Update: Governor McKee has signed the Rhode Island Cannabis Act into law, making it the 19th state to legalize adult use cannabis.

In Rhode Island this week, lawmakers voted to approve a bill that would legalize and regulate adult use cannabis. The state’s legislature passed the bill with overwhelming majorities in both the House of Representatives and the Senate.

The House voted 55-16 and the Senate voted 32-6 to approve the Rhode Island Cannabis Act, a bill that allows adults over 21 to possess, purchase and grow cannabis. The legislation contains a provision for automatic review and expungement of past cannabis convictions. Similar to other neighboring states, the bill also allows for allocating tax revenue from cannabis sales to communities most harmed by cannabis prohibition, such as low income neighborhoods.

Rhode Island Gov. McKee

Governor Daniel McKee has expressed support for the bill previously and is expected to sign it into law. According to Jared Moffat, state campaigns manager for the Marijuana Policy Project, Rep. Scott Slater, Sen. Josh Miller and Rep. Leonela Felix are to thank for their leadership in bringing the bill to a vote. “We are grateful to Rep. Scott Slater and Sen.Josh Miller for their years of leadership on this issue. Rhode Islanders should be proud of their lawmakers for passing a legalization bill that features strong provisions to promote equity and social justice,” says Moffat. “We’re also thankful to Rep. Leonela Felix who advocated tirelessly for the inclusion of an automatic expungement provision that will clear tens of thousands of past cannabis possession convictions.”

Among other provisions, the bill establishes a 10% sales tax in addition to the state’s normal 7% sales tax and 3% local sales tax. A quarter of all retail licenses will go to social equity applicants and another quarter of all licenses will be reserved for worker-owned cooperatives. The legislation also includes a “social equity assistance fund” that will offer grant money, job training and social services to communities most impacted by cannabis prohibition.

By Abraham Finberg, Simon Menkes, Rachel Wright 1 Comment

New York is embarking on a great social undertaking. In awarding its adult-use cannabis licenses, under the plan laid out by Gov. Kathy Hochul on March 10, the state is attempting to right generations of wrongs caused by the war on cannabis. The wrongs are numerous and include mass incarceration and complex generational trauma, prevention of access to housing and employment and the forming of an illicit market – all of which have had a disproportionate impact on African-American and Latinx communities.1

In addition to generating significant revenue for the state, New York hopes to make substantial investments in the communities and people most affected by cannabis criminalization and address the collateral consequences of that criminalization, reduce the illicit market for cannabis and illegal drugs, end the racially disparate impact of existing cannabis laws and strengthen New York’s agriculture sector.2

50% of All Licenses Will Be Social Equity

To accomplish these lofty aims, the state’s goal is to award 50% of adult-use cannabis licenses to social and economic equity applicants – and these licenses will be the first issued.3,4 The state’s entire focus is on this social equity licensing program; issues regarding non-social equity licenses are not being addressed at this time.

No one knows yet how many licenses will be issued. There are currently only 38 medical licenses in the state, although everyone expects the number of adult-use licenses to be significantly higher. (These medical licenses serve around 140,000 patients with sales in 2021 of around $300 million.)

The First 100 to 200 Licenses

Chris Alexander, executive director of the state’s Office of Cannabis Management, says he expected between 100 and 200 licenses to go first to people who were convicted of a cannabis-related offense before the drug was legalized, or those who have “a parent, guardian, child, spouse, or dependent” with a cannabis conviction. Alexander also said his office would evaluate applicants on their business plans and experience in retail.5

What’s the Timeline?

In a recent Q&A interview, Tremaine Wright, chair of New York’s newly-formed Cannabis Control Board (CCB), which will be overseeing the licensing process, stated: “We are setting up a system soup-to-nuts … [final] regulations for the state’s marijuana startups will be issued by the Cannabis Control Board this winter [2022] or early spring [2023] … recreational dispensaries should be licensed to operate by summer 2023.”6

Whom Is New York Looking For?

New York has defined social equity applicants as being:

Individuals from communities disproportionately impacted by the enforcement of cannabis prohibition

Minority-owned businesses

Women-owned businesses

Minority and women-owned businesses

Distressed farmers

Service-disabled veterans.7

Extra priority will be given to an applicant who:

Is a member of a community disproportionately impacted by the enforcement of cannabis prohibition

Has an income lower than 80% of the median income of the county in which the applicant resides

Was either: (a) convicted of a cannabis-related offense prior to the effective date of the N.Y. Cannabis Law; (b) or had a parent, guardian, child, spouse or dependent; or was a dependent of an individual who was convicted of a cannabis-related offence prior to the effective date of the N.Y. Cannabis Law.8

Social Equity Licenses Come With Strings Attached

Social equity licenses cannot be transferred or sold within the first three years of issue. An exception will be made if the license is transferred or sold to another qualified social and economic equity applicant, but this must first be approved in writing by the CCB.9

Types of Licenses

While most people appear to be interested in a cannabis dispensary or lounge license, there will be nine types of licenses available: cultivator, nursery, processor, distributor, retail-dispensary, delivery, on-site consumption, adult-use cooperative and microbusiness.

“I don’t hear many people [talking about] processing and manufacturing,” says CCB chair Wright. She noted that processor licenses cover the production of edibles like candy and baked goods, which create a good opportunity to establish a brand.10

CCB Priorities

Wright also noted delivery companies would likely be capped at 25 employees in order to prevent behemoths like Uber from entering the market. “We’re trying to focus on not creating a space where monopolies can take over and kill all our small businesses,” Wright says.11

License Application Costs

The cost for an adult-use cannabis license in New York is still unknown, so the experts are looking at the cost for a medical cannabis license as the baseline, with a greater cost likely for adult-use. Each applicant was required to submit two fees with its medicinal application: a non-refundable application fee in the amount of $10,000 and a registration fee in the amount of $200,000. The $200,000 registration fee was refunded to the applicant only if the applicant was not issued a registration.12

The Marijuana Regulation and Taxation Act (MRTA) states, however, that fees may be waived for social equity applicants.13

Funding Assistance for License Applicants

Because of the requirement that each applicant be from one or more of the social equity classes, it is quite likely many of the applicants will lack the necessary funding to open a cannabis business currently.

New York Governor Kathy Hochul

On January 5, 2022, Gov. Hochul pledged to commit $200 million to support social equity applicants in building adult-use cannabis businesses. New York’s Office of Cannabis management expects that around $50 million of the fund will be raised from registered organizations licensed to operate medical cannabis businesses in NY and that $150 million will be raised from private investors.14

Wright commented, however, that those loans aren’t guaranteed to be available for the first round of licensing because the money to fund them will largely come from tax revenue generated by the industry. “[The Office of Cannabis Management] is not going to be able to right all the wrongs of the financial services industry,” she added.15

This lack of capital will offer opportunities to those who might want to invest with a social equity license applicant.

Requirements for Those Who Invest With Social Equity Applicants

Any person or entity investing with a social equity applicant must keep in mind the State’s following requirements:

Any entity applying for a New York cannabis license will need to be owned at least 51% by a social equity class applicant.

That ownership must be “real, substantial, and continuing.”

The social equity applicant must have and exercise the authority to control independently the day-to-day business decisions of the enterprise.

The individual or entity seeking the license must be authorized to do business in the state and be independently owned and operated.

The individual or entity must be a small business.16

Business Experience & Labor Union Representation Needed

The state is also looking for applicants with previous successful business experience and competency, and preference will be given to those who can demonstrate such experience.17

Additionally, the state would like to see that the applicant “has entered into [an] … agreement with a bona-fide labor organization that is actively engaged in representing or attempting to represent the applicant’s employees, and the maintenance of such [an] agreement shall be an ongoing material condition of licensure.18

New York’s Careful Approach

New York has moved slowly and thoughtfully in getting into the recreational cannabis market. Its leaders have studied the experiences of other states, noting complications and pitfalls that have arisen in such states as California, where small cannabis operators have been squeezed out and a large illicit market has grown to dwarf the tax-paying legal sector.

