There is a significant increase in demand for all cannabinoid products across the board—including CBD, THC, CBG and THCV—from recreational users, consumer packaged goods and pharmaceutical companies. And the next great race is on for the hottest arrival to scientific cannabis therapeutics: rare cannabinoids.

Research shows rare cannabinoids are poised to be the future of cannabis investing, providing better health benefits in addition to impacting the pharmaceutical, CPG, nutraceuticals, cosmetics and pet care markets significantly. According to recent reports, the biosynthesis of rare cannabinoids will be a $25 billion market by 2025 and $40 billion by 2040.

The companies that will revolutionize this market are ones with the highest quality and lowest prices, which means that biosynthetic cannabinoid companies will be the leaders in investment and capturing market share. We will also see a major consolidation in this market amongst the grow, harvest and extraction companies, increasing efficiencies and driving down costs.

What are rare cannabinoids and why should we care?

Tetrahydrocannabivarin (THCV)

Rare cannabinoids such as CBG, CBN, THCV, THCA and others have significantly better and more specific health benefits than just CBD on its own. Biotech companies like ours, Biomedican, which has a patent-pending biosynthesis platform, can produce pharmaceutical grade, non-GMO, bioidentical, synthetic cannabinoids with 0.0% THC at 70-90% less cost. Producing 0.0% THC means that rare cannabinoids can be added into nutraceuticals, CPG and cosmetics/lotions with zero changes in current cannabis regulations. Also, we produce the same exact product every time (not possible through plants), which is extremely important for pharmaceutical companies conducting clinical trials.

Why are rare cannabinoids important?

The human body contains different cannabinoid receptors that help regulate critical processes, including learning, memory, neuronal development, appetite, digestion, inflammation, overall mood, sleep, metabolism and pain perception. This considerable involvement of cannabinoid receptors, critical to many physiological systems, underscores their potential as pharmaceutical targets.

Tetrahydrocannabinol (THC), just one of hundreds of cannabinoids found in cannabis.

Pharmacological research has uncovered several medical uses for cannabinoids, which bind to cannabinoid receptors. They’ve been shown to help with pathological conditions such as pediatric epilepsies, glaucoma, neuropathic pain, schizophrenia and have anti-tumor effects as well as promote the suppression of chemotherapy-induced nausea. This ongoing research is becoming more prevalent and has the potential to uncover therapeutic uses for an array of cannabinoids.

In addition to the medical field, other prominent sectors have adopted the use of cannabinoids. There is an increasing demand for cannabinoids in inhalables, the food industry and in hygienic and cosmetic products. Veterinary uses for cannabinoids are also coming to light. The use of naturally occurring cannabinoids reduces the need for synthetic alternatives that may produce harmful off-target effects.

So how does this affect the investing market?

Where there is demand, significant and growth investments follow. All the major players from nutraceuticals, CPG, cosmetics and pet care companies are driving the demand for rare cannabinoids. We are seeing a major investment shift from commodity-based prices for cannabis and CBD to the new biosynthesis technology which offers significantly better health benefits and higher profit margins. Those unique qualities of rare cannabinoids open an enormous opportunity to create new drugs and food supplements for treating various medical conditions and improving the quality of life. This creates a massive global opportunity for all companies in these categories differentiating their products from competitors.

The structure of cannabidiol (CBD)

There will be big winners and losers in these markets, but at the end of the day, the highest quality and lowest cost producers will capture most of these markets. Biomedican has the highest quality, highest yields and lowest cost of production in the industry. Which we believe will make us the clear leader in the biosynthesis rare cannabinoid markets.

Which rare cannabinoid to invest in first?

Early reports indicate THCV (not to be confused with THC) could contain a variety of health benefits: it may help with appetite suppression/weight loss, possibly treat diabetes as well the potential to reduce tremors and seizures caused by conditions like multiple sclerosis, Parkinson’s disease and ALS.

There has been an explosion of interest in THCV due to its potential health benefits. We are seeing major players in the nutraceutical, health food and pharmaceutical industries clamoring to add THCV to their product lines. Companies can now produce THCV through biosynthesis, creating a pharmaceutical-grade, organic, bioidentical compound at 70-90% less than wholesale prices. This is exactly what the largest players in the market want: a pharmaceutical-grade, consistent product at significantly less cost. The current prices and quality have limited THCV production, but new breakthroughs in biosynthesis have solved those issues, so we expect a tsunami of orders for THCV in 2021.

Remediation of delta-9 tetrahydrocannabinol (d9-THC) has become a hot button issue in the United States ever since the Drug Enforcement Agency (DEA) released their changes to the definitions of marijuana, marijuana extract, and tetrahydrocannabinols exempting extracts and tetrahydrocannabinols of a cannabis plant containing 0.3% or less d9-THC on a dry weight basis from the Controlled Substances Act. That is because, as a direct consequence, all extracts and tetrahydrocannabinols of a cannabis plant containing more than 0.3% d9-THC became explicitly under the purview of the DEA, including work-in-progress “hemp extracts” that because of the extraction process are above the 0.3% d9-THC limit immediately upon creation.

The legal ramifications of these changes to the definitions on the “hemp extracts” marketplace will not be addressed. Instead, this article focuses on the amount of d9-THC that is available in the plant material prior to extraction and tracks a “hemp extract” from the point it falls out of compliance to the point it becomes compliant again and stresses the importance of accurate track-n-trace protocols at the processing facility. The model developed to support this article was intended to be academic and was designed to follow the d9-THC portion of a “hemp extract” through the lifecycle of a typical CO2-based extract from initial extraction to THC remediation. A loss to the equipment of 2% was used for each step.

Initial Extraction

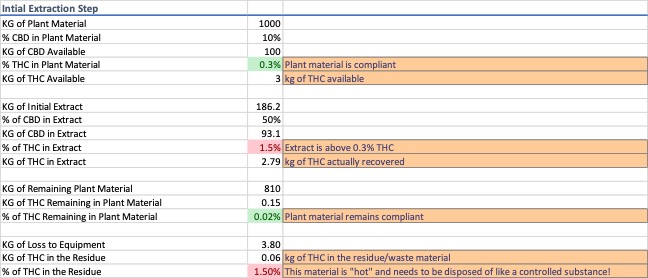

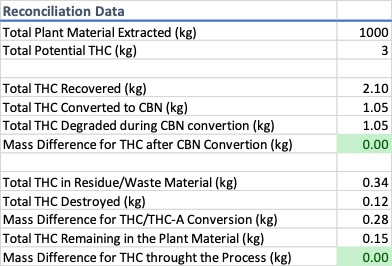

For this exercise, a common processing scenario of 1000 kg of plant material at 10% cannabidiol (CBD) and 0.3% d9-THC by weight was modeled. This amount, depending on scale of operations, can be a facility’s total capacity for the day or the capacity for a single run. 1000 kg of plant material at 0.3% d9-THC has 3 kg of d9-THC that could be extracted, purified, and diverted into the marketplace. CO2 has a nominal extraction efficiency of 95%, meaning some cannabinoids are left behind in the plant material. The same can be said about the recovery of the extract from the equipment. Traces of extract will remain in the equipment and this little bit of material, if unaccounted for, can potentially open an operator up to legal consequences. Data for the initial extraction is shown in Image 1.

