In the most unexpected development to hit the cannabis industry in years, the U.S. Department of Health and Human Services’ (HHS) Secretary Xavier Becerra shared his agency’s recommendation that, based on data and scientific analysis, cannabis, a Schedule I drug under the Controlled Substances Act, should be reclassified as a Schedule III drug. The announcement was made on Wednesday, August 30.

The Background

HHS’ conclusion was sent by letter to the Drug Enforcement Administration (DEA), the agency with authority to reclassify how various substances are treated under federal drug laws. The HHS recommendation means that the nation’s top health agency no longer considers cannabis a drug that lacks medical value and carries the high potential for abuse.

The announcement comes just under a year after President Biden and his administration made a statement on cannabis reform. In that statement, which he made on Oct. 6, the president requested that the Secretary of HHS and the Attorney General (AG) initiate an administrative process to review how cannabis is scheduled under federal law, in addition to pledging to pardon all prior federal offenses of simple cannabis possession, directing the AG to develop an administrative process for the pardons and urging all governors to follow suit for state and local offenses. In a statement, Secretary Becerra said the agency acted “expeditiously” and completed the rescheduling process in less than 11 months, “reflecting the department’s collaboration and leadership to ensure that a comprehensive scientific evaluation be completed.” Indeed, the agency’s announcement reflects the administration’s desire to quickly resolve the country’s failed approach to cannabis reform, as prior rescheduling efforts have taken years. Few thought the federal government would move quickly on cannabis, let alone under a year.

The White House has chosen not to comment on the HHS recommendation as the “administrative process is an independent process led by HHS and DOJ and guided by the evidence.” During a press conference, White House Press Secretary Karine Jean-Pierre reiterated the administration’s position, saying that the administration is taking a more hands-off approach and allowing the federal agencies to determine cannabis’s classification without political influence.

What Does This Mean for the Cannabis Industry?

Although a historic announcement, many industry members hoped for a report that would completely remove cannabis from the CSA. Rescheduling cannabis as a Schedule III drug could provide a route for the FDA to assume a more hands-on regulatory role, and it could open up opportunities for interstate commerce in cannabis. A Schedule III designation does not amount to federal legalization, which means the industry will continue to lack a comprehensive regulatory framework addressing the conflicts between federal and state cannabis laws. Rescheduling cannabis also does not address long-overdue concerns about decriminalization and the effect the war on drugs has had on incarceration rates and racial disparities among the imprisoned.

With the HHS recommendation out in the open and the ball firmly in the DEA’s court, concerns have shifted to the DEA’s timeline for considering rescheduling. No hard deadline exists for the agency to complete its review, and industry stakeholders already know that the rescheduling process can be grueling and lengthy. The last time the DEA rescheduled a drug, hydrocodone combination products (HCPs) in 2004, the process took nearly a decade. In fact, each time the DEA has previously considered rescheduling cannabis, in 2001 and 2006, the process took over two years and resulted in no changes.

While many stakeholders speculate that a decision will be made ahead of the November 2024 presidential election, others remain skeptical given the strict anti-drug posture hardwired into how the DEA operates. In fact, the HHS recommendation coupled with the DEA’s approach to drug policy has led some to speculate that the DEA may compromise by moving cannabis into Schedule II, a category reserved for medicines with high potential for abuse and dependence, including most common opioids.

Either way, the agency’s recommendation is a momentous moment for an industry that has been reeling from falling sales and rising costs. Rescheduling cannabis could open the floodgates to more and better research into cannabis. The Schedule I designation has severely limited scientists’ access to cannabis for research purposes. A Schedule III designation would also have a significant financial impact on cannabis companies that have been deprived of tax deductions and banking services on which most companies depend.

The DEA has confirmed that it received the HHS letter and recommendation and will initiate its five-factor review, which differs from HHS’s eight-factor criteria. It remains to be seen what the DEA will do or when it will be done, but thousands of cannabis companies across the country will be watching closely.

Massively promising news for the cannabis industry today that many are calling historic: the Department of Health and Human Services (HHS) has sent a letter to the Drug Enforcement Administration (DEA), recommending that cannabis be rescheduled from Schedule I to Schedule III. The news was originally reported by Bloomberg, but further expanded on (and without a paywall we’ll add) by Marijuana Moment with comments from the DEA, HHS and the White House.

Many cannabis stocks across the market saw significant spikes in trading prices following the news of the recommendation. Industry stakeholders and trade organizations seem to share a similar sentiment across the board: Not quite exuberance and celebration, but cautious optimism. The move doesn’t mean the federal government is legalizing cannabis, but they are showing their willingness to work with the industry.

The current Schedule I status of cannabis means the DEA and the federal government see no medical value in it and a high potential for abuse, grouping it with heroin and cocaine. Moving it to Schedule III would mean the opposite, that they recognize cannabis does have medical value and does not have a high potential for abuse, which would put cannabis in the same classification as ketamine, testosterone and Tylenol with codeine.

Importantly, the move would remove the dreaded 280E tax burden that has plagued the cannabis industry with huge tax penalties. It would also lift many barriers to study cannabis that have hindered research for decades.

Last year, President Biden asked HHS to review the scheduling of cannabis, and this recommendation letter to the DEA appears to be the culmination of their review. It is only a recommendation and nothing happens instantly. The DEA still has to decide if they choose to reschedule cannabis.

Out of all the quotes and statements flooding the cannabis media today, Rep. Earl Blumenauer (D-OR) best summarized the feelings shared by many folks in the industry: “This is a step in the right direction but it is not sufficient. I hope it is followed by more significant reforms. This is long overdue.”

As the former CEO of Partner Colorado Credit Union (PCCU), Sundie Seefried has been in the credit union space for 39 years. Established in 2015, Safe Harbor Financial is now a leading provider for banking and financial services in the cannabis industry.

Seefried founded Safe Harbor as a cannabis banking program for PCCU, and since then it has withstood scrutiny of 16 separate federal and state exams. Entering its ninth year as a cannabis banking program, they have almost 600 accounts in 20 states and have processed over $14 billion in transactions for the cannabis market. In September, Safe Harbor began trading on Nasdaq under the symbol SHFS. The company has also announced a definitive agreement to acquire Abaca, an industry-leading cannabis financial technology platform.

Seefried has seen it all in the cannabis banking world. We wanted to get her thoughts on some current events, the future of cannabis banking and lending, and what the next few years might hold in store for an industry ready to grow.

Cannabis Industry Journal:Tell us a bit about yourself. What is your background and how did you find yourself in the cannabis industry? How did you get to become president and CEO of SHF?

Sundie Seefried, President & CEO of Safe Harbor Financial

Sundie Seefried: I’ve been in banking in the credit union space since 1983. I became CEO of Partner Colorado Credit Union in 2001 and stayed there for 21 years. Everything I do, I have a very conservative nature just from being in the banking world and doing things methodically and building good foundations that endure long term. In 2014 when FinCen issued guidance, I was supposed to retire, and I had dinner with some old friends that were attorneys who couldn’t get bank accounts for their clients in the cannabis industry. They asked me to help and I looked into it for them. I assumed the regulator would shut me down but he didn’t; he actually encouraged me to move forward and look further into things. As I educated the board, we saw just how unsafe Colorado was and the serious need for the community to figure things out with respect to banking and cannabis. Coming from that credit union perspective, I said I think we can do this, let’s try and I’ll go through the third parties necessary. And that’s how we got into this, just looking to try and help solve Colorado’s problems and get banking access for cannabis companies.

CIJ: Tell me about your company’s mission. What is your financing strategy in cannabis and of the companies you do business with, what do you look for most?

Seefried: Our mission remains the same, and that is to normalize banking in the cannabis industry as much as possible. Because the black market still exists, the issue becomes sorting the legal entities out from the illicit actors in the industry. We know that the illicit market is trying to hide amongst the legal environment, which really makes things difficult for upstanding cannabis businesses. We can normalize banking by making sure we help legitimize the compliant entities and sort out the bad actors. We really only want to work with legitimate players with licenses, who are fulfilling expectations on the regulatory level and have no problems with compliance. We have been able to do that on the depository side.

