Let’s just say it. There is an undeniable chaos in the cannabis industry. It doesn’t matter if you’re a big or small operator, it’s likely that you don’t have a documented system for creating and managing ever-changing SOPs or for consistently training all employees on the most current versions of those SOPs. This chaos is often the result of rapid growth, mergers and acquisitions, and the ever-present turnover in our industry. When department leadership changes, and it often does, established policies and procedures are often left behind. In some cases, this is a positive sign of growth. As a company outgrows SOPs and as it develops more sophisticated ways to cultivate, extract, process, manufacture, package and sell cannabis and cannabis products, inevitably, the old ways of doing business need to be replaced. For those operators who have prioritized operational excellence, whether they want to position their company for new investment, merger or acquisition, or just want to create a consistent and standardized, branded product, it’s critical to get control of SOPs, training and documentation.

By standardizing and documenting safety procedures, manufacturers mitigate the risk of cannabis-specific concerns

As with most big goals, to obtain operational excellence, you need to break the goal into manageable steps. Assuming you have accessible quality policies and procedures in place, properly training employees when they first start work and on an ongoing basis as policies and procedures change is the number one key to successful operations. When employees know how to do their job and understand what is expected of them, they are positioned for success. When employees are successful, it follows that the company will also be successful. Documenting operations is a second important step in obtaining operational excellence. While training and documentation appear to be different, in best-practice organizations, they are inextricably linked.

One Set of SOPs

Those of us who have been in the cannabis industry for a while have experienced firsthand or heard stories of facility staff working off of two sets of SOPs. There’s the set of SOPs that are printed or digitally available for the regulators, let’s call them the “ideal” set, and then there are the SOPs that actually get implemented on a day-to-day basis. While this is common, it’s risky and undermines the foundation of operational excellence. Employees often know there are two sets of SOPs. Whether they express it or not, many are uncomfortable with the intentional or unintentional deception. When regulators arrive, will they have to bend the truth or even lie about daily operations? Taking the time to establish and implement one set of approved SOPs that is compliant with both external regulations and internal standards is good for employee morale, productivity and ultimately, profits.

What’s the best way to get control of a facility’s SOPs? Again, break it into manageable steps:

First, task someone with reviewing all SOPs that are floating around. Determine if any are non-compliant, which ones need to be tossed and which ones need to be revised so they work for the company as well as outside regulatory authorities.

At a minimum, establish a two-person team to draft, review, publish and distribute the final SOPs. Ensure that at least one member of the team has management level authority. Assign that employee the responsibility of reviewing the SOPs before “publication” and distribution.

Archive, delete, or actually throw away outdated or non-compliant SOPs

Revise or create new best-practice SOPs that are in compliance with external regulations and internal standards

Establish a system to update SOPs when external regulations and internal standards change

Use a naming convention that distinguishes draft SOPs from final SOPs, for example, “Post-Harvest Procedure, FINAL”

Inform employees that they will be retrained on the new SOPs and that approved SOPs will always have the word “Final” in the title

Store the final SOPs in an easily accessible location and give employees access, not only during training, but on an ongoing basis

Centralized Repository for Final SOPs

Storing final, approved SOPs in one easily accessible, centralized location and giving employees access sounds simple, but again, this is the cannabis industry, so this often doesn’t happen. Many of us have or are currently working for an organization that stores SOPs in multiple places. Each department may have its own way of updating, disseminating and storing SOPs. Some SOPs are stored in a printed binder stuffed in a drawer or left on a bottom shelf. Others are stored digitally. Some use both systems, which creates confusion. Who knows if the digital versions or the printed versions are the most current? Surely someone knows, but often the front-line staff do not.“Once you’ve established a single set of compliant SOPs and have stored them in one accessible location, it’s time to train your employees.”

Establishing a centralized repository for final, approved SOPs is the foundation of operational excellence. It lets employees know that operations are organized and controlled, and it reassures regulatory authorities and external stakeholders—think insurers, bankers, investors—that the company prioritizes compliance and organization. And external stakeholders who believe that an organization is proactive and well-run tend to be more forgiving when the inevitable missteps occur. Companies that are organized, have effective training systems, regularly conduct internal audits to identify potential issues and take identifiable action steps when necessary to remediate issues, receive fewer deficiency notices, violations and fines than their less organized competitors.

