As the cannabis industry grows, companies are faced with more labor related compliance and regulatory issues, which require time and expertise. Rather than hire internal staff to manage human resources (HR) and compliance, many companies choose to outsource nearly 85% of HR functions. These functions include payroll administration, HR tasks and other employment liabilities, like insurance, to a third-party Managed Service Provider (MSP). This model frees up internal resources to grow and develop the company’s core business, while also offsetting risks associated with employment, taxes and insurance.

Nicholas Murer formed WECO in 2014 to provide human capital financial services to the legal cannabis industry, offering services like payroll management, workforce management, human resource implementation, accounting solutions, recruiting and staffing. The company has since expanded to providing consulting services, financial product representation, investor asset development, wholesale trading and advising emerging market development projects worldwide.

With markets across the country maturing at a rapid rate, change is a constant. Cannabis companies operating in new markets need to maintain compliance while focusing on their business plan, which can be a difficult task. We sat down with Nick Murer to learn more about compliance issues that cannabis businesses face, like workers comp, payroll taxes, insurance and how outsourcing some HR functions can help.

Q: What are some of the major labor compliance issues faced by employers in the cannabis industry?

Nicholas Murer: Like other industries, the cannabis industry is subject to labor related regulations like paid time off, harassment prevention training, workers compensation requirements, payroll taxes, pay transparency, unemployment insurance and reporting. Unless companies have an expert, or a team of experts, monitoring and managing compliance on both the employer and employee side, they may quickly find themselves in hot water with state regulatory agencies, or even with an employee for labor law violations.

Another issue continues to be access to banking and payment processing. Many cannabis companies continue to pay employees and vendors in cash, which creates not only problems in accurate accounting, but safety concerns for employees as well. There are banks and credit unions that will work with cannabis companies, but without a partner who has relationships with and access to a proven and trusted network of banks and processors, monthly account and transaction fees can be expensive and out of reach. With the SAFE Banking Act stalled once again in Congress, this will continue to be an issue.

Q: How can cannabis companies mitigate their risk by outsourcing HR functions?

Murer: By utilizing a Managed Service Provider (MSP), cannabis companies enter a labor contract model for payroll and HR administration. An MSP is a professional workforce management company that provides comprehensive employment services for businesses.Nick Murer and the WECO team will be at the CQC this October 16-18. Click here to learn more.

This model provides the client company with the best labor practices, risk mitigation and claims management with access to national workers compensation and unemployment insurance. The MSP is the employer of record, so is responsible for most aspects of the employee/employer relationship. The day-to-day management of the employee continues with the client company, but the company’s liability and risk are reduced. MSP compliance risk reducing services include:

Background screening and reporting

Labor related compliance management at state and local levels

Handbook and policy management and distribution to employees

A central location for employee onboarding, time and assignment tracking, payroll administration and reporting

Separation of labor cost for each location/company for 280E tax mitigation

All federal, state and local tax filings

Employment verification

Employee access to health insurance

Employee access to banking for payroll direct deposit

Outsourcing to an MSP provides cost savings to the company, including:

Reduced staff

More efficient payroll processing and legal compliance

Streamlined recruitment

Utilizing WECO to manage the employer of record process allows client companies to look beyond traditional payroll to a full workforce management solution that ensures a smooth payroll and provides the tools that can support the growth and development of a workforce including compliant banking, human resources management and employee services.

About Nicholas Murer

Nicholas Murer formed WECO in 2014 to provide human capital financial services to the legal cannabis industry, offering services like payroll management, workforce management, human resource implementation, accounting solutions, recruiting and staffing. Nick Murer has more than twenty years of professional and technical sales experience working globally in the energy, engineering and scientific industries, including a substantial background in industrial technical sales, account development, marketing, human resources, acquisitions and project management. He studied accounting and business management at the University of Pittsburgh and organization development and human resource management from Colorado State University.

As a business owner, insurance is always a must. If you are interested in entering into the cannabis industry or you already have, it’s important to know what to expect when it comes to insuring your cannabis-related business.

That’s why we’ll be exploring what dispensary insurance is, different options for business owners and general advice regarding dispensary and other CRB insurance.

What is Dispensary Insurance?

Insurance for cannabis-related businesses refers to policies that protect the business against risk. This can include dispensaries, cultivation centers and testing labs – all of which require different levels of coverage and liability.

We spoke to Alexander Marenco, an insurance broker from Marenco Insurance, who explained what dispensary owners should know before seeking out insurance. Marenco says it’s similar to shopping for insurance for other businesess. “You need to have full details of the business and location to receive a quote.” He adds. “The applications will ask questions such as location, renovations, or improvements to the location, ownership information, payroll details, and sales or projected annual sales.”

How is Dispensary Insurance Different From Other Forms of Business Insurance?

Because non-hemp-derived cannabis is still considered a schedule one controlled substance under the Controlled Substance Act, cannabis insurance can be more expensive than regular insurance for non-cannabis businesses. Because of the risks associated with being considered a potential retailer of a controlled substance, liability policies and other options can cost a pretty penny.

The cash-only nature of the business makes insuring dispensaries more costly

Additionally, when asking Marenco about how dispensary insurance differs from other brick-and-mortar retail insurance, he says: “With more states increasingly legalizing medicinal and recreational marijuana, insurance carriers have started to open risk acceptability. However, since marijuana is still federally illegal, businesses will find it difficult to find multiple quotes from different carriers.”

Types of Insurance Available for Cannabis-Related Businesses

What kind of insurance is available for cannabis-related businesses? Let’s find out.

First off, it’s important to keep in mind that CRBs are at risk for a lot of things: workplace accidents, damage to property, theft, general liability and product liability. Plus, the fact that most dispensaries work on a cash-only business model until the Secure and Fair Enforcement (SAFE) Banking Act is approved by Congress, CRBs tend to handle big amounts of cash, further putting them at risk of theft and liability. CRB insurance can be as low as $350 and as high as $7,500 depending on the type of business and policy.

Here are some of the most common types of insurance for CRBs and what they cover:

General liability: third-party claims for bodily injury, property damage and reputational harm.

Commercial property: damage to a business-owned property.

Professional liability: third-party accusations of negligence and mistakes.

Workers’ compensation: employees’ medical bills and lost wages due to injury or illness.

Inland marine: damage or theft of business-owned property in transit.

Crop: costs from damage to seeds and plants.

With so many things to watch out for, insurance for cannabis businesses and dispensaries isn’t cheap. Here, Marenco says what CRB owners can do to keep their premiums as low as possible:

A smart safe like this one can help secure cash handling

“Premiums are primarily based on sales (actual or projected). After the term expires, the insurance carrier will conduct an audit for the prior term to confirm the information from the application. The audited discrepancy will adjust the next term’s sales figures. Dispensary insurance will typically be placed through an excess & surplus market which do not provide traditional discounts.”

So, in essence, the best thing a dispensary owner can do is be honest about their projections.

Navigating premiums can be a detailed process, as we learned when speaking to Jesse Giffith, an owner of Smokeless CBD and Vape: a chain of retail shops across the twin cities Minneapolis–Saint Paul, Minnesota:

“Our shops carry insurance that has been offered with a modified rate for vape retailers. This route was not as straightforward as some traditional retail insurance options, but may offer benefits, and a better fit for coverage than other dispensary insurance options.”

A Growing Number of Dispensaries Across America

With the growing legalization and normalization of adult use, medical and hemp-derived cannabis across the nation, it should come as no surprise that the number of dispensaries across the country grows exponentially.

In 2021, the cannabis market in the U.S. was valued at 10.8 billion dollars, with an expected annual growth of 14.9% annually. This is a sign of what’s to come. Cannabis may be an industry that’s been considered taboo for decades, but the growth shows the growing acceptance of the plant for medical and adult use reasons.

Insurance providers remain cautious as cannabis laws are still in flux.

With that growth comes a greater need for insurance providers, opening the door to the possibility that these two industries will grow in tandem. The future may bring a greater variety of options for coverage at cheaper prices. But for the time being, insurance providers remain cautious as the fate of federal and local cannabis laws are still in flux.

Are There Limited Carriers that Issue Dispensary Insurance?

Every CRB needs insurance, just like any other type of establishment, business or company. The issue within the cannabis industry is that there is still a limited insurance market, with insurers willing to provide insurance constantly exiting and entering the market. Plus, the overall capacity and variety of policies that cover different types of risks are limited. Lastly, it can be difficult to use CRB insurance when you read between the lines of the policy. Because cannabis with THC is still federally illegal (excluding hemp-derived cannabis products containing less than 0.3% THC), insurers can negate coverage when a loss or claim occurs.