Image 1: Summary Data Table for Typical CO2-based Extraction of Phytocannabinoids

As soon as the initial extract is produced it is out of compliance with the 0.3% d9-THC limit to be classified as a “hemp extract”, and of the 3 kg of d9-THC available, the extract contains approx. 2.8 kg, because some of the d9-THC remains in the plant material and some is lost to the equipment.

Dewaxing via Winterization and Solvent Removal

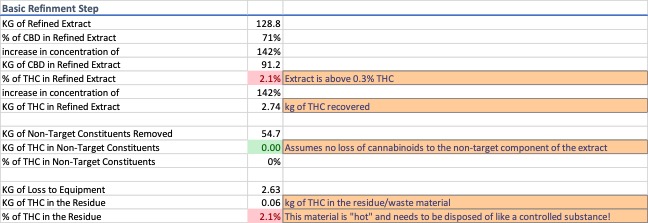

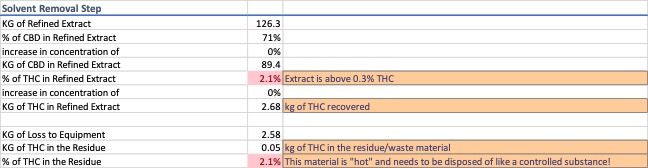

Dewaxing a typical CO2 extract via winterization is a common process step. For this exercise, a wax content of 30% by weight was used. A process efficiency of 98% was attributed to the wax removal process and it was assumed that 100% of the loss can be accounted for in the residue recovered from the equipment rather than in the removed waxes. Data for the winterization and solvent recovery are shown in Image 2 and 3.

Image 2: Summary Data Table for Typical Winterization of a CO2 ExtractImage 3: Summary Data Table for Solvent Removal from a CO2 Extract

Two things occur during winterization and solvent removal, non-target constituents are removed from the extract and there is compounded loss from multiple pieces of process equipment. These steps increase the concentration of the d9-THC portion of the extract and produce two streams of noncompliant waste.

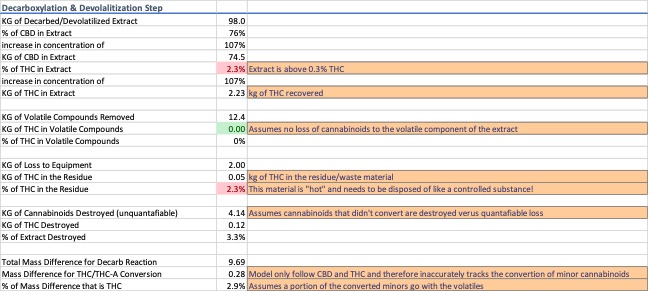

Decarboxylation & Devolatilization

Most cannabinoids in the plant material are in their acid form. For this exercise, 90% of the cannabinoids were considered to be acid forms. Decarboxylation is known to produce a mass difference of 87.7%, i.e. the neutral forms are 12.3% lighter than the acid forms. Heat was modeled as the primary driver and a process efficiency of 95% was used for the conversion rate during decarboxylation. To simplify the model, the remaining 5% acidic cannabinoids are presumed destroyed rather than degraded into other compounds because the portion of the cannabinoids which get destroyed versus degrade into other compounds varies from process to process.

Devolatilization is the process of removing low-molecular weight constituents from an extract to stabilize it prior to distillation. Since the molecular constituents of cannabis resin extracts vary from variety to variety and process to process, the extracts were assumed to consist of 10% volatile compounds. The model combines the decarboxylation and devolatilization steps to account for complete decarboxylation of the available acidic cannabinoids and ignores their weight contribution to the volatiles collected during devolatilization. Destroyed cannabinoids result in an amount of loss that can only be accounted for through a complete mass balance analysis. Data for decarboxylation and devolatilization are shown in Image 4.

Image 4: Summary Data Table for Decarboxylation and Devolatilization of a CO2 Extract

As the extract moves along the process train, the d9-THC concentration continues to increase. Decarboxylation further complicates traceability because there is both a known mass difference associated with the process and an unknown mass difference that must be calculated and justified.

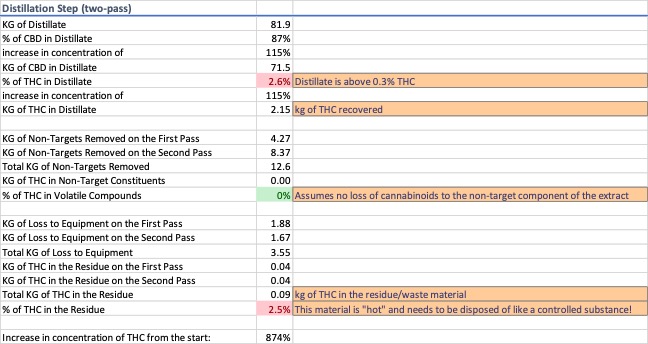

Distillation

A two-pass distillation was modeled. On each pass a portion of the extract was removed to increase the cannabinoid concentration in the recovered material. Average data for distilled “hemp extracts” was used to ensure the model did not over- or underestimate the concentration of the cannabinoids in the distillate. The variables used to meet these data constraints were derived experimentally to match the model to the scenario described and are not indicative of an actual distillation. Data for distillation is shown in Image 5.

Image 5: Summary Data Table for Distillation of a Decarboxylated and Devolatilized Extract

After distillation, the d9-THC concentration is shown to have increased by 874% from the original concentration in the plant material. Roughly 2.2 kg of the available 3 kg of d9-THC remains in the extract, but 0.8 kg of d9-THC has either ended up in a waste stream or walking out the door.

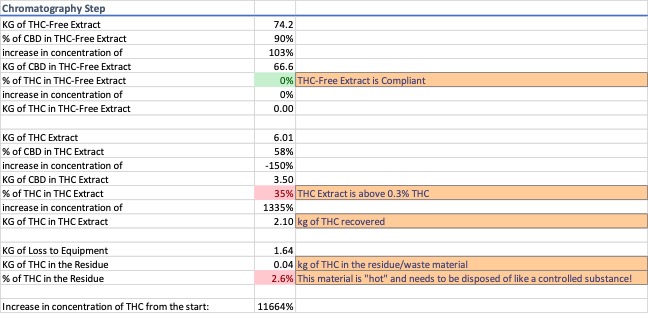

Chromatography – THC Remediation Step 1

Chromatography was modeled to remove the d9-THC from the extract. Because there are several systems with variable efficiency rates at being able to selectively isolate the d9-THC peak from the eluent stream, the model used a 5% cut-off on the front-end and tail-end of the peak, i.e. 5% of the material before the d9-THC peak and 5% of the material after the d9-THC peak is assumed to be collected along with the d9-THC. Data for chromatography is shown in Image 6.

