On Christmas Day, not only did Israel, global leader in medical cannabis in particular, finally decide to legalize medical exports, but in a surprise move, so did Thailand.

Both developments are likely to have huge implications on the entire global cannabis discussion, albeit in slightly different ways.The impact will be interesting to watch.

Israel’s Export Decision

The issue of exports from the original home of the medical cannabinoid revolution has been a perennial sticky wicket for the last several years. As the Israeli medical market liberalized at home and certainly in the last five years, the government steadfastly refused to export the drug. Further, the country’s president Benjamin Netanyahu also cut a political deal with Donald Trump to move the Israeli capital from Tel Aviv to Jerusalem that delayed this discussion over the last 18 months. With a global market now exploding that Israel to date has been excluded from and Netanyahu’s political capital tarnished with corruption, things are about to change.

The impact will be interesting to watch. Especially with the network of Israeli production farms also sprinkling around particularly Eastern Europe and Greece.

Here is also what is intriguing: The country is, like Israel, looking at creating a domestic boon with a tightly controlled domestic economy booster. Not to mention clearing the jails, which are filled to bursting with people on even low level drug offenses.

Thailand’s Parliament

And just like Israel, Thailand is also, already, talking protectionist measures to shield domestic producers from being bought out by foreign interests, certainly of the corporate kind.

The Combination Package

In the short term this means, at least on the export front, that there will be more competitors to the Canadian giants now entering the room. And between Israel and Thailand alone, this also means that new strains on the medical side, will begin to enter global medical markets.

For all the future promise of tweaked product, cheap cannabis flower and oil flooding markets globally by importers and distributors realizing that the game is far from over, is going to be the first real challenge the Canadian cannabis companies have yet faced.

In the wake of the news that Epidiolex is not as effective longer term as hoped (which is a common phenomenon in the pharmaceutical industry known as a “drug holiday” where users initially improve and then develop tolerance to the drug), this is also an intriguing new development. This means that new strains are entering the global market at an unprecedented pace, literally competing with pharmaceutical products at a time when reform continues apace.

At a time when cannabis investments (particularly in the US), quadrupled in 2018, this also means that western dollars, if not companies, will begin to find other markets and market outlets.

And that is a Christmas present in 2018 that will reverberate long into the future.

Right now the map of Europe, from a cannabis cultivation perspective at least, is shaping up to be very much like a game of Risk. Throw the dice, move your armies (or more accurately line up your financing), and apply for federal import and cultivation licenses.

In the process, all sorts of interesting strategic plays are popping up. And as a result, here is a new and actually pretty cool “alternative” reality that is easy to verify in several different ways. Medical cannabis is being cultivated in multiple countries across Europe as of 2018, however unbelievable this was even four years ago. Even though it is still cleary just early days. And those cultivators are already international, operating across federal jurisdictions in Europe and across both the Atlantic and Pacific oceans.

With all the excitement and attention paid to the American hemisphere and the European moves of big Canadian LPs (and they are pretty amazing), there are still other moves afoot that are absolutely of note. Specifically, Australian firms and MGC Pharma in particular, have been moving steadily to establish both distribution and cultivation presence on the ground in Europe.