By opening up New York’s initial adult-use licenses to small, social equity applicants and requiring they have solid business experience, New York is hoping to give awardees a foothold in the cannabis market, enabling them to flourish and build strong roots before the onslaught of sophisticated, multi-state cannabis operators enter the fray.

Additional Keys to a Successful Application

New York City Image: Rodrigo Paredes, Flickr

Beyond fulfilling the ingredients of the social equity applicant “recipe” outlined above, the key to a successful application will come down to the perception it gives the Cannabis Control Board of the applicant’s commitment to the state’s mission. In other words, how committed is the applicant to using his or her license and business to attempt to right some of the social wrongs perpetrated by the state and federal war on cannabis?

In addition to having an owner-applicant from a social equity class, the MRTA gives other clues of steps applicants can take (and discuss in their application) which could put them ahead of the competition in obtaining licensure.

The MRTA suggests the applicant demonstrate that they will “contribute to communities and people disproportionately harmed by enforcement of cannabis laws … and report these contributions to the board.”19

The MRTA asks each applicant to submit documentation of the racial, ethnic and gender diversity of the applicant’s employees and owners. In addition, the MRTA suggests each applicant consult with the CCB’s Chief Equity Officer and Executive Director “to create a social responsibility framework agreement that fosters racial, ethnic, and gender diversity in their workplace.”20

New York is serious about its mission to use the legalization of cannabis to right some of the social wrongs of the past. An applicant’s dedication to this mission, as evidenced by a well-crafted application that emphasizes these values, may be the deciding factor on whether that applicant is rewarded with one of the state’s “Golden Tickets”. With a population of 20.2 million citizens, New York will be the second largest adult use cannabis marketplace behind California. Initial access to such a valuable and important market is worth the commitment of resources to creating not only a well-crafted application, but a well-crafted management team and business as well.

References

New York Consolidated Laws, N.Y. Cannabis Law § 2, added by New York Laws 2021, ch. 92, Sec. 2 (eff. 3/31/2021) [hereinafter, N.Y. Cannabis Law].

As state legalization measures begin to legitimatize the US cannabis industry, stakeholders, both those currently in the industry and those who plan to join in the not-too-distant future, grapple with the best ways to right the wrongs from the decades-old War on Drugs. While some stakeholders support residency requirements and setting aside a percentage of a state’s cannabis licenses for social equity and economic empowerment applicants, others contend that these solutions are discriminatory. Reuters reports that lawsuits against social equity programs have been filed in Michigan, Illinois, Missouri and Maine, and some have received decisions that rule against existing social equity programs. While there is disagreement on the best way to create an equitable cannabis industry, few dispute that we’re dealing with an oppressive legacy against low-income individuals and people of color and the cannabis industry is in a unique position to shape a socially responsible industry that focuses not just on profits, but also on the greater good.

Challenges for Social Equity Applicants and Licensees

Currently, Black Americans make up 13% of the US national population, but own less than two percent of cannabis businesses owners, according to Leafly’s Jobs Report 2021. Why? There are five primary factors.

In most states, cannabis licenses are expensive and difficult to get. The application process requires a team of experienced individuals to work on everything from finding and negotiating real estate contracts; to vetting and hiring architects, safety, and security consultants; to working with community stakeholders to gain local approval.

After the pieces are in place, applicants have to write it all down, which is a challenge in itself. It is not uncommon for one state cannabis application to be over one hundred pages.

Since cannabis is still federally illegal and listed as a Schedule 1 drug, it’s nearly impossible to get a business loan to fund the application process or, if an individual is lucky enough to get a provisional license, to renovate or build out cannabis cultivation, processing and/or retail facilities.

Because of the low-income status of many social equity applicants, few have access to accredited investors or low interest loans.

Finally, if an individual or organization makes it through the application process and receives both a license and funding to operate, they face ongoing operational challenges including ever-changing laws, rules and regulations. Maintaining compliance is a process in and of itself.

If cannabis industry stakeholders don’t make honest efforts to provide real solutions to these challenges in the near future, inequalities will proliferate.

Current State of Social Equity in the US Cannabis Industry

To help mend the harms of the War on Drugs and reduce the institutional challenges faced by marginalized individuals, some states have instituted social equity programs that prioritize cannabis business licenses to those previously incarcerated on cannabis-related convictions and/or those who live in zip codes with high incarceration rates for drug crimes. Some states broaden the social equity lens and include women- and veteran-owned businesses in social equity programs.

The goal of social equity laws is to ensure that people from communities disproportionately harmed by marijuana prohibition and discriminatory law enforcement are included in the new legal marijuana industry. Policymakers are working to address criticisms that outsiders are setting up legal cannabis businesses and profiting by doing the same things their less fortunate neighbors were arrested and given jail time for just a few years ago.

By prioritizing social equity applicants, our industry is starting to bridge the access gap and improve the odds that previously marginalized individuals will make it into the C-suite and other influential positions. But is it enough? Many argue that social equity programs won’t make a real difference until more programs include low-interest loans and/or provide access to capital sources and ongoing support after licensure.

Although social equity programs vary, many require applicants to live in a zip code with a high incarceration rate for drug crimes or have a state residency requirement, meaning that social equity applicants must have lived in the state for an established number of years before they can qualify for social equity status. In some states, municipalities are tasked with creating these programs as is the case in Los Angeles and Oakland, California.

While some states offer social equity applicants priority consideration for their licensing applications, others offer reduced application and licensing fees, technical assistance, entry into an incubator program specifically designed for social equity applicants and/or apprenticeship opportunities.

Although social equity programs focus on developing business leaders with marginalized racial and socioeconomic backgrounds, other components of these programs often include criminal justice reform, such as revising resentencing guidelines and expungement requirements for those with cannabis-related convictions. The MORE Act, for example, not only calls for federal legalization, but also for reassessing the legal status of cannabis-related convictions, arrests, and prison sentences.

US States with Cannabis Social Equity Programs

When Colorado and Washington voted in favor of adult-use cannabis legalization nearly a decade ago, lawmakers were tasked with drafting regulations for what a legal marketplace would look like in their respective states. Although legalization efforts focused on the inequities of prohibition, the War on Drugs, and the legal cannabis industry, social justice initiatives were not initially included.

Out of the 19 states with adult-use cannabis, 13 have developed social equity programs to help marginalized people become cannabis leaders in their markets. States that incorporated social equity programs into initial adult-use cannabis legislation include Massachusetts, California, New Jersey, New York, New Mexico, Michigan, Vermont, Illinois, Connecticut, Arizona and Virginia. Although Colorado and Washington’s laws initially did not include social equity programs, both states are now in the process of implementing them.

It’s important to note that not all US states with legal cannabis programs take the social equity approach. States with legal adult-use programs but without social equity programs include Montana, South Dakota, Maine, Nevada, Oregon and Alaska.

After Social Equity Licensure

For those social equity applicants who receive operational licensure, there is the ongoing issue of compliance. As if there were not enough pressure on social equity applicants and license holders, maintaining state-compliant businesses and developing internal policies and procedures that drive brand awareness and loyalty can be a challenge. The hard reality is that admission into a social equity program and even obtaining licensure does not ensure a business leader’s success. Besides increased access to capital, expanding social equity programs to include post-licensure support, at least for the first year or two, would improve the odds of long-term success.

All in all, social equity programs in the US cannabis industry have begun to make a difference and right some of the wrongs of the War on Drugs, but there is still work to be done. To build an industry that improves lives not only with cannabis products but also with financial opportunity, we must continue to prioritize and expand current social equity programs and fight for new social equity programs in all legal cannabis states.

The cannabis industry in the United States represents about a $50 billion asset class making it one of the largest new asset classes in the country. Commercial real estate lending is a key enabler for companies seeking to expand and scale. Pelorus Equity Group is one of the largest commercial lenders in cannabis with over $170 million deployed since its first cannabis transaction in 2016.

