeals provide some (fact-dependent) hope for cannabis-adjacent companies such as those housing the employees or intellectual property of a plant-touching operational cannabis company (this structure itself largely a solution to deal with federal illegality).

By Abraham Finberg, Rachel Wright, Simon Menkes No Comments

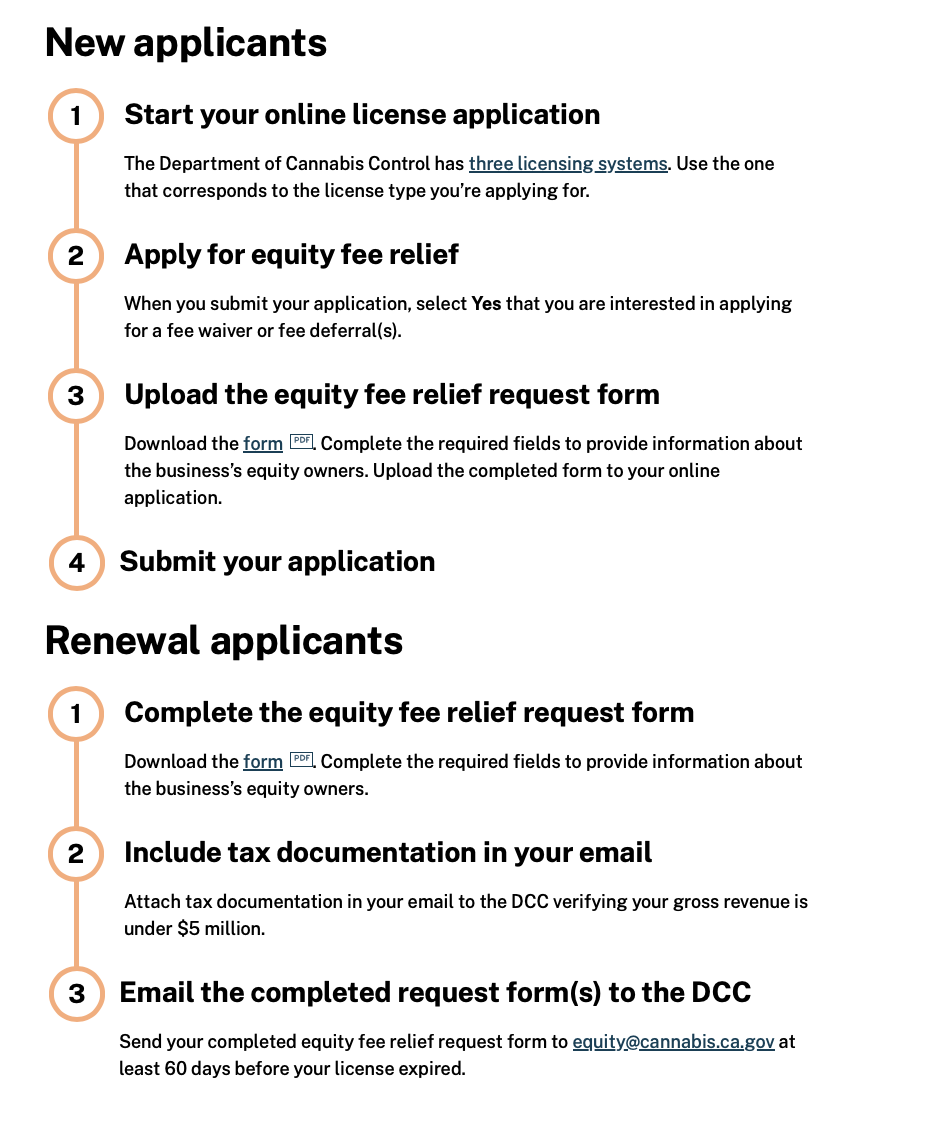

In a move that Old Guard California Cannabis viewed with bittersweet appreciation, the Department of Cannabis Control on January 1, 2022 announced it would waive license fees for those cannabis companies impacted by the War on Cannabis. Many pre-2017 operators experienced persecution by law enforcement including confiscation of inventory. For those who refused to admit defeat and remained in or returned to the business of cannabis, this significant fee waiver feels something like an apology.

As we move through Year 2 of the Equity Fee Waiver, it’s important for all cannabis companies to review their history and their current operations to see if they qualify for this significant reduction in expense. Instead of arrest or conviction, a cannabis business may also qualify through its eligible owner’s income level or location of residence. Since this is a fee waiver for small businesses, a maximum yearly revenue level of $5 million is also a requirement.

For those Qualified Equity Licensees who have already received a fee waiver, it’s important to remember that this is a yearly process, and that they must continue to submit a request for equity fee relief at least 60 calendar days before the annual expiration date of their license.

Who Qualifies for the Equity Fee Waiver?

Gross Revenue: Your cannabis business must have no more than $5 Million gross revenue per year.

Equity Ownership: At least 50% of your business must be owned by people who have only ONE of these three characteristics:

Have experienced a cannabis conviction or arrest, or

Have a lower income level, or

Reside in a neighborhood affected by the criminalization of cannabis (as defined by the DCC)

Arrest or Conviction

The DCC requires that the equity individual have been convicted or arrested for cannabis crimes before November 8, 2016. Crimes must have been sale, possession, use, manufacture or cultivation. The equity individual may also be eligible if an immediate family member was convicted or arrested for cannabis crimes and the equity individual themselves lived in a California county with drug arrest rates that were higher than the state average drug arrest rates.

Residence in a Neighborhood Affected by Criminalization of Cannabis

If an equity individual seeks to qualify by location of residence, they must have lived in the qualified location for at least 5 years between 1980 and 2016. The location must have higher than state average drug arrests and be in the top 25% nationally for unemployment and poverty. The DCC provides an interactive map to check your location for these requirements.

Worth the Trouble

Again, your business needs to be below $5 million annual gross revenue, and at least 50% of the ownership needs to have only 1 of 3 disadvantaged characteristics: cannabis arrest or conviction, or lower income level, or residence in an affected neighborhood.

While it will definitely take time to apply for the Equity Fee Waiver, the savings in zeroed-out license fees can certainly make it worthwhile. In addition, qualifying for the Equity Fee Waiver makes a business eligible for other state equity tax advantages including the California Equity Tax Credit. (See our article on the CETC here.)

The Tohiyusdv Cavalry is a black-owned small business based in rural Virginia. At its core, they grow and process cannabis for CBD products, but it’s really much more than that. Through its Precision Craft Farmer Program, the company works with existing small minority-owned farms to introduce them to the cannabis market.