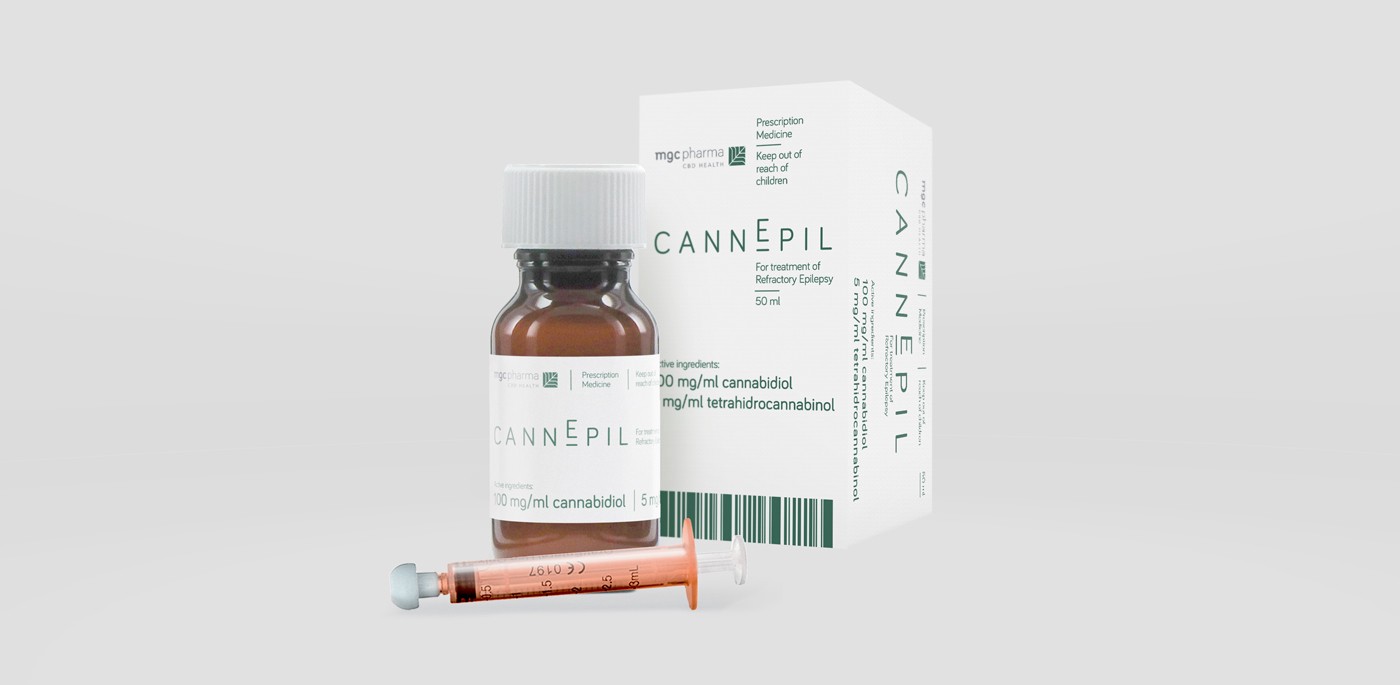

CannEpil, the company’s first pharmaceutical-grade medical cannabis product for the treatment of refractory epilepsy.

The latest news? MGC’s production facility in Slovenia was officially inspected by authorities and issued an interim license for its production plant in January, before presumably being given a green light of approval permanently. The company is also moving forward with the production of CannEpil, the company’s first pharmaceutical-grade medical cannabis product for the treatment of refractory epilepsy.

Refractory epilepsy affects about 30% of all those who suffer from the condition. Refractory is one of those words however, that hides its real meaning. Translation for those without an MD? This is “drug resistant” epilepsy. Resistant to all drugs before, of course, except cannabinoids.

And that is a welcome relief for patients domestically and throughout Europe. It is also a note to investors looking for savvy Euro plays right now.For all manufacturers now considering entering this market, this is a complicated environment to begin negotiating

This is a major win for MGC. Not to mention a vibrant medical market. No matter where specialty drugs are now going to be sourced from.

A Treatment-Driven “Branded” Pharma Market

What more traditional American pharmaceutical companies have known for a long time (certainly since the 1950’s) is now a fact also facing all cannabis brands coming to the European market and Germany in particular. The regulatory environment is hostile to the extreme for Auslanders in particular. Specifically, the development of “branded” or “name brand” drugs runs economically and philosophically counter to the concept of public health insurance itself even as their market accessibility is required by the same. This is even more the case for foreign firms with such ideas.

Here is the problem. Name brands are expensive. They are also usually outlier drugs for specific, relatively rare conditions. This is also the place where new drugs enter the market, no matter what they are.

In an environment where the government negotiates bulk contracts for common drugs and these can be bought at every apotheke (pharmacy) for 10 euros and a doctors rezept (prescription), the chronically ill and those with drug resistant conditions are left out of the discussion. They face steep and usually inaccessible bills up front for all meds not in bulk purchase categories. And that as of last year in Germany specifically, includes cannabis. That is the case even though technically the government is now buying cannabis in bulk and making purchase commitments to foreign companies for the same. Insurance companies, however, are still forcing patients to pay the entire out of pocket cost up front and wait to reimbursed.

