According to a press release published on Monday, SC Labs has acquired C4 Laboratories, a cannabis testing lab located in Scottsdale, Arizona. The acquisition means SC Labs has expanded their footprint into five states total. Originally based in California, the cannabis testing company now has locations in Arizona, California, Colorado, Michigan and Oregon.

Ryan Tracy, Founder/CEO of C4 Labs.

Ryan Treacy founded C4 Laboratories and has been a vocal advocate for product safety testing since 2016. As CEO of the company, he led the laboratory through regulatory upheaval and a lot of changes the state has seen since legalization. He also co-founded the Arizona Cannabis Laboratory Association and led lobbying efforts on behalf of patients and stakeholders to require lab testing.

He says they are excited to join forces, becoming the largest cannabis testing platform in the US. “Our combined leverage of top scientists with specialized cannabis testing knowledge and a leadership team of industry experts will allow us to do everything from harmonizing R&D efforts to improving the data experience to pushing for positive regulatory change,” says Treacy. All current employees of the C4 team will stay on, joining the new SC Labs team.

Jeff Journey, CEO of SC Labs

This acquisition represents another important milestone for the SC Labs expansion plan. Last year, they hired a new CEO, Jeff Journey, and launched their national hemp testing partnership based in Colorado. That, coupled with the expansion through Can-Lab into Michigan last year along with the C4 acquisition, SC Labs has expanded into three new states within the last twelve months.

Journey says they’re thrilled to acquire the C4 team and that they have shared values, a proven track record and good expertise. “With this acquisition, we can continue to expand best-in-market cannabis testing services and the opportunity to service multi-state growers and manufacturers,” says Journey. “It is truly an exciting time for growth, and we know that the C4 team will be an invaluable addition to our team, culture and operations.”

According to a press release published last week, SC Labs is in the midst of a multi-state expansion under new leadership. The company hired Jeff Journey as their new CEO, coming from a VP position at Thermo Fisher Scientific.

Jeff Journey, the new CEO of SC Labs

Last year, in what seemed like an initial move to establish the lab on a coast-to-coast level, SC Labs developed a hemp testing panel that covers a number of contaminants on a national regulatory level. The hemp testing panel they developed purportedly meets testing standards in states that require contaminant levels below a certain action limit.

Then in February of this year, the company announced a partnership with Colorado-based Agricor and Botanacor Laboratories, with the goal of establishing a national testing network, offering comprehensive cannabis and hemp lab testing. All three of those organizations are certified by the Colorado Department of Public Health and Environment (CDPHE) for compliance testing required for hemp products.

In the press release that was published last week, they hinted at another announcement coming soon: a new partnership with Michigan-based Can-Lab. This, coupled with hints at further expansion and their current presence in California, Colorado and Oregon, means Journey will have his hands full and his sights set on nationwide cannabis testing.

“We’re looking forward to partnering with cannabis and hemp brands at every stage of the supply chain to share our innovative and forward-thinking scientific expertise so they can deliver safe products to the marketplace,” says Journey. “As cannabis legalization expands across the country, the testing industry is rapidly shifting and scaling to meet both market and regulatory demands.”

The leadership team will still have a few familiar faces, such as Jeff Gray as chief innovation officer and Josh Wurzer as chief operating officer. “The most important assets we can offer as a multi-state operator are scientific expertise, financial stability, and unquestionable integrity, the principles on which SC Labs has long stood for and will continue to provide to our valued customers,” says Journey.

Canopy Growth Corporation, one of the largest cannabis companies in the world, announced the acquisition of Jetty Extracts this week for $69 million. Jetty Extracts was founded in 2013 and is now a leading cannabis brand in California and a top 5 brand in the vape category. The two companies plan to expand Jetty’s offerings in California, Colorado, New York and across the broder to Canada, according to a press release.

Canadian-based Canopy Growth is a massive international company that has been expanding its presence well beyond Canadian borders. For years now. Their medical arm, Spectrum Therapeutics, is a leading brand in Canada and Germany.

Some of the Jetty Extracts product offerings

Back in 2018, Canopy solidified a partnership and took considerable investment from Constellation Brands on a long-term play to enter the cannabis beverage market. Then in 2019, they began their aggressive expansion into the U.S. through the multi-billion-dollar deal with Acreage Holdings who, at the time, was the largest U.S. cannabis company. In April of last year, they inked a deal with Southern Glazer’s Wine & Spirits following the launch of their first CBD-infused beverage line sold in the United States, Quatreau.

Late last year Canopy Growth announced a deal to acquire Wana Brands, the number one cannabis edibles brand based on market share in North America. The latest acquisition of Jetty Extracts this week follows the same pattern of increasing their North American footprint in the cannabis market considerably.

David Klein, CEO of Canopy Growth, says the cross-border potential excites them. “”Canopy Growth is building a house of premium cannabis brands with a focus on the core growth categories that will power the market’s path forward, now including Jetty – a pioneer of solventless vapes,” says Klein. “There are significant opportunities for Jetty to scale at the state-level across the U.S. by leveraging Canopy’s U.S. ecosystem, and we’re actively working on plans to bring the brand to the Canadian recreational market.”

In this “Flower-Side Chats” series of articles, Green interviews integrated cannabis companies and flower brands that are bringing unique business models to the industry. Particular attention is focused on how these businesses integrate innovative practices to navigate a rapidly changing landscape of regulatory, supply chain and consumer demand.

4Front Ventures Corp. (CSE: FFNT) ( OTCQX: FFNTF) is a multi-state operator active in Washington, Massachusetts, Illinois, Michigan and California. Since its founding in 2011, 4Front has built a reputation for its high standards and low-cost cultivation and production methodologies earned through a track record of success in facility design, cultivation, genetics, growing processes, manufacturing, purchasing, distribution and retail. To date, 4Front has successfully brought to market more than 20 different cannabis brands and nearly 2,000 unique product lines, which are strategically distributed through its fully owned and operated Mission dispensaries and retail outlets in its core markets.

We interviewed Andrew Thut, chief investment officer of 4Front Ventures. Andrew joined 4Front in 2014 after investing in the company in 2011. Prior to 4Front, Andrew worked in investment banking and later moved on to public equity where he was a portfolio manager at BlackRock.

Aaron Green: How did you get involved in the cannabis industry?