Via land leasing, profit-sharing, crop-sharing, facility design, community involvement and incubator-style support, Tohiyusdv Cavalry has built a network of farmers and a community around them that work together to gain access to the larger cannabis market.

Tohiyusdv, pronounced “toe-hee-yoos-da,” means “calm” and comes from a Native American dialect in the region. James Arrington III, founder of the company, is both African American and Native American, so the name is a nod to his roots. While Arrington insists he is just one part of this larger organization, it’s his passion for community, small business, social equity and cannabis that drives the company.

James C. Arrington III, founder of Tohiyusdv Cavalry

We sat down with James to learn more about the Tohiyusdv Cavalry, a bit of his background, how him and his community have found success and what they hope to achieve.

Different Sides of the Tracks

He grew up in Norfolk, Virginia alongside his two brothers and sister with a view of two different lifestyles. “We grew up in the hood of Huntersville, but I was raised in a white church, so it was interesting seeing both sides of the tracks and seeing the side that some of my friends couldn’t see,” says Arrington. The dichotomy of his upbringing gave him a unique perspective that he took to heart, eventually going to Old Dominion University for electrical engineering at the encouragement of a teacher.

Throughout his formative years, he didn’t really get involved with cannabis – that came much later. In his college years though, he met his Delta Chi fraternity brother Ernest Toney, who would go on to become the founder of BIPOCann, a nonprofit that helps social equity entrepreneurs, minority business owners and professionals in the cannabis industry.

Arrington with a recent indoor hemp crop

Working as an electrician to pay for tuition, Arrington graduated and launched what would become a successful career in electrical engineering. He worked as a subcontractor for the government in warzones, designing electrical systems with security and defense in mind, before starting his own company CalArr Consulting. “What really tied me to the industry was when I started using cannabis for my mental health and to understand who I am,” says Arrington. A combination of his upbringing and his career led to his PTSD, which then led him to cannabis as a tool for his wellbeing and mental health.

More recently, he spoke with Ernest Toney, who said, “Look man, I’ve seen what you’ve done with your business over the years and you should consider getting into the cannabis industry.” Arrington took that advice and ran with it. “So, the company I started is a mission-driven company based around healing, cannabis, understanding and helping people,” says Arrington. “Tohiyusdv Cavalry is based around working with small farmers and minorities; We introduce them to the cannabis industry.”

Here Comes the Cavalry

Right now, his company works with hemp and CBD products, but he says they are looking to expand into the THC market once Virginia legalizes and they already have some partners they’re working with in other states to expand the program.

Tohiyusdv Cavalry has been around for about two years now and Arrington says the heartbeat of it is their craft farmer program. “These are existing minority farmers in a community, already growing crops like soybean or corn,” says Arrington. “These are generational farms that have been passed down through family, some of them almost 100 years. They’ve always had to change with the times.” In changing with the times, a lot of these small, rural farms are seeing the hemp market as a possible pivot, but hardly know where to begin. “They are starting to hear about farmers in their community growing hemp, but having trouble finding folks to buy their crop.”

Some of the products from Tohiysudv Cavalry

That’s where the Cavalry comes in. “What you see in minority backgrounds is a lot of opportunities like this that are very scary to step into,” says Arrington. “We’re teaching people how to get into the industry, helping them through processing and getting on the market using new technology, and we do it at their pace.” Some folks in their network just want to rent space on their farm out to a hemp grower, others want to dive right in and create CBD products. They operate a white label program for some and help set up turnkey facilities complete with extraction and processing for others. “We work with them to build a community around their farm,” says Arrington. “We are just the engine behind these small farmers helping them get access to the larger market.”

From the Ground Up

A good example of the work they put in is Everbreeze Acres. Based in Rustburg, Virginia, Everbreeze is a 434-acre farm and bakery that’s been in the same family for generations. They had an interest in the cannabis market, so they approached Tohiyusdv Cavalry. James and his crew came in and built a 2,000-square-foot facility that is hydroponic, fully turnkey and automated. “We are teaching them the process and turning it over to them,” says Arrington. “We are teaching them how to take care of the plants, grow the crop, harvest and process it, all while collecting data.”

Everbreeze Acres

Before brainstorming how they want to market their products and how they want to be represented, the owners of the farm were still a little skeptical. Being in their 70s, they wanted to make a product that has some medicinal properties and could help people take care of themselves. So, James and his team put together a plan to launch a daily supplement, akin to a multivitamin.

Now Everbreeze Acres is using CBD as a megaphone to communicate their story. They were wary at first, but learned about it, grew to like it and now run a fruitful cannabis business. “We have their facility up and running and we’re growing several strains that work best for them right now,” says Arrington. “We’re about a month away from another harvest there.”

Building Community

Everbreeze Acres embodies the concept of the Tohiyusdv Cavalry. Helping small farmers establish themselves in the cannabis industry, building community around them and working to help their following and their mission.

A Tohiyudv Cavalry cultivation facility

Small business is the keystone of many communities, the cannabis industry included. Economic empowerment is sort of a way of staving off big business too. Given the history of big tobacco in the Virginia area, many stakeholders are worried if they’ll still have a seat at the table when Virginia legalizes adult use cannabis. “Looking at it in that sense, we are hoping that creating this group of diverse minds and backgrounds is building a table where everyone can sit at,” says Arrington. “We want to provide that place for them and let them know that, yes, this is the room for you, this is the place for you. We’re lending a helping hand and giving them a voice and a megaphone, sharing what they want to see in this industry.”

When asked what advice James would give himself ten years ago, the mood was somber. “Ten years ago, my mentor, alumni Dave “BamBam” Hoffman died. I would say that was the thing that gave me that kick in the ass, that I wasn’t doing everything I could do.” He has the same advice for minorities and indigenous people getting into the industry now: “Don’t be afraid to do it, the skills that you have you can put into the industry in some way. Your fit is out there. If it’s the right way, it’s never going to be easy. Push through it, keep going,” he says.

Growing in Virginia

Tohiyusdv Cavalry is ready for the day that Virginia legalizes adult use cannabis, but James says he hopes they make room for the small farmers. “Small farmers are what makes Virginia, Virginia.” They are in talks with some larger medical cannabis companies about creating similar programs for sourcing from craft growers. Through their strategic partners, a big part of their work right now is around partner and sponsor outreach, getting more businesses interested in sponsoring facilities and investing with small farmers. “Our hope is that we’ll be able to keep expanding the program and involve more minority farmers in Virginia and that it will only keep growing,” he says. “We’re optimistic that we’ll have three more farms signing on this year. And hopefully when Virginia legalizes adult use cannabis soon, we’ll be ready to expand in that market and keep on growing.”