Train Employees

Many states require cannabis operators to provide a specific number of training hours prior to an employee beginning work, and a specific number of continuing and refresher training hours annually. Once you’ve established a single set of compliant SOPs and have stored them in one accessible location, it’s time to train your employees. To do so, set clear expectations and decide who is responsible for what. Is the HR manager responsible for initial onboarding and training? Are department managers responsible for ongoing and annual training? Create a training responsibility chart that works best for your company; write it down and share with all stakeholders.

Documenting all key areas of operation on a recurring basis will help you keep track of a large facility and workforce

The next step is to figure out how to train your employees. Individuals have different learning styles, so ideally, you’ll offer multiple ways for them to master the requirements of their position. Assign written materials and if possible, attach short videos showing the best way to complete a task. Follow up with a quiz to determine comprehension and a conversation with a department lead or manager to answer questions and review the key take-aways. Ideally, the department manager or lead employee will work with the employee until they are competent and comfortable taking on new assigned tasks and responsibilities.

Sum It Up

Operational excellence begins with:

Knowledge of and access to current external rules and regulations and internal standards

One set of approved and easily accessible policies and SOPs that comply with both external and internal standards

An initial training system with clearly assigned roles, responsibilities, and goals

An ongoing training system with clearly assigned roles, responsibilities, and goals

Systems to:

Test knowledge before employees begin unsupervised work

Stay up-to-date with all changes to external rules and regulations and internal standards

Control policy and SOP revision process

Inform all stakeholders when policies and SOPs change

Test that employees understand new standards

Document all key areas of operation on a recurring basis

Address deficiencies and evaluate whether SOP revisions are warranted

Document and implement necessary remediation when necessary

For those of you rolling your eyes and thinking you don’t have time for this, ask yourself, “Can you afford not to?”

For those of you committed to operational excellence and doing what it takes to get there, congratulations on being a visionary leader. Your efforts will pay dividends for your own company and will help the cannabis industry grow into a well-respected, profitable industry that improves lives.

The rise in the number of optimistic regulatory frameworks instigated by various regional governments will positively anchor the forecast for the cannabidiol (CBD) market. The growing awareness regarding the benefits and effects of the product as an alternative treatment method has accelerated its preference among consumers and suppliers. Moreover, the continued advancements in the approval processes by various authorities worldwide have also made way for numerous opportunities supporting CBD market growth.

According to a report by Global Market Insights, Inc, the global CBD market size could exceed $108.8 billion by 2027.

Growing presence in cosmetics

The overall industry share from creams and roll-on products is poised to hit a 35.8% CAGR up to 2027. This is owing to the increasing scope of CBD in cosmetic applications as it is highly effective in treating skin conditions. This, as well as its anti-inflammatory characteristics from a medicinal perspective, are leading to increased demand for CBD products like creams and roll-ons.

Scope in the treatment of mental health

Some of the many infused products on the market today.

CBD market value from anxiety/stress applications exceeded USD 1.5 billion in 2020 due to the growing need for helping mental health. The World Health Organization reported that over 4.5% of the total population in Europe suffers from depression. This escalating anxiety and stress rate has encouraged healthcare practitioners to increasingly make use of CBD-based medications.

Higher demand for oral administration

Demand for oral cannabidiol administration held nearly 45% of the industry proportion in 2020 due to its growing preference considering the gradual relief of pain compared to other disorders. The increasing dependency on the oral administration route for product development by several manufacturers will add positive impetus to market growth.

Medical benefits of cannabis

Annual revenue of the CBD market from the segment of the market dealing with THC (and CBD) products is expected to cross USD 30.1 billion by 2027. This is largely due to its increasing penetration across various countries and regions on account of its legal status. Furthermore, the relatively higher THC content of the compound has led to its growing usage to combat medical conditions, including Alzheimer’s and Parkinson’s disease, among others.

Online distribution to see a considerable footprint

Ads for CBD products online regularly perform very well

The online CBD industry was responsible for more than 46% of the market in 2020. This is mainly due to the numerous advantages of online channels, like on-time delivery and adequate inventory, compared to their offline counterparts. Besides, this distribution platform minimizes the operational costs related to the maintenance of brick and mortar retail.

Australia to lead the regional landscape

Australia dominated the Asia Pacific CBD market by holding over 25% of the market share owing to the expanding geriatric population and the liberal stance of the regulating bodies in the region. The permittance to the medicinal and cosmetic use of CBD products is likely to spur regional adoption. The rising amendments in regulatory scenarios have also triggered awareness regarding the potential benefits of the product in the country. For instance, in April 2020, the Australian government released a new proposal for over-the-counter CBD in a bid to relax its narcotic scheduling whilst making it a Schedule 3 substance.