Image 6: Summary Data Table for d9-THC Removal using Chromatography

After chromatography, a minimum of three products are produced, compliant “hemp extract”, d9-THC extract, and noncompliant residue remaining in the equipment. The d9-THC extract modeled contains 2.1 kg of the available 3 kg in the plant material, and is 35% d9-THC by weight, an increase of 1335% from the distillation step and 11664% from the plant material.

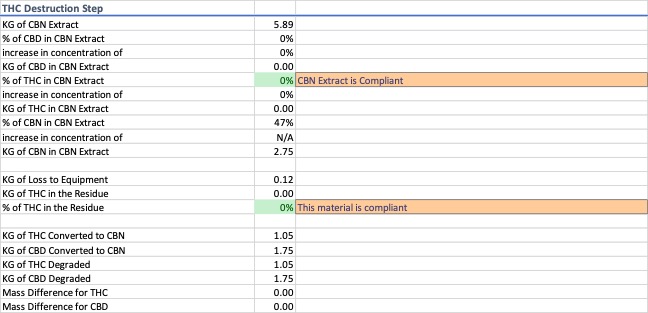

CBN Creation – THC Remediation Step 2

For this exercise, the d9-THC extract was converted into cannabinol (CBN) using heat rather than cyclized into d8-THC, but a similar model could be used to account for this scenario. The conversion rate of the cannabinoids into CBN through heat degradation alone is low. Therefore, the model assumes half of the available cannabinoids in the d9-THC extract are converted to CBN. The entirety of the remaining portion of the cannabinoids are assumed to convert to some form of degradant rather than a portion getting destroyed. Data for THC destruction is shown in Image 7.

Image 7: Summary Data Table for THC Destruction through Degradation into CBN

Only after the CBN cyclization step has completed does the product that was the d9-THC extract become compliant and classifiable as a “hemp extract.”

Image 8: Summary Data Table for Reconciliation of the d9-THC Portion of the Hemp Extract

Throughout the process, from initial extraction to the final d9-THC remediation step, loss occurs. Of the 3 kg of d9-THC available in the plant material only 2.1 kg was recovered and converted to CBN. 0.9 kg was either lost to the equipment, destroyed in the process, attributable to the mass difference associated with decarboxylation, or was never extracted from the plant material in the first place. All of these potential areas of product loss should be identified, and their diversion risk fully assessed. Not every waste stream poses a risk of diversion, but some do; having a plan in place to handle waste the DEA considers a controlled substance is essential. Without a track-n-trace program following the d9-THC and identifying the potential risk of diversion would be impossible. The point of this is not to instill fear, instead the intention is to shed light on a very real issue “hemp extract” producers and state regulators need to understand to protect themselves and their marketplace from the DEA.

On January 15, 2021, the USDA published its final rule on US hemp production. The rule, which becomes effective on March 22, 2021, expands and formalizes previous guidance related to waste disposal of noncompliant or “hot” crops (crops with a THC concentration above .3 percent). Importantly for the industry, the new disposal rules remove unduly burdensome DEA oversight and provides for remediation options.

Producers will not be required to use a DEA reverse distributor or law enforcement to dispose of noncompliant plants. Instead, producers will be able to use common on-farm practices for disposal. Some of these disposal options include, but are not limited to, plowing under non-compliant plants, composting into “green manure” for use on the same land, tilling, disking, burial or burning. By eliminating DEA involvement from this process, the USDA rules serve to streamline disposal options for producers of this agricultural commodity.

Alternatively, the final rule permits “remediation” of noncompliant plants. Allowing producers to remove and destroy noncompliant flower material – while retaining stalk, stems, leaf material and seeds – is an important crop and cost-saving measure for producers, especially smaller producers. Remediation can also occur by shredding the entire plant to create “biomass” and then re-testing the biomass for compliance. Biomass that fails the retesting is noncompliant hemp and must be destroyed. The USDA has issued an additional guidance document on remediation. Importantly, this guidance advises that lots should be kept separate during the biomass creation process, remediated biomass must be stored and labeled apart from each other and from other compliant hemp lots and seeds removed from non-compliant hemp should not be used for propagative purposes.

The final rules have strict record keeping requirements, such rules ultimately protect producers and should be embraced. For example, producers must document the disposal of all noncompliant plants by completing the “USDA Hemp Plan Producer Disposal Form.” Producers must also maintain records on all remediated plants, including an original copy of the resample test results. Records must be kept for a minimum of three years. While USDA has not yet conducted any random audits, the department may conduct random audits of licensees.

Although this federal guidance brings some clarity to hemp producers, there still remains litigation risks associated with waste disposal. There are unknown environmental impacts from the industry and there is potential tort liability or compliance issues with federal and state regulations. For example, as mentioned above, although burning and composting disposal options for noncompliant plants, the final rule does not address the potential risk for nuisance complaints from smoke or odor associated with these methods.

At the federal level, there could be compliance issues with the Resource Conservation and Recovery Act (RCRA), Comprehensive Environmental Response Compensation and Liability Act (CERCLA) and ancillary regulations like Occupation Safety and Health Administration (OSHA). In addition to government enforcement under RCRA and CERCLA, these hazardous waste laws also permit private party suits. Although plant material from cultivation is not considered hazardous, process liquids from extraction or distillation (ethanol, acetone, etc.) are hazardous. Under RCRA, an individual can bring an “imminent and substantial endangerment” citizen suit against anyone generating or storing hazardous waste in a way the presents imminent and substantial endangerment to health or the environment. Under CERCLA, private parties who incur costs for removal or remediation may sue to recover costs from other responsible parties.

At the state level, there could be issues with state agency guidance and state laws. For example, California has multiple state agencies that oversee cannabis and hemp production and disposal. CA Prop 65 mandates warnings for products with certain chemicals, including pesticides, heavy metals and THC. The California Environmental Quality Act (CEQA) requires the evaluation of the environmental impact of runoff or pesticides prior to issuing a cultivation permit. Both environmental impact laws permit a form of private action.

Given the varied and evolving rules and regulation on hemp cultivation, it remains essential for hemp producers to seek guidance and the help of professionals when entering this highly regulated industry.

Last week, GW Pharmaceuticals (Nasdaq: GWPH) announced they have entered into an agreement with Jazz Pharmaceuticals (Nasdaq: JAZZ) for Jazz to acquire GW Pharma. Both boards of directors for the two companies have approved the deal and they expect the acquisition to close in the second quarter of 2021.

GW Pharma is well-known in the cannabis industry as producing the first and only FDA-approved drug containing CBD, Epidiolex. Epidiolex is approved for the treatment of seizures in rare diseases like severe forms of epilepsy. GW is also currently in phase 3 trials seeking FDA approval for a similar drug, Nabiximols, that treats spasms from conditions like multiple sclerosis and spinal cord injuries.

Jazz Pharmaceuticals is a biopharmaceutical company based in Ireland that is known for its drug Xyrem, which is approved by the FDA to treat narcolepsy.