By Abraham Finberg, Simon Menkes, Rachel Wright No Comments

Although Rhode Island is the USA’s smallest state, it has traditionally taken an out-sized dislike for cannabis and its users. It first banned cannabis in 1918 and, up until recently, had some of the strictest mandatory minimum sentences for large-scale possession, sentencing those with more than 5 kg (11 lbs) to 20 years’ imprisonment and fines of between $25,000 and $100,000.

Rhode Island’s Change of Heart

These days, however, the Ocean State has turned over a new leaf. It legalized medical cannabis in 2006, and on May 25, 2022, legalized adult use sales as well. Starting in December 2022, Rhode Island residents could purchase cannabis from five of the six medical cannabis dispensaries across the state which have also been approved to sell to adults.

Over the course of 2023, the state is expected to issue licenses for an additional 28 dispensaries, including a portion reserved for social equity applicants and worker-owned cooperatives. At the same time, 33 cities and towns across Rhode Island voted to determine whether cannabis businesses would be allowed in their jurisdiction. 25 of these municipalities ended up approving these measures.

Social Equity

Like many retail-legal states, Rhode Island has enacted social equity support for cannabis licensees. The state is divided into six retail license zones, and within each zone, one retail license will be reserved for a social equity applicant and one for a worker-owned cooperative. In addition, the state’s cannabis legislation provides for a $1 million fund to help support the social equity license recipients. Funded by all fees collected from adult-use cannabis businesses, this assistance fund will provide grants, promote job training and workforce development, and administer programming for restorative justice. The legislation also establishes a process whereby individuals may have their misdemeanor or felony convictions for cannabis possession expunged.

How Tax-Friendly Toward Cannabis is Rhode Island?

The Ocean State still has a way to go to be considered a truly cannabis-friendly state. For one thing, the state is forcing both individuals and corporations to conform to Internal Revenue Code section 280E which disallows deductions and credits for expenditures connected with trafficking in controlled substances under the Controlled Substances Act, schedule 1 or 2. This means cannabis companies will only be permitted to reduce their sales by cost of goods sold when determining their taxable income on their state tax returns unless they decide to take more aggressive tax positions. For example, with a conservative IRC 280E tax position, a cannabis dispensary would only be allowed to deduct the cost of the product purchased and the cost to transport the product to the dispensary, while disallowing such significant expenses as rent and payroll. All cannabis businesses must forgo expense deductions related to selling, general and administrative expenses, as they are disallowed under the tax code under this traditional method. Rhode Island has also disallowed cannabis businesses from taking an R&D tax credit as a result of conformity with federal tax law.

In addition, Rhode Island is requiring retailers to collect 10% state cannabis excise tax plus 3% local cannabis excise tax from its customers, along with the standard 7% sales tax. Good news: sales tax is not calculated on the excise tax collected (unlike California, which does impose tax-on-tax). Medical sales are subject to sales tax but not to excise tax, and excise tax is not charged on cannabis accessories. Excise tax, like sales tax, must be remitted to the state by the dispensary on or before the 20th of the following month.

In Summary

Rhode Island has taken a big step forward from its anti-cannabis past by legalizing adult use sales and by supporting equity applicants as well as the expungement of past criminal convictions for many of those victimized by the war on cannabis. While Rhode Island’s excise taxes are not the worst we’ve seen, the state’s support of 280E will make it a lot harder for cannabis businesses to thrive.

In 1996, the Harvard Business Review published an article called Making Differences Matter: A New Paradigm for Managing Diversity, in which the authors argued that companies should adopt a radically new way of understanding a diverse workforce. Instead of hiring employees of different backgrounds and asking them to blend in, or limiting people to areas of work based on their identity, they suggested embracing and bringing together the varied perspectives and approaches to work that members of different identity groups bring. Since then, a steady stream of companies – from GE to PricewaterhouseCoopers to cannabis companies – have implemented several new practices, initiatives and programs under the category of Diversity, Equity and Inclusion (DE&I).

DE&I has become highly important over the last few years, and many companies are seeing the benefits. Today, 83% of professional investors are more inclined to invest in stock of a company well-known for its social responsibility. On the other hand, a company that is seen as not responsible stands to lose as much as 39% of its potential customer base, with one in four consumers telling their friends and family to avoid it. As these benefits draw more companies to focus on DE&I, it’s important to remember that your plans should ultimately be centered around uplifting employees from all backgrounds.

“Listen, test, learn and then listen again!”While still relatively new to the cannabis sector, one DE&I initiative that is making some headway towards that goal is the Employee Resource Group (ERG). Essentially, it’s a group of employees who join together in their workplace based on shared characteristics or life experiences. ERGs work to create communities which bring people together, with internal and external partnerships to support those groups, and they are gaining popularity. In fact, according to a Bentley University report, almost 90% of Fortune 500 companies utilize them. They’re often used because issues are addressed from within an organization by the people who are most directly impacted by them. They can also serve as a direct pipeline of communication between employees and employers, as well as a place for new ideas and solutions to problems to blossom.

When it comes to recruiting and retention, ERGs have their own specific benefits. According to a survey conducted by Software Advice, 70% of respondents between 18 to 24 years old and 52% of respondents between 25 and 34 reported they would be more likely to apply for a role at a company that had ERGs. With regards to retention, 50% of survey respondents across all ages stated they would remain at a company because it had an ERG.

While some in the cannabis sector have already implemented ERGs, this new practice is one that all cannabis companies should consider – particularly as this industry grapples with its own unique DE&I challenges and history. To that end, check out the tips below to help get you started.

Gauge interest: Many ERGs start organically. The first question you need to answer before you can start building an ERG is to ask if your employees want one. The statistics indicate they likely will, but it’s important to establish that leadership is willing to listen. Employees should play a major role in this process from the beginning. However, remember that the DE&I strategy is not their responsibility, and ERGs should be a part of a more comprehensive plan.

Find the willing and work with them: You’ve got to find the people that these topics matter to and embrace them. Participation is key, and if the topic at hand is one that someone is not personally connected to, your ERG may not live up to its full potential. ERGs are a significant time investment, so you have to make sure those taking part are ready, willing and capable of balancing their job responsibilities with their additional role in the group. Participation goes both ways, too. You have to make sure that managers are aware that someone is in an ERG. “Be open to making mistakes and learning from them, and then changing for the better.”