“Generic” Brands For Off label Chronic Conditions

However medical cannabis is clearly not just another drug. Cannabis falls on both sides of every fence in this discussion.

The first problem is that the providers (importers and soon to be domestic cultivators) are private companies. All of them are foreign helmed at this point, with a well-developed bench of branded products. That makes all cannabis drugs, oil and flower, by definition, fall into the “expensive” branded category immediately. The German, Italian, and Danish governments appear to be now negotiating bulk buys during a licensing season that is well on the way to domestic cultivation too. That alone will affect domestic prices and new products. But again, this is now several years behind other countries – notably MGC in Slovenia, Tilray in Portugal, all things now afoot in Denmark and clearly, Greece.

Next, cannabis’s status as a still imported, speciality, semi-trial status in the EU means it is in the most restricted categories of drugs to begin with (no matter the name or strength of the cannabinoid in particular). And because it can be bought as bud, in an “unprocessed” form as well as processed oils or other medicine, this is throwing yet another spanner into the mix.

Look for distribution deals all over Europe as a result, starting with PolandThen there is this wrinkle. Cannabis (even CBD) is currently considered a narcotic within the EU and even more specifically the largest continental drug market – Germany. The German regulatory system in particular, also imposes its own peculiarities. But basically what this means in sum is that the legal cannabis community including distributors and pharmas at this point, have to educate doctors in an environment where cannabis itself is a new “brand.” Who manufactures what, for the purposes of German law, at least, is irrelevant. It is what that drug is specifically for that matters.

For all manufacturers now considering entering this market, this is a complicated environment to begin negotiating. This is sure not how things are back home.

What this also means is that low cost, speciality cannabis products will continue to be imported across Europe for the German and other developing, regulated sovereign markets here as doctors learn about cannabis from condition treatments. And that is what makes the news about MGC even more interesting.

Look for distribution deals all over Europe as a result, starting with Poland. And, despite the many well-connected and qualified hopefuls from Canada, a little competition in the German market too.

MS is the only “on-label” drug at present for cannabis treatment in Germany. As a result, particularly when it comes to paediatric treatment for drug resistant epilepsy, this is the kind of strategic presence that will create a competitive source for highly condition-branded medication for a very specific audience of patients. It is also what the German market, for one, if not the EU is shaping up to be at least in the near term.

As this interesting abstract from 2006 clearly shows, this kind of epilepsy is also high on the German radar from a public policy and healthcare-cost containment perspective. The costs of treatment per patient were between 2,600 and 4,200 euros for three months a decade ago, and not only have those risen, but so have the absolute number of people in similar kinds of situations.

Further, with indirect costs far higher than direct costs including early retirement and permanent semi disability, MGC’s market move into an adjacent (and cheaper) production market might be just what the German doctors if not policymakers now looking at such issues, will order.

Just as the dust had settled on the news that Canadian LP Aurora had signed agreements to finance a major growing facility in Denmark, the company also added another European feather to its cannabis cap.

On January 18, the company announced that it is the sole and exclusive winner of an EU-wide tender bid to begin to supply medical cannabis to the Italian government through the Ministry of Defense. Why is this federal agency in charge instead of the federal ministry of health? So far, the Italian cannabis program has been overseen exclusively by the Italian military.

Pedanios cannabis, produced in Canada and imported through Germany

But the military just isn’t cut out to cultivate cannabis for the entire medical needs of a country, which should seem obvious. And that is where the Canadian LPs apparently are coming into play.

There were two stages to the bid, with Pedanios, Aurora’s German-based arm prequalifying in the first. In the final round, Pedianos won exclusive rights to begin supplying the government with medical cannabis.

What is interesting, however, is what this says not only about the potential growth of the cannabis market in Italy, but beyond that, Germany.

A German-Canadian Sourced Italian Product?

Pedanios, who won the bid, is the German-based arm of Aurora, one of Canada’s largest LPs. And Italian medical cannabis is now about to be routed by them from Canada, via Berlin, to market locally via pharmacies. It is certainly one of the stranger paths to market globally.

This announcement is even more interesting given that Aurora is widely suspected to be one of the top contenders in the still-pending German bid.