Andrew Thut: I came at it from the investment side of things. I started my career as a junior investment banker right out of school and then I was a public equity analyst and Portfolio Manager. I ran small-cap growth portfolios for BlackRock where I was on the team for a better part of 11 years.

Andrew Thut, Chief Investment Officer of 4Front Ventures

One of my friends, Josh Rosen, who came from the finance industry, got interested in the cannabis industry really in 2008. He founded 4Front as a consulting company officially in 2011 and I came in as an investor. After that original investment, I left BlackRock and I was looking for something different to do. I was tired of chasing basis points and running public market portfolios. Josh said to me “This industry needs more talent,” and I became more and more involved at 4Front as the years went on. In 2014, I came into the business full time. Originally, I was someone that was kind of the gray hair in the room when we were applying for licenses. We had to go to different municipalities and convince them that we were going to be responsible license holders. I also spent a lot of time on the capital raising side for our business leveraging my career in corporate and more traditional public finance. These are incredibly complex businesses that require a fair amount of capital in some places. So, that’s how I originally got into the business.

These are complicated businesses in a lot of cases. The “sausage making” in cannabis is incredibly complicated. There’s friction at every step along the way. As an example, when you’re buying a building where you want to cultivate your product, you can’t get a mortgage from a typical bank.

While those of us that have been in the industry like to gripe and complain about it, this friction is also the opportunity. Because more traditional investors can’t invest in this industry yet, it allows us more time to build our businesses and have some protective moats around it from a competition standpoint until those folks do come in. So, all this friction is a pain and it’s brutal, but it’s also the opportunity here in cannabis.

Green: Can you speak to the transformation of 4Front from consulting to MSO?

Thut: The original business was consulting. Our original investor was sensitive about touching the plant – it’s one thing to offer services to a federally illegal business, it’s another thing to directly run a federally illegal business. For example, 4Front would have consulting clients that were interested in acquiring a license in Massachusetts. Because of our expertise and our standard operating procedures, we could apply for licenses in limited license states on behalf of our clients and help them show regulators competence and give the regulator’s confidence that these operators knew what they were doing. So, we would help our clients win the licenses and then once those licenses were won, our operations folks would come in and help them get up running.

When I came into the business we said, “well, geez, we have quite a track record helping clients win licenses and get open. If we’re good at winning these licenses and getting them open, why aren’t we just doing this on our own behalf?” So, in 2015, we shifted the business from consulting to being a multi-state operator. We leveraged our capabilities in regulatory compliance and winning licenses to go and get those on our own behalf. We also leveraged our financial expertise in M&A to add to our portfolio, so what we ended up with was a seven-state portfolio at the time.

Green: Chief Investment Officer is an uncommon title, even in the MSO space. What does your day-to-day look like?

Thut: I spend an awful lot of time helping management plot our strategy, and then figuring out how we are going to pay for our growth. Not only structuring finances for the company, but also having contact with our existing and new investors.

I spend a lot of my day to day thinking about where we want to be as a business and what geographies we want to be in. If you look at cannabis longer term, we have less interest in being cultivators or farmers. We think that’s going to be the most quickly commoditized piece of the value chain. We like retail as a business, but I think that we have less interest in managing hundreds of retail locations scattered across the country. We ultimately want to be a finished goods manufacturer. What we think is going to matter longer term is establishing low-cost production.

There is a lot of price elasticity in the end markets for cannabis meaning if you get customers a quality product at a much better price than the competitor, you’re going to take outsize market share. To offer that lower price, you have to be efficient. Over the years, we have figured out how to bring the labor cost out of our production. We have 25 different brands with 1000s of different SKUs of products that have dominant market share in states like Washington. And we’re now putting them into Illinois, Massachusetts, California, Michigan, and hopefully New Jersey.

Green: Do you have a preference towards acquisition, or do you seek growth through internal investments?

Thut: We are always weighing build versus buy. We want our products to have dominant market share, or very strong market share in every state we are in, and we have a lens towards what gets us there faster and most efficiently. For instance, we have two cultivation facilities and one production facility here in Massachusetts – about 15,000 square feet of canopy in the state. That will just about serve our three retail locations in Massachusetts.

Back to our bigger investment thesis, we believe that we should be a finished goods wholesaler in every state that we’re in. We know our products are incredibly well received and we know that consumers love our price point. In Massachusetts, for instance, we’re currently evaluating if we need more capacity from a cultivation standpoint and a production standpoint. And if we do where do the lines cross in terms of whether we should build versus buy that additional capacity?

We are currently in five states, including our facility in Washington has dominant market share in one of the toughest markets in the world for cannabis – somewhere close to 9% market share in Washington. Our brands are in the top 10 of every single category from flower to vapes, to edibles everything across the board. And what we’re doing our strategy is simple. It’s taking those tried-and-true products and operating procedures that have been so effective in Washington, and we’re replicating them in other states where we have licenses: Massachusetts, Illinois, and Michigan, California and hopefully New Jersey. We’re looking for more state, but we want to be deep in the states we’re in.

We also have a lot of confidence that you know, having been having translated some of these, having been able to effectively take our Washington success story and port it to other states. We’re looking for other states to sort of bring into the portfolio because we feel like we’re in a position now to stamp it out.

At our facility in Washington, which is the number one edibles manufacturer in that state, we produce the edible Marmas which is our the number one selling gummy in Washington. We produce 3,500 boxes of those in one shift using 25 people in Washington. Our facility is one of the lowest cost producers in the country.

We are opening what we think is going to be a very disruptive facility in Southern California right now. The facility is 170,000 square feet of purely automated finished goods production. So, rather than making 3,500 boxes of our gummy squares in one shift using 25 people, with the automation that we have in California, we can make 30,000 boxes. So, 10x one shift for the same number of people. We look more like the Mars Candy Company than most investors would think of when they see a typical cannabis company. We’re bringing that kind of scale and automation.

Green: What are some of the industry trends that you’re watching closely?

Thut: We keep a close eye on limited license states. States like Massachusetts and Illinois. For various reasons Massachusetts is very tough to get zoned. So, there’s going to be a limited number of players in a state like Massachusetts, which means you can have pretty good moats around your business and pricing will hold up over several years. We love limited license states like that, where price is going to hold up. On the other hand, we’re not afraid to enter a state like California where we think our low-cost production expertise uniquely qualifies us to go into a huge market like that and be disruptive and take a lot of the pie.