Use executive sponsors: An essential piece of successfully incorporating ERGs into your organization is recruiting executive allies from the corporate side to serve as sponsors. This can help break through barriers, get decisions made, and keep all parties organized. Executive sponsors are also great for employee development, as they can see firsthand the talent in the organization and become a mentor. Executive sponsors are often an important request from ERGs, and they are worthwhile to recruit for. Sponsors don’t have to be from the same affinity as the group, and in some ways, that can actually be a good thing. Solidarity is another important factor to company health, and allyship is imperative for solidarity.

Set goals: Define a mission early on. It’s important for ERGs to have a strong mission statement with core goals that the group is formed around achieving. Keep in mind, these need to be tangible goals with specific benchmarks. It can’t just be “increase diversity in hiring.” Set a number you’d like to reach and a date you’d like to reach it by. Having clear objectives keeps a track record for your ERG, and is the foundation for success. These will also ensure that your ERG is not just for marketing purposes. Achieving substantive goals will keep the group going, as confidence gets built on the inside and from the outside.

Be clear: ERGs are all about communication, so clarity has to be a top priority. None of the above tips work without that. You have to make sure the groups are not questioning what is expected of them, what resources they have to work with and what goals they are working towards. It’s always going to be a learning process, and there will certainly be unforeseen challenges, but being on the same page from chapter one will make the process that much more beneficial to all involved.

As stated above, ERGs are still new, just like the industry we want to bring them into. Be open to making mistakes and learning from them, and then changing for the better. That process is what ERGs are about at their core, after all. Listen, test, learn and then listen again!

Businesses often require outside capital to finance operating activities and to enable scaling and growth. Financing in the cannabis industry is notoriously challenging with regulatory obstacles at the local, state and federal levels. Recent market dynamics pose additional challenges for both financiers and cannabis operators.

We sat down with Travis Goad, Managing Partner of Pelorus Equity Group to learn more about Pelorus and to get his perspective on recent market trends.

Aaron Green: In a nutshell, what is your investment/lending philosophy?

Travis Goad: Our investment and lending philosophy is focused on being honest, upfront and doing what we say we’re going to do for both our borrowers and our investors. At Pelorus, we lend against cannabis-use real estate assets.

Every lender in this space is a hybrid between real estate and corporate lending. However, if you think about it as a political spectrum, with one side being pure real estate lending and the other pure corporate lending, Pelorus is as close as you can be to pure real estate lending in this sector while also being properly collateralized. What sets us apart from our recently launched lending peers is that we lend against the real estate asset value only, even though we’re collateralized by the real estate and license.

We lend between 60% to 75% of the value of the real estate, which means sponsors need to raise equity for the 25% to 40% remainder of the project cost. This allows us to be covenant-lite for our borrowers while giving them the flexibility to grow their business as they see fit.

Travis Goad, Managing Partner at Pelorus Equity Group

The other lending options in the space are much different. While our lending peers may call themselves mortgage REITs, they really are based on a business development company (BDC) lending model. While they may lend borrowers as much as 150% to 180% of the real estate value, they will require significant financial covenants, require control of major decisions and most often want a board seat. We’ve seen this model severely hamstring growth of companies.

The third option available to sponsors is a sale-leaseback. In this structure, lenders will buy your real estate for 100% of the value, but require you to enter into a 15-to-20-year lease that increases 3% each year. There is a temporary benefit to this model from a federal tax perspective, but that will go away when 280E is addressed, either by descheduling cannabis or amending the tax code.

While this structure means you don’t have to raise equity, it gives up the most valuable asset cannabis companies have in the early stages of the industry. Once you sell this asset, it hampers optionality for sponsors – and in a fast-growing industry like cannabis – optionality is the most critical thing a company has. Pelorus’ structure allows maximum optionality, as well as the ability to lower your cost of capital as the industry matures.

From an investor standpoint, they should know that the BDC and sale-leaseback models are a lot riskier than our model. While we’ve seen those models work well in mature industries, we think the cannabis industry is too early-stage and too volatile to go that far out on the risk spectrum. We have the longest history in the space of deploying capital successfully and seeing it returned. Prior to making any loans, we spend a lot of time underwriting the company we’re working with, the real estate and the projections. We look for strong sponsors, great projects and attractive markets.

Before we entered the cannabis lending space, our team at Pelorus had more than 5,000 transactions under our belt, worth $5B, and we leveraged our decades of underwriting experience when starting the Pelorus Fund. As the first dedicated lender in the cannabis space, we have more data and experience than anyone in terms of transactional volume – we’ve looked at more than 2,000 deals and have made 71 deals, worth $468M. We know the intricacies of every market, the particular ordinances, what the costs should be, and utilize the data to help our borrowers succeed. Through our deals and sustained success, we’ve made a name for ourselves as the most trusted and efficient lender in the cannabis space.

Green: What types of companies are you primarily financing?

Goad: We finance construction and stabilized loans for a range of clients including MSOs, SSOs and ancillary companies. We don’t lend on outdoor cultivation, but are open to working with any cannabis-related business that has commercial real estate, strong financials and experience in the cannabis space. Today, our sweet spot is closing loans in the $10M to $30M per transaction range, but we can fund loans $100M+ and as low as $5M. Since 2016, we’ve financed 4.2M feet of cannabis-use properties for a total of $468M in loans – roughly 15% to 20% of the entire US market.

Green: What qualities do you look for in a cannabis industry operator or operating group?

Goad: We are meticulous in our underwriting process and underwrite the company, the real estate and the market. We’re one of the few lenders today that has capital to deploy, which has given us the opportunity to continue to take market share while also increasing the quality of our borrowers. Whether you’re an MSO, smaller state operator or ancillary business, we recognize quality across the sector. Brand affinity and shelf space are critical in this market, and we like working with companies that have a competitive edge in getting their branded product to customers. We try to target companies that offer a unique product, or have a unique position within the state they are located.

To qualify for our lending program, borrowers need to own their real estate. If the sponsors own the real estate or intend to own the real estate, we offer two main lending products: we provide construction loans that range between 60% to 75% of the project that are typically 18-month terms; and more recently implemented, we also lend on fully stabilized assets that are cash flowing and operational up to 75% of the value and up to a 5-year term.

By the time a borrower comes to us, they should already have a license (or be acquiring a license at closing), have their required equity raised to completely fund the project and have all local approvals to begin construction.