Since 1991, Pelorus principals have participated in more than $1 billion of real estate investment transactions using both debt and equity solutions. Pelorus offers a range of transactional solutions addressing the diverse needs of cannabis related business operators. While most cannabis private equity lenders focus on real estate acquisition and refinancing, Pelorus has leveraged its experience in more than 5,000 transactions of varying size and complexity to offer value-add loans, a rarity in the industry.

We spoke with Rob Sechrist, president of Pelorus Equity Group and manager of the Pelorus Fund. Rob joined Pelorus in 2010 after several years in the California real estate market. In 2018, Pelorus launched the Pelorus Fund where Rob is currently the manager. The Fund converted to an REIT in 2020.

Aaron Green: How did you get involved in the cannabis industry?

Rob Sechrist: Pelorus is a value-add bridge lender. We’ve been lending for a long time, originally in the non-cannabis space. We’ve done 5000 transactions for over a billion dollars – more than a lot of banks.

In 2014, our local congressman Dana Rohrabacher passed the Rohrabacher-Blumenauer Amendment that defunded the Department of Justice from prosecuting any cannabis related business in a medically licensed state. We were a supporter of that legislation and once that passed, we took a serious look at utilizing our expertise in being a value-add lender and applying it to the largest asset class of real estate that is newly coming about today. That cannabis related asset class is about $50 billion.

Rob Sechrist, president of Pelorus Equity Group and manager of the Pelorus Fund

We decided that we had the expertise to move into this space and to build these facilities out for our borrowers so that the cannabis use tenants would have a fully stabilized facility and make it operate. After the amendment passed in 2014, by 2016 we had originated our first transaction. Since that time, we’ve originated 51 transactions in the cannabis space for over $177 million so far. It wasn’t that big of a pivot when you’re just providing the value-add loan.

“Value-add” in the loan business means that a portion of the loan amount, let’s just say is a million dollars, maybe 250,000 of that, is a pre-approved budget to go back into the property. In cannabis property those are typically tenant improvements and/or equipment to fully stabilize that tenant. So, we’re the first fully dedicated lender in the nation exclusively to cannabis and we’ve done more transactions than anybody else in the nation.

Green: What are some challenges of cannabis lending compared to traditional lending?

Sechrist: The number one challenge in cannabis is that you must disclose to your investors that you’re originating the loans to cannabis use tenants. Many people have concerns that lending indirectly might be federally illegal. If you did not disclose that to your investors when you form that capital stack to fund these transactions, you’re going to run into issues. So, you would need to create a vehicle where you disclose to your investors that you’re intending to lend into cannabis and it’s still federally illegal. Doing one-off stand-alone transactions deal by deal is not sustainable if you’re going to be a large lender.

There are other challenges. Because cannabis is still federally illegal, it gives insurers and other third parties the ability to deny a claim, or certain lender protections. Some examples include errors and omissions insurance, title insurance, property insurance, etc. and all of them say in those policies that if you’re doing something federally illegal, then the policy is null and void. So, you must think your way through very carefully all the things that could potentially be an issue. You also have to disclose to those third parties and find a way to get them to acknowledge it to make sure you have the coverage if you ever have to make a claim. That’s a very difficult process.

Green: How has the investor profile in cannabis lending changed over time?

Sechrist: Our fund was structured to allow for institutional capital from the inception. We were able to do that because we are completely non-plant touching. Our fund only lends to the owners of commercial real estate. We do not lend to any cannabis licensed operator directly whatsoever. Our borrowers – the owners of the properties – would then have a lease agreement with the cannabis use tenant. Even if it’s an owner-operator, those are separate entities. That’s how we’ve distinguished ourselves.

Pelorus Equity Group, Inc. Logo

Regarding the investor profile, the first $100 million plus we raised was primarily from retail investors who were individuals writing checks up to a million dollars. Once we had three years of audited track record and our fund was $100 million, we then pivoted over to family offices and institutional investors and pension funds. We’re now working primarily with those types of investors.

The reason that we started with retail investors is that it’s very easy for me to explain our model to a single decision maker and answer their questions. Once I move into family offices or institutional investors, the opportunity goes to a credit committee where I’m relying on some other party to educate the investor about our investment. It’s enormously challenging at that point if it’s not me doing the talking. I know the answers, but I’m having to rely on somebody else to answer questions. We’ve tried to educate everybody we speak with and craft our documentation in such a way that even when it’s not myself answering the questions directly, people can understand how we thread the needle through some of the legal hurdles.

Green: How do you prioritize deal flow, and what are the qualities of a successful loan applicant?

Sechrist: We typically maintain a pipeline of around $150 million in transactions at any one time.

Applicants must have real estate. We’re not doing business loans or operator loans directly to tenants or business operations. So, that’s the starting point. We want a real estate piece of collateral where we feel more than comfortable with the loan-to-value and ratios and the loan to cost and other figures, that we feel that this transaction is going to be a success for our borrower and ultimately the tenant.

Next, we will only work with very experienced operators who have a proven track record where this is not their first transaction. Ideally, we are working someone who is looking to expand their operations and who is ready to either move from being a tenant of their previous facility and buying their next facility.

The next aspect that we’re looking for is the strength of the borrower’s guarantor. They must be able to qualify to support that transaction. Many of our transactions are millions or 10s of millions of dollars. You must have a sponsor that can support that size of a transaction.

Green: What sort of value-adds should a cannabis property owner look for in their lender?

Sechrist: Most people that are looking for loans are only familiar with getting loans for themselves on their owner-occupied house. Most loans have points, they have a rate and a term, loan-to-value and things like that.

“We wanted to make sure that when we underwrite the transaction, that every single piece of capital is necessary to get that facility all the way to where that tenant can start generating their first crops and make their lease payments.”When you move into construction loans or value-add lending, there are other elements that are more important than the pricing of the loan. The number one thing is to get that property fully stabilized and built as quickly as possible. Cannabis tenants are generating 10 to 15 times more revenue per month than non-cannabis tenants.

If you go to a bank and borrow money it may be a third of what it costs to borrow from us, but they process draws maybe once a month. So, if you’re having to advance the money for improvements of the property, and then the bank reimburses once a month, at a certain point you’re not going to be able to advance any more money until you get reimbursed. The project comes to a stop. So, in your mind, you might have saved an enormous amount on the pricing of the rate, but it’s costing you dearly in revenue and opportunity costs. We typically process 50 to 100 draws post-closing on transactions, and we get that facility built and the money reimbursed to all the contractors on a multiple-times-a-week basis. It’s happening in real flow all the time.

A typical problem for a tenant is that the tenant improvements are orders of magnitude higher than a non-cannabis tenant – anywhere from $150 to $250 per square foot. In addition, the equipment is often enormously expensive as well. It’s tough to put money into a buildout for a building that you may not own. Our vision at Pelorus was, let’s not force these tenants – the cannabis operators – to raise equity at the worst possible time when they’re not generating revenue through the facility. Let’s shift that capital balance for those tenant improvements and equipment from the from the tenant to the owner of the building, which is where it’s secured and adds value to that building anyway. Our vision was to shift that money from the balance sheet of the tenant over to the owner of the real estate so the tenant didn’t have to sell equity to come up with that money. Then the tenant is paying for the improvements in the lease rate and the borrower is paying for improvements in the note rate. And so we’ve shifted tenant improvements from being an equity component to now it’s just priced in the debt. This way you know what the terms are and you know what your total exposure is there.

We wanted to make sure that when we underwrite the transaction, that every single piece of capital is necessary to get that facility all the way to where that tenant can start generating their first crops and make their lease payments. Most of our peers in the space don’t look at it that way. They just do the acquisition or the refinance. They don’t do anything for the tenant improvements. They don’t do anything for the equipment. The tenant is left out there to either raise that equity or the borrower – the owner of the real estate – is having to come up with that additional capital on their own. We think you’re set up for failure in that circumstance. So, we blend all that into one capital stack. It’s important that the tenants can get all the way up to being able to cash flow and support that facility and be fully stabilized so they can refinance into a lower cost bank or credit union transaction.