Providers of various CBD products are actively indulging in numerous growth strategies, like acquisitions and partnerships, to reinforce their market presence. For example, Mota Ventures Corp., in January 2020, acquired Spanish producer and online retailer, Sativida OU in a USD 2.2 million deal. The acquisition expanded the company’s presence in Europe and Latin America.

Although the demand for CBD is likely to experience certain hesitation from consumers in the short term, the market will witness lucrative growth in the long run. However, counterfeit and substandard quality products may potentially restrain industry expansion to some extent.

In this “Flower-Side Chats” series of articles, Green interviews integrated cannabis companies and flower brands that are bringing unique business models to the industry. Particular attention is focused on how these businesses integrate innovative practices to navigate a rapidly changing landscape of regulatory, supply chain and consumer demand.

4Front Ventures Corp. (CSE: FFNT) ( OTCQX: FFNTF) is a multi-state operator active in Washington, Massachusetts, Illinois, Michigan and California. Since its founding in 2011, 4Front has built a reputation for its high standards and low-cost cultivation and production methodologies earned through a track record of success in facility design, cultivation, genetics, growing processes, manufacturing, purchasing, distribution and retail. To date, 4Front has successfully brought to market more than 20 different cannabis brands and nearly 2,000 unique product lines, which are strategically distributed through its fully owned and operated Mission dispensaries and retail outlets in its core markets.

We interviewed Andrew Thut, chief investment officer of 4Front Ventures. Andrew joined 4Front in 2014 after investing in the company in 2011. Prior to 4Front, Andrew worked in investment banking and later moved on to public equity where he was a portfolio manager at BlackRock.

Aaron Green: How did you get involved in the cannabis industry?

Andrew Thut: I came at it from the investment side of things. I started my career as a junior investment banker right out of school and then I was a public equity analyst and Portfolio Manager. I ran small-cap growth portfolios for BlackRock where I was on the team for a better part of 11 years.

Andrew Thut, Chief Investment Officer of 4Front Ventures

One of my friends, Josh Rosen, who came from the finance industry, got interested in the cannabis industry really in 2008. He founded 4Front as a consulting company officially in 2011 and I came in as an investor. After that original investment, I left BlackRock and I was looking for something different to do. I was tired of chasing basis points and running public market portfolios. Josh said to me “This industry needs more talent,” and I became more and more involved at 4Front as the years went on. In 2014, I came into the business full time. Originally, I was someone that was kind of the gray hair in the room when we were applying for licenses. We had to go to different municipalities and convince them that we were going to be responsible license holders. I also spent a lot of time on the capital raising side for our business leveraging my career in corporate and more traditional public finance. These are incredibly complex businesses that require a fair amount of capital in some places. So, that’s how I originally got into the business.

These are complicated businesses in a lot of cases. The “sausage making” in cannabis is incredibly complicated. There’s friction at every step along the way. As an example, when you’re buying a building where you want to cultivate your product, you can’t get a mortgage from a typical bank.

While those of us that have been in the industry like to gripe and complain about it, this friction is also the opportunity. Because more traditional investors can’t invest in this industry yet, it allows us more time to build our businesses and have some protective moats around it from a competition standpoint until those folks do come in. So, all this friction is a pain and it’s brutal, but it’s also the opportunity here in cannabis.

Green: Can you speak to the transformation of 4Front from consulting to MSO?

Thut: The original business was consulting. Our original investor was sensitive about touching the plant – it’s one thing to offer services to a federally illegal business, it’s another thing to directly run a federally illegal business. For example, 4Front would have consulting clients that were interested in acquiring a license in Massachusetts. Because of our expertise and our standard operating procedures, we could apply for licenses in limited license states on behalf of our clients and help them show regulators competence and give the regulator’s confidence that these operators knew what they were doing. So, we would help our clients win the licenses and then once those licenses were won, our operations folks would come in and help them get up running.

When I came into the business we said, “well, geez, we have quite a track record helping clients win licenses and get open. If we’re good at winning these licenses and getting them open, why aren’t we just doing this on our own behalf?” So, in 2015, we shifted the business from consulting to being a multi-state operator. We leveraged our capabilities in regulatory compliance and winning licenses to go and get those on our own behalf. We also leveraged our financial expertise in M&A to add to our portfolio, so what we ended up with was a seven-state portfolio at the time.

Green: Chief Investment Officer is an uncommon title, even in the MSO space. What does your day-to-day look like?