We have always been a low-cost provider and our clients count on that. As we move into the lending part of the industry, we’re looking to do the same thing. There are lenders who charge one-to-three percent per month, 18 to 36 percent per year. We, on the other hand, are targeting more of an eight to thirteen percent annual rate. More of a conservative approach. Real debt underwriting. No extremely high interest rates. We look for the collateral, we look for well-organized businesses and solid documentation. Those are the businesses we are trying to bring into the fold and offer them normal loans. Cannabis will always have a premium on it simply because it is illegal at the federal level and there are additional hoops we have to jump through. Because of the potential forfeiture and seizure, if there are bad actors, etc., it really behooves any clients coming to us to also place their depositary services with us so we can prove their legitimacy and provide loans to them.

CIJ: Let’s talk about the Canopy Growth news. They announced they are pulling the trigger on acquiring Wana Brands, Acreage Holdings and Jetty Extracts, under the Canopy USA holding company and ahead of federal legalization. On the surface, it looks like they are bypassing a lot of the hurdles American cannabis companies currently face with financial red tape. As a foreign company trading on the NASDAQ dealing with a schedule 1 substance, do you expect Canopy to have a significant, some would say unfair, competitive advantage with their early entry? Or is this perhaps more of a rising tide lifting all boats scenario? What effect will this have on the current market landscape?

Seefried: I find it a very interesting move on their part. Certainly, they have a big advantage in comparison to other companies. The consolidation in the industry is moving so quickly. Other players will keep up with this just as fast as Canopy is moving in. That’s my opinion in terms of what I see in the consolidation area of the market. I think what it really hurts is small businesses. My heart goes out to them. So many of them worked so many years to build excellent small companies with boutique shops, and this whole move will really change that part of the industry.

I see a lot of these small players, non-vertically integrated companies, being impacted in a negative way due to such mass consolidation and the entry of foreign businesses. We need to get more competitive on a global level in order for our companies to grow and thrive. This happened back in 2018, when so many companies started doing those reverse takeovers onto the Canadian Securities Exchange and suddenly, they were putting tens of millions of dollars into the U.S. market. People didn’t see that as a competitive disadvantage for American companies, but now this move by Canopy may really show that we have to look at things more globally.

CIJ: Biden’s announcement regarding the scheduling review for cannabis has a lot of industry folks very hopeful that federal legalization is closer to a reality than before. Do you share their optimism?

Seefried: Closer than before, yes. But how close? I am not convinced it will happen quickly. If they are really going to consider rescheduling or descheduling, everything happens in Washington very incrementally. Eight years and seven attempts at the SAFE Banking legislation and still no movement on that front. Tomorrow, we’re going straight to legalization? I have a hard time swallowing that one. I just don’t see that big of a jump all at once. I think it is interesting coming just before the midterms and votes are really needed now more than ever.

What Biden did was a great start. Especially for those people in prison for possession. The interesting part of it is, we are very serious about people who have used it, but the people who have sold it and are in prison might be in the same situation. Given how the laws worked for so long, just based on the amount of cannabis you had could get you automatically labeled as a dealer, which isn’t the case for a lot of incarcerated folks.

The fact is, the social equity and justice issue, who do you free or who do you not free from prison, is a very difficult issue to get through. I think it is a great step forward and it will help some people who were treated unjustly, but there is still a lot of work to be done.

“I believe we’ll start seeing pressure from the global market on the United States to move things along a little faster in our own country.”As far as rescheduling, if they go from a Schedule I drug to a Schedule II drug, that will do no good, but it certainly is a bone to throw to the industry if you want to look like you are making some progress. Schedule II is still subject to 280E tax code so it will only do so much. If they want to make things more equitable and actually level the playing field, they have to do something about the 280E issue hindering every cannabis business in the country.

As far as full legalization, I am not optimistic because of all the players that need to be involved. Full legalization will require a change to the IRS tax code 280E as well as other tax issues. I think there are too many players: The DOJ, FinCen, the DEA, the FDA, the IRS. All of these agencies will have to agree on full legalization and moving forward in unison. The DEA is trying to fight illicit actors and illicit drugs. FinCen is trying to follow the money to find illicit actors. As long as there is an illicit market it will make their job tough, and on top of all of that, we have politics in play. That is just my take on legalization. It is going to be a much more complex problem than just legalizing the plant and moving on. Rescheduling seems like lower hanging fruit, but they will have to move it higher than a Schedule II.

CIJ: With the midterm elections here, there are a number of legalization measures in a handful of states, along with political control of Congress on the ballot. How do you think a Republican or Democrat controlled Congress will affect cannabis legalization progress?

Seefried: I just finished doing some lobbying in September in DC and spoke to some Senator offices in person, and I heard a lot of interesting topics being discussed. One of the things that keeps popping up is that social equity and justice is a huge issue. If we can’t solve this injustice in our system that has been going on for decades and decades, maybe they’ll hold banking legislation hostage. You can’t correct 50-60 years with one piece of legislation. Everything has to be incremental, unfortunately, so there will be some give and take there. I think that was a primary focus, especially with the Democrats and I do think it is a worthy cause.

On the Republican side, economically improving our competitive advantage as a country. They are starting to see the jobs being created and the tax revenue coming in and the growth of the industry. They will have to make that decision at some point in time whether they are going to leave the American cannabis industry behind or allow them to compete on a global level. I really think everything will move slowly and continue as it has happened in the past.

I believe we’ll start seeing pressure from the global market on the United States to move things along a little faster in our own country.

CIJ: As we inch closer to 2023, what do you expect the next year to offer for the cannabis financing market?

Seefried: I would say, with or without legislation, they’re finding greater access to banking. And the reason they are getting better access to banking is because none of us have been prosecuted for simply engaging in cannabis banking. I think we have set a precedent over the past eight years, not only us but other service providers in the industry and that we are not being prosecuted.

I see more financial institutions entering the market slowly. The second reason access to capital and banking will increase is because every financial institution in the country wants that lending relationship. In order to get there, they want to start with the depository relationship, and they don’t want smaller players presently doing it and getting all of those relationships before they enter the market. I think the competitive nature of the financial industry to land that lending relationship is going to force them into the game sooner than later.

By Tamara L. Kolb, Amy Bean, Caitlin Strelioff No Comments

As the legal cannabis market expands, banks and nonbank financial institutions (NBFIs) across the United States continue to explore how to safely provide banking and other financial services to cannabis-related businesses (CRBs) and other CRB ecosystem players. At the same time, these organizations are taking into account changes they might need to consider relative to their Bank Secrecy Act ( BSA), anti-money laundering (AML) and related compliance programs.

Regulatory conundrum

The Controlled Substances Act (CSA) identifies the cannabis plant and all its derivatives as a Schedule 1 controlled substance. Schedule 1 controlled substances have a “high abuse potential with no accepted medical use,” and they cannot be “prescribed, dispensed, or administered.” Because cannabis remains classified as a Schedule 1 controlled substance, the CSA “imposes strict controls on possession, manufacturing, distribution, and dispensing” of cannabis.

Under the Money Laundering Control Act of 1986 (MLCA) and the BSA as amended, covered banks and NBFIs are prohibited from providing financial services to businesses that are engaged in illicit activities. Because federal law prohibits the distribution and sale of cannabis, financial transactions involving CRBs are therefore deemed to be transactions that involve funds derived from illegal activities.

As of Feb. 3, 2022, 18 states, two territories, and the District of Columbia have enacted legislation to regulate cannabis for adult use. Thirty-seven states, the District of Columbia and four territories have approved comprehensive, publicly available medical and cannabis programs. Eleven states allow for the use of low-THC, high-CBD substances for medical reasons in limited situations or as a legal defense.

