Here we are again, crossing our fingers, hoping that the Senate will approve the passage of the Secure and Fair Enforcement Banking Act (SAFE Banking Act). This Act would provide banks with regulatory protections, allowing them to offer critical financial services to cannabis businesses without risking the loss of their banking charter.

As the 2024 elections loom, the stakes have never been higher for passing the SAFE Banking Act.

Cannabis Legalization is On the Rise

As of August 2023, 40 states, four territories and the District of Columbia have legalized medical or adult use cannabis. While some states have moved more slowly, the entire West Coast (including Nevada and Colorado) has voted to pass laws allowing the sale and purchase of adult use cannabis. Most of the East Coast has followed suit; New York, Pennsylvania, New Jersey and Massachusetts have all voted to regulate cannabis. It has become evident that the majority of U.S. citizens are now comfortable with legalized cannabis (156 million people live in jurisdicitons that have legalized adult use).

Banking Roadblocks for the Cannabis Industry

Under current federal policy, banks and other large financial institutions face regulatory restrictions that make it challenging to provide the most basic services to local cannabis companies, regional cannabusinesses and MSOs (Multi-State Operators).

Federal anti-money laundering laws and related record-keeping regulations, such as the Bank Secrecy Act (BSA), have presented complex compliance protocols that prevent banks from meeting the business needs of local growers, manufacturers and dispensaries. Local cannabis business owners are therefore put in a difficult position, as they must balance daily business activity against the potential dangers of operating as a cash-only business.

Federal anti-money laundering laws and related record-keeping regulations, such as the Bank Secrecy Act (BSA), have presented complex compliance protocols that prevent banks from meeting the business needs of local growers, manufacturers and dispensaries. Local cannabis business owners are therefore put in a difficult position, as they must balance daily business activity against the potential dangers of operating as a cash-only business.

How Would the SAFE Banking Act Help Banks Serve the Cannabis Industry?

The proposed SAFE Banking Act would protect banks from federal penalties for offering their services to cannabis businesses in states with regulated cannabis industries. Critically, the bill would shield banks from losing their deposit insurance. Without reform through the SAFE Banking Act, financial institutions will remain essentially prohibited from working directly with legal cannabis companies.

What Will It Take to Pass the SAFE Banking Act?

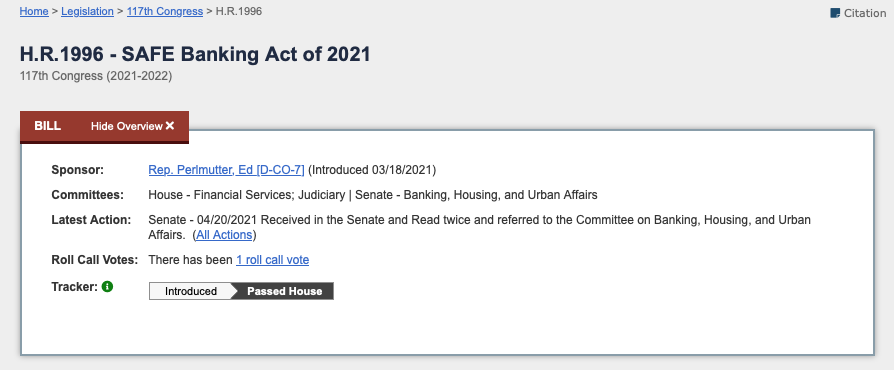

While the bill has successfully passed in the House of Representatives seven times, it has yet to pass in the Senate. Considering the current political climate, the clock is ticking to finally pass the SAFE Banking Act in the Senate.

Policymakers may need to introduce the Act as a stand-alone bill that outlines clear objectives and specifically addresses the issue from a public safety perspective. Cannabis is a hot-button issue, so adding additional legislation will muddy the water and make it easier for Senate members on the fence to vote against the bill.

Policymakers may need to introduce the Act as a stand-alone bill that outlines clear objectives and specifically addresses the issue from a public safety perspective. Cannabis is a hot-button issue, so adding additional legislation will muddy the water and make it easier for Senate members on the fence to vote against the bill.

Cannabis industry representatives and political allies must be strategic in navigating the bill’s potential passage and take the process step by step. First, the SAFE Banking Act must pass to allow cannabis businesses the opportunity to stabilize, grow and prosper. As the sector grows stronger and more accepted by mainstream America, more progressive bills can be introduced and will have a greater chance of successful passage in the House and Senate.

The SAFE Banking Act is an Issue of Public Safety

Every day the Senate chooses to sit on their hands, they put more Americans in harm’s way. This is unacceptable.

Because dispensaries and other cannabis businesses must process daily transactions without basic banking services, they often accumulate large amounts of cash. Dispensaries are, therefore, frequent targets for criminals. Even as the cannabis industry matures and contributes significant tax dollars to State coffers, banks and financial institutions have no choice but to sit with their hands tied, watching with horror as organized criminals literally take aim at dispensary staff.

The passage of the SAFE Banking Act is literally life and death for many cannabis industry employees. How many workers and customers must suffer harm before the Senate wakes up and passes this critical bill? Regardless of their stance on cannabis, members of the Senate must do their jobs, heed the will of the American people and pass the SAFE Banking Act to rectify this increasingly dangerous situation for the good of their constituents.