Because of the complications that may arise even if you do have insurance, Marenco offers some advice for dispensary owners that are searching for the right insurance option for them: “Before shopping for insurance make sure you have all your licenses and are in full compliance with all regulations. Insurance carrier’s requirements from the state. Additionally, consider different coverage options.” He continues. “At a minimum, a business needs general liability insurance. Insurance companies can also consider covering business property including inventory, betterments, and improvements to a rented space, among others. When shopping for insurance make sure your agent reviews different coverage options.”

2022 brought more change and visibility to the cannabis industry than nearly any year before. Two of five legalization ballot measures passed, bringing the total number of states with legal medical or medical and recreational laws to 39. President Biden issued an executive order pardoning nonviolent offenders and directing a review into rescheduling cannabis. The Medical Marijuana and Cannabidiol Research Expansion Act was enacted. Cannabis arose prominently in legislatures across the country, with over 50 federal bills and hundreds of state-level measures introduced.

We’ve yet to see the full impact from Biden’s October 6 announcement

But as 2022 came to a close, only a handful of actions are being carried into the new year, and the industry faces more hardship and turmoil than it has since the inception of legalization. Legal cannabis retailers and cultivators in markets across the country continue to struggle with onerous regulations and competition from the illicit market, and oversupply in these markets is driving down prices as West Coast growers and manufacturers anxiously await interstate commerce.

Looking ahead to the coming year, industry watchers can anticipate certain issues and legislation: further investigation into cannabis’ classification on the Controlled Substances Act (CSA) from federal agencies, federal cannabis pardons coming to fruition, a follow-up from the Department of Justice’s technical report, and the reintroduction of high-profile federal legislation, like the Cannabis Opportunity Act (CAOA), the States Reform Act, Marijuana Opportunity Reinvestment and Expungement (MORE) Act, Harnessing Opportunities by Pursuing Expungement (HOPE) Act and the Secure and Fair (SAFE) Banking Act.

Below, we recap some of the big moments of 2022 and what to expect in 2023.

A Presidential Pardon for Simple Possession

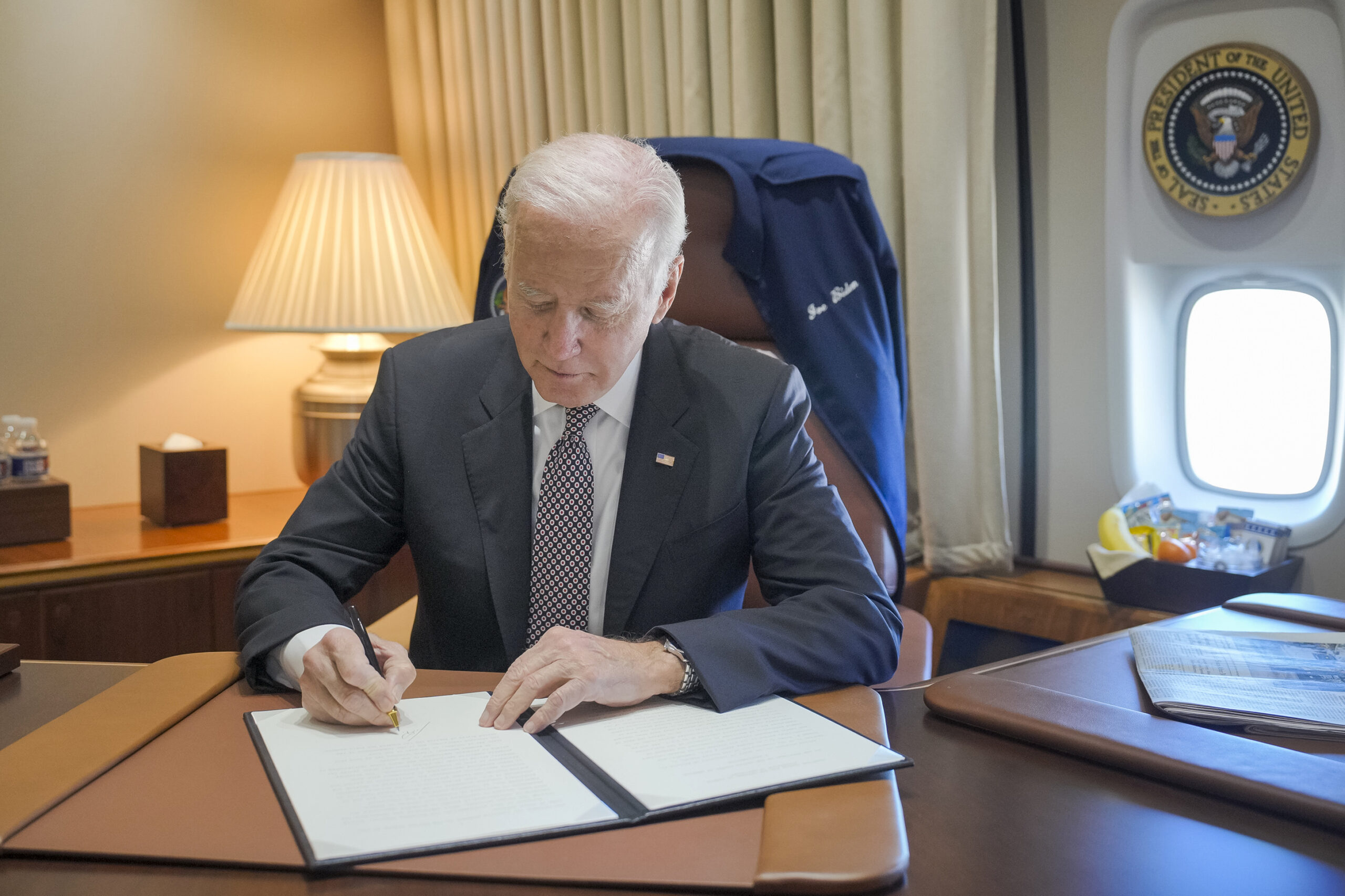

On Oct. 6, President Biden made a historic announcement to “grant a full, complete, and unconditional pardon to all current United States citizens and lawful permanent residents who committed the offense of simple possession of marijuana in violation of the Controlled Substances Act” and “all current United States citizens and lawful permanent residents who have been convicted of the offense of simple possession of marijuana in violation of the Controlled Substances Act.” His executive order also encouraged governors to follow suit for cases regarding state offenses and requested that the secretary of Health and Human Services and the attorney general “expeditiously” review how cannabis is scheduled under federal law.

Biden signing his executive order back in October of 2022

The president’s strategic plan attempts to at least partly address some of the adverse impacts of the United States’ war on drugs on certain populations like low-income and Black and Latinx Americans. While an admirable and important effort, certain portions of his executive order will take much longer than others to yield tangible impact. A federal pardoning can take anywhere between two to five years, and the laws and duration of state-level pardoning vary—depending on the state and its governing practices. Additionally, since governors are not required to pardon individuals following the president’s executive order, some convicted persons may never see or be able to seek justice. And the most uncertain timeline relates to the review of cannabis’ classification on the CSA. Rescheduling or descheduling a substance under the CSA can be tedious and grueling, and, as seen with other substances, the process can range from four to ten years. However, the exercise is ongoing, and although results may not be shared in time for the 118th Congress, it is to be expected that the issue will be discussed at length in 2023 and beyond.