Thut: I spend an awful lot of time helping management plot our strategy, and then figuring out how we are going to pay for our growth. Not only structuring finances for the company, but also having contact with our existing and new investors.

I spend a lot of my day to day thinking about where we want to be as a business and what geographies we want to be in. If you look at cannabis longer term, we have less interest in being cultivators or farmers. We think that’s going to be the most quickly commoditized piece of the value chain. We like retail as a business, but I think that we have less interest in managing hundreds of retail locations scattered across the country. We ultimately want to be a finished goods manufacturer. What we think is going to matter longer term is establishing low-cost production.

There is a lot of price elasticity in the end markets for cannabis meaning if you get customers a quality product at a much better price than the competitor, you’re going to take outsize market share. To offer that lower price, you have to be efficient. Over the years, we have figured out how to bring the labor cost out of our production. We have 25 different brands with 1000s of different SKUs of products that have dominant market share in states like Washington. And we’re now putting them into Illinois, Massachusetts, California, Michigan, and hopefully New Jersey.

Green: Do you have a preference towards acquisition, or do you seek growth through internal investments?

Thut: We are always weighing build versus buy. We want our products to have dominant market share, or very strong market share in every state we are in, and we have a lens towards what gets us there faster and most efficiently. For instance, we have two cultivation facilities and one production facility here in Massachusetts – about 15,000 square feet of canopy in the state. That will just about serve our three retail locations in Massachusetts.

Back to our bigger investment thesis, we believe that we should be a finished goods wholesaler in every state that we’re in. We know our products are incredibly well received and we know that consumers love our price point. In Massachusetts, for instance, we’re currently evaluating if we need more capacity from a cultivation standpoint and a production standpoint. And if we do where do the lines cross in terms of whether we should build versus buy that additional capacity?

We are currently in five states, including our facility in Washington has dominant market share in one of the toughest markets in the world for cannabis – somewhere close to 9% market share in Washington. Our brands are in the top 10 of every single category from flower to vapes, to edibles everything across the board. And what we’re doing our strategy is simple. It’s taking those tried-and-true products and operating procedures that have been so effective in Washington, and we’re replicating them in other states where we have licenses: Massachusetts, Illinois, and Michigan, California and hopefully New Jersey. We’re looking for more state, but we want to be deep in the states we’re in.

We also have a lot of confidence that you know, having been having translated some of these, having been able to effectively take our Washington success story and port it to other states. We’re looking for other states to sort of bring into the portfolio because we feel like we’re in a position now to stamp it out.

At our facility in Washington, which is the number one edibles manufacturer in that state, we produce the edible Marmas which is our the number one selling gummy in Washington. We produce 3,500 boxes of those in one shift using 25 people in Washington. Our facility is one of the lowest cost producers in the country.

We are opening what we think is going to be a very disruptive facility in Southern California right now. The facility is 170,000 square feet of purely automated finished goods production. So, rather than making 3,500 boxes of our gummy squares in one shift using 25 people, with the automation that we have in California, we can make 30,000 boxes. So, 10x one shift for the same number of people. We look more like the Mars Candy Company than most investors would think of when they see a typical cannabis company. We’re bringing that kind of scale and automation.

Green: What are some of the industry trends that you’re watching closely?

Thut: We keep a close eye on limited license states. States like Massachusetts and Illinois. For various reasons Massachusetts is very tough to get zoned. So, there’s going to be a limited number of players in a state like Massachusetts, which means you can have pretty good moats around your business and pricing will hold up over several years. We love limited license states like that, where price is going to hold up. On the other hand, we’re not afraid to enter a state like California where we think our low-cost production expertise uniquely qualifies us to go into a huge market like that and be disruptive and take a lot of the pie.

“You’re starting to see the market expand. There’s some anecdotal evidence that we’re taking a fair amount of share from the beer industry.”What we’re seeing in terms of industry trends, particularly on the THC side of this business, has just been phenomenally strong. You’ve had robust medical markets where, by and large, we’re seeing those dominoes start to fall quickly and going recreational. When that happens, the size of the market increases – call it from 2% of the population to as much as 10% of the population. So, from a state regulatory standpoint, having states go form medical to adult use is a huge deal in terms of the market opportunity.

We’re also seeing states get a lot more comfortable with the idea of selling cannabis. I’ve been around for close to seven years in this industry. When I started and I went into a municipality, and I said we wanted to open a cannabis store you’d have people following me to my car with pitchforks. As these municipalities open and public acceptance comes around, people are realizing that these stores are providing jobs and providing a good tax base for communities. So, the acceptance of cannabis has a snowballing effect that just continues to roll.