The growing divide between federal prohibition and state legalization of the cannabis industry creates a precarious position for federally regulated banks and NBFIs with the main concern involving exposure to legal, operational and regulatory risk. The situation begs the question: How might the federal government and regulators pursue and prosecute players in the legal cannabis industry?

The current economic trajectory predicts that retail sales of legal cannabis products in the U.S. will surpass an estimated $41.5 billion annually by 2025, and many banks and NBFIs are eagerly awaiting the federal green light to do business with CRBs without fear of prosecution or legal ramifications.

From 2018 forward, Congress has made several attempts to pass legislation that would protect CRBs when cultivating, distributing, marketing, and selling cannabis products in their state-legalized form. These efforts to declassify cannabis-related activity as a specified unlawful activity have thus far been unsuccessful.

The House passing the MORE Act back in 2020

Passage of the Secure and Fair Enforcement Banking Act of 2021 (SAFE Banking Act) and the Marijuana Opportunity Reinvestment and Expungement Act of 2021 (MORE Act) would enable banks and NBFIs to provide financial services to CRBs. The SAFE Banking Act would provide a safe harbor for banks and NBFIs that provide financial services to CRBs. The MORE Act would deschedule cannabis from the CSA entirely.

Questions to ask

Banks and NBFIs interested in providing financial services to CRBs should ask these questions:

Do we adequately understand our risk, and what are the implications for our organization? How should we augment our risk assessment process and our controls?

To what extent are we willing to accept the risk of banking CRBs? Do we have the ability to identify CRB customers, and if so, do we have any?

How should we advise the board of directors about setting risk appetite?

What customer due diligence (CDD) and enhanced due diligence (EDD) will we need to safely continue with existing customers and onboard new ones?

How will we monitor for unusual and suspicious activity? What will be the alerting and judgmental criteria?

How will our resource needs change so that we stay abreast of new processes and controls?

Risk appetite considerations

In order to determine whether to accept or prohibit CRBs, banks and NBFIs should identify the level of acceptable risk they are willing to take on. Several key components need to be considered, such as:

The board of directors’ stance on legal cannabis, given that good governance recommends and regulators expect that the board sets risk appetite

Cannabis laws in states within the customer footprint and the impact on customers’ communities

Risk profile, customer base, geographic location, products, and services

Relationship with regulators and any recent deficiencies or weaknesses in the BSA and associated compliance programs

Ability to implement appropriate controls and staffing

Developing a strategic road map

If the decision is made to bank CRBs, banks and NBFIs should perform an assessment of compliance maturity for existing BSA/AML program processes and controls to identify potential gaps and develop a strategic road map that helps the organization achieve its vision for future state compliance and sustainable operations.

A well-developed and well-articulated strategic road map visualizes what actions or key outcomes are needed to help organizations achieve their long-term goals. When creating the road map, banks and NBFIs need to demonstrate a keen understanding of their desired strategy, outcomes, markets, and products for onboarding and banking CRB customers. Specifically, banks and NBFIs need to define and explain how desired outcomes and business strategies create risk and exposure.

In addition to a road map, banks and NBFIs should develop and document a detailed risk-based approach that is aligned to the organization’s risk tolerance to determine necessary compliance steps when banking CRB customers.

Specifically, the following activities should be considered when developing a CRB banking program that meets regulatory expectations:

Identifying BSA/AML control gaps related to CRB risk identification and mitigation and formulating a plan to address them

Updating a board-approved policy framework

Updating detailed operating policies and procedures

Planning for capacity, developing job descriptions, and onboarding new personnel

Training for all three lines of defense, senior management, and the board

Developing and documenting a phased or full approach to acceptance of CRB customers

Developing and documenting a CRB program oversight policy

This framework is intended to help banks and NBFIs differentiate types of CRBs and their corresponding risks, and it separates CRBs into three tiers and details risks for each tier. The following exhibit summarizes the approach:

Risk framework by tier

Level

Risk

Tier 1

Direct

Tier 2

Indirect with substantial revenue from Tier 1

Tier 3

Indirect with incidental revenue from Tier 1

Source: CRB Monitor

Even the most conservative of risk appetites equivalent to outright prohibition is not devoid of significant risk considerations. Residual risk frequently encompasses a large number of indirect connections in the total CRB ecosystem. Common examples are printers, lawyers, accountants, landlords, and even utilities and taxing authorities, and all of these are subject to regulatory scrutiny and, importantly, visibility to law enforcement. Also, policies to prohibit or restrict will be audited and examined for compliance, and exceptions will require explanations.

This panorama necessitates expertise and prudence in identifying and evaluating risks within the many layers of CRBs. For example, consider a bank or NBFI that banks a CRB’s employee or vendor. If a bank fails to properly implement controls that would allow it to identify and mitigate risk associated with banking CRBs, it will be susceptible to severe violations of the BSA, including civil money penalties, criminal penalties, and regulatory enforcement actions.

Implementing necessary precautions

A well-developed road map should consider and implement the following activities:

Understanding the most current state and federal cannabis laws and regulations to ensure the bank or NBFI’s compliance

Understanding the local, state, or tribal program to ensure CRB customers are compliant with the program

Implementing a CRB risk assessment

Implementing executive approval practices for direct CRBs

Developing adequate risk ratings (possibly through a risk-based, tiered approach) and corresponding monitoring for CRB customers that includes:

Integrating various customer onboarding and AML solutions at both onboarding and periodic levels

Scheduling regular reviews to include recurring enhanced due diligence, site visits, and transaction monitoring

Monitoring for suspicious activity, including red flags, via open sources for adverse information about the CRB customers and related parties such as beneficial owners

Performing adequate CDD and EDD that will validate that the CRB-offered products, services, and programs are compliant with most current state laws and regulations by:

Collecting appropriate documentation as evidence of compliance, perhaps including a comprehensive onboarding questionnaire, beneficial ownership information, and contracts for the growing, harvesting, transporting and processing of the product

Reviewing applications and supporting documentation used to obtain a legal cannabis state license

Understanding the normal and expected activity of the organization’s CRB customers and their product usage

Developing adequate training programs and governance and oversight programs to address this customer type by:

Updating existing policies and procedures to review inherent risk presented by banking CRB customers

Updating annual training for employees

Auditing initial program design and periodic operational effectiveness

Moving forward cautiously

The ins, outs, and unknowns of cannabis banking are complex, and they require banks and NBFIs to be extremely vigilant with current policy and aware of new developments. Overall, the idea of creating a cannabis program might seem like a daunting task, but with appropriate guidance and care, organizations can provide services in compliance with laws and regulations.

Crowe disclaimer: Qualified organizations only. Independence and regulatory restrictions may apply. Some firm services may not be available to all clients. Given the continued evolution and inconsistency of various state and federal cannabis-related laws, any company should seek competent legal advice relating to its involvement in the cannabis industry, including when considering a potential public offering as a cannabis-related company.

Cannabis is still federally illegal and is included on Schedule 1 of the Controlled Substances Act (CSA), along with such other substances as heroin, fentanyl and methamphetamines.1 It is a federal crime to grow, possess or sell cannabis.

Despite being federally illegal, 36 U.S. states and the District of Columbia have legalized the sale and use of cannabis for medical and/or adult use purposes,2 and both direct and indirect cannabis-related businesses (CRBs) are growing at a rapid rate. Revenue from medical and adult use cannabis sales in the US in 2019 is estimated to have reached $10.6B-$13B and is on track to reach nearly $37B in 2024.3

Because the sale of cannabis is federally illegal, financial institutions face a dilemma when deciding to provide services to CRBs. Should they take a significant legal risk or stay out of the market and miss out on a significant revenue opportunity? So far, the vast majority of financial institutions have been unwilling to take the risk, resulting in a dearth of options for CRB’s. Until recently, cannabis business operators had few options for financial services, but times are changing.