Bruce Cozadd, chairman and CEO of Jazz, says the acquisition will bring together two companies that have a track record of developing “differentiated therapies,” adding to their portfolio of sleep medicine and their growing oncology business. “We are excited to add GW’s industry-leading cannabinoid platform, innovative pipeline and products, which will strengthen and broaden our neuroscience portfolio, further diversify our revenue and drive sustainable, long-term value creation opportunities,” says Cozadd.

Justin Gover, CEO of GW Pharma, says the two companies share a vision for developing and commercializing innovative medicines, with a focus on neuroscience. “Over the last two decades, GW has built an unparalleled global leadership position in cannabinoid science, including the successful launch of Epidiolex, a breakthrough product within the field of epilepsy, and a diverse and robust neuroscience pipeline,” says Gover. “We believe that Jazz is an ideal growth partner that is committed to supporting our commercial efforts, as well as ongoing clinical and research programs.”

Part One of this series took a look at how the regulated cannabis market can only be understood in relation to the previous medical market as well as the ongoing “traditional” market. Part Two of the series describes how regulation defines vertical integration in California cannabis, and conversely, how vertical integration can address some of the problems that the regulations create. But first:

A Grain of Salt

Take the conventional wisdom about vertical integration with a grain of salt. Expected benefits may not materialize under the current circumstances:

Overall, the business environment is highly challenging due to extensive regulation, over taxation, insufficient retail capacity and competition from the “traditional” market. As a result, integrating businesses upstream or downstream may mean capturing losses, not profits.

The three major types of cannabis activity span three major industrial sectors: raw materials (i.e., cultivation), manufacturing and service (distribution, testing and retail). As a result, a vertically integrated company needs to carry out very different types of activity, which require very different types of core competencies, equipment and facilities.

Developing core competencies is especially challenging because each of the major cannabis sectors is still evolving.

Realizing the benefits of vertical integration requires an additional core competency in cross-sector operations.

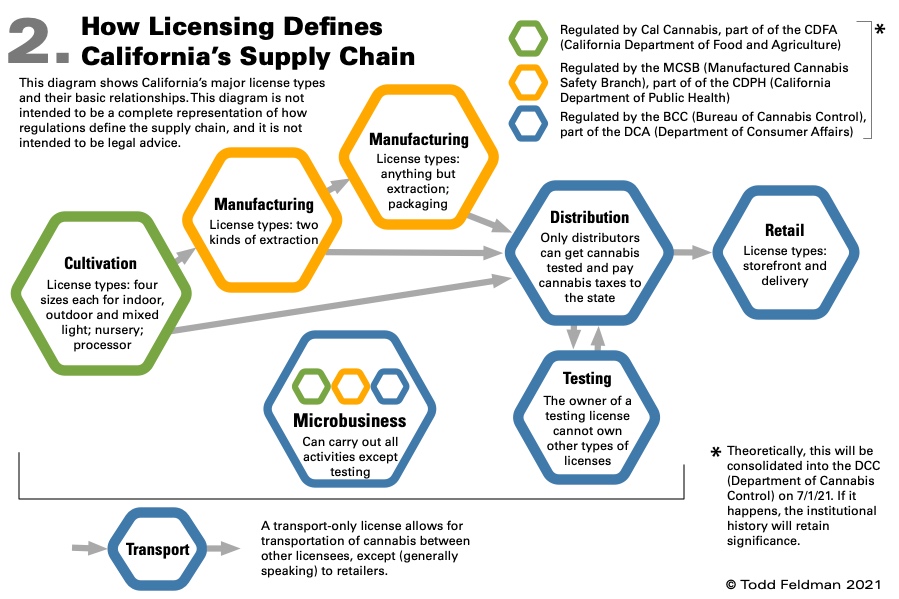

Regulations Define the Supply Chain

California’s regulations define the cannabis supply chain by defining both the individual links (licensees) and the relationships between those links. Therefore, an understanding of vertical integration must be grounded in an understanding of the underlying regulatory definitions.

The regulatory definition of each link is extensive. For example, each licensee is tied to a specific facility, and must have its own procedures for production, inventory control, security, etc. When the links are strung together, this definition tends to preserve operational redundancies, and impede operational integration.

Overall, the relationships between the links are primarily defined in terms of preserving the chain of cannabis custody. On top of that, regulations define very specific (and very consequential) links between certain licenses, as discussed below.

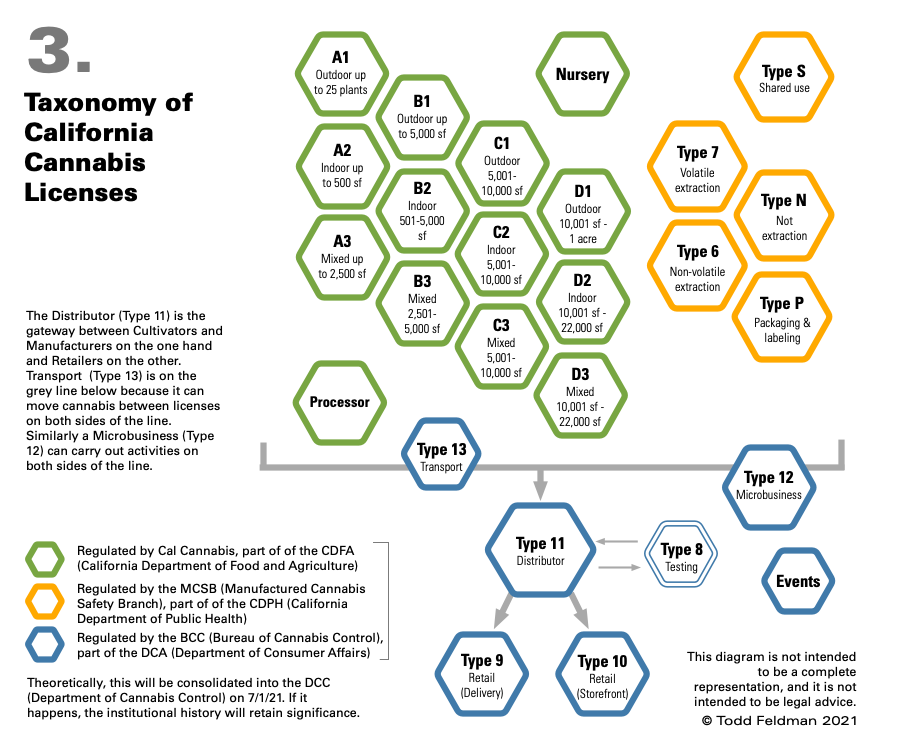

A Taxonomy of Links

There are currently 26 types of cannabis license in California, 25 of which can be vertically integrated:

Cultivation – 14 licenses, including 4 sizes each for Indoor (up to 22,0000 sf), Mixed Light (up to 22,000 sf) and Outdoor (up to 1 acre), as well as Nursery and Processor (drying, trimming and packaging/labeling). Note that cultivation licenses are the only licenses that restrict the scale of activities.

Manufacturing – 5 licenses, including volatile extraction, non-volatile extraction, everything but extraction (i.e., infusion) and packaging/labeling.