“You’re starting to see the market expand. There’s some anecdotal evidence that we’re taking a fair amount of share from the beer industry.”What we’re seeing in terms of industry trends, particularly on the THC side of this business, has just been phenomenally strong. You’ve had robust medical markets where, by and large, we’re seeing those dominoes start to fall quickly and going recreational. When that happens, the size of the market increases – call it from 2% of the population to as much as 10% of the population. So, from a state regulatory standpoint, having states go form medical to adult use is a huge deal in terms of the market opportunity.

We’re also seeing states get a lot more comfortable with the idea of selling cannabis. I’ve been around for close to seven years in this industry. When I started and I went into a municipality, and I said we wanted to open a cannabis store you’d have people following me to my car with pitchforks. As these municipalities open and public acceptance comes around, people are realizing that these stores are providing jobs and providing a good tax base for communities. So, the acceptance of cannabis has a snowballing effect that just continues to roll.

It’s not just the ultra-frequent users of cannabis who are totally driving the bus in terms of the demand growth for your business. You’re starting to see the market expand. There’s some anecdotal evidence that we’re taking a fair amount of share from the beer industry. So, the fundamentals of this industry are phenomenal. I think that we’re probably in the second inning of what is a mega-trend of legalization of cannabis and the investment opportunity here.

Green: I think one of the interesting things about the fundamentals is you’ve got this hardship of 280E, that all the companies are facing, and yet you still have groups that are surviving, profitable and growing. What are your thoughts on 280E’s effect on cannabis businesses? Do you foresee anything happening there?

Thut: There was a huge liquidity crunch in cannabis in 2019, meaning it was hard for people to come up with capital to grow their businesses. You had a bunch of companies that had licenses who didn’t really know how to operate and weren’t really focused on profitability. That liquidity crunch of 2019 made people get religious about being profitable and being efficient with capital allocation. Fast forward to 2021 and if you look at the top 10 cannabis MSOs in the US, I think we’re all profitable.

So, here you have an industry with accelerating top line growth and they’re already profitable. That profitability should only improve as you’re able to leverage your operating expenses and that’s a unique thing. When the internet craze was started in 1999 you had companies that a weren’t profitable, didn’t have business models, and no one really knew what they wanted to be. You have companies here in cannabis that are growing the top line 50% a year, and they’re profitable, and they’re trading at under 10 times EBITDA, which is totally disjointed.

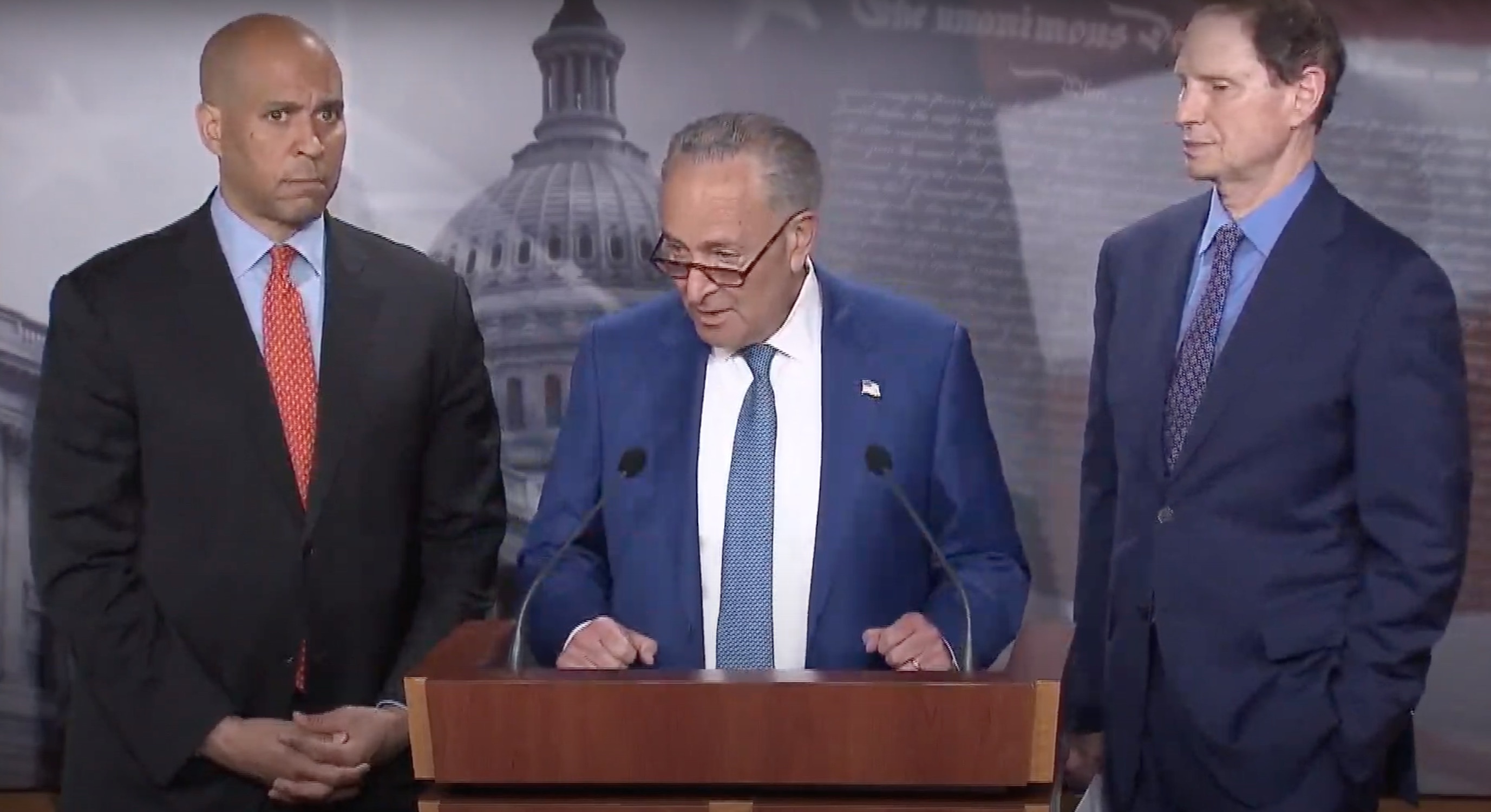

Sen. Schumer unveiling the Cannabis Administration and Opportunity Act

So, that leads me to your question on to 280E. 280E has been a problem. Banking has been a problem. Having to list our companies over the counter instead of on exchanges like the NASDAQ and NYSE – that’s been a problem in terms of attracting capital. But the good news is Senator Schumer, Senator Booker and others have put out some bold initiatives on what they want to achieve from a legalization standpoint. From an investment standpoint, the biggest thing that investors should be focused on is access to banking, which is included in the senators’ proposed legislation.