This piece will discuss current trends in banking for cannabis-related businesses. We will cover differences in legality at state and federal levels, complexities in dealing in cash versus digital currencies, Congressional actions impacting banking and CRBs and how banking is changing. The explosion of state legalization of cannabis over the past several years has had a strong ripple effect across the US economy, touching many industries both directly and indirectly. Understanding the implications of doing business with a CRB is both challenging and necessary.

Feds Versus States

Money laundering is the process used to conceal the existence, illegal source or illegal application of funds.4 In 1986 Congress enacted the Money Laundering Control Act (MLCA), which makes it a federal crime to engage in certain financial and monetary transactions with the proceeds of “specified unlawful activity.”5 Therefore, CRB transactions are technically illegal transactions under the MLCA.

Financial institutions therefore face a risk of violating the MLCA if they choose to do business with CRBs, even in states where cannabis operations are permitted. In addition, financial institutions could also face criminal liability under the Bank Secrecy Act (BSA) for failing to identify or report financial transactions that involve the proceeds of cannabis businesses operating legally under state law.6

Federal authorities continued to aggressively enforce federal cannabis laws

In short, because cannabis is illegal at the federal level, processing funds derived from CRBs could be considered aiding and abetting criminal activity or money laundering. States, however, began legalizing cannabis in 1996, and by 2009, thirteen states had laws allowing cannabis possession and use.7 Despite this legislation, federal authorities continued to aggressively enforce federal cannabis laws.8 That changed under the Obama administration when, shortly after being elected, President Obama stated that his administration would not target legal CRB’s who were abiding by state laws.[9] In an attempt to provide clarity in this murky environment, beginning in 2009, the Department of Justice (DOJ) issued three memos designed to guide federal prosecutors in this area. However, none of the DOJ memos issued from 2009 through 2013 addressed potential financial crime related to the legal sale or distribution of cannabis in states allowing the use of medicinal or recreational cannabis.

To assist financial institutions in navigating potential financial crime implications of banking CRBs, the Financial Crimes Enforcement Network (FinCen) issued guidance in 2014 that clarified how financial institutions could conduct business with CRBs and maintain compliance with their Bank Secrecy Act requirements (2014 Guidance).9 According to the 2014 Guidance, financial institutions may choose to interact with CRBs based on factors specific to each institution, including the institution’s business objectives, the evaluated risks associated with offering such services, and its ability to manage those risks effectively.

The 2014 Guidance requires those who choose to provide services to CRBs to design and implement a thorough customer due diligence review that includes, in part, analyzing the licensing of the entity, developing an understanding of the business operations of the entity, and ongoing monitoring of the entity.9 In addition, financial institutions are required to file a Suspicious Activity Report (SAR) for every transaction they process for a CRB, should they choose to accept the business.

Although the 2014 Guidance does outline a path for financial institutions to engage with CRBs, it does not change federal law and, therefore, does not eliminate the legal risk to financial institutions.10 By its very nature, the 2014 Guidance was a temporary fix, subject to changing views of different administrations, evidenced by the fact that all three of the DOJ guidance documents noted above were rescinded by then Attorney General Jeff Sessions on January 4, 2018.12 The DOJ enforcement posture could change once again in a Biden administration. Biden is on record as favoring decriminalization, and Attorney General candidate Merrick Garland has stated that if confirmed he will deprioritize enforcement of low-level cannabis crimes. Garland also believes using limited government resources to pursue prosecution of cannabis crimes states where cannabis is legal does not make sense.12

Because of the uncertainty and high risk, most banks remain unwilling to serve CRBs. Those that do serve CRBs charge exorbitant fees (fees of $750-$1,000 or more per account per month are not uncommon), pricing many smaller operators out of the financial services market.

Cash is King – Or Is It?

Cannabis operators have discovered the old adage “cash is king” is not necessarily true when it comes to the cannabis space. Bank-less CRBs are forced to utilize cash to pay business expenses, which can be particularly difficult. Utility companies, payroll companies, and taxing authorities are just some of the providers that are difficult, if not impossible, to pay in cash. For example, cannabis operators have been turned away from IRS offices when attempting to pay large federal tax obligations in cash. Likewise, cannabis operators have been unable to utilize payroll processing companies to administer payroll and benefits for their businesses because the processors won’t take cash. CRBs can’t use Amazon or other online retailers because online providers cannot accept cash.

Because dealing in cash is so difficult, CRB operators look for workarounds such as using personal credit/debit cards to purchase business equipment and supplies. This doesn’t eliminate the cash problem, however, because the credit card holder will likely have to accept cash as reimbursement. Such transactions could be considered an attempt to hide the source of the cash, which is, by definition, money laundering.

CRBs often have large sums of money onsite

Some bank-less CRBs try to skirt the system by obtaining bank accounts in the name of management companies or other entities one step removed from the actual business. While operators often choose this route in an effort to streamline business and operate out of the shadows, it again runs afoul of banking laws. Transferring cannabis related financial transactions to another entity is actually the very definition of money laundering – which, as noted above, is defined as the process used to conceal the existence or source of “illegal” funds.

In addition to the difficulties in making payments or purchasing business supplies, operating in a cash-heavy environment poses significant safety risks for cannabis operators. CRBs often have large sums of money onsite and transport large sums of cash when purchasing product or paying bills, making them a target for robbery. In 2017, there was a spate of dispensary robberies across the Phoenix Metro area, including one at Bloom Dispensary that took place during operating hours.13

Managing all that cash increases the cost of doing business as well, in the form of increased labor, insurance, and security costs. Cash must be counted and double counted, which can be time consuming for staff, not to mention the time it takes to deliver physical cash payments to hither and yon. Ironically, lack of banking significantly decreases transparency and clouds the waters of compliance, as operating strictly in cash makes it easier to manipulate reported financial results.

Potential Congressional Solutions

In recent years Congress has undertaken several efforts to pass legislation designed to address the state/federal divide on cannabis, which would likely clear the way for financial institutions to provide services to CRBs, including:

R. 1595 – Secure and Fair Enforcement Banking Act of 2019 (“SAFE Act”);

1028 & H.R. 2093 – Strengthening the Tenth Amendment Through Entrusting States Act (STATES Act); and

2227 – Marijuana Opportunity Reinvestment and Expungement Act of 2019 (MORE Act).

The climate in Washington DC, however, did not allow any of these initiatives to pass both houses of congress. Had any been sent to the White House, President Trump was unlikely to sign them into law.

The cannabis industry has new reason to believe reform is on the horizon with shift in political leadership in the White House and Senate. Newly anointed Senate Majority Leader Chuck Schumer recently committed to making federal cannabis reform a priority, and President Biden appears committed to decriminalization, reviving the hope of passage of one of these pieces of legislation.

The Changing Banking Landscape

Even though there is little in the way of formal protections for financial institutions, and with the timeline for a legislative fix unknown, an increasing number of banks are working with cannabis operators.

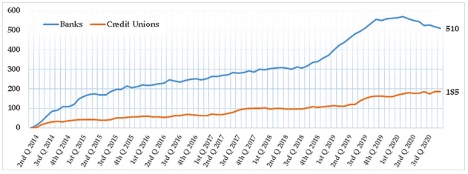

According to FinCen statistics, there were approximately 695 financial institutions actively involved with CRBs as of June 30, 2020. It is important to note that these statistics are based on SAR filings, which banks are required to file when an account or transaction is suspected of being affiliated with a cannabis business. However, some of these SARs may have been generated on genuine suspicious activity rather than on a transaction with a known cannabis customer.

Number of Depository Institutions Actively Banking Cannabis-Related Businesses in the United States (Reported in SARS)14

There are arguably more banking institutions offering services to CRBs than ever before. The challenges for CRBs are (1) finding an institution that is willing to offer services; (2) building/maintaining a compliance regime that will be acceptable to that institution; and (3) cost, given the high fees associated with these types of accounts.