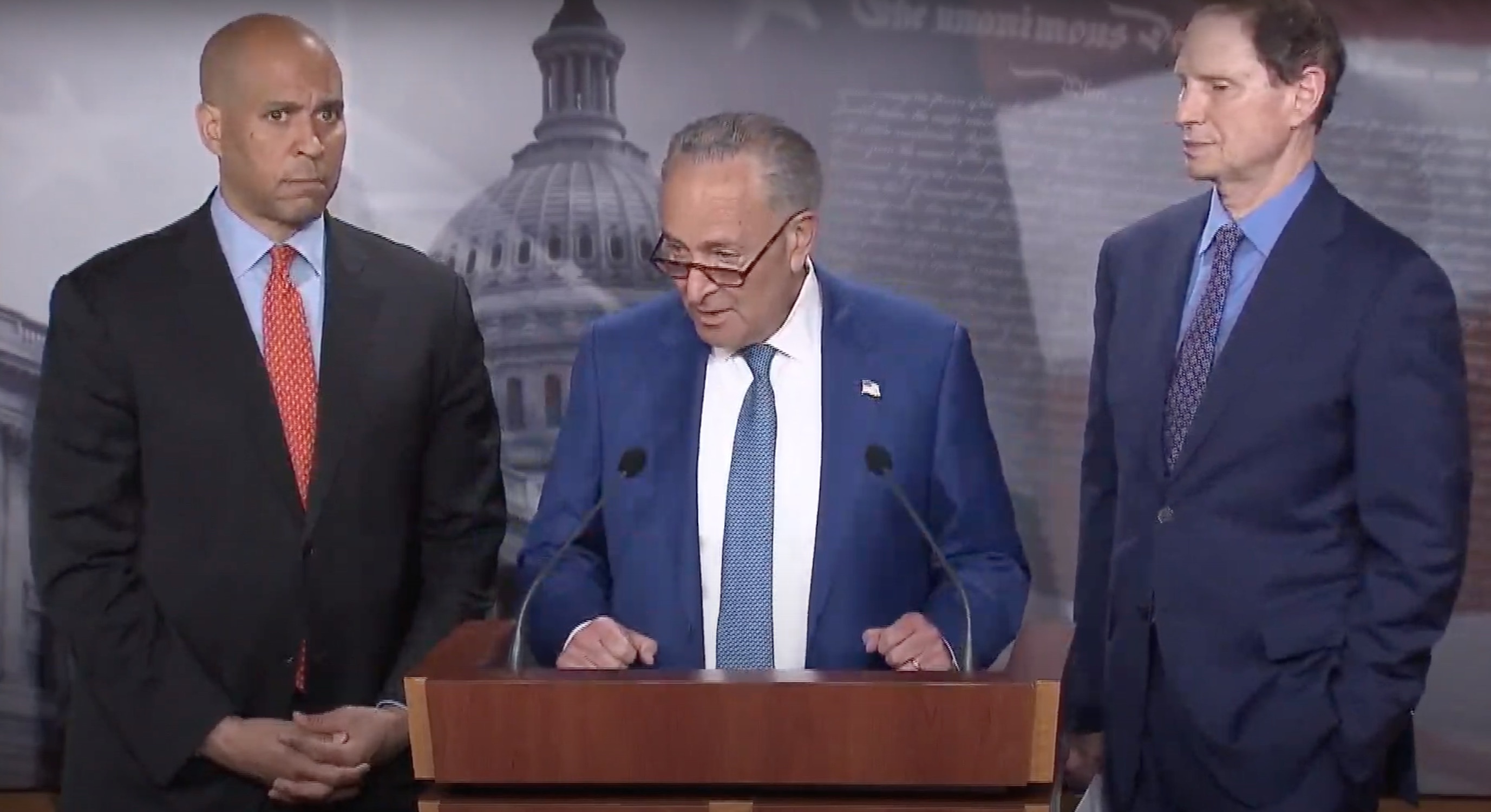

When it comes to legislation, there is no question that Majority Leader Chuck Schumer (D-NY) and Sens. Ron Wyden (D-OR) and Cory Booker (D-NJ) will reintroduce the CAOA in 2023. The comprehensive legislation aims to decriminalize cannabis by removing the drug from the CSA and tackles issues related to research, public safety, restorative justice and equity, taxation and regulation, public health and industry practices.

2. States Reform Act.

Sen. Schumer unveiling the Cannabis Administration and Opportunity Act

Another piece of legislation we anticipate seeing in the 118th Congress is Rep. Nancy Mace’s (R-SC) States Reform Act. Coming from a state without any cannabis laws, the freshman congresswoman introduced a measure that would federally decriminalize cannabis by fully deferring to state powers over prohibition and commercial regulation and regulate cannabis products like alcohol. In 2022, the bill received positive feedback from the industry and dominated the discussions during the Developments in State Cannabis Laws and Bipartisan Cannabis Reforms congressional hearing. With its bold cannabis sponsor, who will now serve as the House Oversight Subcommittee on Civil Rights and Civil Liberties chair, the States Reform Act will undoubtedly take center stage in 2023.

3. MORE Act.

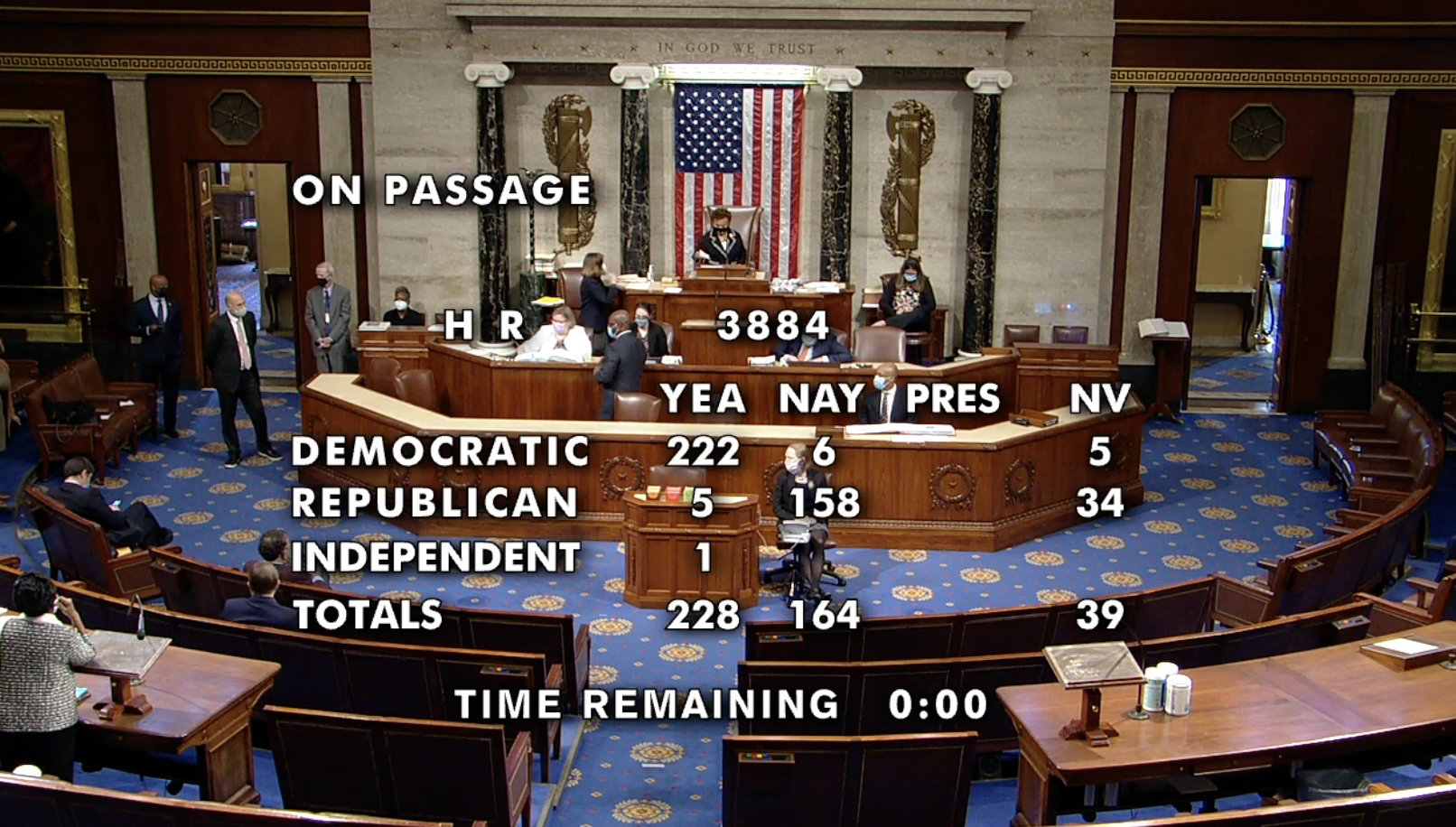

Sponsored by Rep. Jerry Nadler (D-NY), the MORE Act will also be reintroduced in 2023; however, it remains to be seen how much attention the bill will receive. The MORE Act aims to decriminalize cannabis by removing the drug from the CSA and eliminating criminal penalties for anyone who manufactures, distributes or possesses cannabis. In the 117th Congress, Rep. Nadler served as the chair to the House Judiciary Committee and was able to advance his measure through the chamber with ease. But since the House majority has flipped, and Rep. Jim Jordan (R-OH) is likely to serve as the chair, getting the MORE Act to the floor for a vote may be challenging—especially given Rep. Jordan’s opposition to the cannabis sector.

The House passing the MORE Act back in 2020

4. HOPE Act.

The HOPE Act often flies under the radar, but this Republican-sponsored bill made headlines during the 117th Congress. Sponsored by Co-Chair of the Congressional Cannabis Caucus (CCC), Rep. Dave Joyce (OH), the bipartisan legislation aims to help states with expunging cannabis offenses by reducing the financial and administrative burden of such efforts through federal grants. Although it was not considered in the House, the language of the bill was heavily debated by the Senate, particularly toward the end of the year when the chamber was negotiating the final text for end-of-year must-pass packages, like the National Defense Authorization Act (NDAA), the Omnibus and the Continuing Resolution (CR). Alongside the SAFE Banking Act, the HOPE Act was one of the only cannabis bills that had a realistic chance of advancing as part of a larger legislative vehicle, so there is no question that the congressman will reintroduce the measure in the upcoming congressional session.