Once we get access to banking services, the federal government is basically acknowledging cannabis as an industry will be able to not only have more traditional financing for our growth, but it will also lead to uplift into exchanges and real institutions like the Fidelity’s and the BlackRock’s of the world being able to come and invest in these companies. It also acknowledges 280E is an antiquated law. Getting rid of 280E will give us a much lower tax rate and will allow us to have a bigger proportion of our pretax cash flow into growing our businesses rather than having to go outside for that funding. My crystal ball is probably no better or worse than others in the industry, but if you fast forward 18 months to two years, I have a tough time seeing 280E still in place.

Green: Last question here. What’s the thing you’re most interested in learning about in the cannabis industry?

Thut: I’m just fascinated to see how these various business models will play out. People are placing bets on picks and shovels. People are placing bets on whether being a finished goods manufacturer works. People are placing bets on whether a retailer business model is going to win the day.

If you look at the leadership in the cannabis industry today, it’s totally different than it was four years ago. People that were foregone winners four years ago like MedMen had to do significant recaps. I put Acreage in that sort of bucket too. The leadership had shifted and so I’m really curious to see just from an intellectual standpoint, how this business evolves.

I sometimes scratch my head, you know, do you really want to be a cannabis company with 200 retail locations? You’re going to have a tough time growing same store sales in three to five years in 200 retail locations. So, I’m just most curious in proving out our thesis of being finished goods producers and low cost finished goods producers in the value chain. I’m most curious in seeing how that plays out. I think we are seeing our strategy play out in the most competitive markets in the world. We have a high degree of conviction that we’re on the right track here, but our eyes are always open and we’re always making little pivots here and there trying to make sure to stay on top of the sweet spot in the value curve.

If you describe the cannabis industry generically and you didn’t say cannabis, you said “widget” I think it’s the most fascinating Business School case ever presented. If you’re taking this market that already exists, it’s just illegal. So, all it needs to do is switch from the black market to the legal market and then you’re always trying to plot a course and steer the ship towards where the highest value creation can be. So, I’m fascinated to see how it’s going play out here.

Green: That concludes the interview. Thanks Andrew!

In this “Flower-Side Chats” series of articles, Green interviews integrated cannabis companies and flower brands that are bringing unique business models to the industry. Particular attention is focused on how these businesses integrate innovative practices in order to navigate a rapidly changing landscape of regulations, supply chain and consumer demand.

The California legal flower market is the largest in North America. According to recent BDSA data, monthly cannabis sales in January 2021 were $243.5 million. Flower sales represented 35.6% of overall sales, or about $87 million, representing a $1 billion yearly run rate for 2021 flower sales in California.

Union Electric was founded in California in 2020 as one of OpenNest Labs’ first incubator brands. Its model is uniquely asset-light, and focused on filling an area of opportunity with a consumer-first approach, aimed at an underserved market: the working-class customer. The name Union Electric was inspired by the punching-in and punching-out aspect of working a union job — more specifically, the average cannabis user’s job. The name also represents the brand’s union of stakeholders: Customers, cultivators and retailers alike, working together to provide affordable, quality products.

Max Goldstein is the CEO of Union Electric and Founding Partner at OpenNest Labs. Max incubated Union Electric at OpenNest Labs, a cannabis venture studio he helped co-found, and launched the brand in 2020 the day after COVID lockdowns began in California. Prior to Union Electric, Max worked at Google managing a 90 person, 12-market partnerships team.

Aaron Green: How did you get into the cannabis industry?

Max Goldstein: I’ve had a fun entrepreneurial and professional journey. I started my career in my 20s with Google working in the marketing department sitting at the intersection of new product development and customers. During that time, I really learned the ins and outs of bringing products to market and building brands. I had to understand how to value and champion the customer, or the user. At Google, I was sitting at the intersection of people building products that are affecting billions of people’s lives and users and customers that potentially have really cool insights and feedback. It was an incredible learning experience. I was able to focus on what I’m good at, which is that early stage of businesses and most importantly, listening to the consumer and developing products and services that they ultimately really want.

Max Goldstein, CEO of Union Electric and Founding Partner at OpenNest Labs

Near the end of 2018, I co-founded OpenNest Labs, a cannabis venture studio. We came together as a four-person partnership to form OpenNest, as an assortment of skill sets, with all of us contributing an area of focus that we could really combine our experiences to take focused and concerted efforts at building brands that resonate with different consumers across various form factors in cannabis and health. My partner Tyler Wakstein has been in the cannabis industry for several years and helped launch the brand, hmbldt (which is now Dosist) and a number of other projects in the cannabis space.

Green: Was Union Electric an incubation project out of OpenNest?

Goldstein: Yes. Union Electric is the first project we incubated out of OpenNest. We launched the day after the pandemic. So, it was interesting timing.

At Union Electric we’re focused on the core, everyday consumer of cannabis. I think a lot of folks, particularly the new money that have come into the industry, have often focused on new form factors or things that they think the new cannabis consumer is going to enjoy or appreciate. Because quite frankly, that’s their level of familiarity with the industry. For us at Union Electric, we want to hit the end of the market with exactly what they want and that is high-potency, affordable flower with a brand that really stands for something and has values.

Union Electric is positioned as an advocate for the legal cannabis industry as a whole. We look at the stakeholders and the work that needs to be done across the board. The idea of just being one member of the value chain and not trying to ultimately uplift and elevate everyone in that value chain, it’s just not going to work in cannabis. We’ve seen a lot of people trying to go at this alone and I think the pandemic, if anything, showed that you’re only as good as your partners. We truly believe that the investment in our partners, in the local communities and everyone that’s really touching this industry is critical to ultimately building success for one company because a rising tide raises all ships.

Green: How did you settle on the name Union Electric?