Green: Capital market dynamics have led to significant public cannabis company revaluations in 2022. How has this affected your business?

Goad: As far as how market dynamics have impacted our fund, we’ve been pretty insulated because we are a privately held company. From our inception, we’ve worked hard to create an innovative model, and have had many firsts. We were: the first dedicated lender in the cannabis sector; the first lender to become a private mortgage REIT; the first to be issued an FDIC warehouse line of credit; the first to get an investment grade rating; the first to issue an unsecured bond with institutional investors; the first to update our fund to a billion dollars. Amid all these firsts, we made a conscious decision not to go public. This has been one of the best decisions we’ve made and has shielded us from much of the market volatility we are seeing.

As for the broader market, we’ve seen our sponsors that are publicly traded impacted pretty significantly by the recent market dynamics. We’ve also seen flow-on effects for non-publicly traded firms. Our loan book is performing excellently, but we’re in a very challenging market for marijuana-related businesses to raise equity, making debt even more attractive. For most of our competitors, who chose to go public, they’ve been unable to raise much capital to deploy, whereas our market share is increasing and we continue to grow in this tough environment. We remain bullish on the sector in the medium/long term and are finding excellent opportunities to lend in this challenging environment.

Green: Debt on cannabis companies balance sheets have increased significantly in recent years. What is your perspective on that?

Goad: Increased access to debt capital markets is a sign of a maturing market. The U.S. cannabis sector has a great tailwind with growth of new markets, but it’s facing some significant headwinds tied to tax inefficiencies and inadequate state-level enforcement. All of these issues can be solved with political action, but so far that hasn’t happened and it’s causing pain in the industry. These industry dynamics are set against a broader macro backdrop of risk-asset repricing and increased volatility, which leads to outsized volatility in cannabis due to limited liquidity. That increased volatility has made it very challenging to raise equity in this market.

For companies that have strong assets on their balance sheet, they’re still able to access capital via the debt markets. This is creating clear winners and losers, as companies that choose to sell their real estate have significantly fewer capital raising options than those that choose to keep real estate assets on their balance sheets. Overall, this increased debt trend has been great for our business – our pipeline has increased rapidly and we’re able to lend to strong operators with solid assets at attractive rates for investors. Our fund continues to have inflows, and since we’re one of the few lenders with capital to deploy, we’re still open for business and deploying capital in this challenging environment.

Green: How does the lack of institutional investor participation in the cannabis industry affect your business?

Goad: The current regulatory environment impacts the type of investor that comes into this space. Rather than being dominated by institutions, this sector has largely been funded by retail investors and family offices. This has created challenges in aggregating large amounts of capital, both on the operator and the debt-fund side of the business. It can lead to delays in loan closings, as it takes borrowers a longer amount of time to raise the required equity to close their transaction. As we’re seeing with our publicly traded peer group, it can also lead to lenders having trouble raising capital to deploy. As for Pelorus, we’ve been very fortunate that our length of time in the industry and track record of successfully making loans and having them repaid has set us apart in fundraising. Our decision to stay private has been a critical factor in our fundraising success as well. Overall, the lack of institutional investor participation is a double-edged sword: the lack of liquidity has caused challenges broadly, but since we’ve had significant capital to deploy, it’s created great opportunities for us to make loans with attractive risk/returns in this challenging market.

Green: What would you like to see in either state or federal legalization?

Goad: Given the stalemate in the Senate and the sharp bipartisan divide, I don’t think federal legalization will happen during this administration. That said, there are incremental actions that the government should take to strengthen the cannabis sector. First of all, the Cole Memo needs to be reinstated to add additional protections for cannabis and cannabis-related businesses. As 280E has clearly been detrimental to the overall health of the cannabis industry, we also believe the tax code should be amended, or better yet, we should address the conflict between state and federal policy. We also need to get SAFE Banking approved in order to open up the cannabis sector to credit cards and potentially open up banking to the sector in a more material way. Unfortunately, there’s a choke point in the Senate to get SAFE Banking approved, since there needs to be 60 votes to be filibuster proof. And while there is some talk of SAFE Banking passing during the lame duck session, we are not holding our breath.

Green: What trends are you following closely as we head towards the end of 2022?

Goad: The biggest trends we’re following are on the legislative front (both federally and at state level), which heavily impact revenue and net cash flow growth for the industry. We’re following emerging state markets, such as Alabama and Mississippi, as well as current medical markets poised to transition to adult use in the near term, such as Missouri. The more addressable the population, the faster the industry can grow.

We’d also like to see current legal states address the often-heavy tax burdens that have led to additional challenges for legal businesses and kept illicit markets thriving. No state got everything right at the beginning, but we’re starting to see states address some of the inequities and harmful policies now. California has made some progress in this area, however there are many issues that still need to be addressed.

Federally, 280E is the other major headwind that needs to be addressed as extremely high tax rates are one of the biggest problems for the industry. We’d really like to see that addressed, as cannabis is the only new industry, I’m aware of in the U.S. that has had such disadvantages out of the gate.

Doing business in California’s legal cannabis industry remains a risky endeavor. The majority of the industry is still unlicensed, tax rates at the state and local levels are high (notwithstanding a recent reprieve from California’s cultivation tax) and there are not enough licenses to meet geographic demand throughout the state. Outside financing remains difficult to secure for equipment, tenant improvements, account receivables and working capital because, under the federal Controlled Substances Act (CSA), cannabis remains a Schedule I narcotic. Therefore, entrepreneurs, investors and lenders who have stakes in state-sanctioned cannabis enterprises expect to see returns that justify the higher level of risk, which places additional financial pressure on cannabis businesses. In addition to the industry specific challenges, the United States economy is on the verge of a recession that may further hamper the industry notwithstanding the industry’s resiliency during the pandemic when it was deemed to be an “essential” industry that benefited from consumer spending of stimulus monies.

These outside pressures increasingly lead to ownership disputes and creditor defaults that result in litigation and the need for restructuring. In some instances, business partners cannot agree about control and finances of the licensed businesses and in other instances unpaid creditors file suit to enforce their interest in a company’s assets. And sometimes a local municipality discovers wrongdoing by an operator and initiates a health and safety lawsuit to cease the illegal condition.

Bankruptcy reorganization is an option typically utilized by struggling businesses to shed or restructure debt. Cannabis businesses, however, cannot take advantage of bankruptcy remedies because bankruptcy is a product of federal law and federal law still prohibits the sale of cannabis.