Testing (Type 8), for testing cannabis according to state standards prior to sale. The owner of a testing license cannot own any other type of license.

Distribution (Type 11), acts as the gateway between cultivation and manufacturing on the one hand, and retail on the other. The distributor’s gateway status is entirely an artifact of regulation – cannabis must be officially tested before it is sold to a consumer, and only a distributor can order the official test. All products must stay in a “quarantine” area at the distributor until they pass testing. Products that fail testing must be destroyed if they cannot be remediated.

Transport (Type 13), which can move cannabis between licensees (with a narrow exception). This license does not allow for official testing.

Delivery Retail (Type 10), for delivery services that are subject to the vagaries of software platforms and the intransigence of local authorities.

Microbusiness (Type 12), which allows the licensee to carry out cultivation (up to 10,000 square feet), non-volatile manufacturing, distribution and retail.

Event Organizer

Self-Distribution – A Case of Useful Integration

You may gather from the previous section that shoving a gratuitous and mandatory distributor into the middle of the supply chain creates problems for cultivators and manufacturers. Savvy operators solve this problem by getting a distribution license. This allows the cultivator or manufacturer to:

Pick the time and place for the testing of its cannabis products.

Avoid paying someone else for the storage of cannabis products as they await test results or purchase.

Reduce transport costs (particularly if the distributor is near the other operations).

Sell directly to retailers.

The bottom line is that vertical integration in California cannabis is useful as a means to an end, as opposed to an end in itself. Therefore, cannabis operators should carefully consider how vertical integration will benefit their core business before incurring the risks and expenses associated with an additional license.

This article is an opinion only and is not intended to be legal advice.

It’s no secret that the rollout of cannabis legalization has underperformed in countries like Canada. Since legalization in October of 2018, industry experts have warned that the projections of the big cannabis firms and venture capitalists far exceeded the expected demand from the legal market.

Today, major production facilities are closing down, some before they even opened, dried flower inventory is sitting on shelves in shocking quantities (and degrading in quality), and an extremely robust illicit market accounts for an estimated 80% of the estimated $8 billion Canadian cannabis industry. None of those things sound like reasons for optimism, but while some models for cannabis business are withering away, others are beginning to put down stronger roots. Crucially, we are beginning to see new business models emerge that will be able to compete against the robust black market in Canada.

The Legal Cannabis Industry Can’t Compete

Legal rollout in Canada could easily be described as chaotic, privileging larger firms with access to capital who were able to fulfil the rigid – and expensive – regulatory requirements for operating legally. But bigger in this case certainly did not mean better. The product these larger firms offered immediately following legalization was of a lower qualityand higher price than consumers would tolerate. In Ontario, cannabis being shipped to legal distributors lacks expiration dates, leaving retailers with no indication of what to sell first, and consumers stuck with a dry, poor quality product.

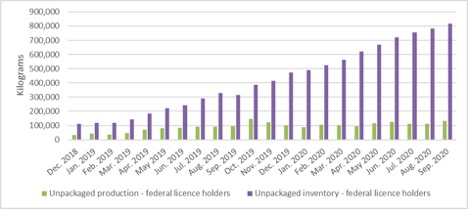

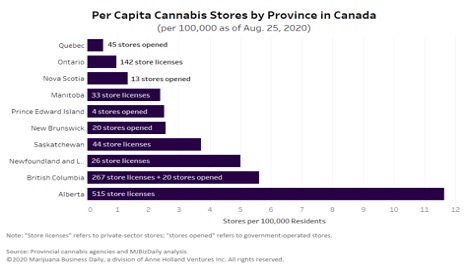

The majority of existing cannabis consumers across the country prefer the fresher, higher quality and generally lower priced product they can easily find on the illicit market. That preference couldn’t be clearer when you look at the growth of inventory, which is far outpacing sales, in the graph below:

Which brings us to the crux of the matter: when it comes to building up the Canadian cannabis industry, what will succeed against the black market that has decades of expertise and inventiveness behind it?

Rising From the Ashes: Craft Growers and Other Small-Scale Producers

The massive facilities like Canopy’s may be shutting down, but our friends over at Althing Consulting tell us that those millions of square feet facilities are being replaced by smaller, more boutique-style cultivation facilities in the 20,000 ft tier, which are looking to be the future of the industry.

Consumers have consistently shown a strong preference for craft cultivators and other small-scale producers who produce higher quality, more varied products that are more responsive to consumer needs. It also hasn’t hurt that prices are also coming down: Pure Sun Farms in Delta, BC is consistently selling out of their $100/ounce special, which is highly competitive even with the illicit market.

This vision of the industry matches up better with the picture we’ve been getting from other legalization projects around the world. It also squares with other indicators of success. Despite the small market capture of the legal market, industry employment numbers are still relatively high, especially when compared with more established legal consumer products markets such as beer. In fact, craft cannabis growers now employ nearly as many people as the popular craft brewing sector here in British Columbia.

But in order to make the craft cannabis market actually competitive in both the regulated and unregulated spaces, the government will have to address four major challenges.

Challenge #1: License Distribution is Uneven and Chaotic

A December 2020 report by Ontario’s auditor general contains admissions by the Alcohol and Gaming Commission of Ontario (AGCO), Ontario’s cannabis industry regulator, that they lack the capacity and resources to manage the number of applications for private cannabis retailing. Problems relating to the issuing of licenses, including long delays and difficult requirements, are widespread across provinces. One way this becomes clear is by looking at the very uneven distribution of stores across the country in the graph below.

Challenge #2: Basic Regulatory Compliance is Complex and Time-Consuming

Smaller-scale micro cultivators, whose good quality craft product remains in high demand, still face prohibitive barriers to entry into the legal market. Licensing from Health Canada is one onerous challenge that everyone must tackle. Monthly reporting requirements have in excess of 477 compliance fields. Without additional support to navigate these requirements – including automation technology to ease the administrative burden – these smaller producers struggle to meet the minimum regulatory standards to compete in the legal market.

Challenge #3: A Long-Distance Road to Compliance and Safety Means Higher Costs

Even with all regulatory requirements satisfied, cannabis cultivators can’t sell their product from “farm to fork” (to borrow a phrase from the food industry). Many growers ship their product to be irradiated in order to ensure they are below the acceptable microbial threshold set by Health Canada. While irradiation positively impacts the safety of the product, new evidence shows that it may degrade quality by affecting the terpene profile of the plant. Furthermore, only a few facilities in Canada will irradiate cannabis products in the first place, meaning that companies have to ship the finished product sometimes thousands of kilometers to get their product to market.

Next year, Health Canada looks set to lower the limit on microbials, making it virtually impossible to avoid cannabis irradiation. If Health Canada follows through, the change will be a challenge for small-scale cultivators who strive to prioritize quality, cater to consumers who are increasingly becoming more educated about terpene profiles, and seek to minimize the environmental impact of production.