Goldstein: One of the things that we wanted to do was focus the brand on who we see as the core consumer, which is somebody that is working hard, like a shift worker punching in and punching out and putting in the long hours on a daily basis and using cannabis as a critical part of their personal wellness and relief. There are elements of that which we certainly want to tap into. The “Union” represents our stakeholder approach, which is, all of us are in this together and our tagline “roll together” represents that. The “Electric” part is what we’ve seen cannabis sort of representing culturally, and for people more broadly. This is an exciting product that’s going to change a lot of people’s lives and, and I just don’t think there’s anything else in our lifetimes that we’re necessarily going to be able to work on from a consumer-packaged goods perspective, that’s going to change as many people’s lives. It’s electric. That’s how we came up with the name.

The coloring and a lot of the brand elements that we focused on were about providing transparency and simplicity to the marketplace: big font and bold colors. There are little nuances with our packaging, like providing a window just so people can see the flower on our bags. We look at the details and made sure that we’re ultimately out of the way of the consumer and what they want, but providing that vehicle that they’re really comfortable with.

Green: You have an asset-light business model, focusing on brand and partnerships. How did you come to that model?

Goldstein: I think everyone who’s operating and working in cannabis right now is looking at strategy and what the model is that’s going to work for them. We’re ultimately going to find out what works, which is why this industry is so fun and exciting. Our specific approach is really under the assumption that vertical integration in a market that’s maturing as quickly as California is going to be hard, if not impossible – it’s just too competitive. There are too many things going on in order to be successful in California. You have to be really good at cultivation, really good at manufacturing, really good at distribution, and then ultimately, you have to be able to tell a story of that process to ensure sell-through and that you really resonate with the consumer.

I think the big, missed opportunities that we’re seeing are that a lot of great cultivators are not marketers or storytellers. They really do need people that are there to help amplify and provide transparency to their stories. There are amazing stories out there of sacrifice and what cultivators have done to create a new strain. We all enjoy Gelato. What’s the process to make that happen or to create any other new strain? It’s fascinating. It’s too hard for a lot of these cultivators to go out and tell that story themselves. So, we act as a sales and marketing layer on top of the supply chain to provide visibility, transparency and trust with the consumer so that they know who grew their product, how it was grown, when it was cultivated and that they can build a real strong relationship with that cultivator as well.

It’s also hard to be a brand that’s using 19 different suppliers, selling the same genetics and expecting the same results. As an example, we’ve gotten Fatso from one of our partners, Natura. We’ve also gotten Fatso from Kind Op Corp (fka POSIBL). We renamed one of the strains – by adding a number on the end – just so that the consumer knew that we’re not saying that this is the same product, because it’s not. It’s from a different farmer and there’s going to be differences. While it does create a little bit more complexity for the consumer, we ultimately believe that every consumer has a right and will expect to know that type of information in the future.

Green: You launched Union Electric one day after the COVID lockdowns began in California. How did you navigate that landscape?

OpenNest Labs Logo

Goldstein: A lot of praying to the cannabis gods! It was really an incredibly challenging and difficult time. We were all concerned about the impacts of the virus. There were moments where we didn’t even know if dispensaries would be open, particularly in states that just legalized. You went from something being completely illegal to an essential business in 12 months. As a team, we were just trying to hold on to our hats and focus on product and partnerships.

Fortunately, with a brand like ours and the price point that we’re operating at, we just needed to consistently be on the shelves and available, and to be present with the bud tenders. So, we focused on that and shoring up our supply chain and just trying to wait it out. COVID forced a lot of cannabis companies to make a lot of decisions quickly and I think in some ways, because we have not been in the market for 24 months under one paradigm, we were pretty quick to be able to adjust and keep the team super lean to fit the emerging and rapidly changing environment. We learned a lot. We focused on partnerships and we leaned into the model that we set out to build which is being asset-light and focusing on the sell-through.

Green: I understand you have a 2% giveback program. Tell me about that.

Goldstein: The 2% giveback program was something that we wanted to put on the bag from day one. It’s on every bag that we made and put out into the market. We’ve seen a lot of cannabis companies come in and invest tens and hundreds of millions of dollars in infrastructure. Then, month 24 they realize “oh, crap, I gotta figure out what I’m going to do to get back and actually tap into the issues that are most important to cannabis consumers.” These are issues like social equity, equitable development of the industry, and ensuring that cannabis companies and its owners are active, responsible members of society.

What we’re going to focus on with our giveback program is working with our supply chain partners. We highlight the local communities, because when you look at the landscape in California, two thirds of its municipalities still don’t allow cannabis operations. We’re in a heart and minds battle still, even here in California, just proving that the operators here are not criminals and that they’re not going to bring negativity to local communities.

As we scale in California and scale to other states, the giveback program for us is a platform and a medium to work with our supply chain partners to make sure that we’re giving back and investing every step of the way. As founders and operators, it’s how we show that we are being mindful of the importance of equitable development of the industry. Ultimately, prosperity is going to come if everyone is getting a piece of the pie.

Green: What are you most interested in learning about?

Goldstein: I’m a student of history (I was a history major) and I was very fortunate to be part of a big evolution of technology development starting in 2011 working at Google and other tech companies. In some ways, this is the second generational industry that I’ve been a part of, and I have a lot of regrets about how the first one developed – not that I necessarily was the chief decision maker. The idea that large tech companies would always act responsibly (i.e. “Don’t be evil”) didn’t really pan out. I think it was an ignorant thought process as a person in my young 20s.

What I’m most interested in learning is: Can the cannabis industry develop consciously? Can you keep the greed and the things that bring industries down at bay? How can I, as an operator, be the best facilitator of that future? I’m always thinking how I can continue to bring in the people around us and around me as the CEO of Union Electric to ensure that we’re always focused on that.

Green: Great, that concludes the interview. Thank you, Max.

Goldstein: Thanks Aaron.

From Union Electric: Union Electric Cannabis will be offering their first Regulation CF crowdfund raise in an effort to give everyday consumers a stake in one of California’s fast growing cannabis brands. Due to the ever-evolving legal status of cannabis in the US, there have been very few opportunities for individuals to invest early on in American cannabis brands. This decision to give everyday cannabis smokers access to investing in their favorite cannabis brand (for as little as $100) is a natural manifestation of Union Electric’s mission: Collective power and championing accessibility for the plant. You can learn more about their raise by visiting https://republic.co/union-electric

As the cannabis industry — now estimated to be worth more than USD 200 billion — continues to erupt around the world, Europe is about to take off.