Could this herald a German-sourced cannabis crop for an Italian neighbour?

And what does this say about the sheer amount of volume potentially needed for cultivation next door (or even in Italy) as Germany begins its own cultivation program, presumably this year, to source an already undersupplied domestic market where growing numbers of patients are getting their medical cannabis covered under public health insurance?

Will Germany further antagonize its neighbours over a cannabis trade imbalance? Or does this mean that a spurt of domestic Italian cannabis production is also about to start?

There are 80 million Germans and about 60 million Italians. Who will be the cannabis company to supply them?

Nuuvera Also Makes Italian Moves

Less widely reported, however, was the news that Aurora/Pedanios would not be the only private supplier to the Italian market. Nuuvera, which just announced that they had become finalists in the competitive Germany cultivation bid, also just acquired an import license to Italy for medical cannabis by buying Genoa based FL Group.

One thing is clear. The pattern of establishing presence here by the foreign (mostly Canadian) firms has been one of acquisition and financing partnerships for the past 2 years.

Import until you cultivate is also clearly the guiding policy of legalizing EU countries on the canna front.

The question really is at this point, how long can the import over cultivation preference continue? Especially given the expense of imported cannabis. Not to mention the cannabis farms now popping up all over the EU at a time when the Canadian market will have enough volume from recreational sales to keep all the large (and small) LPs at production capacity for years to come.

In the next year, in fact, look for this reality to start changing. No matter who has import licenses now with flower and oil crossing oceans at this point, within the next 18-24 months, look for this pattern to switch.

The distributors will be the same of course. But the brand (and source) of their product will be from European soil.

Foreign Invasions, Domestic Cultivation Rights & More

One of the more interesting professional conferences this year globally will clearly be the ICBC in Berlin, where all of these swirling competitions and companies come together for what is shaping up to be the most influential cannabis business conference in Europe outside of Spannabis (and with a slightly different approach). Nowhere else in the world now are international companies (from bases in Canada, Australia and Israel primarily) competing in such close proximity for so many foreign cannabis markets and cultivation rights to go with them.

With the average cultivation facility in Europe going for about USD $30-40 million a pop in terms of sheer capital requirements plus the additional capital to finance the inevitable delays, such market presence does not come cheap.

It is increasingly clear that the only business here will also be of the highly regulated, controlled medical variety for some time to come.

That said, when the move towards recreational does come, and within the next four years or so, the global players who have opened these markets on the medical side, will be well positioned to provide product for a consumer base that is already being primed at the pump. Even if for now, the only access is via a doctor’s prescription.

The Greek Parliament is finally expected to approve the medical use of cannabis – probably in the first weeks of February. The move is far from a surprise. Greek politicians announced last summer that this development was in the cards.

What is even more promising for the sector domestically, not to mention in terms of European reform, is the unflinching acceptance of this industry by the establishment and national politicians, and further as one with great economic development potential for a still-ailing economy.

A $2 Billion Injection of Capital

Deputy Agricultural Development Minister Yannis Tsironis (for one) has already publicly expressed his hope that the Greek medical program will attract beaucoups bucks from overseas.

However given the context in which this announcement has taken place, is this seriously a commitment to medical cannabis? Or is it an easy (if not slightly buzzy) way to attract foreign capital to a Mediterranean paradise still in dire need of a capital injection from any source it can get one?

Deputy Agricultural Development Minister Yannis Tsironis

Maybe it is a combination of both.

Many in Europe are forecasting that 2018 might finally be the light at the end of the tunnel for the Greek economy, which has been mired in austerity for the last decade. The Greek government is now in the process of moving forward with the final requirements of both labour reforms and receiving what is hoped to be the last bailout of its economy by foreign investors before it finally goes it alone by August 2018.

The Greek economy finally grew 1.5% last year. In 2018, in part thanks to the final package of reforms, the economy is expected to grow by 2.4%.

A foreign-financed medical cannabis business might be just what the economists have ordered. Especially if it is also open to visitors.

Medical Marijuana on Mykonos?

The development of a domestic medical cannabis industry in Greece is good news for not only medical reformers but also those who are looking for ways to expand the influence of the flower into the broader economy.

And Greece is one place where such ideas could easily and quickly take root in Europe.