As a result, stakeholders in legal California cannabis enterprises must consider alternatives to bankruptcy to collect what they can on their loans and investments in the event the enterprise becomes insolvent or requires restructuring. A well-established alternative to bankruptcy is a state court remedy – the appointment of a receiver over the assets of a business or over the entire business operations. Through the receivership process, stakeholders may obtain many of the same protections available to them through bankruptcy

A. Federal Illegality Bars Access to Bankruptcy Protection

Over the past ten years, bankruptcy courts have routinely prohibited licensed cannabis businesses from seeking bankruptcy protection because cannabis remains illegal at the federal level under the Controlled Substances Act (CSA). Bankruptcy trustees are typically charged with managing and operating property in the same manner that the owner would be bound to do if in possession thereof. Because cannabis remains illegal at the federal level, trustees are not able to manage and operate licensed cannabis businesses.

B. Receivership as an Alternative to Bankruptcy

Under California law, a receiver is a neutral agent of the court appointed to preserve, control, manage and ultimately dispose of property that is subject to the litigation before the court.1 The receiver, therefore, holds property for the court, not the parties to the litigation.

Appointment of a receiver is a statutory provisional remedy. Other than corporate dissolutions under Code of Civil Procedure section 565, the law does not have a specific cause of action to appoint a receiver. Thus, the proponent of a receiver must have a valid cause of action in an underlying lawsuit.

1. The Appointment of a Receiver

The appointment of a receiver rests within the trial court’s discretion. Code of Civil Procedure section 564 contains the broadest statutory authority to appoint a receiver. Subdivision (b), details twelve possible situations in which a receiver may be appointed, most of which are beyond the scope of this article. The most common of these is a lender’s request to appoint a receiver when a borrower defaults on a loan and the lender seeks the appointment of a receiver over its collateral. The statute, however, clarifies that the situations listed in the statute are not exclusive: a court may appoint a receiver “[i]n all other cases where necessary to preserve the property or rights of any party.”

The receiver’s powers are limited by the statute under which the court appointed the receiver and those conferred by the court. The appointment order should, therefore, detail the duties the receiver owes to the court, and actions that the court authorizes the receiver to take to perform those tasks. The order should also specify the property that will be part of the receivership estate.

2. The Receiver’s Powers

The receiver has general statutory powers.2 The statutory powers include (i) commencing or defending litigation; (ii) taking and possessing property of the receivership estate, (iii) receiving rent, collecting debts, and making transfers, and (iv) acting in accordance with the court’s instruction with respect to the property.3 But the court’s authorization is necessary to sue the receiver and for the receiver to commence litigation.4 In the foregoing scenarios, the receiver is immunized personally from tort liability, but not in his or her official capacity as receiver.5

In addition to taking possession of property, the receiver may dispose of receivership property with the court’s approval.6 If the receiver is an equity receiver, the receiver may take possession and satisfy creditors from all the debtor’s assets.7

The court may further authorize the receiver to issue “certificates of indebtedness” to raise money to administer the receivership estate.8 This device permits the receiver to provide liquidity to the estate and gives the certificate holder an interest-bearing priority claim against the receivership estate.

3. Liquidating Cannabis Assets Through a Court Appointed Receiver

After the court appoints the receiver, the receiver should have sufficient powers to, among other things: (i) take over the management of the company; (ii) open bank accounts; (iii) borrow money by issuing receivership certificates; (iv) manage all of the company’s property; (v) hire counsel and other professionals; and (vi) sell the receivership estate’s assets for the benefit of the creditors. To maximize repayment to the creditors, the receiver may hold an auction to sell the assets and assist in facilitating the cancellation of company’s state license while the buyer of the assets secures its state license after the local license is transferred.

State cannabis licenses may not be sold or transferred.9 Yet, to maximize recovery for the creditors, the receiver may need to participate in the regulatory process to maintain a license during the pendency of the receivership and to assist in the amendment of a license while a prospective buyer seeks to obtain its own license. To do so, the receiver will first need to qualify as a licensee under state law to join as a licensee on the license and further the licensee as a going concern. Next, the principals of the prospective buyer will themselves need to qualify as licensees under the license. Then, once the sale of the company’s assets (including any interest in the license) to the buyer closes, the receiver and the company’s original owners will terminate their capacities as licensees of the license, leaving only the new owners as licensees. Thus, the proposed order should be written with attention to ensure the receiver has powers to further the foregoing and not diminish the value of the receivership estate.

After the conclusion of the sale of all assets, the receiver will need to obtain a discharge from the court of his or her duties as receiver. The receiver may do so by the parties’ stipulation or by motion. Together with the request for a discharge, the receiver should seek approval to pay: (i) any lenders to the receivership estate; (ii) professionals that the receiver hired; and (iii) him or herself for his or her services. Upon the court’s approval, the receivership will be terminated.

The conflict between federal and California law regarding cannabis continues to be an impediment for stakeholders in California’s cannabis market. Because of this conflict, stakeholders in California’s legal cannabis market lack access to vital traditional institutions, such as bankruptcy remedies. As a result, stakeholders must be prepared to consider alternatives such as a court appointed receiver, which can be a useful alternative to both secured creditors and unsecured creditors. Stakeholders who pursue a court appointed receiver will benefit from a long-established body of law and experienced professionals.

Like this article and want to see more? Subscribe to our free newsletter here The cannabis industry could receive a significant boost if the recently introduced Capital Lending and Investment for Marijuana Businesses (CLIMB) Act passes Congress. The bipartisan bill was introduced by Rep. Troy A. Carter, Sr., a Democrat from Louisiana, and Rep. Guy Reschenthaler, a Republican from Pennsylvania. It is intended to boost the cannabis industry by creating greater access to capital, banking insurance and other business services. Unlike the SAFE Banking Act (which specifically addresses banking services for the cannabis industry), the CLIMB Act was introduced “to permit access to community development, small business, minority development and any other public or private financial capital sources for investment in and financing or cannabis-related legitimate businesses.”

Rep. Troy A. Carter, Sr.

Currently, the cannabis industry faces a serious dilemma with regard to accessing not only traditional banking services, but also essential capital and financing sources. The latest member of the cannabis bill alphabet soup attempts to remedy this by addressing two key issues.

First, the CLIMB Act would permit access to key “business assistance” programs from various financial institutions by prohibiting any federal agency from bringing any civil, criminal, regulatory or administrative actions against a business or a person simply because they provide “business assistance” to a cannabis state-legal company. The CLIMB Act defines “business assistance” broadly to include, among other things, management consulting work, accounting, real estate services, insurance or surety products, advertising, IT and other communication services, debt or equity capital services, banking or credit card services and other financial services.