This draws a parallel with the watershed legislative events of November 2012, when Colorado Amendment 64 and Washington Initiative 502 were implemented. These two bills kicked off a wave of medical and adult use acceptance in the United States. Europe’s medical referendums which started in 2017-2018 and the recent December 2020 United Nations acceptance of medical attributes of cannabis will do the same in that continental marketplace. Europe is following science and studying popular opinion about cannabis, just like the United States nearly a decade ago.

In many ways, the American “medical” market has been a political ploy, while the European market is truly medical in every way. Distribution through pharmacies and mainstream channels is the wave of the future. This method of distribution will both increase access and taxable bases quicker than the U.S. “medical” dispensary model. People who truly need cannabis should not be hindered by any rules or regulations to get the medicine, and the U.N. has paved the way for access while the U.S. still awaits rescheduling.

Markets in Europe require EU-GMP manufacturing for a variety of different products

The road to medical cannabis in Europe is more stringent than that of the U.S. and Canada. This is because most European markets have strict medical standards and medicines must be produced in European Union Good Manufacturing Practices (EU GMP) certified pharmaceutical manufacturing facilities. This is the same standard that all medical Active Pharmaceutical Ingredient (API) producers are held to.

Both Canadian companies, who have just launched extraction with Canada’s “Cannabis 2.0”, and American manufacturers alike are unfamiliar with pharmaceutical API production. Some argue that food-grade GMP standards are the most similar to already-existing systems in the U.S. and Canada. However, the meaning of “medical” is clear in Europe — it means medical. Improving access for patients to products will be the central challenge for Europe over the next few years as patient growth increases.

Europe is also embracing its potential adult use markets. First came Denmark, then Luxembourg, and now the Netherlands are all beginning to engage with the question of adult use cannabis legalization. We expect Portugal will soon join this list. After all, in a post-coronavirus world, every country will be looking for a means to grapple with a devastated economy and to boost employment to widen its taxable base.

The United States was supposedly founded by Puritans escaping gregarious Europeans. Now it’s likely America will legalize cannabis within the year and Europeans will be left asking, “Why them and not us?” And it will become harder to explain why such potential for growth in employment and increased tax revenue isn’t being taken advantage of as Europe begins to emerge from lockdown. It would be shrewd to expect a wave of European adult use kick-offs in 2022.

It’s anyone’s guess what retail will look like for the cannabis market in Europe as it evolves

It is clear that 2021 is setting a blistering economic pace: from mergers and acquisitions to monster capital raises, to increased debt raises to the hot special purpose acquisition companies (SPACs) London Stock Exchange (LSE) up listings and initial public offering (IPO) fever. This year will be a cannabis-fueled explosion that Europe will not be able to ignore. With Canada, the U.S. and Mexico all likely to legalize cannabis in the near future, how long will it be before South and Central America follows suit? And then, how long for this wave to reach Europe?

The real answer is, it’s already here. Early adopters of cannabis overbuilt as the Canadians were given more money than they deserved, while the U.S. market was largely fueled by private equity and proved that it could be the biggest and best-run model. Europe will follow its own path by acknowledging the failures and successes of these markets, blending them to form its own unique European model.

The American dispensary will eventually pop up in Europe in a form similar to the current social clubs of Barcelona and coffee shops of Amsterdam. Possibly specialized pharmacies will carry more cannabis products, but it’s too early to call — countries are only just beginning to figure out how cannabis rules might be shaped to fit their needs and values.

2021 could be a decisive year for the European cannabis market

There are greater issues people are dealing with in the age of COVID-19, but that will change. Economic recovery, the need to provide medicine more quickly and affordably, social reform, green projects and many more pressing issues will become thematic of a post-COVID world; a set of themes for which a cannabis-shaped solution checks many of the necessary boxes.

There is a certain misrepresentation of cannabis as a panacea, able to cure every medical ailment and remedy every social problem if only it were legalized more broadly. While cannabis certainly is not a cure-all, it can fix many issues facing governments today. People were grateful for cannabis during these troubled times with cannabis stockpiling and usage through the roof in the early stages of the pandemic. As a result, 2021 has the potential to shatter old establishment perceptions as more consumers speak out.

Now, it is only a question of how the individual and collective European nations choose to regulate expansion across the continent. And the power to create a truly world-beating cannabis model is in their hands; without the international market differences and troubles that plague the North American sector, there will be virtually no limits to cannabis expansion throughout Europe if those in charge believe it to be so.

Charlotte’s Web Holdings, the company that just about launched the entire CBD industry, announced this week that they have just been approved for registration on Health Canada’s list of approved cultivars (LOAC) for 2021. Three of their proprietary hemp cultivars have made the cut, gaining the company access to the Canadian market.

Jared Stanley, co-founder and chief cultivation officer at Charlotte’s Web, says they plan to lead the market in Canadian hemp-derived CBD products. “The majority of approved cultivars on the LOAC to date have been for industrial hemp grown to produce food, fiber, and animal feed,” says Stanley. “Now our approved cultivars are paving the way for full-spectrum hemp CBD demand in Canada and most importantly, will provide access to Charlotte’s Web products in Canada.”

Largely due to the difference in regulatory approaches between Canada and the U.S., the CBD product market in Canada is somewhat small. Health Canada currently regulates CBD products the same as products containing more than 0.3% THC. In the U.S., a checkerboard of state laws, the 2018 Farm Bill and the subsequent state hemp programs led to massive growth for the CBD product marketplace.

Charlotte’s Web is one of the leading hemp-derived CBD companies operating in the United States. With the soon-to-be expansion into Canada, the company hopes to develop a global footprint, says Deanie Elsner, president and CEO of Charlotte’s Web. “Today, Charlotte’s Web is the leading hemp wellness company in the U.S. with the most recognized and trusted hemp CBD extract,” says Elsner. “We aspire to be the world’s leading botanicals wellness company, entering countries with an asset light model where federal laws permit hemp extracts for health and wellness. Israel and Canada are included in the first steps of our international expansion.”

The unusual nature of 2020 gave rise to a reciprocally roller-coaster-like cannabis market. Cannabis was cemented officially as an essential industry with the rise of COVID-19, and November elections resulted in even more United States markets welcoming medical and adult-use sales.