How CRBs Get Accepted by Banks

The gap between CRBs’ need for banking and the financial services providers’ sparse and expensive offerings to the sector has created an opportunity for third-party firms to intervene and provide a compliance structure that will satisfy the needs of the financial institutions, making it easier for the CRB to find a bank.

These third-party firms perform extensive BSA-compliant due diligence on applicants to ensure potential customers are following FinCen guidance required to receive banking services. After the completion of due diligence, they connect the CRBs with financial institutions that are willing to do business with CRBs and provide checking/savings accounts, check writing capability, and merchant processor accounts. These firms often provide additional services such as armored car and cash vaulting services. Some of these firms also offer vendor screening, pre-approving vendors before any payments can be made.

One such firm, Safe Harbor Private Banking, started as a project implemented by the CEO of Partners Credit Union in Denver, Colorado, who set out to design a cannabis banking program that would allow Partners to do business with Colorado CRBs.15 The program was successful and has since expanded into other states who have legalized cannabis. Other operators include Dama Financial and NaturePay.

While these services offer hope for many CRBs, the downside is cost. These services perform the operations necessary to find, open, and maintain a compliant bank account; however, the costs of compliance are still high, pricing some small operators out of the market.

Is Digital Currency an Answer?

Digital currency is also making its way into the cannabis world. Digital currency, or cryptocurrency, is a medium of exchange that utilizes a decentralized ledger to record transactions, otherwise known as a blockchain. One of the largest benefits of blockchain is that it is a secure, incorruptible digital ledger used for, among other things, financial transactions.16 Blockchain technology offers CRBs a transparent and immutable audit trail for business and financial transactions. Several cannabis-specific cryptocurrencies have sprung up in the past several years, including PotCoin, CannabisCoin, and DopeCoin, to name a few.

In July 2019, Arizona approved cryptocurrency startup ALTA to offer services to the state’s medical cannabis operators.17 ALTA describes itself as a “digital payment club where cash-intensive businesses pay each other using digital tokens instead of cash.”18 ALTA members purchase digital tokens that are used to pay other members using a proprietary blockchain based system. The tokens are redeemable for US dollars at a stable rate of 1:1, and CRBs do not need a bank account to participate in the ALTA program.

ALTA proposes to pick up members’ cash and exchanges it for tokens, which are then used to pay other members for goods and services. Tokens may be redeemed for cash at any time.18 The company has been approved by the Arizona State Attorney General, and one of the first members they hope to enlist is the Arizona Department of Revenue (ADOR). Enlisting ADOR into the program would allow dispensary members to pay state taxes digitally rather than hauling large amounts of cash to ADOR offices.

Similarly, Nevada recently contracted with Multichain Ventures to supply a digital currency solution to the Nevada cannabis industry. Nevada Assembly Bill 466 requires the state create a pilot program to design a “closed loop” system like Venmo in an effort to reduce cash transactions in the cannabis sector. Like ALTA, Nevada’s proposed system will convert cash to tokens which can then be transacted between system participants.19

While both proposals are promising for Arizona and Nevada CRBs, the timeline as to when, or if, these offerings will come online is unknown. Action on cannabis reform at the federal level may render these options moot.

Looking to the Future

Although states are legalizing cannabis in one form or another in growing numbers, the fact that cannabis is still federally illegal poses a significant barrier to accessing the financial services market for CRBs. While most banks are still reluctant to offer services to this rapidly growing industry, there are more banks than ever before willing to participate in the cannabis industry. Recent changes in leadership in Washington DC offer a positive outlook for cannabis reform at the federal level.

As the “green rush” continues to envelop the country, financial services options available to CRBs are slowly growing. Many new options are now available to help CRBs find a bank, develop compliance programs, and manage the cash related problems encountered by most CRBs. However, these solutions may be out of reach for the budget-conscious small operator. Also, there are a number of cryptocurrency solutions designed specifically for CRBs; however, when, or if, these solutions will gain significant traction is still unknown.

References

Controlled Substances Act, 21 U.S.C., Subchapter I, Part B, §812.

“State Marijuana Laws”; National Conference of State Legislatures, February 19, 2021.

“Exclusive: US Retail Marijuana Sales On Pace to Rise 40% in 2020, near $37B by 2024”. Marijuana Business Daily, June 30, 2020.

Kaufman, Irving. “The Cash Connection: Organized Crime, Financial Institutions, and Money Laundering”. Interim Report to the President, October 1984.

S. Code § 1956 – Laundering of Monetary Instruments.

Rowe, Robert. “Compliance and the Cannabis Conundrum.” ABA Banking Journal, September 11, 2016.

“History of Marijuana as a Medicine – 2900 BC to Present”. ProCon.org, December 4, 2020.

Truble, Sarah and Kasai, Nathan. “The Past – and Future – of Federal Marijuana Enforcement”. org, May 12, 2017.

Sessions, Jefferson B. “Memorandum for All United States Attorneys”. January 4, 2018.

“Attorney General Nominee Garland Signals Friendlier Marijuana Stance”. Marijuana Business Daily, February 22, 2021.

Stern, Ray. “Robbers Hitting Phoenix Medical Marijuana Dispensaries: Is Bank Reform Needed?” The Phoenix New Times, April 11, 2017.

FinCen Marijuana Banking Update, June 30, 2020.

Mandelbaum, Robb. “Where Pot Entrepreneurs Go When the Banks Just Say No.” The New York Times, January 4, 2018.

Rosic, Ameer. “What is Blockchain Technology? A Step-by-Step Guide for Beginners.” com, 2016.

Emem, Mark. “Marijuana Stablecoin Asked to Play in Arizona Fintech Sandbox.” CCN.com, October 25, 2019.

http:\\Whatisalta.com\

Wagner, Michael, CFA. “Multichain Ventures Secures Public Sector Contract with Nevada to Supply Tokenized Financial Ecosystem for the Legal Cannabis Industry”, January 26, 2021.

During a press conference held today, Senate Majority Leader Chuck Schumer, Senate Finance Committee Chair Ron Wyden and Senator Cory Booker introduced the preliminary draft for the Cannabis Administration And Opportunity Act, a bill that would remove cannabis from the list of controlled substances.

“This is the first time in American history that the majority leader of the United States Senate is leading the call to end prohibition of marijuana,” Sen. Booker said toward the end of their remarks. Sen. Wyden stressed the history of the failed war on drugs, the successes of his state’s legalization and the need to include minority-owned small businesses in the new legislation.

Senate Majority Leader Chuck Schumer introducing the bill during today’s press conference

Sen. Schumer emphasized the need for revisions to the bill, bipartisanship and cooperation as they present the preliminary draft to their colleagues. “The waste of human resources because of the historic overcriminalization has been one of the great historical wrongs for the last decades and we are going to change it,” Sen. Schumer said.

While the bill is still in the early stages of its draft, the promising new legislation offers a few provisions that cannabis industry advocates and stakeholders have been hoping to see. Firstly, it would completely remove cannabis from the Controlled Substances Act. It sets up a framework for states to establish their own policies around cannabis, much like the current state of affairs in the industry and also akin to how the federal government treats alcohol.

Speaking to the social equity matters that Sen. Wyden emphasized, the bill would immediately expunge all federal records of non-violent cannabis crimes as well as establish a small business grant program for funding equity applicants, those impacted by the drug war and funding for state-level social equity programs.

As a strange year heads to a final, painful finish, there have been some major (and some less so) changes afoot in the global world of cannabis regulation. These developments have also undoubtedly been influenced by recent events, such as the recent elections in the United States, state votes for adult use reform in the U.S. and the overall global temperature towards reform. And while all are broadly positive, they have not actually accomplished very much altogether.

Here is a brief overview of the same.

The UN Vote On Cannabis Despite a wide celebration in the cannabis press, along with proclamations of an unprecedented victory by large Canadian companies who are more interested in keeping their stock prices high than anything else, the December 2 vote on cannabis was actually fairly indecisive.