It’s not just the ultra-frequent users of cannabis who are totally driving the bus in terms of the demand growth for your business. You’re starting to see the market expand. There’s some anecdotal evidence that we’re taking a fair amount of share from the beer industry. So, the fundamentals of this industry are phenomenal. I think that we’re probably in the second inning of what is a mega-trend of legalization of cannabis and the investment opportunity here.

Green: I think one of the interesting things about the fundamentals is you’ve got this hardship of 280E, that all the companies are facing, and yet you still have groups that are surviving, profitable and growing. What are your thoughts on 280E’s effect on cannabis businesses? Do you foresee anything happening there?

Thut: There was a huge liquidity crunch in cannabis in 2019, meaning it was hard for people to come up with capital to grow their businesses. You had a bunch of companies that had licenses who didn’t really know how to operate and weren’t really focused on profitability. That liquidity crunch of 2019 made people get religious about being profitable and being efficient with capital allocation. Fast forward to 2021 and if you look at the top 10 cannabis MSOs in the US, I think we’re all profitable.

So, here you have an industry with accelerating top line growth and they’re already profitable. That profitability should only improve as you’re able to leverage your operating expenses and that’s a unique thing. When the internet craze was started in 1999 you had companies that a weren’t profitable, didn’t have business models, and no one really knew what they wanted to be. You have companies here in cannabis that are growing the top line 50% a year, and they’re profitable, and they’re trading at under 10 times EBITDA, which is totally disjointed.

Sen. Schumer unveiling the Cannabis Administration and Opportunity Act

So, that leads me to your question on to 280E. 280E has been a problem. Banking has been a problem. Having to list our companies over the counter instead of on exchanges like the NASDAQ and NYSE – that’s been a problem in terms of attracting capital. But the good news is Senator Schumer, Senator Booker and others have put out some bold initiatives on what they want to achieve from a legalization standpoint. From an investment standpoint, the biggest thing that investors should be focused on is access to banking, which is included in the senators’ proposed legislation.

Once we get access to banking services, the federal government is basically acknowledging cannabis as an industry will be able to not only have more traditional financing for our growth, but it will also lead to uplift into exchanges and real institutions like the Fidelity’s and the BlackRock’s of the world being able to come and invest in these companies. It also acknowledges 280E is an antiquated law. Getting rid of 280E will give us a much lower tax rate and will allow us to have a bigger proportion of our pretax cash flow into growing our businesses rather than having to go outside for that funding. My crystal ball is probably no better or worse than others in the industry, but if you fast forward 18 months to two years, I have a tough time seeing 280E still in place.

Green: Last question here. What’s the thing you’re most interested in learning about in the cannabis industry?

Thut: I’m just fascinated to see how these various business models will play out. People are placing bets on picks and shovels. People are placing bets on whether being a finished goods manufacturer works. People are placing bets on whether a retailer business model is going to win the day.

If you look at the leadership in the cannabis industry today, it’s totally different than it was four years ago. People that were foregone winners four years ago like MedMen had to do significant recaps. I put Acreage in that sort of bucket too. The leadership had shifted and so I’m really curious to see just from an intellectual standpoint, how this business evolves.

I sometimes scratch my head, you know, do you really want to be a cannabis company with 200 retail locations? You’re going to have a tough time growing same store sales in three to five years in 200 retail locations. So, I’m just most curious in proving out our thesis of being finished goods producers and low cost finished goods producers in the value chain. I’m most curious in seeing how that plays out. I think we are seeing our strategy play out in the most competitive markets in the world. We have a high degree of conviction that we’re on the right track here, but our eyes are always open and we’re always making little pivots here and there trying to make sure to stay on top of the sweet spot in the value curve.

If you describe the cannabis industry generically and you didn’t say cannabis, you said “widget” I think it’s the most fascinating Business School case ever presented. If you’re taking this market that already exists, it’s just illegal. So, all it needs to do is switch from the black market to the legal market and then you’re always trying to plot a course and steer the ship towards where the highest value creation can be. So, I’m fascinated to see how it’s going play out here.

Green: That concludes the interview. Thanks Andrew!

ACS Laboratory, a cannabis and hemp testing lab based outside of Tampa Bay, Florida, announced the launch of their “Tested Safe Certified Seal” program. The program is designed to help raise standards and put more consumer trust in safe, tested products.