Challenge #4: It is Virtually Impossible to Market Improved Products

Finally, there is a marketing problem. Even though the regulated market has made dramatic improvements in terms of product quality from legalization two years ago, Health Canada’s stringent marketing restrictions means that cannabis producers are virtually unable to communicate these improvements to consumers. Cannabis producers have little to no opportunity to reach consumers directly, even at the point of sale – most legal sales are funneled through government-run physical and online stores.

What Can a Thriving, Legal Cannabis Market Look Like in Canada?

The good news is that change is being driven by cannabis growers. Groups like BC Craft Farmers Co-Op are pooling resources, helping each other navigate financial institutions still hostile to the cannabis trade, obtain licenses and organizing craft growers to advocate to the government for sensible regulatory changes. As a result of their advocacy, in October, the federal government initiated an accelerated review of the Cannabis Act’s restrictive regulations related to micro-class and nursery licenses.

Now, more co-op models are popping up. Businesses like BC Craft Supply are working to provide resources for licensing, quality assurance and distribution to craft growers as well. Indigenous growers are also showing us how cannabis regulation could work differently. Though Indigenous cultivators currently account for only 4% of Canadian federal cannabis licensees (19/459), that number looks to be growing, with 72 new site applications in process self-identified as Indigenous, including 27 micro cultivators. In September, Williams Lake First Nation entered into a government-to-government agreement with the province of British Columbia to grow and sell their own cannabis. The press release announcing the agreement includes the following statement:

“The agreement supports WLFN’s interests in operating retail cannabis stores that offer a diverse selection of cannabis products from licensed producers across Canada, as well as a cannabis production operation that offers farm-gate sales of its own craft cannabis products.”

More widespread adoption of the farm-gate model, which allows cultivators to sell their products at production sights like a winery or brewery, has a two-fold benefit: it better supports local, small-scale producers, and it offers opportunities in the canna-tourism sector. As the economy begins its recovery alongside vaccine rollouts and restrictions on travel ease, provincial governments will have the chance to leverage the reputation of unique regional cannabis offerings (i.e. BC bud) through these farm-gate operations.

While the cannabis legalization story in Canada has had its bumps, the clear path forward for greater legal market success lies in increased support for micro-cultivators. By increasing support for these small-scale producers to navigate regulatory requirements, more will be able to enter the legal market and actually compete against their illicit counterparts. The result will be higher quality and more diverse products for consumers across the country.

More and more we are seeing the development of proprietary hardware platforms in cannabis. With proprietary technology in hand, manufacturers often lean on MSOs, LPs and other brand partners to grow their business through existing sales channels.

We spoke with Mike McDonald, President and CEO at Ammonite, to learn more about the history of the Dablicator™ platform and Ammonite’s North American brand partner strategy. Mike formed Ammonite as a spin-off company from Jetty Extracts after getting to know the founders in a real estate transaction. Prior to Ammonite, Mike was an operator in the manufacturing and product development space, having helped to launch the Giant bicycle brand as well as growing and eventually selling the Atlas Snowshoe Company to K2 Sports.

Aaron: How did you get involved in cannabis?

Mike: Well, like a lot of folks in the industry, my background is pretty eclectic. I come primarily from an operator’s perspective – I’ve been in manufacturing, product development and company growth for my whole career. I lived in Taiwan for several years and helped to launch the Giant bicycle brand worldwide. I was also involved with a ski business that was started at Stanford as a thesis project called Atlas Snowshoe Company. Fast-forward, we built it into the largest snowshoe brand and activity in the US and later sold it to K2 Sports. So, I’ve always been involved in the growth of product-related businesses.

Mike McDonald, President and CEO at Ammonite

I’ve also done some real estate development as well; I actually sold our building to the Jetty guys, which is how we met. In that process, I got involved with their company, helped Jetty reorganize its business model, raise some money, and then just got addicted to the whole industry and really found it fascinating. I liked the team at Jetty and couldn’t resist jumping in, and now I’ve been full-time in the business for over three years.

Aaron: How did you get involved in Ammonite?

Mike: Ammonite is actually a spin out company from Jetty Extracts, which is one of the largest brands in California. Our main Ammonite product is called the Dablicator™ Oil Applicator, which was originally invented at Jetty as a medical device for cancer patients. We saw a big demand for it as a private label partnership product, so we decided to spin out a separate hardware company and really focus on developing unique IP and CBD and cannabis related hardware.

Aaron: What trends are you following in the industry?

Mike: Certainly the MSOs of the world are really expanding and the top three to five are making a mark with growth and more sophistication in the market. I think the social equity movement is really a big component that we’re all excited about in the industry. You’re seeing the larger players really put their money where their mouth is around that. We’ve always been a big part of that in California.

Specifically, regarding trends in the cannabis space, Colorado and California are probably the two most mature markets. We generally say what’s happening in California and Colorado eventually make their way out to the rest of the world. Vaping was invented in California and Colorado, and now it’s a huge part of the business where before, four or five years ago, the market was mostly flower-centric.

There’s a trend away from inhalables, with more awareness around lung-related illnesses and of course COVID, so we’re seeing a big growth in edibles, drinks and so forth. Interestingly enough, although it’s an inhalable, infused pre-rolls are a big growth sector as well. Jetty is actually launching an infused pre-roll program in February.

Folks are looking for ways to get their medicine without smoking – and this has definitely led to a growth in the oil application business. Oil application has traditionally been delivered via a syringe. Dablicator™ oil applicator is essentially an improved, more convenient syringe. On the medical side, patients have been taking oil sublingually, putting it in food and drink and so forth for years because a lot of them can’t smoke. As that trend transfers over to the adult use market, oil application is becoming really big. You can take it sublingually; you can put it in your food or beverage. On the recreational side, you can add it to your loose flower or joints, or of course, dab it directly onto your rig via the heat resistant tip.

Further, you’re probably familiar with a lot of these portable dab rigs that are taking off, like the G Pen Roam and the Puffco Peak and a variety of others. So now you can dab on the go with your standard wax and shatter in a jar. It’s just not the most convenient way if you’re up on a hike or on a mountain bike ride. So now, with a portable dab rig and something like the Dablicator™ oil applicator, you can have a really convenient mess-free way to enjoy cannabis. The big growth in concentrates and areas that aren’t necessarily inhalables is where our product hardware really fits in.

Aaron: How did you come up with the idea for the Dablicator?

Mike: The Jetty team had a friend that had brain cancer. He was doing a lot of chemotherapy and was having trouble eating and keeping weight on and he couldn’t smoke. So, the guys at Jetty began to bring him cannabis oil, which he was able to use ingesting it from a spoon initially and it really helped him with his pain, his anxiety and his appetite. In that process, we realized that there wasn’t really a great way to deliver oil. Syringes were there, but they were kind of sketchy and they weren’t convenient.

So, the Jetty team developed a better mousetrap. Several iterations later, this Dablicator™ product was ready for patients. In fact, it became a big part of the Jetty Shelter Project, a non-profit where the team delivers cannabis to cancer patients, and it was a very much sought-after product delivery device in that world. So, it was developed inside of a need on the medical side and it’s really sort of grown inside the expansion on the adult-use side.

Aaron: Can you explain how the Dablicator™ oil applicator works from a perspective of form and function?