Following the WHO recommendations to reschedule cannabis, the UN voted in favor of the symbolic move. Despite removing cannabinoids from Schedule IV globally, a regulatory label designed for highly addictive, prescription drugs (like Valium), the actual results on the ground for the average company and patient will be inconclusive.

The first issue is that the UN did not remove cannabinoids themselves, or the plant, from Schedule I designation. This essentially means that countries and regions will be on the front lines to create more local, sovereign policies. This is not likely to change for at least the next several years (more likely decade) as the globe comes to terms with not just a reality post-COVID-19, but one which is very much pro-cannabis.

In the meantime, however, the ruling will make it easier for research to be conducted, for patient access (for the long term), and more difficult for insurers to turn down in jurisdictions where the supposed “danger” of cannabis has been used as an excuse to deny coverage. See Germany as a perfect example of the same.

It is also a boon for the CBD business, no matter where it is. Between this decision and the recent victory in Europe about whether CBD is a narcotic or not (see below), this is another nail in the coffin for those who want to use semantic excuses to restrain the obvious global desire for cannabinoids, with or without THC.

That said, the vote is significant in that it is a test of the current trends and views towards big issues within the overall discussion, beginning with decriminalization and a reform of current criminal and social justice issues inherent in the same. The Biden Administration, while plagued with a multitude of issues, beginning with the pandemic and its immediate aftershocks, will not be able to push both off the radar. Given the intersection of minority rights’ issues, the growing legality of the drug and acceptance thereof, as well as the growing non-partisan position on cannabis use of both the medical and adult use kind, and the economy, expect issues like banking to also have a hope of reform in the next several years.

Cannabis may be taking a back seat to COVID, in other words, but as the legalization of the industry is bound up, inextricably, in economic issues now front and center for every economy, it will be in the headlines a great deal. This makes it an unavoidable issue for the majority of the next four years and on a federal level.

Prognosis in other words? It’s a good next federal step that is safe, but far from enough.

The European Commission (EC) Has Finally Seen The Light On CBD

This combined with the UN rescheduling, will actually be the huge boost the CBD industry has been waiting for here, with one big and still major overhanging caveat – namely whether the plant is a “novel” one or not. It is unlikely as the situation continues to cook, that Cannabis Sativa L, when it hits a court of law, will ever be actually found as such. It has inhabited the region and been used by its residents for thousands of years.

However, beyond this, important regulatory guidance will need to fall somewhere on the matter of processing and extraction. It is in fact in the processing and extraction part of the debate that this discussion about Novel Food actually means something, beyond the political jockeying and hay made so far.

Beyond this of course, the marketing of CBD now allowed by this decision, will absolutely move the topic of cannabinoids front and center in the overall public sphere. That linked with sovereign experiments on adult use markets of the THC kind (see Holland, Luxembourg and Denmark as well as Portugal and Spain right after that), is far from a null sum game.

Legal Challenges Of Note

The European Court of Human Rights

Against this changing regulatory schemata, court cases and legal decisions remain very important as they also add flavor to how regulations are interpreted and followed. The most important court case in Europe right now is the one now waiting to be decided in the Court of Human Rights at Strasbourg regarding the human rights implications of accessing the plant.

Beyond that, in Germany, recent case law at a regional social benefits court (LSG) has begun to establish that the cannabis discussion is ultimately between doctors and their patients. While this still does not solve the problem of doctor reluctance to prescribe the drug, barriers are indeed coming down thanks to legal challenges.

Bottom line, the industry has been handed a nice whiff of confidence, but there is a still high and thorny bramble remaining to get through – and it will not happen overnight, or indeed even over the next several years.

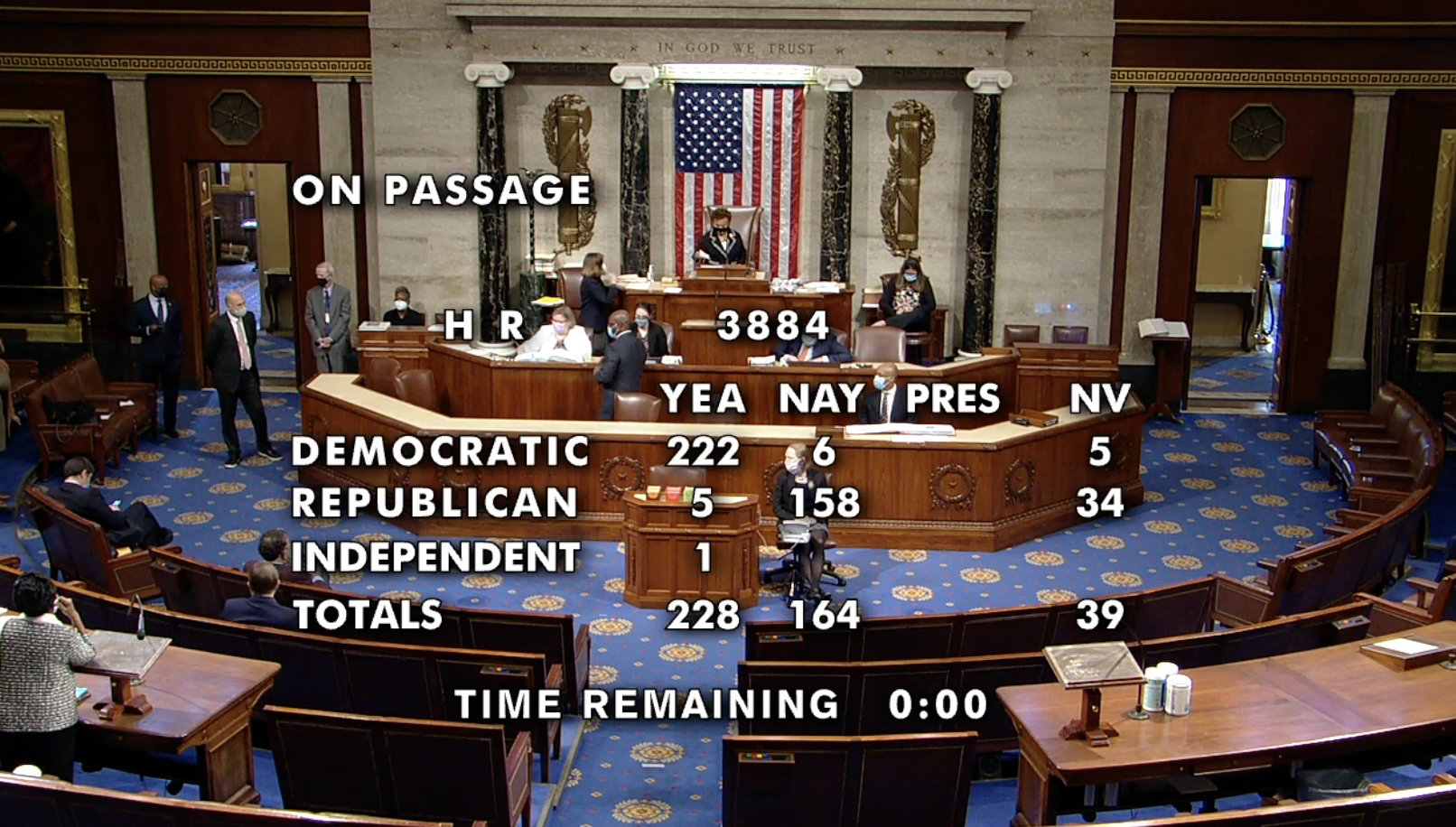

On Friday, December 4, 2020, the US House of Representatives passed the Marijuana Opportunity Reinvestment and Expungement Act of 2019 (the MORE Act), which would effectively legalize cannabis by removing it from the Controlled Substances Act. The bill (H.R. 3884) has several key components:

Most importantly, the bill would remove cannabis from the list of controlled substances in the Controlled Substances Act, as well as other federal legislation such as the National Forest System Drug Control Act of 1986. This would effectively end many of the obstacles created by the federal illegality of cannabis such as the lack of access to banking, tax consequences such as 280E, adverse immigration impacts and threats of federal criminal enforcement.