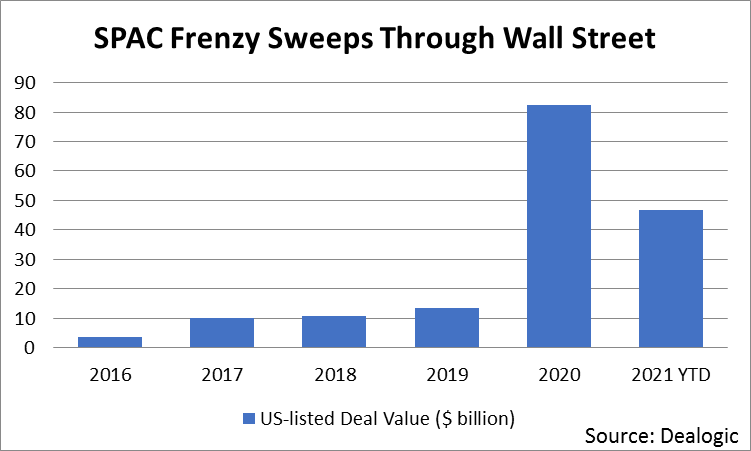

The stagnant cannabis stock market of 2019 became a thing of the past by the end of 2020. Throughout the course of last year, bag holders anxiously watched cannabis options creep back up. Now, nearly two years since market decline in 2019, the cannabis stock market is exploding with blank checks and buyout fever. Much of this expectant purchasing is due to Canadian companies considering U.S. market entrance. Combined with the recent surge in the use of special purpose acquisition companies (SPACs) to invest, this has led to an increase in asset prices.

A SPAC is defined as “a company with no commercial operations that is formed strictly to raise capital through an initial public offering (IPO) for the purpose of acquiring an existing company.” Though they have existed for decades, SPACs have become popular on Wall Street the last few years because they are a way for a company to go public without the associated headaches of preparing for a traditional IPO.

In a SPAC, investors interested in a specific industry pool their money together without knowledge of the company they’re starting. The SPAC then goes public as a shell company and begins acquiring other companies in the associated industry. Selling to a SPAC is usually an attractive option for owners of smaller companies built from private equity funds.

The U.S.-Canadian market questions that this rising practice asks are: Can Canadian companies enter a bigger market and be more successful? Is it advisable for U.S. companies to sell their assets to Canadian corporations whose records may be marred by a history of losses and a lack of proper corporate governance? Regardless — if both SPAC’s and Canadian bailout money is here, what comes next?

What is Driving this Bull Market?

Underpinning these movements are record cannabis sales internationally, making last year’s $15 billion dollars’ worth of sales in the U.S. look small in comparison. New markets have opened up in various states and countries throughout 2020, and that trend is only expected to continue. New demographics are opening up, especially among older age groups. This makes sense, as most cannabis sales — even in a recreational setting — are people treating something that ails them like insomnia or aches and pains.

Cannabis is set to take off, and we are entering only the second phase of its market expansion. The world is becoming competitive. Well-run companies that are profitable in key markets are prime targets for bigger, growing companies. At the same time, the world of SPACs will continue to drive valuations. Irrespective of buying assets, growing infrastructure is and will continue to be greatly needed.

The Elusive Profitability Factor

When Canada blew up, one of the biggest changes was companies began focusing the year on cost cutting and — most importantly — profitability. Profitability became the buzzword. But bigger companies are on the search for already-profitable enterprises, not just those that have the potential to be. However, profitability is currently still unobtainable in Canada. Reasonable forecasters should expect this year will show a few companies getting bailed out while many others will be forced to either merge for survival or declare bankruptcy.

An ideal company’s finances should highlight not only revenue growth, but also profitability. Attention should be focused on how well businesses are run, and not on how much money they have the potential to raise or spend. Over the years, there have been many prospective companies that spent hundreds of millions only to barely operate, and are now shells in litigation. Throwing money at any deal should have been a lesson learned in the past, but SPACs are tempting because they are trendily associated with new, interesting management styles and charismatic businesspeople.

Companies should be able to present perfect and clear financials along with maintenance logs for all equipment. In today’s day and age, books must be stellar and clean. As money pours into SPACs, asset valuations for all qualities of companies will rise. The focus instead becomes about asset plays, which will cause assets to continue rising as money is poured into SPACs.

Once upon a time, if number counters presented a negative review or had to dig too much, executives would turn a cold shoulder on investment. But in the age of SPACs, these standards of evaluation will be greatly undervalued. Aging equipment and reportability of every piece of equipment may or may not be properly serviced and recorded in a fast-moving market. Costs of repair or replacing equipment that isn’t properly maintained may be a problem of the past. Because when money comes fast, none care for the gritty details.

Issues for SPACs

Shortage of talent and training has become a big concern already in the era of SPACs. How many quality assets are out there? Big operators in the U.S. are content and don’t see Canada as an enticing market to enter. So, asset buys are likely to primarily be in the U.S. Large companies like Aphria may buy out some of the major American players, but most Canadian companies will use new funding rounds to pay down debts. Accordingly, they will then be forced to piece together smaller operators as a strategy.

A cannabis company’s personnel and office culture are very important when looking to integrate into a larger corporate culture. Remember, it’s not just the brick and mortar that is being invested into, it is also the people that run a facility. Maintaining employee retention when a deal occurs is always critical. Your personnel should be highly trained and professional if you want to exit. Easy to plug-in corporate structures make all the difference in immediately gaining from the sale or having to retool the shed and bring in all new people.

The rise of the SPAC-era and Canadian entry into the U.S. market will cause asset increases, but it is only the second chapter in the market expansion of cannabis. Proper buys will nail profitability, impeccable books, proper maintenance records and will have created an efficient corporate structure with talented personnel. The rest will be overpriced land buys that will require massive infrastructure spending. The basics of a well-run organization don’t change. The cannabis market is going to ROAR, but don’t worry if the SPACs pass you by- they are buying at the start of cannabis only.

Cresco Labs, one of the largest multistate operators (MSOs) in the country, announced the acquisition of Bluma Wellness Inc., a vertically integrated cannabis company based in Florida.

Cresco Labs, with roots in Chicago, Illinois, operate 29 licenses in 6 states across the United States. With this new acquisition, Cresco Labs solidifies their ubiquitous brand presence in the most populous markets and cements their position in Florida, a new market for them.