This provision of the CLIMB Act would immediately create more access to traditional insurance, lending and credit. This broad protection would not only apply to private entities providing “business assistance,” but arguably means that the U.S. Small Business Administration (SBA) could not be penalized by Congress or another government agency for providing loans to state-legal cannabis companies. Moreover, currently the cannabis industry does not have access to use credit cards, as major credit card companies refuse to permit such transactions. The CLIMB Act could pave the way for major credit card providers to begin permitting cannabis transactions. Permitting the use of major credit cards like American Express, Mastercard and Visa could result in an increase in sales for cannabis retailers.

The second, and possibly the most important, aspect of the CLIMB Act is that it would amend the Securities and Exchange Act of 1934 to create a “safe harbor” for national securities exchanges like Nasdaq and the New York Stock Exchange (NYSE) to list cannabis companies and would permit the trading of these cannabis businesses stock. Currently, plant-touching cannabis companies with operations in the U.S. can only be listed on a Canadian-based exchange and can also only be traded in the U.S. via the over-the-counter (OTC) markets. Trading securities on the OTC markets does not provide the same level of security as securities traded on a national exchange like Nasdaq or NYSE. Specifically, the CLIMB Act delineates that the federal illegality of cannabis is not a bar to listing or trading of securities for legitimate cannabis-related businesses.

Rep. Guy Reschenthaler

This provision of the CLIMB Act has two immediate effects. First, the CLIMB Act would allow for U.S. cannabis companies currently listed in Canada to list on the Nasdaq or NYSE. Second, this provision would allow more traditional, “blue-chip” industry companies currently listed on Nasdaq or the NYSE who haven’t been able to operate within the cannabis industry as a plant-touching entity, to enter the cannabis industry as an active participant.

In announcing the CLIMB Act, Representative Reschenthaler stated that “American cannabis companies are currently restricted from receiving traditional lending and financing, making it difficult to compete with larger, global competitors. The CLIMB Act will eliminate these barriers to entry, and provide state-legal American cannabis companies, including small, minority, and veteran-owned businesses, with access to the financial tools necessary for success.”

It is important to note that the CLIMB Act, like the SAFE Banking Act, only represents one small, but important step toward cannabis reforms. Neither proposal would legalize, de-schedule or reschedule cannabis. Rather, the CLIMB Act addresses very real-world, operational issues facing the cannabis industry. With that in mind, the CLIMB Act would certainly provide much needed clarity for issues facing all cannabis companies.

Passage of the CLIMB Act is not a forgone conclusion, but rather is quite uncertain. Other pieces of cannabis-related legislation, like the SAFE Banking Act, have passed the House of Representatives multiple times without the U.S. Senate taking any action. Moreover, the CLIMB Act was introduced with only two legislative supporters.

Christopher Lacy and The TGC Group recently won a Tier 3 conditional license under New Jersey’s social equity licensing program. Their story is one of misfortune, persistence, family and the dreadful effects that cannabis prohibition and the War on Drugs has had on impoverished BIPOC communities.

Chris’s father was a sharecropper in Mississippi before he moved to Illinois and started a family. Growing up in a poor neighborhood of Chicago, Chris was surrounded by gangs and crime. He started selling drugs when he was 12 and went to prison for cannabis before he was old enough to drink. When he got out, he saw firsthand the effects that incarceration has on a person, their family and their community.

When it was first announced, Illinois’s social equity program seemed revolutionary and one that other states soon followed, setting the stage for markets all over the country to establish social equity licensing programs. However, legal hurdles, red tape and intense litigation have bogged down the system, causing severe delays. Chris and Taneeshia are still waiting to hear back about approval of their license application, years later.

Good news came recently when they were notified that they were awarded a conditional license in New Jersey. With the help of his family, business partners and The Garden State, The TGC Group is moving forward with launching their business. We caught up with Chris, to check in on his business’s progress, hear his story and see if it might inspire others to take a similar path.

Cannabis Industry Journal: Tell me a little bit about yourself and your story with cannabis

Christopher Lacy, Founder of The TGC Group

Christopher Lacy: I grew up on a dead-end block in a little town in Illinois on the far south side of Chicago called Robbins. It has a very high crime rate and a very impoverished community so as you could imagine we grew up pretty poor. I personally didn’t feel the effects of poverty until just before I turned 13. I guess that became more obvious as I started hanging out and seeing that most of my friends had more than 2 pairs of pants. I starting selling drugs when I was 12 years old. When I was about 16-17 years old, I had started trying to grow cannabis. Like any task, it takes time to develop the skills produce a good product. Cannabis definitely has it challenges when it comes to cultivating a product that could be considered good.

It’s not like there was an abundance of information out there specific to cannabis cultivation to aid in the task so besides the basic book knowledge of horticulture, you had to grind it out. It took me a couple years to really get it figured out. Once I did get it going, I started expanding. At first it was basements in the suburbs. We’d grab really nice houses and fill the basements with plants. When that wasn’t enough, we started doing warehouses. There was no real limit, outside of capital and the desire to not draw attention via odor or traffic from workers, if you could produce it, the demand was there. I did go to prison for a short stint when I was 20 years old for delivery of a controlled substance. 0.8 grams. After I got out of prison, I had a very successful illegal operation growing and selling cannabis. Life was pretty good for a few years. I wasn’t rich or anything like that but I was able to be around my family and provide the things that I was denied when I grew up. I don’t blame my parents for what I went through growing up. Because of my father’s age, I’m generation 1 out of the sharecropping era. My parents believed in one thing and that was learning. I tried to instill that into my kids as well. Being a father feels really good to me. Unfortunately, that dream was ended when I was arrested in one of our warehouses in Illinois. I did 3.5 years, locked down 21 hours a day for growing weed.

While serving my time I was able to really take a look at myself and develop a new me. I established some new core principles that I would hold close to my heart. One of them being not going back to jail for the sake of a dollar. I was not going back to prison. I had kids when I was young so I missed out on a big part of their childhoods. I had three daughters and two sons at the time that were of an age where having a stable home plays a huge role on how the child will turn out in the future compared to a typical American lifestyle. When I got out of jail, my kids came and lived with me during and after high school but some serious damage had already been inflicted. I worked a job as a truck driver and did the best that I could to support my family, but I never really gave up on cannabis in the back of my mind. My older brother used to always tell me that I didn’t learn what I knew about weed for nothing and that one day it would all make sense.