Rep. Earl Blumenauer (D-OR) donning his cannabis mask as he presides over the Congress

Second, not only does the bill preclude future prosecution for cannabis-related crimes, the bill is designed to be retroactive and would provide for the expungement of past non-violent cannabis offenses.

The bill creates a prescribed excise tax on cannabis and cannabis products. The funds collected from the taxes would be channeled into opportunity and reinvestment programs.

A Community Reinvestment Grant Program would be established aimed at the provision of services for “individuals most adversely impacted by the War on Drugs,” such as job training, education, literacy programs, mentoring, and substance use treatment programs;

A Cannabis Opportunity Program would be established providing state funds for small business loans in the cannabis industry targeted at social equity candidates; and

An Equitable Licensing Grant Program providing funds for states to implement equitable cannabis licensing programs aimed at minimizing “barriers to cannabis licensing and employment for individuals most adversely impacted by the War on Drugs.”

The bill would require all cannabis producers to obtain a federal permit. Cannabis businesses would need to be licensed at the state, local, and federal levels to operate.

This MORE Act is a substantial step in cannabis legislation. Reactions to the proposed legislation have been mixed. While the bill does include some measures aimed at social equity, critics of the bill claim it does not go far enough. Similarly, while the bill includes a federal permitting provision, this would be the beginning of a nascent federal regulatory scheme.

What does this mean for your business?

While this bill passed in the US House of Representatives, it would still need to pass in the U.S. Senate this term, which by most accounts does not seem likely. However, the passage of this bill signifies the progress that has been made and provides insight on what further legislation may look like.

It was 1996. I was four years old. California Proposition 215 passed and for the first time, legal medical cannabis became available. I don’t remember it honestly, but that moment triggered a reckoning of outdated and ineffective efforts to control cannabis, which continues on November 3rd.

The moment in 1996 created for me and my generation of millennials a new, decriminalized lens for which to view cannabis and its potential. In my lifetime, from first experimenting with cannabis after high school and then earning my PhD in plant biochemistry, advancing cannabis research, to starting an agtech company dedicated to the genetic improvement of cannabis, we continue this march toward legalization. But another march hasn’t started yet.

The cannabis we consume today is still largely the same (albeit more potent today) as the cannabis that was legalized in 1996. There’s been little advancement in our scientific understanding of the plant. This can and should change. I believe the future and legitimacy of the cannabis crop in the medical field and in farmers’ fields is on the ballot this November.

Five states have cannabis on the ballot for November 3rd

In 33 states, medical cannabis is currently legal and in eleven of those, including my home states of Nevada and Washington, legalized adult-use recreational cannabis is generating millions in tax revenue every month. But compared to every other commercial crop, cannabis is still decades behind.

We are seeing a glacial cadence with cannabis research. As voters in five more states consider this November whether to legalize cannabis, that same tipping point we reached in 1996 comes closer to being triggered for cannabis research.

Here’s what cannabis scientists, like me, face as we work to apply real scientific methods to the long-neglected crop: I published one of the most cited papers on cannabis research last year, titled, Gene Networks Underlying Cannabinoid and Terpenoid Accumulation in Cannabis. But, as per university policy, we were unable to touch the plant during any of our research. We could not study the physical cannabis plant, extracts or any other substantive physical properties from the plant on campus or as a representative of the university. Instead we studied cannabis DNA processed through a third-party. Funding for the research came from private donors who were required to be unassociated with the cannabis industry.

While we were conducting our heavily restricted, bootstrapped cannabis research, the university lab in the next building over was experimenting with less restrictions on mice using other drugs: cocaine, opioids and amphetamines. (Quick note, marijuana is listed as more dangerous than cocaine, which is a Schedule II drug.)

I get it. Due to the federal prohibition on cannabis as a heavily regulated Schedule I drug, universities cannot fund research without the risk of losing all of their federal funding. While the USDA does not support research and SBIR grants are all but impossible, one government agency does allow research, from cannabis grown only in Mississippi. It’s the Drug Enforcement Agency (DEA) and any research conducted using its crop is as ineffective as you’re imagining. Relevant research is likely impossible using the crop which dates back to a 1970’s strain with a potency that’s about 30 percent of today’s commercial cannabis offerings.

To change this anti-research climate, do what those in California did with Prop 215 in 1996. Vote.

Dr. Jordan Zager, author and CEO of Dewey Scientific

Vote for legalization of cannabis if you’re in those five states where legalization is on the ballot; that’s Arizona, New Jersey, Montana, South Dakota and Mississippi. The more states that align with cannabis legalization, the stronger the case becomes for the federal government to reschedule the drug from a Schedule I controlled substance. Currently cannabis is listed as a Schedule I alongside heroin. The DEA claims cannabis has no currently accepted medical use and a high potential for abuse. Both are not true, just listen to the scientists.

Those outside of the five states putting cannabis on the ballot can still play a role in creating a Congress that is more receptive to cannabis reform. This Congress is the oldest, one of the most conservative and least effective in our country’s history. Younger, more progressive representation will increase our odds of advancing cannabis research.

Cannabis holds far too much possibility for us to allow it to be an unstudied “ditch weed.” THC and CBD are just two of nearly 500 compounds found in cannabis which, when scientifically scrutinized will harvest – I believe – vast medicinal and commercial benefits and the tax windfalls that accompany both. But first you have to vote.

If cannabis and your representatives are not on the ballot, do something millennials have built somewhat of a reputation for failing to do; pick up a phone and call your current representative. Tell them cannabis deserves scientific attention and investment. There’s too much potential in the cannabis plant to wait any longer.

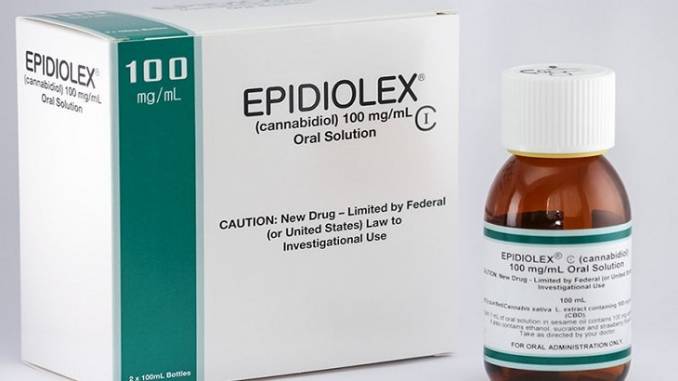

As of this writing, the United States Food and Drug Administration (FDA) has approved GW Pharma’s CBD drug Epidiolex for treating profound refractory pediatric epilepsy syndromes (Dravet syndrome and Lennox Gastaut syndrome) as well as for treating seizures associated with tuberous sclerosis complex (TSC) in patients one year of age or older. The product is a very simple, orally-administered formulation comprised of 100mg/ml cannabidiol (CBD), dehydrated alcohol, sesame seed oil, strawberry flavor and sucralose – basically, an alcohol-based solution with sesame seed oil to help solubilize the CBD oil, flavoring and sweetener.

On April 6th, 2020 GW Pharma performed a regulatory miracle when they succeeded in convincing the Drug Enforcement Administration (DEA) to deschedule Epidiolex (i.e., remove it from the Schedule 1 and Schedule 5 lists of substances that the agency regulates due to concerns regarding safety, potential for abuse or both) for all indications – including indications for which it has not yet been approved by the FDA.1 The benefit to GW of having their product descheduled is incalculable. This status change removed potential barriers to insurance reimbursement and made the need to set up and administer an expensive REMS2 drug safety program less likely. In part because of this regulatory coup d’état, the drug recently posted yearly earnings of nearly $300 million.