According to the press release, the two companies entered an agreement where Cresco will buy all of Bluma’s issued and outstanding shares for an equity value of $213 million. They expect the transaction to be completed by the second quarter of this year.

Charles Bachtell, CEO of Cresco Labs, says their expansion strategy is based largely on population. “Our strategy at Cresco Labs is to build the most strategic geographic footprint possible and achieve material market positions in each of our states,” says Bachtell. “With Florida, we will have a meaningful presence in all 7 of the 10 most populated states in the country with cannabis programs – an incredibly strategic and valuable footprint by any definition. We recognize the importance of the Florida market and the importance of entering Florida in a thoughtful way – we identified Bluma as having the right tools and key advantages for growth.”

Bluma Wellness operates through its subsidiary, One Plant Florida, which has 7 dispensaries across the state and ranks second in sales in the state. They also have an impressive delivery arm of their retail business, deriving 15% of their revenue from it.

Cannabis presents a plethora of challenges for entrepreneurs not seen in more traditional industries. Akin to the dot-com boom of the early 2000s, the cannabis industry has seen an astonishing flurry of business over the past decade. Within this dynamic landscape, new cannabis companies come and go on a near-daily basis.

To capitalize on novel markets’ potential, hopeful entrepreneurs from all walks of life have “jumped headfirst” into the cannabis space. This new breed of entrepreneurs must not only be smart, but they must also be challenging. Yet, as the cannabis industry evolves under the forces of legalization and innovation, our understanding of what defines cannabis entrepreneurs continues to change.

Cannabis businesses are shaped by the regulations, challenges and opportunities of specific market niches. As such, cannabis entrepreneurs have evolved with the environments in which they do business.

California & Proposition 215

California paved the way for the industry of today by legalizing medical cannabis in 1995. Since the passage of historic Proposition 215, cannabis has continued to gain momentum across the globe. This progress has happened through the visions and hard work of small business owners.

The early days of legal cannabis in California are now criticized for their lack of regulation. During the late 1990s and early 2000s, all you needed to start a cultivation business in California was a place to grow a garden. While early dispensaries did need local business licenses, they could legally purchase and sell untested products from unlicensed growers.

The genealogy of the modern cannabis industry can be traced directly back to the days of California’s Prop 215. During this era, the first cannabis dispensaries were founded – this model has since been replicated thousands of times. Also, the Prop 215 model gave rise to America’s first legal, commercial cannabis farms.

Cannabis entrepreneurs in California’s medical space focused primarily on developing the blueprints for a brand-new industry. To this end, they did not have the time or luxury to finetune the businesses for such things as operational efficiency and brand awareness. Even more, these people did not have to deal with such complexities as employee screening, product testing and seed-to-sale tracking.

Medical Cannabis Entrepreneurs

New medical markets stand in stark contrast to those seen in the early days of California. To this end, today’s medical markets operate within a web of stringent government regulations. For entrepreneurs, these rules set forth major emphases on both compliance and technology.

The Pennsylvania medical cannabis industry provides an excellent platform for understanding how the regulatory system of a market shapes entrepreneurial paths. For instance, medical cannabis cards are only issued to patients that meet the minimum criteria of 23 qualifying conditions, including severe conditions like aids, cancer and epilepsy. Beyond that, cannabis dispensaries in Pennsylvania must meet a slew of challenging criteria to operate and pay large sums of money in licensing fees.

To handle the regulatory requirements in places like Pennsylvania and remain profitable, medical cannabis entrepreneurs are incredibly dependent on technology. To this end, dispensaries utilize point-of-sale (POS) and seed-to-sale software to track inventory and stay compliant carefully. Even more, they use state-of-the-art security systems to safeguard their operations.

Cannabis entrepreneurs in medical markets must be able to run compliant operations and support their businesses with requisite technology. These elements stand in stark contradiction to the “wild west” mentality that pervaded the early industry. As such, it’s safe to assume that the rules of today’s markets force entrepreneurs to be more professional than in the days of CA Prop 215.

Adult-Use Cannabis Entrepreneurs

The most considerable difference between medical and adult-use cannabis companies has to do with their available customer base. Importantly, adult-use cannabis companies are only bound by minimum age requirements and state borders. Furthermore, limited restrictions on licensing create highly competitive markets that require sophisticated sales and marketing operations.

As there are no limits on potential customers, and limited regulations on license counts, business opportunities in adult-use markets are primarily directed by supply and demand rules. Because competition is the driving force in adult-use markets, entrepreneurs in this vertical have a good deal in common with peers outside the cannabis industry.

Perhaps the most defining characteristic of adult-use entrepreneurs is an emphasis on branding and marketing. As adult-use markets mature in places like Colorado, a phenomenon known as “brand concentration” occurs when a few companies come to dominate a majority of the market. As smaller companies fight for market share, they must develop professional brands that appeal to a broad customer base.

Cannabis entrepreneurs in adult-use markets must master the skills required in medical cannabis while also expanding their knowledge base in modern business dealings. Of these, the development of professional brands is one of the most defining characteristics of adult-use entrepreneurs.

It’s astonishing to see how much the cannabis industry has grown and matured looking back just a few short years. As business opportunities come about with new legalization efforts, entrepreneurs quickly rise to take advantage of untapped markets. As the cannabis business continues to evolve with the times, entrepreneurs must pivot to stay compliant, relevant and successful.

While the early Prop 215 market in California barely resembles today’s industry, it’s important to remember where we came from. Namely, our understanding of the contemporary cannabis business results from everyone who came before us. As the industry progresses, we will continue to complement established best practices with the requisite innovations that come with new opportunities.

This website uses cookies so that we can provide you with the best user experience possible. Cookie information is stored in your browser and performs functions such as recognising you when you return to our website and helping our team to understand which sections of the website you find most interesting and useful.

Strictly Necessary Cookies

Strictly Necessary Cookie should be enabled at all times so that we can save your preferences for cookie settings.

We use tracking pixels that set your arrival time at our website, this is used as part of our anti-spam and security measures. Disabling this tracking pixel would disable some of our security measures, and is therefore considered necessary for the safe operation of the website. This tracking pixel is cleared from your system when you delete files in your history.

We also use cookies to store your preferences regarding the setting of 3rd Party Cookies.

If you disable this cookie, we will not be able to save your preferences. This means that every time you visit this website you will need to enable or disable cookies again.