Mike: Pre-Dablicator™ you would use a syringe type product – for direct oil application, sublingual application, or as an add on to your flower. The difference between Dablicator™ oil applicator and a traditional syringe is that Dablicator™ is a twist and plunge product. Imagine a pen filled with oil, but instead of inhaling it, you’re able to dispense it through a tip that is heat resistant, which means you can apply directly to your dab rig nail. You’re able to put it in your pocket without fear of cannabis oil leakage. It’s discreet, precise, compact and portable.

Aaron: How does the user dose using Dablicator™ oil applicator?

Mike: Basically, there’s measurements on the plunger of 55 milligrams apiece – one click is 55 milligrams, and you can dispense as many clicks as you like. What’s cool about the product itself is if you’ve clicked too many times accidentally, you can back it off and the excess oil won’t dispense. You can go to dablicator.com and see demo videos as well.

Aaron: Dablicator™ oil applicator started as a Jetty Extracts spin-off. I see you are now white labeling for other oil brands. How do you go about selecting your partners?

Mike: We call it our brand partner program. It’s not too dissimilar to what other hardware manufacturers, like PAX and GPen, are doing. We’ve got a patented and innovative device where our brand partners, MSOs and leading brands throughout the US and Canada, can take their existing vape and tincture oils and offer them in Dablicator™ oil applicator hardware.

Our focus is signing up major, well respected brands and MSOs on to the “platform,” meaning they are able to immediately offer between six and ten new SKUs to their consumers. They take their existing oils, put them into a custom branded Dablicator™ hardware unit and add their custom branded packaging. It’s a full turnkey solution. For example, one of our partners, 710 Labs, is developing their RSO and were shopping for a delivery method specifically geared towards medical patients. Within eight weeks, we had a custom program for them and delivered hardware, and we assisted on the packaging front as well.

Our partners have to be reputable folks that are interested in developing or delivering oil in a unique and innovative way. Frankly, our early partners are those that see where the growth is. 710 Labs is on the platform, as well as Surterra in Florida, Ancient Roots in Ohio, and we’ve got multiple conversations going to some of the other MOSs and the LPs in Canada.

Aaron: Are the brand partners loading the oil applicator themselves?

Mike: We customize the product for them and then ship them unassembled and empty. In their lab, they use the same machinery and equipment they use to fill their vape cartridges. They then fill their Dablicator™, assemble it, package it and ship it out just like any other product that they’re processing and manufacturing.

Aaron: What kind of oils are suitable for Dablicator™?

Mike: Pretty much any oil that’s going into a vape cart is suitable and then some. Some of our customers, including Jetty, started out with a THC distillate. Live resin is becoming a big product category in California as well as solventless oils. Dablicator™ oil applicator can accommodate everything from distillate to live resin to solventless to RSO and even full spectrum CBD. If it can flow, if it doesn’t crystallize up like shatter and sugars and diamonds, you can put it into Dablicator™, even the thickest of oils. It’s designed to contain any kind of liquids that are flammable.

Aaron: What geographies are you currently in?

Mike: We’re in multiple states throughout the US and actually just signed up with an LP in Canada. We only launched the program in August of 2020, and today we’ve got partners California, Colorado, Ohio, Arizona, Missouri, Florida, soon to be Michigan, Illinois, and throughout Canada.

Aaron: Any plans for international expansion beyond North America?

Mike: We’re getting inquiries on a regular basis from all over the place, including internationally. We’re in conversations with some folks down in Brazil. Spain is actually a big cannabis market and we’re having some conversations with some folks there. The inquiries are coming in faster than we can process the relationships, but right now our major focus is on North America.

Aaron: What are your goals with Ammonite?

Mike: We are developing a category, right? So today, oil dispensing isn’t top of mind. Today, if you want oil, you go into a dispensary and say, “Hey, give me those syringes.” My goal is that a year from now, you can walk into Harborside in Oakland and you see a wall of different branded Dablicator™ oil applicators. The goal is to really turn the oil dispensing business into a category, and then position Dablicator™ oil applicator as the best and leading product in that category.

Aaron: What are you personally interested in learning more about?

Mike: Well, I’ve got two teenagers – two daughters, as a matter of fact, a freshman and a senior – and they’re being homeschooled right now. So that’s been quite an interesting development!

I think on the cannabis side, it’s just fascinating what it is as a business model. It’s the most recent multi-billion-dollar opportunity in consumer products. You only get a chance to participate in something like that maybe once in a lifetime. I’m really looking forward to seeing it become more adopted into the mainstream and it’s already becoming that way from a consumer perspective. I am watching the cannabis market become legal from a federal perspective, hoping that the social equity component of the industry really stays with it.

I’ve been in a lot of businesses over the years; I feel like one of the gray hairs in this business that is actually an operator versus someone who came over from the financial side. I am continuing to learn, grow and work with great people and this has been a really amazing experience for me.

Aaron: Okay, great. Mike, that’s the end of the interview. Thank you for your time today!

According to a press release sent out last week, MCR Labs just opened their newest facility in Pennsylvania. The laboratory, based in Allentown, PA, began accepting and testing cannabis samples last week.

A lab technician at MCR Labs weighs flower for testing.

MCR Labs became the first independent cannabis testing lab to get certified in Massachusetts. The lab based in in Framingham, Massachusetts (a little west of Boston) is ISO 17025:2017 accredited.

Michael Kahn, president and founder of MCR Labs, believes this is a huge step for their company. “We’re excited to be expanding and excited for the opportunity to carry out our mission of advancing public health and safety here in the Keystone State,” says Kahn.

The Allentown, PA facility is led by Julia Naccarato. “I’m grateful to MCR for the opportunity to offer the team’s expertise to Pennsylvania’s cannabis providers and to help ensure the safety of products they offer to medical marijuana patients,” says Naccarato.

According to a press release sent out last week, Complex Biotech Discovery Ventures (CBDV) has expanded their testing capabilities considerably with the new addition of a vapor/smoke analyzer. CBDV is a licensed cannabis and psilocybin research laboratory embedded in the University of British Columbia, led by CEO Dr. Markus Roggen.

Dr. Markus Roggen, Founder of Complex Biotech Discovery Ventures (CBDV)

The ability to analyze vapor and smoke is a relatively novel concept for the cannabis space, but has been utilized by the tobacco industry for years now. In the early days of adult-use cannabis legalization in the United States, stringent testing regulations for contaminants like pesticides were adopted out of a fear for what would happen when consumers ingest toxic levels of contaminants.

One of the common refrains iterated throughout the industry over the past ten years was that there just wasn’t enough research on how different contaminants affect patients and consumers when burned and inhaled. We still don’t know too much about what happens when someone smokes a dangerous pesticide, such as myclobutanil. Beyond just contaminants, the new technology allows for companies to measure precise levels of cannabinoids in vapor and smoke, getting a more accurate reading on what cannabinoids are actually making it to the end user.