Green: What federal policies and trends are you monitoring?

Sechrist: First, I think that it’s important to remind people that the Rohrabacher-Blumenauer Amendment has protected everybody from any prosecution. So, there’s no jeopardy out there that exists. The second thing I like to tell people is there are 695 banks on FinCEN’s website of cannabis Tier 1 depositors, and of those, we’re tracking numerous FDIC insured state banks and credit unions that are lending directly. We’ve been paid off by banks.

So, there’s this massive misconception that there’s no banking at all and that everything is happening by cash. The only cash buildup that happens is at the retail dispensary level because credit cards aren’t allowed for retail sales at the dispensaries. Out of the 2,000 transactions that we’ve either processed or reviewed, not one has ever not had banking set up. So, it is a big misnomer that there’s no depositor relations for Tier 1 banking, which is plant touching.

Tier 2/3 depositors are ancillary, which is what we are at Pelorus. There are 100 private lenders and dozens and dozens of state and federal credit unions or state banks and credit unions, not federal, that are FDIC insured and lending. Those banks are difficult to get loans from because they only want to do urban environments. They want to do fully stabilized companies and they want to use alternative views and the facility has to have seasoning for cash flow. It’s difficult to qualify for them. So, banking and lending exists out there, and most people are not aware of that.

Green: What are you most interested in learning about? This could be either in cannabis or in your personal life.

Sechrist: My two passions are snowboarding and racetrack driving. I just came back from the Mille Miglia race in Italy, and I do a lot of driving on the racetracks. I’m always looking to learn from those experiences.

In the cannabis sector, social equity programs are happening across the nation and cannabis licenses are being issued to operators. We would like to help participate in some system of educating these applicants that win the awards. Lending to an owner of a property who just won a license but has no experience is going to be problematic. Somebody needs to be thinking that out and making sure that these people that win have enough experience and education to set them up for success. Cannabis is one of the most complicated businesses ever, and they’ve got this license as their ticket, but they need to know how to make sure they’re going to be successful.

By Gregory S. Kaufman, Jessica R. Rodgers No Comments

With the signing of the Cannabis Control Act (the Act) on April 21, 2021, Virginia became the first southern state to legalize adult use cannabis and just the fourth state to do so through the legislature. Legalizing adult use cannabis through the legislature, as opposed to through the ballot box, is not the typical route states have followed up to now. Eleven of the sixteen states and the District of Columbia have legalized adult use cannabis through the use of ballot measures. Virginia joins Vermont, Illinois, New York and New Mexico (which legalized after Virginia) as one of the few states that have gone the legislative route. Under Governor Northam’s administration, the path to legalization was swift, taking less than four months from introduction to passage.

Governor Northam added amendments to the already passed Senate Bill 1406 and the General Assembly voted to approve those amendments, with the Lieutenant Governor breaking the tie in the Senate’s vote. Upon signing, Governor Northam called the law a step towards “building a more equitable and just Virginia and reforming our criminal justice system to make it more fair.” This message and the opportunities to promote social equity through a legal cannabis industry have been consistent points of advocacy made by supporters as the bill advanced to becoming law.

Prior to the Governor’s amendments, the Act under consideration set July 1, 2024 as the date on which both legal possession and adult use sales would begin. The Governor decided to accelerate the date for legal possession to July 1 of this year, a decision believed to have been influenced by data showing that Black Virginians were more than three times as likely to be cited for possession, even after simple possession was decriminalized in the state a year prior. The regulated adult use market is still set to begin making sales on July 1, 2024; however, it remains possible that this date could be advanced through the legislature in the meantime. Nevertheless, Virginia is on track to becoming the first southern state with an operating regulated commercial cannabis market.

Creating an Administrative Structure for the Adult Use Program

Virginia became the first state in the South to legalize adult use cannabis

This sweeping fifty-page law creates the Cannabis Control Authority to regulate the cultivation, manufacture, wholesale and retail sale of cannabis and cannabis product. The Act further lays the groundwork for licensing market participants and regulating appropriate use of cannabis; defining local control; testing, labeling, packaging and advertising of cannabis and cannabis products; and taxation. The Act also contains changes to the criminal laws of the Commonwealth. Companion to the Act are new laws addressing the testing, labeling and packaging of smokable hemp products and manufacturing of edible cannabis products. Additionally, the Cannabis Equity Reinvestment Board was created to address the impact of economic divestment, violence and criminal justice responses to community and individual needs through scholarships and grants.

While persons 21 years or older may possess up to one ounce of cannabis and cultivate up to four plants for personal use per household beginning on July 1, 2021, there are a host of regulations to be written in order to regulate the adult use market. These regulations will be the devil in the details of how the regulated market will work. Regardless, the Cannabis Control Act does establish the framework for adult use cannabis that is unique to Virginia and designed to promote and encourage participation from people and communities disproportionately impacted by cannabis prohibition and enforcement.

The Cannabis Control Authority (CCA) will consist of a Board of Directors, the Cannabis Public Health Advisory Council, the Chief Executive Officer and employees. The Board will have five members appointed by the Governor and confirmed by the legislature, each with the possibility of serving two consecutive five-year terms. The Board is tasked with creating and enforcing regulations under which retail cannabis and cannabis products are possessed, sold, transported, distributed, and delivered. It is expected that the Board will begin discussing regulations next year and that applications for licenses for cannabis cultivation facilities, manufacturing facilities, cannabis testing facilities, wholesalers, and retail stores will begin to be accepted in 2023. Importantly, a Business Equity and Diversity Support Team, led by a Social Equity Liaison, and the Equity Reinvestment Board, led by the Director of Diversity, Equity and Inclusion, are to contribute to a plan to promote and encourage participation in the industry by people from disproportionately impacted communities.

Regulating Participation in the Market

The Act empowers the Board to establish a robust and diverse marketplace with many entry opportunities for market participants. Up to 450 cultivation licenses, 60 manufacturing licenses for the production of retail cannabis products, 25 wholesaler licenses and 400 licenses for retail stores can be granted. These numbers do not include the four permits granted to pharmaceutical processors (entities that cultivate and dispense medical cannabis) under the Commonwealth’s medical program.

Virginia Governor Ralph Northam Image: Craig, Flickr

In addition to the sheer number of licenses that can be granted, the Act devises a unique approach to addressing concerns of a concentration of licenses in too few hands and a market dominated by large multi-state operators. At the same time, it sets up a mechanism to capitalize two cannabis equity funds intended to benefit persons, families and communities historically and disproportionately targeted and affected by drug enforcement through grants, scholarships and loans. Over-concentration and market dominance concerns are addressed by limiting a person to holding an equity interest in no more than one cultivation, manufacturing, wholesaler, retail or testing facility license. This eliminates the ability of companies to be vertically integrated from cultivation through retail sales operations. However, there are two exceptions to the impediment to vertical integration. First, the Board is authorized to develop regulations that permit small businesses to be vertically integrated and ensure that all licensees have an equal and meaningful opportunity to participate in the market. These regulations will be closely scrutinized by those looking to enter Virginia’s regulated market once they are proposed. Qualifying small businesses could benefit substantially from the economic advantages commensurate with being vertically integrated, assuming they have the access to the capital needed to achieve integration and operate successfully. The second exception allows permitted pharmaceutical processors and registered industrial hemp processors to hold multiple licenses if they pay $1 million to the Board (to be allocated to job training, the equity loan fund or equity reinvestment fund) and submit a diversity, equity and inclusion plan for approval and implementation. Consequently, Virginia is attempting to fund, in part, its ambitious social equity programs by monetizing the opportunity for these processors to participate vertically in the adult use market.

Those devilish details of how this market will function, and how onerous compliance obligations will be, will emanate from those yet to be proposed regulations covering many areas and subject matters including:

Outdoor cultivation by cultivation facilities;

Security requirements;

Sanitary standards;

A testing program;

An application process;

Packaging and labeling requirements;

Maximum THC level for retail products (not to exceed 5 mg per serving or 50 mg per package for edible products);

Record retention requirements;

Criteria for evaluating social equity license applications based on certain ownership standards;

Licensing preferences for qualified social equity applicants;

Low interest loan program standards;

Personal cultivation guidelines; and

Outdoor advertising restrictions.