Mykonos, the Greek island Image: Maggie Meng, Flickr

Greece has long been the haven for a highly niche, international tourist audience. Tourism in general has also been on the uptick over the last two years again as particularly Europeans look for relatively cheaper beaches and sunshine. Over 30 million foreign tourists flocked to the country last summer – a number of people roughly three times the population of the country.

Again, mainstreamed medical cannabis would only add to the economic results in a way that is just as heady if not (economically) stimulating as a good sativa.

The idea of a medical tourism industry here, could also potentially create not only a Greek medical paradise, but potentially also have a growth impact on European cannabis programs too. Especially if reciprocal medical rights we

re also offered to EU citizens looking for an extended canna-friendly vacation.

Greek Cannabis Club Med?

Of all the countries in Europe, the Greek cannabis experiment offers the first real chance for a Canadian/American style cannabis industry to begin to flourish in Europe. In colder, more northern European countries, medical cannabis is still being treated as an expensive adjunct to traditional healthcare. And no matter how much citizens are moving towards acceptance of a recreational industry down the road, things are moving much slower in the rest of Europe. Germany, to put things in perspective, passed medical reform several months before the Greek decision to legalize medical use last summer. Yet now it appears that Greece might actually move into a full-fledged, domestically grown industry before its Teutonic neighbour to the north.

And further, unlike Germany, Greece may well decide to develop its “medical cannabis industry” as an adjunct to its tourist industry.

Sure, Holland and Spain led the way in this part of the world if not internationally. Neither country, however, needs new industries now in the same dire way, nor is emerging from a national, decade-long recession.

All the elements are here, in other words, for the Greeks to turn a new page in their very long and documented history, and do something a little different.

In rather shocking news out of Germany on the cannabis front, it appears that Canadian LP ABcann has not been selected as one of the finalists in the country’s first tender bid to cultivate cannabis domestically.

As reported in the German press, the company has not been invited to submit an offer in the final award procedures. The reason per a company spokesman as quoted in the German media? The company proved it met the required qualification thresholds – namely it could deliver the required amount of product as required by the German government. However the amount it could produce was less than other firms being considered.

That is a strange statement, especially because the ten licenses on offer only called for a total of 2,000 kgs of production total by 2019 and 6600 kgs by 2022.

Who Is ABCann?

ABcann has been in business since 2014 in Canada, when it received one of the first cultivation licenses issued by the Canadian government. It has also been aggressively positioning itself in the German and European market this year – and in multiple ways. It got itself listed on both American and German stock exchanges by summer. The company established a subsidiary headquarters in Schönefeld as of August 2017. As late as October, the company also was appearing at industry conferences, like the IACM medical conference in Cologne, as an expected finalist in the first bid.

An ABCann facility in Canada

However, the company’s plans to build a $40 million, 10,000 square meter plant somewhere in Lusatia are now also reportedly on hold. The exact location of the plant is unknown, per German government requirements that grow facilities remain secret. That said, with a year and a half to complete construction, if given the green light even by early next year, it may be that this was the reason the company has apparently not made the cut. Or perhaps the German government did not believe the company was adequately funded. A September exercise of warrants netted the company an additional $45 million in operating cash. But with expansion plans in not only Canada and Europe, but Australia too, did the company pass the German test for liquidity?

Management changes are also afoot. As of October 1, Barry Fishman, a former Eli Lilly executive took over as CEO of ABCann Global. Ken Clement, founder of the company, announced in mid-October that he was stepping down from his position as Executive Chair of the Board to be replaced by Paul Lucas a former President and CEO of GlaxoSmithKline Canada. John Hoff, the Geschäftsführer (or CEO) of ABcann’s German subsidiary, has also recently left the company. When asked by CannabisIndustryJournal about his reasons for doing so at the Cannabis Normal conference in Berlin at the beginning of November, Hoff cited “management and creative differences” with ABcann Canada as the impetus for his recent departure.

However with the news of ABcann’s apparent loss of a front-runner position in the pending bid, such news appears to herald a bit more of a shakeup at the company, if not a refocussing of overall global strategy.

A source within the company who wished to remain anonymous also said this when contacted directly by CannabisIndustryJournal. “Our top priority currently is to acquire an import license. We also fully intend to pursue all of our plans in the German market, but we have no firm dates on the construction front.”