Christopher with his wife, Taneeshia

For the next few years, we just grinded it out as a family. It wasn’t the ideal situation but we made it work. And when we couldn’t make it work, we lived with it! I just was glad to be there doing Chemistry homework with the kids. That shows what happens when a father is at home with his family. We get college grads.

When the message came out that Illinois was going to do craft grow licenses, I got really excited. I figured this was my chance to do what I love and to make a living doing it. I had no idea how I was going to get to where I wanted to be but I figured if I could just put one foot in front of the other, sooner or later I would get there. I caught a break when my nephew, Edward Lacy, introduced me to someone who understood the application process. She introduced me to some of the most wonderful/helpful people in the world. People who literally wanted to help true social equity applicants like myself. With the help of these new friends, we were able to drop our first application in Illinois. After we submitted that application, that is when the first story came out about us in Cannabis Industry Journal. This story helped me get into a conversation with Cresco labs and I was able to get into a situation that really changed how I saw cannabis production. I got to work around some of the smartest people in the industry for just under a year. I can’t thank Charlie, Barrington and the rest of the guys at Cresco enough for the opportunity. From there, I knew it had to be my destiny to grow cannabis for a living. I just kept beating up the phones and emails. Something was gone give.

CIJ: When we last spoke, you were trying to get a social equity license in Illinois, can you tell me about that? How did it go?

Chris: Ultimately, after 2 years of waiting, we were denied a license in Illinois. When I first got this news. it took me about a week to get out the bed. Lol. It took my wife to pull me through. I can only imagine the pain that all the other disappointed groups are feeling, Ultimately, we all couldn’t win in Illinois so it is what it is. But definitely a big shout out to all the successful applicants that did win. You all have a torch to carry that should ignite the black and brown communities.

From the political standpoint in Illinois, it’s just not conducive for social equity applicants to succeed due to all of the legal hurdles, courts, lawsuits, etc. Not to say that the Illinois process is truly different from other states going through similar processes, New Jersey and other states went through a similar process when social equity licenses were announced. The laws that helped me qualify are what came out of the legal battles in New Jersey. The issue is the resources available for legal fees, holding property, and the time required to see these things through; this all equals dollars and that’s just something lacking in most social equity groups.

CIJ: So, what made you look at New Jersey?

Chris: After I had submitted my application in Illinois, I began looking for financial support. I knew this would be my limiting factor because access to the type of capital required to get a grow facility off the ground is quite substantial. For the most part no one returned calls but I called one financial institution in particular, VenCanna Ventures, and for some miraculous reason, they returned my call. I’m not sure what made them; but we kept an open line of communication going all while we were dealing with Illinois. I knew these guys were good because they were behind an impressive project in Ohio that actually won LEED certification. When I look back on it, it felt like a one-year interview. Then one day this past winter David McGorman, the CEO, asked me to partner up with him in New Jersey. It was exactly what we both needed. He has the expertise in finance and I bring the operations side.

Christopher with his daughter, Janeace Lacy

Once we had that team together, we put together a strategy to try and apply in New Jersey. We built the application and New Jersey actually had some very unique laws. If you had a cannabis conviction, you could qualify. Also, my oldest daughter, Janeace, whom I think my prison time hurt the most, actually lives in New Jersey with my granddaughter. So, she’s our resident in the state that helped us win the application and now a part owner, which led us to where we are now. I just couldn’t be more excited about all of this. It just feels right

We won a tier 3 conditional license and now we’re working on finding a good facility and building the operation.

CIJ: How did you set up your social equity license application for NJ?

Chris: It was a process very similar to Illinois except that the process was split into two phases. A conditional license and an annual license. Phase one was winning the conditional license. This is a more condensed application compared to what I was used to. After filling out the application, we had to submit a bunch of documents and proof of incarceration. That was for the conditional license. We still have to convert the conditional to the annual. The conditional basically tells us that we qualify and we can move forward with the rest of the business plan, find some property and spend some money on a lease. We’re still in that process for converting to annual, but we have won the conditional.

CIJ: What is your plan now that you’ve received conditional approval?

Chris: Right now, we’re working on property and securing a space for our facility. We are pretty close to nailing down a couple good locations. One of the locations that I am really excited about is in Somerset County. If we can lock down the property, submit everything to the state as far as our SOPs, security plans, cultivation plan, design, etc. we can try get approval to convert to the annual license and then we can start the build out. The good thing about the two-step process is that it really helps when it comes to spending money. Basically, if you don’t win a conditional, don’t go out spending tons of cash trying to hold onto property.

CIJ: You’ve come a long way from being put in prison for cannabis, to now being close to establishing a business in New Jersey. What made you decide to stick with the business of cannabis?

Chris: You know, I can’t really describe it very well. It was just one of those feelings, you know it felt good to me. It drew me in when I was a young kid, although, I actually didn’t try using cannabis until I was 21. That’s when I first used it and it really jelled with me. Also, I’ve always loved gardening.

Chris Lacy

My father was a sharecropper in Mississippi, when our family moved to the suburbs of Chicago the first thing he did was plant a huge garden. I grew up in the garden and around plants. He used to spend so much time in that garden and I loved being there with him. We grew everything out there year after year until he was too old to keep it up. I can’t imagine a more peaceful environment then out in the fields with the plants.

It was also therapeutic, not just the obvious therapeutic aspects of cannabis, but also how therapeutic gardening is. Working with cannabis plants can be a challenge. To try to achieve unique terpene and cannabinoid profiles has always been a lot of fun for me. I love the challenge. Pushing genetics as far as I can to really experience what different cultivars have to offer. It is just one of those things that has always stuck with me and I really enjoy it. Once it became legal, a world of opportunity opened up for me.

You know, people say if you do something you love, you’ll never have to work a day in your life. I was a truck driver after I got out of prison, and I really didn’t like it. I had to have neck surgery from the pounding my spine took. I had to work long hours, man I hated doing it. On the flip side, cannabis is something I love to do. And this is about me trying to control my own destiny, control my own life. I don’t have to struggle mentally and physically just to provide for my family. That’s what keeps me going – the drive to do what I love to do to provide for my family. I see cannabis cultivation as more of an art than I do anything else. The guy behind the growing at any facility in the country could share with people what he believes to be fire. I just love to provide an experience and there’s nothing more satisfying than a satisfied customer. Everything about this process seems to fit perfectly with my life.

CIJ: It’s a pretty inspiring story. How do you hope your story might inspire others to follow in your footsteps?