Needless to say, the CCA Board has a lot work ahead in order to issue reasonable regulations that will carry out the dictates in the Act and encourage the development of a well-functioning marketplace delivering meaningful social equity opportunities.

Much work needs to be done before July 1, 2024 to prepare for its debutThe application process for the five categories of licenses will be developed by the Board, along with application fee and annual license fee amounts. It is not clear how substantial these fees will be and what effect they will have on the ability of less-well-capitalized companies and individuals to compete in the market. The Act dictates that licenses are deemed nontransferable from person to person or location to location. However, it is not entirely clear that changes in ownership will be prohibited. The Act contemplates that changes in ownership will be permitted, at least as to retail store licensees, through a reapplication process. Perhaps the forthcoming regulations will add clarity to the transferability of licenses and address the use of management services agreements as a potential workaround to the limitations in license ownership.

Certain requirements particular to certain license-types are worthy of highlighting. For example, there are two classes of cultivation licenses. Class A cultivation licenses authorize cultivation of a certain number of plants within a certain number of square feet to be determined by the Board. Interestingly, Class B licenses are for cultivation of low total THC (no more than 1%) cannabis. Several requirements specific to retail stores are noteworthy. Stores cannot exceed 1,500 square feet, or make sales through drive-through windows, internet-based sales platforms or delivery services. Prohibitive local ordinances are not allowed; however, localities can petition for a referendum on the question of whether retail stores should be prohibited in their locality. Retail stores are allowed to sell immature plants and seek to support the home growers, an allowance that is fairly unique among the existing legal adult-use states.

Taxing Cannabis Sales

Given the perception that regulated cannabis markets add to state coffers, it is little surprise that Virginia’s retail market will be subject to significant taxes. The taxing system is straightforward and not complicated by a taxing regime related to product weight or THC content, for example. There is a 21% tax on retail sales by stores, in addition to the current sales tax rates. In addition, localities may, by ordinance, impose a 3% tax on retail sales. These taxes could result in a retail tax of approximately 30%.

Changes to Criminal Laws

Changes to the criminality of cannabis will have long lasting effects for many Virginians. These changes include:

Fines of no more than $25 and participation in substance abuse or education programs for illegal purchases by juveniles or persons 18 years or older;

Prohibition of warrantless searches based solely on the odor of cannabis;

Automatic expungement of records for certain former cannabis offenses;

Prohibition of “gifting” cannabis in exchange for nominal purchases of some other product;

Prohibition of consuming cannabis or cannabis products in public; and

Prohibition of consumption by drivers or passengers in a motor vehicle being driven, with consumption being presumed if cannabis in the passenger compartment is not in the original sealed manufacturer’s container.

These changes, and others, represent a balancing of public safety with lessons learned from the effects of the war on drugs.

Potpourri

The Act contains myriad other noteworthy provisions. For example, the Board must develop, implement and maintain a seed-to-sale tracking system for the industry. Plants being grown at home must be tagged with the grower’s name and driver’s license or state ID number. Licenses may be stripped from businesses that do not remain neutral while workers attempt to unionize. However, this provision will not become effective unless approved again by the legislature next year. Banks and credit unions are protected under state law for providing financial services to licensed businesses or for investing any income derived from the providing of such services. This provision is intended to address the lack of access to banking for cannabis businesses due to the federal illegality of cannabis by removing any perceived state law barriers for banks and credit unions to do business with licensed cannabis companies.

The adult use cannabis industry is coming to Virginia. Much work needs to be done before July 1, 2024 to prepare for its debut. However, the criminal justice reforms and commitment to repairing harms related to past prohibition of cannabis are soon to be a present-day reality. Virginia is the first Southern state to take the path towards legal adult use cannabis. It is unlikely to be the last.

The bill establishes the Office of Cannabis Management, which will launch and manage the regulatory system for the commercial cannabis market in New York.

According to Steve Schain, senior attorney at Hoban Law Group, the Office of Cannabis Management will have a five-member board that will oversee not just the adult use cannabis market, but also medical cannabis as well as the state’s hemp market. For the medical market, the new legislation provides for more patient caregivers, home cultivation and an expanded list of qualifying conditions.

New York Governor Andrew Cuomo Image: Chris Rank, Flickr

Troy Smit, deputy director of the New York NORML chapter, says the bill might not be perfect, but it’s a massive win for the cannabis community. “It’s taken a great amount of work and perseverance by activists, patients, and consumers, to go from being the cannabis arrest capital of the world, to lead the world with a legalized market dedicated to equity, diversity, and inclusion,” says Smith. “This might not be the perfect piece of legislation, but today, cannabis consumers can hold their heads high and smell the flowers.”

The MRTA sets up a two-tier licensing structure that separates growing and processing licenses from dispensary licenses. The bill includes a social equity aspect that requires 50% of the licenses to be awarded to, “minority or women-owned business enterprise, service-disabled veterans or distressed farmers,” says Schain.

New York City Image: Rodrigo Paredes, Flickr

Melissa Moore, New York State director of the Drug Policy Alliance, says she’s proud of the social equity plan the bill puts in place. “Let’s be clear — the Marijuana Regulation and Taxation Act is an outright victory for the communities hit hardest by the failed war on drugs,” says Moore. “By placing community reinvestment, social equity, and justice front and center, this law is the new gold standard for reform efforts nationwide. Today we celebrate, tomorrow we work hard to make sure this law is implemented fairly and justly for all New Yorkers.”

Schain says the new tax structure in the bill shifts to the retail level, with a 9% excise tax and 4%-of-the-retail-price local excise tax (split 25%/75% between the respective counties and municipalities). Revenue from cannabis taxes will enter a fund where 40% will go to education, 40% to community grants reinvestment fund and 20% to drug treatment and public education fund.

It appears that businesses already established in New York’s medical market get a head start on the new adult use market, while other businesses enter the license application process, according to Schain. “Although the existing Medical Marijuana licensees should be able to immediately to sell Adult-Use Cannabis, it will take up to two years for the New York’s Adult Use Program to launch and open sales to the public,” says Schain.

The cannabis industry saw close to $15.5B in deals across VC, private equity, M&A and IPOs in 2020 according to PitchBook data. Early and growth stage capital has been a key enabler in deal activity as companies seek to innovate and scale, taking advantage of trends towards national legalization and consolidation. Entourage Effect Capital is one of the largest VC firms in cannabis with over $150MM deployed since its inception in 2014. Some of their notable investments include GTI, CANN, Harborside (CNQ: HBOR), Acreage Holdings, Ebbu, TerrAscend and Sunderstorm.

We spoke with Matt Hawkins, co-founder and managing partner at Entourage Effect Capital. Matt started Entourage in 2014 after exiting his previous company. He has 20+ years of private equity experience and serves on the Boards of numerous cannabis companies. Matt’s thought leadership has been on Fox Business in the past and he has also recently featured on CNBC, Bloomberg, Yahoo! Finance, Cheddar and more.

Aaron Green: How did you get involved in the cannabis industry?

Matt Hawkins: We’ve been making investments in the cannabis industry since 2014. We’ve made 65 investments to date. We have a full team of investment professionals, and we invest up and down the value chain of the industry.

I had been in private equity for 25 years and I kind of just fell into the industry after I’d had an exit. I started lending to warehouse owners in Denver that were looking to refinance their mortgages out of commercial debt into private debt, which would then give them the ability to lease their facilities to growers. I realized there would be a significant opportunity to place capital in the private equity side of the cannabis business. So, I just started raising money for that project and I haven’t looked back. It’s been a great run and we’ve built a fantastic portfolio. We look forward to continuing to deploy capital up to and through legalization.

Green: Do you consider Entourage Effect Capital a VC fund or private equity firm? How do you talk about yourself?