The State of Medical Cannabis Reform Auf Deutsch

The German medical cannabis question has certainly jerked forward over the past several years through several rough patches. This year it has gotten even stranger. And nobody is quite sure where it will end up.

The news about ABcann is also the latest episode in a very strange story that has continued to develop mostly out of sight of the public.

That bid process, which was expected to announce the winners by late summer, has now dragged on through the fall.Germany began moving forward quietly on the cannabis issue in the first decade of the century. Patients could only access the drug in basically trial mode. Most patients who qualified with a doctor’s prescription and a special permit to take the drug, could also access only Sativex (which is very expensive) or the synthetic form of the drug, dronabinol, manufactured domestically in a facility near Frankfurt. All bud cannabis was imported from Holland by Bedrocan. Strictly controlled not by German, but rather Dutch law on cannabis imports.

In 2014, the first German patients successfully sued the government to grow their own plants if their insurance companies refused coverage of the drug and they proved they could not afford alternatives.

This year, in January, the German government voted unanimously to change the law to mandate public health insurance. The law went into effect in March. Mainly driven by a desire to halt home-grow, the rules changed again. Post March 2017, patient grow rights have now been revoked. Now patients are theoretically allowed to get cannabis covered under public health insurance. In reality, the process has been difficult.

In April, the German government created a new “Cannabis Agency” under the auspices of BfArM. And BfArM in turn issued a tender bid for the country’s first domestic licences in April.

That bid process, which was expected to announce the winners by late summer, has now dragged on through the fall.

When Will The Winners Be Announced?

That too is unclear. It is very likely that the final announcement will not be made by the government until the beginning of the year – after the new government is formed. The so-called “Jamaica Coalition” – of the mainstream CDU, the Greens and the liberals (FDP) is under major pressure to address the issue of access. So far Chancellor Angela Merkel has signalled her resistance for additional changes to the new cannabis law. That said, the current situation in Germany, which is untenable for patients and doctors, as well as companies trying to enter the market and investing heavily, is unlikely to hold for even the next several years.

Problems with finding doctors and medical reimbursement under insurance have kept this patient population from growing the way it would otherwise.In late October, the news broke that two legal complaints had been unsuccessfully filed against the bid itself. Both parties’ complaints were dismissed. Yet there also appears to have been a third complaint that has actually devolved in to a real Klage – or lawsuit. Lexamed GmbH’s claim directly addresses issues expressed by many German-only firms this year. Namely that they were unfairly left out of the bid process because of a supposed lack of experience. As such it is likely to be closely watched by other existing German hopefuls.

This lawsuit has now formally delayed the announcements on the bid decision until at least after December 20th of this year, when the oral arguments will be heard in the case. A decision about the bid will go forward when this has been decided, by the beginning of 2018.

In the meantime? Cannabis imports are starting to enter the country. In late summer last year, Spektrum Cannabis, formerly MedCann GmbH, located just south of Frankfurt, received the first import licenses from the German government to bring medical cannabis into Germany from Canada. Both Aurora and Tilray were granted import licenses this fall.

There are 16 different kinds of cannabis on the market right now. And about 170 kilos of cannabis were imported into the country in the last year. There are also currently about 1,000 patients although this number is artificially low. Problems with finding doctors and medical reimbursement under insurance have kept this patient population from growing the way it would otherwise. There are easily a million patients in Germany right now who would qualify for cannabis if the system worked as it was originally intended in the legislation passed in January.

That said, despite the recent news that ABcann is “out” – at least for this round– apparently the pan-European bid process is still very much alive, despite many recent rumours that it was dead in the water. And plans also seem to be afoot for a separate and additional cultivation licensing round potentially as soon as next year. Details however are unclear and nobody either in the industry or the government is willing to be quoted or give any further information.

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

We use tracking pixels that set your arrival time at our website, this is used as part of our anti-spam and security measures. Disabling this tracking pixel would disable some of our security measures, and is therefore considered necessary for the safe operation of the website. This tracking pixel is cleared from your system when you delete files in your history.

We also use cookies to store your preferences regarding the setting of 3rd Party Cookies.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.