5. SAFE Banking Act.

And last, but certainly not least, is the most discussed cannabis bill this year: the SAFE Banking Act. The legislation aims to create a safe harbor for financial institutions to provide traditional banking services to cannabis businesses in states that have legalized the drug. It also allows cannabis businesses to access lines of credit, loans and wealth management. It has now passed in the House seven times, with bipartisan support. And although the SAFE Banking Act was debated by the House several times throughout the year, the Senate did not tackle the bill until November. By the time discussions for the bill’s language had taken off, Sen. Booker remained firm that he would only support a cannabis bill if it included criminal justice and social equity reform language. In an attempt to satisfy the senator’s demands, Majority Leader Schumer considered marrying the SAFE Banking Act and the HOPE Act as part of a larger package.

However, and much to the cannabis industry’s detriment, not only was the timeline for those bills a little too late, but Democrats were, unfortunately, unable to fix the money laundering and cash legacy concerns of Sen. Chuck Grassley (R-IA) and other Republicans.

Sen. Cory Booker (D-NJ) Photo: Nick Fisher, Flickr

After attempting to attach the SAFE Banking Act to multiple vehicles, retiring Congressman Ed Perlmutter (D-CO), sponsor of the legislation, and Sen. Schumer were unsuccessful in getting the bill over the finish line. In a final Hail Mary, Sen. Schumer attempted to include the language to the Omnibus, but compounded with the technical assistance report from the Department of Justice (DOJ) and ongoing media flurry, he and the Democratic party yet again came up empty-handed.

The question now is: who will carry the SAFE Banking Act and Rep. Perlmutter’s legacy in 2023? Many will look toward cannabis industry champions like Reps. Joyce, Mace, Earl Blumenauer (D-OR) and Brian Mast (R-FL). However, it would be worth considering other members of the CCC and some of the incoming freshmen, particularly those from a state with legal cannabis laws. It is also entirely possible that Sen. Jeff Merkley (D-OR) finds his own sponsor to carry his companion bill in the House since he has already announced that he looks forward to working on the legislation in the upcoming year. Regardless, it is highly likely that the SAFE Banking Act will be reintroduced in 2023 and considered throughout the year.

6. Other Measures

Other measures that are likely to reappear in 2023 are the Capital Lending and Investment for Marijuana Businesses (CLIMB) Act, Veterans Equal Access Act, the GRAM Act, Common Sense Cannabis Reform for Veterans, Small Businesses and Medical Professionals Act, VA Medicinal Cannabis Research Act and the Homegrown Act. Additionally, the passage of the Medical Marijuana and Cannabidiol Research Expansion Act and the advancement of many of these federal bills have opened the gates for new legislation related to medical and recreational cannabis, research, veterans’ access, financial services, criminal justice reform and social equity, and public health and safety to emerge.

For states with legal cannabis laws, bills related to enhancing the state’s medical or medical and recreational programs, preventing industry oversaturation and price gouging, expanding licensing opportunities, criminal justice reform, youth and advertising protections and impaired driving are likely to be introduced. States where cannabis ballot measures failed will likely see those measures resurface.

The continued growth of legalization across the country is all but inevitable. In the nearer term, the industry will focus on how to remain viable in the face of high taxes and oversupply in 2023. New Congressional leadership could lead to bipartisan cannabis legalization if enough members are willing to rally behind their colleagues who are pushing for cannabis legislation. While the road is long before we will see the full impact from President Biden’s Oct. 6 announcement, the action proves those in power cannot ignore the ever-growing numbers of Americans across party lines and demographics who agree that cannabis use should be legal and regulated.

Like this article and want to see more? Subscribe to our free newsletter here The cannabis industry could receive a significant boost if the recently introduced Capital Lending and Investment for Marijuana Businesses (CLIMB) Act passes Congress. The bipartisan bill was introduced by Rep. Troy A. Carter, Sr., a Democrat from Louisiana, and Rep. Guy Reschenthaler, a Republican from Pennsylvania. It is intended to boost the cannabis industry by creating greater access to capital, banking insurance and other business services. Unlike the SAFE Banking Act (which specifically addresses banking services for the cannabis industry), the CLIMB Act was introduced “to permit access to community development, small business, minority development and any other public or private financial capital sources for investment in and financing or cannabis-related legitimate businesses.”

Rep. Troy A. Carter, Sr.

Currently, the cannabis industry faces a serious dilemma with regard to accessing not only traditional banking services, but also essential capital and financing sources. The latest member of the cannabis bill alphabet soup attempts to remedy this by addressing two key issues.

First, the CLIMB Act would permit access to key “business assistance” programs from various financial institutions by prohibiting any federal agency from bringing any civil, criminal, regulatory or administrative actions against a business or a person simply because they provide “business assistance” to a cannabis state-legal company. The CLIMB Act defines “business assistance” broadly to include, among other things, management consulting work, accounting, real estate services, insurance or surety products, advertising, IT and other communication services, debt or equity capital services, banking or credit card services and other financial services.

This provision of the CLIMB Act would immediately create more access to traditional insurance, lending and credit. This broad protection would not only apply to private entities providing “business assistance,” but arguably means that the U.S. Small Business Administration (SBA) could not be penalized by Congress or another government agency for providing loans to state-legal cannabis companies. Moreover, currently the cannabis industry does not have access to use credit cards, as major credit card companies refuse to permit such transactions. The CLIMB Act could pave the way for major credit card providers to begin permitting cannabis transactions. Permitting the use of major credit cards like American Express, Mastercard and Visa could result in an increase in sales for cannabis retailers.

The second, and possibly the most important, aspect of the CLIMB Act is that it would amend the Securities and Exchange Act of 1934 to create a “safe harbor” for national securities exchanges like Nasdaq and the New York Stock Exchange (NYSE) to list cannabis companies and would permit the trading of these cannabis businesses stock. Currently, plant-touching cannabis companies with operations in the U.S. can only be listed on a Canadian-based exchange and can also only be traded in the U.S. via the over-the-counter (OTC) markets. Trading securities on the OTC markets does not provide the same level of security as securities traded on a national exchange like Nasdaq or NYSE. Specifically, the CLIMB Act delineates that the federal illegality of cannabis is not a bar to listing or trading of securities for legitimate cannabis-related businesses.

Rep. Guy Reschenthaler

This provision of the CLIMB Act has two immediate effects. First, the CLIMB Act would allow for U.S. cannabis companies currently listed in Canada to list on the Nasdaq or NYSE. Second, this provision would allow more traditional, “blue-chip” industry companies currently listed on Nasdaq or the NYSE who haven’t been able to operate within the cannabis industry as a plant-touching entity, to enter the cannabis industry as an active participant.

In announcing the CLIMB Act, Representative Reschenthaler stated that “American cannabis companies are currently restricted from receiving traditional lending and financing, making it difficult to compete with larger, global competitors. The CLIMB Act will eliminate these barriers to entry, and provide state-legal American cannabis companies, including small, minority, and veteran-owned businesses, with access to the financial tools necessary for success.”

It is important to note that the CLIMB Act, like the SAFE Banking Act, only represents one small, but important step toward cannabis reforms. Neither proposal would legalize, de-schedule or reschedule cannabis. Rather, the CLIMB Act addresses very real-world, operational issues facing the cannabis industry. With that in mind, the CLIMB Act would certainly provide much needed clarity for issues facing all cannabis companies.

Passage of the CLIMB Act is not a forgone conclusion, but rather is quite uncertain. Other pieces of cannabis-related legislation, like the SAFE Banking Act, have passed the House of Representatives multiple times without the U.S. Senate taking any action. Moreover, the CLIMB Act was introduced with only two legislative supporters.

The Center for Scientific Cannabinoid Information (CSCI) announced their launch on June 14. In a press release announcing their launch, the non-profit organization says they want to serve as a resource for healthcare professionals, psychologists, doctors, athletic trainers and others looking for information on the safety and efficacy of cannabinoids. The organization is focused on providing current, research-based information on cannabis.

The advisory board for the CSCI includes: Margaret Roche, a dietitian; Dr. Steven Salzman, a surgeon; Dr. George Gavrilos, a pharmacist; Joseph Cachey, an attorney and former hemp executive; Dr. David Kushner, a hospitalist; Dr. Bonni Goldstein, a physician; Dr. Kylie O’Brien, an integrative medicine specialist; and Dr. Jason Canner, an oncologist.