Hawkins: In the early stages of the industry, we were more purely venture capital because there was hardly any revenue. We’re probably still considered a venture capital firm, by definition, just because of the risk factors. As the industry has matured, the investments we make are going to be larger. The reality is that the checks we write now will go to companies that have a track record of not only 12 months of revenue, but EBITDA as well. We can calculate a multiple on those, and that makes it more like lower/middle-market private equity investing.

Green: What’s your investment mandate?

Matt Hawkins, Co-Founder and Managing Partner at Entourage Effect Capital

Hawkins: From here forward our mandate is to build scale in as many verticals as we can ahead of legalization. In the early days, we were focused on giving high net worth individuals and family offices access to the industry using a very diversified approach, meaning we invested up and down the value chain. We’ll continue to do that, but now we’re going to be really laser focused on combining companies and building scale within companies to where they’re going to be more attractive for exit partners upon legalization.

Green: Are there any particular segments of the industry that you focus on whether it’s cultivation, extraction or MSOs?

Hawkins: We tend to focus on everything above cultivation. We feel like cultivation by itself is a commodity, but when vertically integrated, for example with a single-state operator or multi-state operator, that makes it intrinsically more valuable. When you look at the value chain, right after cultivation is where we start to get involved.

Green: Are you also doing investments in tech and e-commerce?

Hawkins: We’ve made some investments in supply chain, management software, ERP solutions, things like that. We’re not really focused on e-commerce with the exception of the only CBD company we are invested in.

Green: How does Entourage’s investment philosophy differ from other VC and private equity firms in cannabis?

Hawkins: We really don’t pay attention to other people’s philosophies. We have co-invested with others in the past and will continue to do so. There’s not a lot of us in the industry, so it’s good that we all work together. Until legalization occurs, or institutional capital comes into play, we’re really the only game in town. So, it behooves us all to have good working relationships.

Green: Across the states, there’s a variety of markets in various stages of development. Do you tend to prefer investing in more sophisticated markets? Say California or Colorado where they’ve been legalized for longer, or are you looking more at new growth opportunities like New York and New Jersey?

Hawkins: Historically, we’ve focused on the most populous states. California is obviously where we’ve placed a lot of bets going forward. We’ll continue to build out our portfolio in California, but we will also exploit the other large population states like New Jersey, New York, Arizona, Massachusetts, Michigan, Ohio and Illinois. All of those are big targets for us.

Green: Do you think legalization will happen this Congress?

Hawkins: My personal opinion is that it will not happen this year. It could be the latter part of next year or the year after. I think there’s just too much wood to chop. I was encouraged to see the SAFE Banking Act reappear. I think that will hopefully encourage institutional capital to take another look at the game, especially with the NASDAQ and the New York Stock Exchange open up. So that’s a positive.

I think with the election of President Biden and with the Senate runoffs in Georgia going Democrat, the timeline to legalization has sped up, but I don’t think it’s an overnight situation. I certainly don’t think it’ll be easy to start crossing state lines immediately, either.

Green: Can you explain more about your thoughts on interstate commerce?

Hawkins: I think it’s pretty simple. The states don’t want to give up all the tax revenue that they get from their cultivation companies that are in the state. For example, if you allow Mexico and Colombia to start importing product, we can’t compete with that cost structure. States that are neighbors to California, but need to grow indoors which is more expensive, are not going to want to lose their tax revenues either. So, I just think there’s going to be a lot of butting heads at the state level.

The federal government is going to have to outline what the tax implications will be, because at the end of the day the industry is currently taxed as high as it ever will be or should be. Anything North of current tax levels will prohibit businesses from thriving further, effectively meaning not being able to tamp down the illicit market. One of the biggest goals of legalization in my opinion should be reducing the tax burden on the companies and thereby allowing them to be able to compete more directly with the illicit market, which obviously has all the benefits of reduced crime, etc.

Green: Do you foresee 280E changes coming in the future?

Hawkins: For sure. If the federal illegality veil is removed – which means there’ll be some type of rescheduling – cannabis would be removed from the 280E category. I think 280E by definition is about just illegal drugs and manufacturing and selling of that. As long as cannabis isn’t part of that, then it won’t be subject to it.

Green: What have been some of the winners in your portfolio in terms of successful exits?

Hawkins: When the CSC started allowing companies in Canada to own U.S. assets, the whole landscape changed. We were fortunate to be early investors in Acreage and companies that sold to Curaleaf and GTI before they were public. We are big investors in TerrAscend. We were early investors in Ebbu which sold to Canopy Growth. Those were huge wins for us in Fund I. We also have some interesting plays in Fund II that are on the precipice of having similar-type exits.

You read about the big ones, but at the end of the day, the ones that kind of fall under the radar – the private deals – actually have even greater multiples than what we see on some of the public M&A activity.

Green: Governor Cuomo has been hinting recently at being “very close” on a deal for opening up the cannabis market in New York. What do you think are the biggest opportunities in New York right now?

Hawkins: If it can get done, that’s great. I’m just concerned that distractions in the state house right now in New York may get in the way of progress there. But if it doesn’t, and it is able to come to fruition, then there isn’t a sector that doesn’t have a chance to thrive and thrive extremely well in the state of New York.

Green: Looking at other markets, Curaleaf recently announced a big investment in Europe. How do you look at Europe in general as an investment opportunity?

Hawkins: We have a pretty interesting play in Europe right now through a company called Relief Europe. It’s poised to be one of the first entrants to Germany. We think it could be a big win for us. But let’s face it, Europe is still a little behind, in fact, a lot behind the United States in terms of where they are as an industry. Most of the capital that we’re going to be deploying is going to be done domestically in advance of legalization.

Green: What industry trends are you seeing in the year ahead?“We’re constantly learning from other industries that are steps ahead of us to figure out how to use those lessons as we continue to invest in cannabis.”

Hawkins: Well, I think you’ll see a lot of consolidation and a lot of ramping up in advance of legalization. I think that’s going to apply in all sectors. I just don’t see a scenario wherein mom and pops or smaller players are going to be successful exit partners with some of the new capital that’s coming in. They’re going to have to get to a point where they’re either selling to somebody bigger than them right now or joining forces with companies around the same size as them and creating mass. That’s the only way you’re going to compete with companies coming in with billions of dollars to deploy.

Green: How do you see this shaking out?

Hawkins: That’s where you start to look into the crystal ball. It’s really difficult to say because I think until we get to where we truly have a national footprint of brands, which would require crossing state lines, it’s going be really difficult to tell where things go. I do know that liquor, tobacco, beer, the distribution companies, they all are standing in line. Big Pharma, big CPG, nutraceuticals, they all want access to this, too.

In some form or fashion, these bigger players will dictate how they want to go about attacking the market on their own. So, that part remains to be seen. We’ll just have to wait and see where this goes and how quickly it goes there.

Green: Are you looking at other geographies to deploy capital such as APAC or Latin America regions?

Hawkins: Not at this point. It’s not a focus at all. What recently transpired here in the elections just really makes us want to focus here and generate positive returns for investors.

Green: As cannabis goes more and more mainstream, federal legalization is maybe more likely. How do you think the institutional investor scene is evolving around that? And is it a good thing to bring in new capital to the cannabis market?

Hawkins: I don’t see a downside to it. Some people are saying that it could damage the collegial and cottage-like nature of the industry. At the end of the day, if you’ve got tens of billions of dollars that are waiting to pour into companies listed on the CSC and up-listing to the NASDAQ or New York Stock Exchange, that’s only going to increase their market caps and give them more cash to acquire other companies. The trickle-down effect of that will be so great to the industry that I just don’t know how you can look the other way and say we don’t want it.

Green: Last question: What’s got your attention these days? What’s the thing you’re most interested in learning about?