The smoke analyzer at CBDV

This new development coming from our neighbor to the north could lead to a breakthrough in the cannabis lab testing and research space. CBDV claims they can now analyze cannabis material with a much more in-depth analysis than basic compliance testing labs. The new technology for analysis of smoke, vapor, plant material and formulations allows companies to thoroughly understand their materials in each stage of the product formulation process, all the way to product consumption.

Beyond just smoke and vapor analysis CBDV also offers NMR spectroscopy, metabolomics, nanoparticle characterization, computational modeling and other testing services that go far beyond the traditional compliance testing gamut.

“Our new services offer comprehensive insights into plant material, extracts, end-products and even the smoke/vapor by using state-of-the-art analytical instruments,” says Dr. Roggen. “By understanding the chemical fingerprint of the material, cannabis producers can eliminate impurities, adjust potencies, and optimize extraction processes before wasting money and resources on producing inconsistent end products. As a chemist I am really excited about adding NMR and high-res mass spectroscopy to the cannabis testing offerings.”

As a cannabis lawyer, I spend a lot of time thinking about the ways that regulations affect a cannabis company’s bottom line. Since I’m in California, the ways are many.

In late 2017 I became the chief compliance officer for an Oakland startup that carried out delivery, distribution, cultivation and six manufacturing operations. A big part of my job was preparing my company, along with several equity cannabis companies, for California’s First Wave of cannabis licenses.

For the most part, First Wave licensees came from California’s essentially unregulated medical cannabis market, and/or from California’s by-definition unregulated “traditional” market. When California began issuing licenses in January 2018, many First Wavers were unprepared because their businesses practices had evolved in an unregulated market. A big part of my job was to help them adapt to the new requirements. As a result, I saw the regulations, and the effects of regulations, in sharp relief.

Regulation touches virtually every aspect of the legal cannabis industry in California. So anyone who wants to understand the industry should have at least a basic understanding of how the regs work. I’m writing this series to lay that out, in broad strokes.

Some key points:

The regulated market must be understood in relation to the previous unregulated (medical) market as well as the ongoing traditional market.

Regs define the supply chain.

Regs are designed to ensure product safety and maximize tax revenue.

Many regulations mandate good business practices.

Local enforcement of building, health and safety codes tends to be zealous and costly.

A Tale of Three Markets

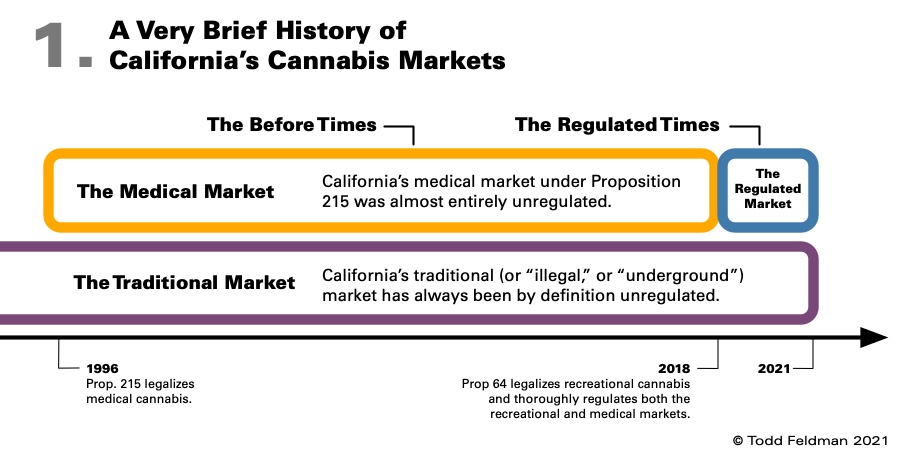

California’s regulated cannabis market can only be understood in relation to the medical market that preceded it, and in relation to the traditional market (illegal market) that continues to compete with it.

The Before Times

California’s legal medical cannabis market goes back to 1996, when the Compassionate Use Act passed by ballot measure. One fact that shaped the medical market was that it was never just medical – while it served bona fide patients, it also served as a Trojan horse for adult-use (recreational) purchasers.

Another fact that shaped the medical market was a near complete lack of regulation. On the seller’s side, you had to be organized as a collective. On the buyer’s side, you had to have a medical card. That was it.

Meanwhile, the cannabis supply chain was entirely unregulated. This tended to minimize production costs. It also meant that a patient visiting a dispensary had no way of verifying where the products had been made, or how.

The Regulated Times

Licensing under the Medical and Adult-Use Cannabis Regulation and Safety Act (the “Act”) began on January 1, 2018. It was the beginning of legal adult-use cannabis in California. It was also the beginning of the Regulated Times, as the Act and accompanying 300-plus pages of regulations transformed the legal cannabis market.

Across the supply chain, the internal procedures of cannabis companies are subject to review by state agencies;

Cultivators and manufacturers cannot sell directly to a dispensary – they must go through a distributor;

All cannabis must be tested for potency and a long list of contaminants by a licensed testing laboratory before it may be sold to consumers;

And beginning in 2019, all licensees were required to participate in the California Cannabis Track and Trace (CCTT) program, which is designed to track all cannabis from seed to sale.

Just as importantly, the Act establishes a dual licensing system – that is to say, in order to operate, a cannabis company needs a local permit (or other authorization) as well as a state license. In fact, local authorization is a prerequisite for a state license. And your local jurisdiction will have its own rules for cannabis that apply in addition to the state rules, up to and including a ban on cannabis activities.

Needless to say, operating in the Regulated Times is a lot more complicated and expensive than it was during the Before Times.

Especially when you consider the taxes. For example, in the City of Los Angeles, sale of adult-use cannabis is taxed at 10%, which means that any adult-use purchase in L.A. gets a 34.5% markup:

15% state cannabis excise tax, plus

10% Los Angeles Adult Use Cannabis Sales tax, plus

Note that the distributors must collect the excise tax from the retailer, so the 15% markup is not necessarily visible to the consumer. Similarly, consumers are generally unaware that there is a cultivation tax of $9.65 per ounce (or about $1.21 per eighth) of dried flower that the distributor has to collect from the cultivator.

Theoretically, all of this might be unproblematic if licensed retailers were only competing with each other. Which brings us to:

The Traditional Market

The traditional market is the illegal market, which is to say, the untaxed and unregulated market.

Legalization of adult-use cannabis was supposed to destroy the traditional market, but it hasn’t. As of early 2020, the traditional market was estimated to be 80% of the total cannabis market in California. This is not surprising, since the traditional market has the advantages of being untaxed and unregulated.

The traditional market has a pervasive negative effect on the legal market. For example, the traditional market tends to depress prices in the legal market and tends to attract talent away from the legal market. Some of these effects will be discussed in the following articles.

This article is an opinion only and is not intended to be legal advice.

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

We use tracking pixels that set your arrival time at our website, this is used as part of our anti-spam and security measures. Disabling this tracking pixel would disable some of our security measures, and is therefore considered necessary for the safe operation of the website. This tracking pixel is cleared from your system when you delete files in your history.

We also use cookies to store your preferences regarding the setting of 3rd Party Cookies.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.