According to Dr. Steven Salzman, who is named as CSCI Chief Medical Officer, their organization will help fill the knowledge void in the healthcare space. “As a physician and practitioner working with cannabinoids, I’ve heard from many other practitioners who have been searching for reliable, evidence-based information on cannabinoids, and realized there was a void,” Says Dr. Salzman. “The CSCI fills this void by serving as a valuable resource where practitioners can access accurate, up-to-date information on CBD and other cannabinoids to help them gain a better understanding of this emerging field.”

The press release says that the organization will compile the latest research and clinical best practices for cannabinoid treatments and share the information with their community. The CSCI invites folks interested in medical cannabinoid research to check out their website and join their community to receive up-to-date scientific information.

By Tamara L. Kolb, Amy Bean, Caitlin Strelioff No Comments

As the legal cannabis market expands, banks and nonbank financial institutions (NBFIs) across the United States continue to explore how to safely provide banking and other financial services to cannabis-related businesses (CRBs) and other CRB ecosystem players. At the same time, these organizations are taking into account changes they might need to consider relative to their Bank Secrecy Act ( BSA), anti-money laundering (AML) and related compliance programs.

Regulatory conundrum

The Controlled Substances Act (CSA) identifies the cannabis plant and all its derivatives as a Schedule 1 controlled substance. Schedule 1 controlled substances have a “high abuse potential with no accepted medical use,” and they cannot be “prescribed, dispensed, or administered.” Because cannabis remains classified as a Schedule 1 controlled substance, the CSA “imposes strict controls on possession, manufacturing, distribution, and dispensing” of cannabis.

Under the Money Laundering Control Act of 1986 (MLCA) and the BSA as amended, covered banks and NBFIs are prohibited from providing financial services to businesses that are engaged in illicit activities. Because federal law prohibits the distribution and sale of cannabis, financial transactions involving CRBs are therefore deemed to be transactions that involve funds derived from illegal activities.

As of Feb. 3, 2022, 18 states, two territories, and the District of Columbia have enacted legislation to regulate cannabis for adult use. Thirty-seven states, the District of Columbia and four territories have approved comprehensive, publicly available medical and cannabis programs. Eleven states allow for the use of low-THC, high-CBD substances for medical reasons in limited situations or as a legal defense.

The growing divide between federal prohibition and state legalization of the cannabis industry creates a precarious position for federally regulated banks and NBFIs with the main concern involving exposure to legal, operational and regulatory risk. The situation begs the question: How might the federal government and regulators pursue and prosecute players in the legal cannabis industry?

The current economic trajectory predicts that retail sales of legal cannabis products in the U.S. will surpass an estimated $41.5 billion annually by 2025, and many banks and NBFIs are eagerly awaiting the federal green light to do business with CRBs without fear of prosecution or legal ramifications.

From 2018 forward, Congress has made several attempts to pass legislation that would protect CRBs when cultivating, distributing, marketing, and selling cannabis products in their state-legalized form. These efforts to declassify cannabis-related activity as a specified unlawful activity have thus far been unsuccessful.

The House passing the MORE Act back in 2020

Passage of the Secure and Fair Enforcement Banking Act of 2021 (SAFE Banking Act) and the Marijuana Opportunity Reinvestment and Expungement Act of 2021 (MORE Act) would enable banks and NBFIs to provide financial services to CRBs. The SAFE Banking Act would provide a safe harbor for banks and NBFIs that provide financial services to CRBs. The MORE Act would deschedule cannabis from the CSA entirely.

Questions to ask

Banks and NBFIs interested in providing financial services to CRBs should ask these questions:

Do we adequately understand our risk, and what are the implications for our organization? How should we augment our risk assessment process and our controls?

To what extent are we willing to accept the risk of banking CRBs? Do we have the ability to identify CRB customers, and if so, do we have any?

How should we advise the board of directors about setting risk appetite?

What customer due diligence (CDD) and enhanced due diligence (EDD) will we need to safely continue with existing customers and onboard new ones?

How will we monitor for unusual and suspicious activity? What will be the alerting and judgmental criteria?

How will our resource needs change so that we stay abreast of new processes and controls?

Risk appetite considerations

In order to determine whether to accept or prohibit CRBs, banks and NBFIs should identify the level of acceptable risk they are willing to take on. Several key components need to be considered, such as:

The board of directors’ stance on legal cannabis, given that good governance recommends and regulators expect that the board sets risk appetite

Cannabis laws in states within the customer footprint and the impact on customers’ communities

Risk profile, customer base, geographic location, products, and services

Relationship with regulators and any recent deficiencies or weaknesses in the BSA and associated compliance programs

Ability to implement appropriate controls and staffing

Developing a strategic road map

If the decision is made to bank CRBs, banks and NBFIs should perform an assessment of compliance maturity for existing BSA/AML program processes and controls to identify potential gaps and develop a strategic road map that helps the organization achieve its vision for future state compliance and sustainable operations.

A well-developed and well-articulated strategic road map visualizes what actions or key outcomes are needed to help organizations achieve their long-term goals. When creating the road map, banks and NBFIs need to demonstrate a keen understanding of their desired strategy, outcomes, markets, and products for onboarding and banking CRB customers. Specifically, banks and NBFIs need to define and explain how desired outcomes and business strategies create risk and exposure.

In addition to a road map, banks and NBFIs should develop and document a detailed risk-based approach that is aligned to the organization’s risk tolerance to determine necessary compliance steps when banking CRB customers.

Specifically, the following activities should be considered when developing a CRB banking program that meets regulatory expectations:

Identifying BSA/AML control gaps related to CRB risk identification and mitigation and formulating a plan to address them

Updating a board-approved policy framework

Updating detailed operating policies and procedures

Planning for capacity, developing job descriptions, and onboarding new personnel

Training for all three lines of defense, senior management, and the board

Developing and documenting a phased or full approach to acceptance of CRB customers

Developing and documenting a CRB program oversight policy

This framework is intended to help banks and NBFIs differentiate types of CRBs and their corresponding risks, and it separates CRBs into three tiers and details risks for each tier. The following exhibit summarizes the approach:

Risk framework by tier

Level

Risk

Tier 1

Direct

Tier 2

Indirect with substantial revenue from Tier 1

Tier 3

Indirect with incidental revenue from Tier 1

Source: CRB Monitor

Even the most conservative of risk appetites equivalent to outright prohibition is not devoid of significant risk considerations. Residual risk frequently encompasses a large number of indirect connections in the total CRB ecosystem. Common examples are printers, lawyers, accountants, landlords, and even utilities and taxing authorities, and all of these are subject to regulatory scrutiny and, importantly, visibility to law enforcement. Also, policies to prohibit or restrict will be audited and examined for compliance, and exceptions will require explanations.

This panorama necessitates expertise and prudence in identifying and evaluating risks within the many layers of CRBs. For example, consider a bank or NBFI that banks a CRB’s employee or vendor. If a bank fails to properly implement controls that would allow it to identify and mitigate risk associated with banking CRBs, it will be susceptible to severe violations of the BSA, including civil money penalties, criminal penalties, and regulatory enforcement actions.

Implementing necessary precautions

A well-developed road map should consider and implement the following activities:

Understanding the most current state and federal cannabis laws and regulations to ensure the bank or NBFI’s compliance

Understanding the local, state, or tribal program to ensure CRB customers are compliant with the program

Implementing a CRB risk assessment

Implementing executive approval practices for direct CRBs

Developing adequate risk ratings (possibly through a risk-based, tiered approach) and corresponding monitoring for CRB customers that includes:

Integrating various customer onboarding and AML solutions at both onboarding and periodic levels

Scheduling regular reviews to include recurring enhanced due diligence, site visits, and transaction monitoring

Monitoring for suspicious activity, including red flags, via open sources for adverse information about the CRB customers and related parties such as beneficial owners

Performing adequate CDD and EDD that will validate that the CRB-offered products, services, and programs are compliant with most current state laws and regulations by:

Collecting appropriate documentation as evidence of compliance, perhaps including a comprehensive onboarding questionnaire, beneficial ownership information, and contracts for the growing, harvesting, transporting and processing of the product

Reviewing applications and supporting documentation used to obtain a legal cannabis state license

Understanding the normal and expected activity of the organization’s CRB customers and their product usage

Developing adequate training programs and governance and oversight programs to address this customer type by:

Updating existing policies and procedures to review inherent risk presented by banking CRB customers

Updating annual training for employees

Auditing initial program design and periodic operational effectiveness

Moving forward cautiously

The ins, outs, and unknowns of cannabis banking are complex, and they require banks and NBFIs to be extremely vigilant with current policy and aware of new developments. Overall, the idea of creating a cannabis program might seem like a daunting task, but with appropriate guidance and care, organizations can provide services in compliance with laws and regulations.