Hawkins: We’re constantly learning about just where this industry is headed. We’re constantly learning from other industries that are steps ahead of us to figure out how to use those lessons as we continue to invest in cannabis. We all saw the correlation between cannabis and alcohol prohibition. The reality is that the industry is mature enough now where you can see similarities to industries that have gone from infancy to their adolescent years. That’s kind of where we are now and so we spend a lot of time studying industries that have been down this path before and see what lessons we can apply here.

Green: Okay, great. So that concludes the interview!

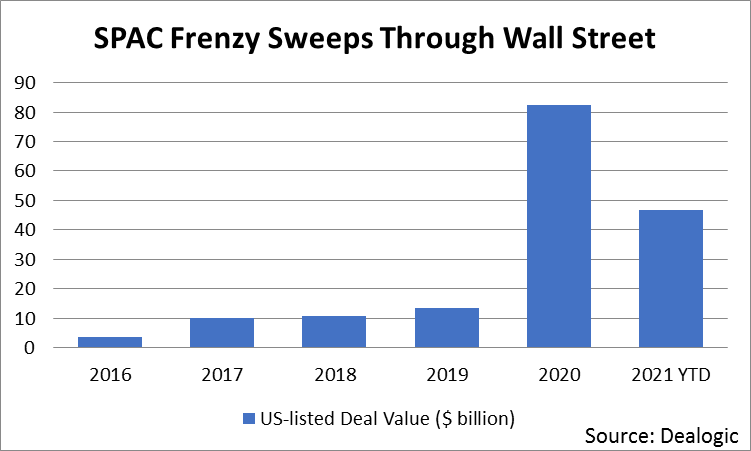

The unusual nature of 2020 gave rise to a reciprocally roller-coaster-like cannabis market. Cannabis was cemented officially as an essential industry with the rise of COVID-19, and November elections resulted in even more United States markets welcoming medical and adult-use sales.

The stagnant cannabis stock market of 2019 became a thing of the past by the end of 2020. Throughout the course of last year, bag holders anxiously watched cannabis options creep back up. Now, nearly two years since market decline in 2019, the cannabis stock market is exploding with blank checks and buyout fever. Much of this expectant purchasing is due to Canadian companies considering U.S. market entrance. Combined with the recent surge in the use of special purpose acquisition companies (SPACs) to invest, this has led to an increase in asset prices.

A SPAC is defined as “a company with no commercial operations that is formed strictly to raise capital through an initial public offering (IPO) for the purpose of acquiring an existing company.” Though they have existed for decades, SPACs have become popular on Wall Street the last few years because they are a way for a company to go public without the associated headaches of preparing for a traditional IPO.

In a SPAC, investors interested in a specific industry pool their money together without knowledge of the company they’re starting. The SPAC then goes public as a shell company and begins acquiring other companies in the associated industry. Selling to a SPAC is usually an attractive option for owners of smaller companies built from private equity funds.

The U.S.-Canadian market questions that this rising practice asks are: Can Canadian companies enter a bigger market and be more successful? Is it advisable for U.S. companies to sell their assets to Canadian corporations whose records may be marred by a history of losses and a lack of proper corporate governance? Regardless — if both SPAC’s and Canadian bailout money is here, what comes next?

What is Driving this Bull Market?

Underpinning these movements are record cannabis sales internationally, making last year’s $15 billion dollars’ worth of sales in the U.S. look small in comparison. New markets have opened up in various states and countries throughout 2020, and that trend is only expected to continue. New demographics are opening up, especially among older age groups. This makes sense, as most cannabis sales — even in a recreational setting — are people treating something that ails them like insomnia or aches and pains.

Cannabis is set to take off, and we are entering only the second phase of its market expansion. The world is becoming competitive. Well-run companies that are profitable in key markets are prime targets for bigger, growing companies. At the same time, the world of SPACs will continue to drive valuations. Irrespective of buying assets, growing infrastructure is and will continue to be greatly needed.

The Elusive Profitability Factor

When Canada blew up, one of the biggest changes was companies began focusing the year on cost cutting and — most importantly — profitability. Profitability became the buzzword. But bigger companies are on the search for already-profitable enterprises, not just those that have the potential to be. However, profitability is currently still unobtainable in Canada. Reasonable forecasters should expect this year will show a few companies getting bailed out while many others will be forced to either merge for survival or declare bankruptcy.

An ideal company’s finances should highlight not only revenue growth, but also profitability. Attention should be focused on how well businesses are run, and not on how much money they have the potential to raise or spend. Over the years, there have been many prospective companies that spent hundreds of millions only to barely operate, and are now shells in litigation. Throwing money at any deal should have been a lesson learned in the past, but SPACs are tempting because they are trendily associated with new, interesting management styles and charismatic businesspeople.

Companies should be able to present perfect and clear financials along with maintenance logs for all equipment. In today’s day and age, books must be stellar and clean. As money pours into SPACs, asset valuations for all qualities of companies will rise. The focus instead becomes about asset plays, which will cause assets to continue rising as money is poured into SPACs.

Once upon a time, if number counters presented a negative review or had to dig too much, executives would turn a cold shoulder on investment. But in the age of SPACs, these standards of evaluation will be greatly undervalued. Aging equipment and reportability of every piece of equipment may or may not be properly serviced and recorded in a fast-moving market. Costs of repair or replacing equipment that isn’t properly maintained may be a problem of the past. Because when money comes fast, none care for the gritty details.

Issues for SPACs

Shortage of talent and training has become a big concern already in the era of SPACs. How many quality assets are out there? Big operators in the U.S. are content and don’t see Canada as an enticing market to enter. So, asset buys are likely to primarily be in the U.S. Large companies like Aphria may buy out some of the major American players, but most Canadian companies will use new funding rounds to pay down debts. Accordingly, they will then be forced to piece together smaller operators as a strategy.

A cannabis company’s personnel and office culture are very important when looking to integrate into a larger corporate culture. Remember, it’s not just the brick and mortar that is being invested into, it is also the people that run a facility. Maintaining employee retention when a deal occurs is always critical. Your personnel should be highly trained and professional if you want to exit. Easy to plug-in corporate structures make all the difference in immediately gaining from the sale or having to retool the shed and bring in all new people.

The rise of the SPAC-era and Canadian entry into the U.S. market will cause asset increases, but it is only the second chapter in the market expansion of cannabis. Proper buys will nail profitability, impeccable books, proper maintenance records and will have created an efficient corporate structure with talented personnel. The rest will be overpriced land buys that will require massive infrastructure spending. The basics of a well-run organization don’t change. The cannabis market is going to ROAR, but don’t worry if the SPACs pass you by- they are buying at the start of cannabis only.

According to a press release published on February 8, a number of associations, advocacy organizations and cannabis businesses launched the U.S. Cannabis Council (USCC), which they claim is the largest coalition of its kind.

The 501(c)4 nonprofit organization goals are to advance social equity and racial justice, and end federal cannabis prohibition, according to their debut press release. The USCC says it will focus on federal reforms that achieve those goals above as well as promoting a safe and fair cannabis market on a national level.

The USCC’s Interim CEO is Steven Hawkins, who is also the executive director of the Marijuana Policy Project, which is one of the founding members of the USCC. “USCC is a unified voice advocating for the descheduling and legalization of cannabis,” says Hawkins. “Legalization at both the state and federal level must include provisions ensuring social equity and redress for harms caused to communities impacted by cannabis prohibition.”

In the press release, Representative Earl Blumenauer (D-OR) is quoted saying he is looking forward to working with the USCC on Capitol Hill. “As founder and co-chair of the Congressional Cannabis Caucus, I’ve seen firsthand that our most successful cannabis wins have been secured by a team,” says Rep. Blumenauer. “That’s why I am glad to see this first-of-its-kind alliance. We have a unique opportunity in the 117th Congress to advance cannabis reform, but we must remain united to create the change we know is possible.”

Founding members of the USCC include Acreage Holdings, Akerna Corp, the American Trade Association of Cannabis and Hemp, Canopy Growth, the Cannabis Trade Federation, Cresco Labs, MedMen, Marijuana Policy Project, PharmaCann, Vireo, Wana and much more. For a full list of its founding members, visit their website here.