It is important to note that the DEA descheduled the Epidiolex formulation and not cannabis-derived CBD itself. Thus, GW Pharma is now in the enviable position of being the only company that can legally sell cannabis-derived CBD. More importantly, because the DEA descheduled the formulation and not the active ingredient, other companies who wish to market cannabis-derived CBD pharmaceutical formulations will have to repeat whatever it is that GW did to get Epidiolex descheduled.3 The DEA effectively gave the company a huge head start with respect to competitors who are developing other cannabis-derived CBD formulations that would compete with Epidiolex. That advantage will remain in place unless and until cannabis-derived CBD itself is descheduled or cannabis is legalized at the federal level.

GW Pharma’s CBD drug Epidiolex, which is FDA-approved to treat profound refractory pediatric epilepsy syndromes

GW Pharma’s attorneys demonstrated considerable virtuosity in devising this approach. However, there is another aspect of the GW Pharma story – one that could have profound implications for the exploding CBD consumer packaged goods (CPG) industry. The Federal Food, Drug, and Cosmetics Act4 (FFDCA) prohibits the introduction into interstate commerce of any food to which has been added an approved drug or a drug for which substantial clinical investigations have been instituted and made public.5 Because CBD was and is still the subject of clinical trials run by GW Pharma and others, even hemp-derived CBD is currently illegal to use as a food additive or dietary supplement under the FDCA

The FDA has recently re-started the public commentary stage of a long process that will hopefully result in the creation of a regulatory pathway for CBD to be used as a food additive – something that would seemingly be a straightforward matter given the copious amounts of safety data being generated from all of GW Pharma’s clinical trials. However, as long as the FDA continues to drag its feet in providing a regulatory pathway for CBD CPG products, CBD, regardless of its source, will remain illegal to use as a food additive or supplement under either the CSA or the FFDCA despite the existence of safety data obtained through the Epidiolex clinical trials. If, as many people in the industry anticipate, the agency decides to begin enforcement action, this could have a hugely negative impact on the industry.

In addition to the potentially disastrous effect that federal law could have on an important new industry, the federal regulatory scheme introduces unnecessary regulatory complexity and cost by imposing two different regulatory schemes depending on the source of the CBD. CBD derived from hemp is chemically identical to CBD derived from cannabis. Despite that identity, the 2018 Farm Bill nonsensically exempts only hemp-derived CBD from the Controlled Substances Act. If a regulatory pathway is created for hemp-derived CBD, but the DEA insists on maintaining cannabis-derived CBD as a schedule 1 substance, then the same molecule will be subject to two different regulatory schemes. This scenario would require tracking and certifying CBD sources and thereby impose regulatory and economic burdens that are entirely unnecessary from a public health point of view.

An alternative, economically disastrous scenario: given the pharmaceutical industry’s formidable lobbying power, it is entirely possible that the FDA could decide to limit the use of CBD exclusively in prescription drug formulations. This could kill the entire US hemp CBD CPG industry, currently estimated to reach $22 billion by 2022.6

Overall, the current state of affairs is unfair, expensive, uncertain and entirely unworkable over the long term. The CSA must be amended, ideally to deschedule both hemp and cannabis entirely, but at least in the short term, to deschedule CBD and preferably all non-THC cannabinoids regardless of their source. Further, the FDA must provide a regulatory pathway to allow the use of low doses of cannabinoids shown to be safe, either by existing clinical trial data or future testing pursuant to the NDIN submission process.

A 2019 Gallup poll found that 14% of Americans – 1 in 7 – use CBD products.7 The demand is there, the industry is thriving, and adequate safety data exists to justify a regulatory system that allows low-dose over the counter CBD products provided those products are produced using Current Good Manufacturing Practices (CGMPs) for food and dietary supplement manufacturing prescribed by the FDA and that such products undergo regular testing that demonstrates they are safe, unadulterated and accurately labeled. It is time for the industry to collectively fund a New Dietary Ingredient Notification (NDIN) submission that would provide safety data sufficiently compelling to force the FDA to either recognize CBD and other non-THC cannabinoids as being GRAS substances regardless of their source, or in the alternative create a regulatory path for CPG products containing low-doses of CBD and other non-THC cannabinoids.

Editor’s Note: The opinions expressed in this publication are those of its author. They do not purport to reflect the opinions or views of the Cannabis Industry Journal, its editorial staff or its employees.

References

Clincialtrials.gov lists 256 different clinical trials in which Epidiolex has been, is being or will be tested for a wide variety of other indications, including but not limited to opioid use disorder, several types of prostate cancer, alcohol use disorder, musculoskeletal pain, and a host of others.

REMS – risk evaluation and mitigation strategy – are drug safety programs that the FDA requires in cases where mediations pose serious safety concerns with respect to potential abuse and other adverse effects.

Exactly what they did isn’t clear, and won’t be for a long while given the snail’s pace at which FOIA requests are filled.

Title 21 United States Code Chapter 9

Title 21 United States Cod Chapter 9, Sections 331(ll), 342(a)(1) and Section 342(d)(f)(1)

“Exclusive: New Report Predicts CBD Market Will Hit $22 Billion by 2022” Rolling Stone Magazine, September 11, 2018, citing cannabis industry analysis from the Brightfield Group.

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

We use tracking pixels that set your arrival time at our website, this is used as part of our anti-spam and security measures. Disabling this tracking pixel would disable some of our security measures, and is therefore considered necessary for the safe operation of the website. This tracking pixel is cleared from your system when you delete files in your history.

We also use cookies to store your preferences regarding the setting of 3rd Party Cookies.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.

The announcement comes just under a year after President Biden and his administration made a statement on cannabis reform. In that statement, which he made on Oct. 6, the president requested that the Secretary of HHS and the Attorney General (AG) initiate an administrative process to review how cannabis is scheduled under federal law, in addition to pledging to pardon all prior federal offenses of simple cannabis possession, directing the AG to develop an administrative process for the pardons and urging all governors to follow suit for state and local offenses. In a statement, Secretary Becerra said the agency acted “expeditiously” and completed the rescheduling process in less than 11 months, “reflecting the department’s collaboration and leadership to ensure that a comprehensive scientific evaluation be completed.” Indeed, the agency’s announcement reflects the administration’s desire to quickly resolve the country’s failed approach to cannabis reform, as prior rescheduling efforts have taken years. Few thought the federal government would move quickly on cannabis, let alone under a year.

The announcement comes just under a year after President Biden and his administration made a statement on cannabis reform. In that statement, which he made on Oct. 6, the president requested that the Secretary of HHS and the Attorney General (AG) initiate an administrative process to review how cannabis is scheduled under federal law, in addition to pledging to pardon all prior federal offenses of simple cannabis possession, directing the AG to develop an administrative process for the pardons and urging all governors to follow suit for state and local offenses. In a statement, Secretary Becerra said the agency acted “expeditiously” and completed the rescheduling process in less than 11 months, “reflecting the department’s collaboration and leadership to ensure that a comprehensive scientific evaluation be completed.” Indeed, the agency’s announcement reflects the administration’s desire to quickly resolve the country’s failed approach to cannabis reform, as prior rescheduling efforts have taken years. Few thought the federal government would move quickly on cannabis, let alone under a year. While many stakeholders speculate that a decision will be made ahead of the November 2024 presidential election, others remain skeptical given the strict anti-drug posture hardwired into how the DEA operates. In fact, the HHS recommendation coupled with the DEA’s approach to drug policy has led some to speculate that the DEA may compromise by moving cannabis into Schedule II, a category reserved for medicines with high potential for abuse and dependence, including most common opioids.

While many stakeholders speculate that a decision will be made ahead of the November 2024 presidential election, others remain skeptical given the strict anti-drug posture hardwired into how the DEA operates. In fact, the HHS recommendation coupled with the DEA’s approach to drug policy has led some to speculate that the DEA may compromise by moving cannabis into Schedule II, a category reserved for medicines with high potential for abuse and dependence, including most common opioids.