Crowe disclaimer: Qualified organizations only. Independence and regulatory restrictions may apply. Some firm services may not be available to all clients. Given the continued evolution and inconsistency of various state and federal cannabis-related laws, any company should seek competent legal advice relating to its involvement in the cannabis industry, including when considering a potential public offering as a cannabis-related company.

Federal regulations have made compliant credit processing in the cannabis industry difficult to achieve. As a result, most cannabis retailers operate a cash-only model, limiting their ability to upsell customers and placing a burden on customers who might rather use credit. While some dispensaries offer debit, credit or cashless ATM transactions, regulators and traditional payment processors have been cracking down on these offerings as they are often non-compliant with regulations and policies.

Two companies, KindTap Technologies and Aeropay, are addressing the cannabis industry’s payment processing challenges with innovative digital solutions geared towards retailers and consumers.

We interviewed both Cathy Corby Iannuzzelli, president at KindTap Technologies and Daniel Muller, CEO at Aeropay. Cathy co-founded KindTap in 2019 after a career in the banking and payments industries where she launched multiple financial and credit products. Daniel founded AeroPay in 2017 after a career in digital product innovation, most recently at GPShopper (acquired by Financial), where he oversaw the design and development of over 300 web and mobile applications for large scale Fortune 500 companies.

Green: What is the biggest challenge your customers are facing?

Cathy Corby Iannuzzelli, co-founder and president at KindTap Technologies

Iannuzzelli: Our customers include both cannabis retailers and their end consumers. As long as cannabis is illegal at the federal level, normal payment solutions such as debit and credit cards cannot be accepted for cannabis purchases. This has resulted in heavy cash-based sales and unstable, transient work-around ATM payment solutions that can be ripped out with little notice, disrupting the entire business. The lack of a mature payment network to support retail payments for cannabis purchases is a huge challenge for all stakeholders. Cannabis retailers bear the high cost and safety issues of operating a heavily cash-based retail business. Consumers encounter several friction points that require them to change their behavior when purchasing cannabis relative to how they purchase everything else.

Muller: Our cannabis business customers have faced a constantly changing and, frankly, exhausting financial services environment. From the need to move and manage large amounts of cash, to card workarounds, added to the disappointment from legislation around the SAFE Banking Act, these inconsistencies have acted as a roadblock to their potential growth and profitability. Aeropay is in the position to be a stable, long-term, reliable payments partner ready to help them scale their businesses. We believe these opportunities are limitless.

Green: What geographies have got your attention and why?

Daniel Muller, CEO and founder of Aeropay

Iannuzzelli: KindTap’s focus is on the U.S. market where federal policy has created the need for alternatives to traditional payment networks. KindTap is available in every U.S. state where cannabis is legally sold. In terms of our distribution channels, KindTap’s digital payment solution was brought to market during the COVID-19 pandemic when curbside pick-up and delivery became critically important. These channels are where the exchange of cash at pick-up posed the greatest security risk to employees and customers. Our early integrations were with e-commerce platforms focused on delivery and pick-up orders, and our integration partners have strong customer bases in California and the northeast. So, while KindTap can provide its “Pay Later” lines of credit and “Pay Now” bank account solutions anywhere, we have heavier penetration in those regions.

Muller: California, for its established tech culture and how it plays into the cannabis industry – your product simply has to live up to their tech standards to be heard. Also, Chicago, our headquarters, with its newly emerged commitment to financing the cannabis industry and bringing with it a more traditional business approach. In Chicago, you have to have elevated standards of professional practices in any industry you enter. And of course, we love to watch emerging markets like New York and Florida as they head towards adult-use and what shape cannabis and payments will take.

Green: What are the broader industry trends you are following?

Iannuzzelli: We continue to see a strong transition from cash and ATM transactions over to digital payments. Since KindTap has a fully-integrated payment “button” on e-commerce checkout screens, the adoption rate of end consumers to that one-click experience is quite strong. We are also seeing trends of more “express lines” in the retail environment – for those KindTap users who paid online/ahead – and faster/safer delivery experiences to people’s homes since there is no longer the need to collect any payment upon delivery. We are firm believers in the delivery/digital payments combination and a strong increase of that trend as more states allow for delivery.

Muller: The cannabis industry is starting to normalize payments and mirror traditional online and brick-and-mortar. With bank-to-bank (ACH) payments, cannabis businesses can now offer modern customer shopping experiences including pre-payment for delivery orders without the need for a cash exchange at the door, offering the option to buy online pickup in-store and contactless in-store QR scan-to-pay customer experiences. With these familiar and customer-driven options now available, we are seeing widespread adoption, as well as meaningful increases in spend and returning customers.

Green: Thank you both. That concludes the interview!

About KindTap: KindTap Technologies, LLC operates a financial technology platform that offers credit and loyalty-enabled payment solutions for highly-regulated industries typically driven by cash and ATM-based transactions. KindTap offers payment processing and related consumer applications for e-commerce and brick-and-mortar retailers. Founded in 2019, the company is backed by KreditForce LLC plus several strategic investors, with debt capital provided by U.S.-based institutions. Learn more at kindtaptech.com.

About AeroPay: AeroPay is a financial technology company reimagining the way money is moved in exchange for goods and services. Frustrated with the current, antiquated payments landscape, we believe there is a better way to pay and a better way to get paid. AeroPay set out to build a payments platform that works for all- businesses, consumers, and their communities. Learn more at aeropay.com.

Cannabis risks have always outpaced the availability of insurance, in large part because of its status as a federally illegal substance and the dangers in extraction and production. But it now shares many of the same risks as other industries — catastrophic crop damage, cyber risk and a shortage of skilled workers.

With legalization becoming more common, the industry is positioned for enormous growth despite these challenges. However, enterprises that will benefit the most are those best positioned to manage risk.

Here are four obstacles to growth in the industry in 2022 and how enterprises can combat them:

Cybercrime will be the top manufacturing risk

Both cybercrime and cannabis have experienced major booms since the start of the COVID-19 pandemic. Cannabis companies watched as healthcare and pharmaceutical organizations were hit hard by cybercriminals in 2020, and now the threat could be headed their way.

For retailers, the vulnerability often lies in their POS tech

For cannabis retailers, the vulnerability lies in their dependence on point-of-sale tech, while the threat for cultivators exists within their strong use of intelligent automation to manage the grow environment. Across the industry, the lack of sophisticated IT security systems is like a beacon for bad actors.

Nearly 60% of cannabis businesses say they haven’t taken the necessary steps to prevent cyberattack, but the winds are changing. Due to these concerns and the growing attention on cybercrime in the industry, cyber coverage is expected to rise 30% or more in 2022, which puts the onus on risk management practices that will help prevent cyberattacks and ensure coverage from insurers concerned about risk.

Barriers to business growth may result in more M&A

As of summer 2021, 18 U.S. states have legalized adult use and 37 states have legalized medical cannabis.

While this is opening opportunities for many cannabis businesses, the U.S. remains a complicated market. Federal regulations continue to hinder even more cannabis industry growth by restricting lending to the industry from traditional banking and financial institutions. While it’s not illegal to do service with the cannabis industry, many institutions stay away due to its high risk.

Smaller cannabis companies are impacted most heavily by this barrier and await passage of the Secure and Fair Enforcement (SAFE) Banking and Clarifying Law Around Insurance of Marijuana (CLAIM) Acts to allow easier access to capital. Together, these two acts of legislation will provide guidelines on how to work lawfully with legal cannabis businesses and prohibit penalizing or discouraging institutions from working with them.

In the meantime, M&A activity is expected to increase in 2022 as large cannabis businesses have the means to access capital and acquire these small companies. This includes Canadian cannabis companies, unburdened by federal restrictions, who are expected to increase their cross-border mergers and acquisitions.

Severe weather isn’t easing up

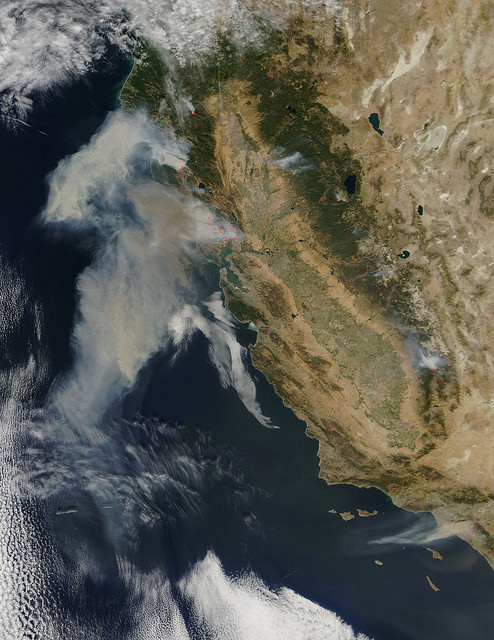

Extreme natural catastrophes are no longer rare, and they have only added greater uncertainty to the industry which has always had difficulties securing crop insurance.