As a cannabis lawyer, I spend a lot of time thinking about the ways that regulations affect a cannabis company’s bottom line. Since I’m in California, the ways are many.

In late 2017 I became the chief compliance officer for an Oakland startup that carried out delivery, distribution, cultivation and six manufacturing operations. A big part of my job was preparing my company, along with several equity cannabis companies, for California’s First Wave of cannabis licenses.

For the most part, First Wave licensees came from California’s essentially unregulated medical cannabis market, and/or from California’s by-definition unregulated “traditional” market. When California began issuing licenses in January 2018, many First Wavers were unprepared because their businesses practices had evolved in an unregulated market. A big part of my job was to help them adapt to the new requirements. As a result, I saw the regulations, and the effects of regulations, in sharp relief.

Regulation touches virtually every aspect of the legal cannabis industry in California. So anyone who wants to understand the industry should have at least a basic understanding of how the regs work. I’m writing this series to lay that out, in broad strokes.

Some key points:

The regulated market must be understood in relation to the previous unregulated (medical) market as well as the ongoing traditional market.

Regs define the supply chain.

Regs are designed to ensure product safety and maximize tax revenue.

Many regulations mandate good business practices.

Local enforcement of building, health and safety codes tends to be zealous and costly.

A Tale of Three Markets

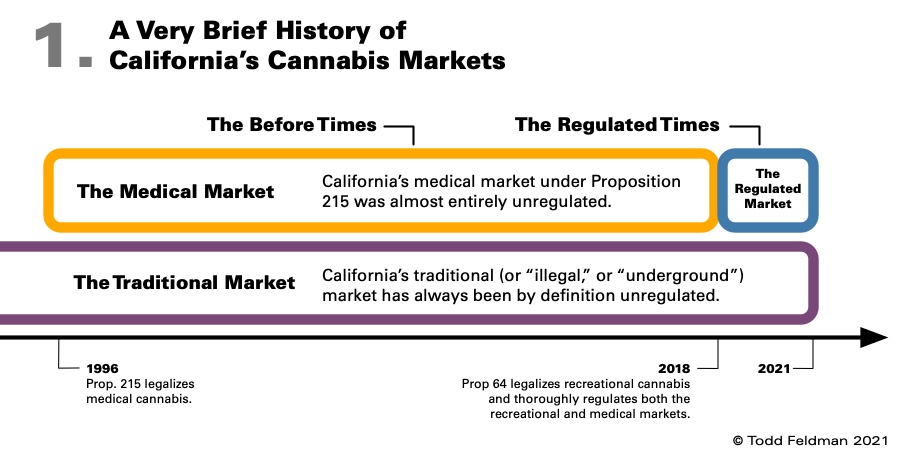

California’s regulated cannabis market can only be understood in relation to the medical market that preceded it, and in relation to the traditional market (illegal market) that continues to compete with it.

The Before Times

California’s legal medical cannabis market goes back to 1996, when the Compassionate Use Act passed by ballot measure. One fact that shaped the medical market was that it was never just medical – while it served bona fide patients, it also served as a Trojan horse for adult-use (recreational) purchasers.

Another fact that shaped the medical market was a near complete lack of regulation. On the seller’s side, you had to be organized as a collective. On the buyer’s side, you had to have a medical card. That was it.

Meanwhile, the cannabis supply chain was entirely unregulated. This tended to minimize production costs. It also meant that a patient visiting a dispensary had no way of verifying where the products had been made, or how.

The Regulated Times

Licensing under the Medical and Adult-Use Cannabis Regulation and Safety Act (the “Act”) began on January 1, 2018. It was the beginning of legal adult-use cannabis in California. It was also the beginning of the Regulated Times, as the Act and accompanying 300-plus pages of regulations transformed the legal cannabis market.

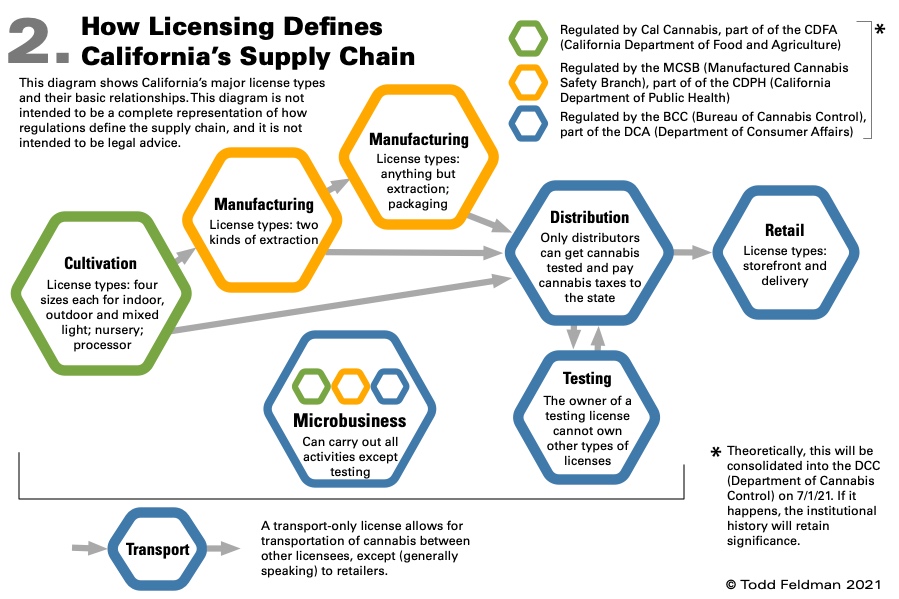

Across the supply chain, the internal procedures of cannabis companies are subject to review by state agencies;

Cultivators and manufacturers cannot sell directly to a dispensary – they must go through a distributor;

All cannabis must be tested for potency and a long list of contaminants by a licensed testing laboratory before it may be sold to consumers;

And beginning in 2019, all licensees were required to participate in the California Cannabis Track and Trace (CCTT) program, which is designed to track all cannabis from seed to sale.

Just as importantly, the Act establishes a dual licensing system – that is to say, in order to operate, a cannabis company needs a local permit (or other authorization) as well as a state license. In fact, local authorization is a prerequisite for a state license. And your local jurisdiction will have its own rules for cannabis that apply in addition to the state rules, up to and including a ban on cannabis activities.

Needless to say, operating in the Regulated Times is a lot more complicated and expensive than it was during the Before Times.

Especially when you consider the taxes. For example, in the City of Los Angeles, sale of adult-use cannabis is taxed at 10%, which means that any adult-use purchase in L.A. gets a 34.5% markup:

15% state cannabis excise tax, plus

10% Los Angeles Adult Use Cannabis Sales tax, plus

Note that the distributors must collect the excise tax from the retailer, so the 15% markup is not necessarily visible to the consumer. Similarly, consumers are generally unaware that there is a cultivation tax of $9.65 per ounce (or about $1.21 per eighth) of dried flower that the distributor has to collect from the cultivator.

Theoretically, all of this might be unproblematic if licensed retailers were only competing with each other. Which brings us to:

The Traditional Market

The traditional market is the illegal market, which is to say, the untaxed and unregulated market.

Legalization of adult-use cannabis was supposed to destroy the traditional market, but it hasn’t. As of early 2020, the traditional market was estimated to be 80% of the total cannabis market in California. This is not surprising, since the traditional market has the advantages of being untaxed and unregulated.

The traditional market has a pervasive negative effect on the legal market. For example, the traditional market tends to depress prices in the legal market and tends to attract talent away from the legal market. Some of these effects will be discussed in the following articles.

This article is an opinion only and is not intended to be legal advice.

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

We use tracking pixels that set your arrival time at our website, this is used as part of our anti-spam and security measures. Disabling this tracking pixel would disable some of our security measures, and is therefore considered necessary for the safe operation of the website. This tracking pixel is cleared from your system when you delete files in your history.

We also use cookies to store your preferences regarding the setting of 3rd Party Cookies.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.