NASA’s Aqua satellite took this picture of the smoke over California in 2017 Photo: NASA

For example, policies that transfer wind and hurricane damage risk in Florida or wildfire and smoke taint in California are virtually non-existent for cannabis — and for outdoor growers, a single weather event can wipe out an entire crop with no recourse.

One possible solution for cannabis companies that cannot secure traditional crop insurance is parametric insurance, which pays out in full when a weather element reaches a threshold, regardless of the actual damage.

Growers with indoor operations, or those considering moving that way, must cope with energy conservation initiatives. Measures like the one in California that would require indoor growers to use LED lighting by 2023 could cost the industry millions and present a direct threat to small operations’ viability. This makes it important for cannabis producers to institute conservation measures and undertake risk mitigation measures like improved safety measures at indoor growth facilities ahead of 2022 renewals.

As a continually emerging market, cannabis risks are great. Adding to these pressures is the growing impacts of climate change and cybercrime raising the bar even further. Growth for the cannabis industry in 2022 will depend upon strong risk management solutions and the ability for cannabis companies to implement them.

Social consumption lounges are becoming increasingly popular in legal cannabis markets. Just what are social consumption lounges? They’re a safe, enclosed space where cannabis consumers of legal age can come together and enjoy cannabis products, much like a bar environment for consuming alcoholic beverages.

Social consumption lounges are particularly attractive for their potential to bring in cannabis tourists. Although adult use cannabis can help promote tourism, tourists typically can’t smoke in most places indoors (including their hotel accommodations) nor consume on the street or in public, due to strict public consumption rules set by state regulations. This leaves the perfect set-up for consumption lounges, which provide the appropriate and legal environment for tourists to consume cannabis.

What do social consumption lounges look like in practice? What are the rules and regulations that social consumption lounges must adhere to? How and where are social consumption lounges currently legal in the United States? Here’s what you need to know.

What are social consumption lounges?

Social consumption lounges—also known as consumption lounges, cannabis lounges, cannabis consumption area and cannabis consumption lounges—are retail lounges that permit on-site cannabis consumption, such as smoking and vaping cannabis flower as well as ingesting cannabis infused products like edibles and tinctures. Similar to a bar that serves alcoholic beverages, all consumers in a cannabis lounge must be at least 21 years of age. While smoking typically isn’t permitted in retail businesses, smoking is permitted in lounges.

Mellow Yellow in Amsterdam

While state-specific regulatory bodies are responsible for developing, implementing and enforcing the rules surrounding U.S. social consumption lounges, Dutch “coffee shops” may have served as the inspiration and model for U.S. industry. Contrary to the name “coffee shops”, patrons don’t go to Dutch coffee shops for coffee. Rather, they go because the sale and consumption (including smoking) of cannabis is permitted and socially accepted. According to travel resource Amsterdam.info, Dutch coffee shop culture emerged in the 1970s when the federal government made a clear legal distinction between “hard” and “soft” drugs. Soon after in 1972, the first coffee shop named Mellow Yellow opened. Although cannabis wasn’t clearly legal or illegal, Dutch law enforcement tolerated the growing number of cannabis coffee shops, focusing instead on prosecuting heroin and lethal illicit substances. Today, the Amsterdam City Council permits coffee shops to operate after they obtain a non-transferable license, which must be displayed in shop windows, thanks to an agreement with the coffee shop union Bond van Cannabis Detaillisten (BCD).

Unlike Dutch coffee shops, U.S. social consumption lounges must adhere to numerous rules and regulations specific to their state and municipality. One major difference is who is permitted to own and operate a lounge. In some U.S. states, consumption lounges are operated by existing cannabis businesses, such as adult use and medical dispensaries. In these cases, the lounge may be required to be on the cannabis business’s existing premises. In New Jersey, this must be an “indoor structurally enclosed area of the cannabis retailer or medical cannabis dispensary that is separate from the retail sales or medical dispensary area” or “an exterior structure on the same premises as the cannabis retailer or medical dispensary, either separate from or connected to the cannabis retailer or medical dispensary,” according to the National Law Review. In many places within the U.S., “stand alone” lounges that aren’t attached to an existing cannabis business aren’t permitted.

In the Netherlands, coffee shops operate in a legal grey area with their products being supplied by an entirely underground cultivation market. Cannabis being consumed in coffee shops isn’t regulated or checked. Per regulations in the U.S. states that allow them, however, only legal cannabis may be consumed in these lounges. While consumers might be able to bring their own cannabis or cannabis products, consuming any cannabis or cannabis products obtained through the underground market is strictly prohibited.

Where are social consumption lounges legal?

The Barbary Coast lounge in San Francisco

Not all U.S. states with legal recreational, adult-, or personal-use cannabis programs permit social consumption lounges. Although it’s been a decade since Colorado and Washington voted in favor of legalization, consumption lounges are a fairly recent trend, likely because states without legal consumption spaces found out the hard way that they couldn’t accommodate tourists or anyone who wished to consume cannabis outside of their home. Here’s where social consumption lounges are legal in the U.S.:

Nevada: After the Governor signed a bill in June 2021, a new cannabis law permitting social consumption lounges went into effect in October 2021 and lounges are anticipated to open in early 2022, according to Nevada public radio station KNPR. Additionally, efforts are being made to prioritize minority-owned business owners of consumption lounges, reports local news station Fox5 KVVU-TV.

New Jersey: Although consumption lounges weren’t initially permitted in the recent regulatory framework, individual municipalities now decide whether or not to permit lounges within their communities. Atlantic City and Jersey City have approved social consumption lounges, reports Hudson County View.

New York: The state’s recently passed adult use cannabis law allows social consumption lounges, but the recreational market isn’t expected to take off until mid-2023, according to Business Insider. Lawmakers still need to adopt a regulatory framework to how lounges (along with other cannabis businesses) will operate.

Illinois: Currently, two social consumption lounges have opened, and two others are planned to open across the state,” says the Chicago Tribune.

Colorado: Similar to New Jersey, individual municipalities decide whether to permit lounges in their communities. Denver and Aurora have approved consumption lounges.

California: Given the state’s rich history of an underground market, informal social consumption lounges aren’t particularly new. However, a recently approved law officially allows social consumption lounges, reports Marijuana Moment.

The number of states considering and/or permitting social consumption lounges is growing. Which states will likely legalize them next? As noted below, it looks like Michigan, Massachusetts and Maine will be next.

Michigan: The state doesn’t allow for them now, but they could come in the future, reports WZZM13.

Massachusetts: The state is considering them, reports Boston.com.

Maine: The state delayed them until 2023, according to MJ Biz Daily.

Why are social consumption lounges becoming increasingly popular?

Consumption lounges are becoming increasingly popular for many reasons. First and foremost, they’re a win for the cannabis industry because they provide consumers with a physical place to consume safely and legally.

The Original Cannabis Cafe by Lowell Farms in West Hollywood

Second, the tourism sector benefits from social consumption lounges. “The problem is people can buy marijuana products in states that have legalized adult-use cannabis, but they have limited options when they want to consume the cannabis that they purchase legally,” explains Cannabiz Media. For instance, Las Vegas has promoted itself as a cannabis travel destination since 2017, despite lack of adequate space for visitors to consume. Meanwhile, those who don’t consume cannabis have criticized the city for its growing public consumption, complaining especially about the odor of smoked cannabis. Social consumption lounges can potentially help fix these growing pains in the state’s cannabis market.

Additionally, lounges are a win for harm reduction. Lounges provide beginner cannabis consumers the opportunity to consume alongside experts, to be shown the ropes with professionals present. Being in a community with experienced consumers provides opportunities for novices to understand how to smoke, dose and overall consume properly and safely.

Lastly, MG Magazine emphasizes other benefits including de-stigmatization, social connection, industry partnerships and product innovation.

Regulation and compliance differences between states

Without federal cannabis legalization, states are tasked with regulating their own cannabis markets. Likewise, state regulatory agencies are responsible for drafting regulations for social consumption lounges.

California and Colorado have fewer limitations, likely because both states have more experience and overall comfort with the plant. In states with more lenient regulations, 420-friendly cafes, hotels, bus tours, paint nights and other businesses are tolerated.

New Jersey has notably strict regulations for social consumption lounges. For example, the current state law doesn’t permit any stand-alone consumption spaces independent of existing permitted cannabis businesses. Therefore, a cannabis cafe or bud and breakfast isn’t permitted.

There is, however, one legal loophole in New Jersey for stand-alone consumption space. The microbusiness license model allows for temporary licenses, permitting a temporary social consumption lounge, such as for an event at a private venue. New Jersey permits them in Newark, Hoboken, Highland Park, Jersey City,Elizabeth, Long Branch Atlantic City and Trenton.

In closing, it is likely that social consumption lounges will become increasingly common especially in major U.S. cities with legal adult-use cannabis programs. While Dutch coffee shops may have inspired the emerging U.S. social consumption lounge model, their U.S. counterparts must comply with much stricter rules and regulations. Since regulations vary from state to state, it’s important to be on top of your state’s policies in order to stay compliant.

Two decades ago, California became the first state to legalize the medical use of cannabis. In 2021, medical use of cannabis is legal is 36 US states, and 17 states allow adult (‘recreational’) use. This trend of rapid legalization of the cannabis industry, while encouraging for industry growth, attracts more attention from federal regulatory bodies such as the Occupational Safety and Health Administration (OSHA). Following a number of incidents and near misses, cannabis facilities have been increasingly frequented by OSHA visits, leading to a spike in citations and fines. A review of past OSHA citations reveals that the most common citations in the cannabis industry pertains to the employer’s lack of awareness about the hazardous nature of some operations and materials handled in the facility. This leads to an absence of a formal fire prevention plan, lack of proper hazardous chemical training, deficiency in proper documentation related to workplace injury and limited evaluation of required personal protective equipment (PPE).1

Cannabis industry data suggests that as of today, an incident is often followed by an OSHA inspection. This naturally leads to the facility asking, ‘How do we prepare for an OSHA inspection and prevent future citations?’ The answer is a combination of identifying and mitigating risks in advance to avoid incidents and developing management systems that support the identification and risk mitigation efforts. Recent collaboration between cannabis business owners and organizations that write codes and standards have provided a framework in which to address the industry’s unique safety challenges to help reduce inherent risk to a facility. These codes and standards typically impact building construction/safety features and operation of the facility, however, additional risk mitigation can be drawn from the best practices already in place in process industries with similar hazards. These process industries have embraced process safety management (PSM) programs, which are built around principles flexible enough to be successfully implemented in the cannabis industry. Adopting such programs will serve the dual purpose of improving the overall safety record of the cannabis industry while enhancing company sustainability2 and help avoid events that lead to OSHA citations.

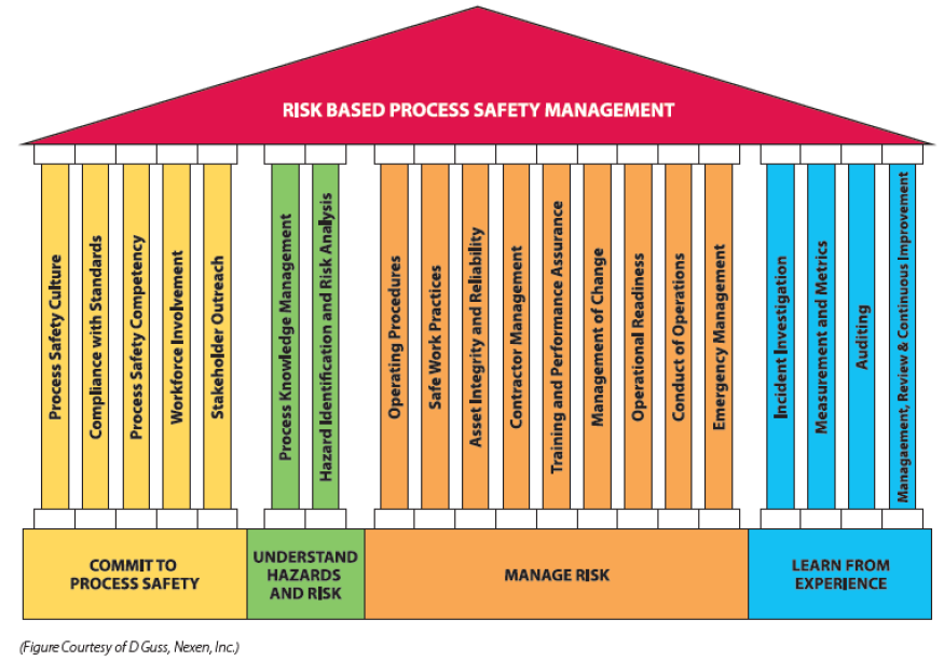

Figure 1. Risk Based Process Safety Management System

The risk-based process safety (RBPS) approach developed by the Center for Chemical Process Safety (CCPS)3 may prove to be the most effective framework to implement PSM programs in the cannabis industry. Unlike the prescriptive regulatory approach provided by OSHA 29 CFR 1910.119, the RBPS methodology recognizes that not all hazards and risks are equal. By assessing risk, an organization can develop an effective management system that will prioritize allocation of limited resources to address the highest risks. Figure 1 shows the four foundational blocks (pillars) of RBPS and the various elements that make up each pillar.

If a cannabis business owner were to develop programs on each of the pillars presented in Figure 1, a comprehensive safety program would be in place that delivers sustainable risk reduction and mitigation. However, as with any industry, the elements can be prioritized and tackled over time, starting with the elements having the most influence on the overall safety of a given facility. For example, a given facility may have great procedures and practices, but may not consistently train or instill employee knowledge or competency. Conversely, a facility may have personnel with great knowledge of hazards and risks, but are less developed with regard to documenting procedures, safe practices or training for new hires. Focusing available resources on the less developed elements will lead to an overall improvement in facility risk, leading to a lower likelihood of an incident and OSHA inspection.

Figure 2. Still image from surveillance video of an explosion at New MexiCann Natural Medicine in July 2015.

As with any industry, positive and negative public perception is driven by the media, which tends to focus on attention-grabbing headlines. The majority of past incidents reported in the news for the cannabis industry were explosions that occurred during the extraction process. One such extraction explosion, shown in Figure 2, occurred in July 2015 at the New MexiCann Natural Medicine facility in Santa Fe, New Mexico. With a focus on the ‘hazard identification and risk analysis’ pillar of RBPS, future such events may be mitigated.

Of the twenty RBPS elements, hazard identification and risk analysis (HIRA) stands out as having the highest potential for immediate impact on the cannabis industry’s safety profile.

HIRA is a collection of activities carried out through the life cycle of a facility to ensure that the risks to employees and the public are constantly monitored to be within an organization’s risk tolerance. The four major areas to analyze are:

Hazards – What are the possible deviations from the design intent?

Consequences – What are the worst possible consequences (or severity) if any deviation occurs?

Safeguards – Are there safeguards in the system to reduce the likelihood of this event?

Risk – Is the risk within the tolerable level? If not, what steps are needed to reduce the risk? (Severity X Likelihood = Risk)

Figure 3. A simplified HIRA flow chart for an Extraction Process

Let us consider an example case where the extraction process utilizes propane or butane as the extracting solvent. Figure 3 shows a simplified HIRA flow chart for the extraction process.

This systematic approach helps to understand the hazards and evaluate the associated risk. In addition, this approach highlights operator training as a crucial safeguard that can be credited to lower the overall risk of the extraction facility. Remember, lack of proper safety training (another element!) is one of the most cited OSHA violations in the cannabis industry. Another advantage to the HIRA methodology is that other safeguards that may be present can be identified, their effectiveness evaluated and additional risk reduction measures may be recognized. This will help business owners allocate their limited resources on the critical safeguards that provide the greatest risk reduction. Identifying, analyzing and solving for potential hazards is a key step in safe operation of a facility and avoiding OSHA citations.

While this article discusses only a single RBPS element, this example demonstrates how best practices from process industries can become a powerful tool for use in the cannabis industry. The “hazard identification and risk analysis” element of the RBPS approach is pertinent not only for the extraction process as discussed above, but also directly applicable to other aspects of the industry (e.g., dust explosions in harvesting and processing facilities, toxic impacts from fertilizers, hazards from the CO2 enrichment process in growing facilities, etc.).

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

We use tracking pixels that set your arrival time at our website, this is used as part of our anti-spam and security measures. Disabling this tracking pixel would disable some of our security measures, and is therefore considered necessary for the safe operation of the website. This tracking pixel is cleared from your system when you delete files in your history.

We also use cookies to store your preferences regarding the setting of 3rd Party Cookies.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.

With markets across the country maturing at a rapid rate, change is a constant. Cannabis companies operating in new markets need to maintain compliance while focusing on their business plan, which can be a difficult task. We sat down with Nick Murer to learn more about compliance issues that cannabis businesses face, like workers comp, payroll taxes, insurance and how outsourcing some HR functions can help.

With markets across the country maturing at a rapid rate, change is a constant. Cannabis companies operating in new markets need to maintain compliance while focusing on their business plan, which can be a difficult task. We sat down with Nick Murer to learn more about compliance issues that cannabis businesses face, like workers comp, payroll taxes, insurance and how outsourcing some HR functions can help. About Nicholas Murer

About Nicholas Murer