The “Tested Safe Certified Seal” on a hemp oil product

ACS Laboratory is an ISO 17025-accredited and DEA-licensed cannabis testing company founded in 2008. Last year they were certified by the Florida Department of Health to perform cannabis testing for state-licensed cannabis companies. In addition, the company acquired Botanica Testing, Inc. in 2020, adding more than 500 hemp and CBD clients to their portfolio. They now perform hemp testing for clients in more than 44 states.

The “Tested Safe Certified Seal” program allows companies to adorn their products with the trademarked seal following testing, informing consumers that their product has met safety standards and a full panel of compliance tests. “Unlike a mandated QR code that links to a Certificate of Analysis (COA) with detailed test results, the Seal shows visual proof at a glance that consumers can trust a brand,” reads the press release.

The program is also endorsed by the American Cannabinoid Association (ACA). “It is exciting to see our industry legally providing cannabis and cannabis-derived products on a commercial scale,” says Matthew Guenther, founder of the ACA. “As with any consumer product, safety and quality control remain our absolute priority.”

To earn the seal, companies send their products to the ACS lab for a full panel of safety and potency tests. ACS has a scope of services that includes: potency testing for 21 cannabinoids, 38 terpene profiles, 42 residual solvents, screening for 105 pesticides, moisture content, water activity, microbiology panels, heavy metals screening, flavonoid testing for 16 profiles, micronutrient testing, mycotoxins, Vitamin E acetate, shelf life & stability, plant regulators (PGRS), PAH testing and Pharmacokinetic Studies (PK) aka human trials.

Cannabis is still federally illegal and is included on Schedule 1 of the Controlled Substances Act (CSA), along with such other substances as heroin, fentanyl and methamphetamines.1 It is a federal crime to grow, possess or sell cannabis.

Despite being federally illegal, 36 U.S. states and the District of Columbia have legalized the sale and use of cannabis for medical and/or adult use purposes,2 and both direct and indirect cannabis-related businesses (CRBs) are growing at a rapid rate. Revenue from medical and adult use cannabis sales in the US in 2019 is estimated to have reached $10.6B-$13B and is on track to reach nearly $37B in 2024.3

Because the sale of cannabis is federally illegal, financial institutions face a dilemma when deciding to provide services to CRBs. Should they take a significant legal risk or stay out of the market and miss out on a significant revenue opportunity? So far, the vast majority of financial institutions have been unwilling to take the risk, resulting in a dearth of options for CRB’s. Until recently, cannabis business operators had few options for financial services, but times are changing.

This piece will discuss current trends in banking for cannabis-related businesses. We will cover differences in legality at state and federal levels, complexities in dealing in cash versus digital currencies, Congressional actions impacting banking and CRBs and how banking is changing. The explosion of state legalization of cannabis over the past several years has had a strong ripple effect across the US economy, touching many industries both directly and indirectly. Understanding the implications of doing business with a CRB is both challenging and necessary.

Feds Versus States

Money laundering is the process used to conceal the existence, illegal source or illegal application of funds.4 In 1986 Congress enacted the Money Laundering Control Act (MLCA), which makes it a federal crime to engage in certain financial and monetary transactions with the proceeds of “specified unlawful activity.”5 Therefore, CRB transactions are technically illegal transactions under the MLCA.

Financial institutions therefore face a risk of violating the MLCA if they choose to do business with CRBs, even in states where cannabis operations are permitted. In addition, financial institutions could also face criminal liability under the Bank Secrecy Act (BSA) for failing to identify or report financial transactions that involve the proceeds of cannabis businesses operating legally under state law.6

Federal authorities continued to aggressively enforce federal cannabis laws

In short, because cannabis is illegal at the federal level, processing funds derived from CRBs could be considered aiding and abetting criminal activity or money laundering. States, however, began legalizing cannabis in 1996, and by 2009, thirteen states had laws allowing cannabis possession and use.7 Despite this legislation, federal authorities continued to aggressively enforce federal cannabis laws.8 That changed under the Obama administration when, shortly after being elected, President Obama stated that his administration would not target legal CRB’s who were abiding by state laws.[9] In an attempt to provide clarity in this murky environment, beginning in 2009, the Department of Justice (DOJ) issued three memos designed to guide federal prosecutors in this area. However, none of the DOJ memos issued from 2009 through 2013 addressed potential financial crime related to the legal sale or distribution of cannabis in states allowing the use of medicinal or recreational cannabis.

To assist financial institutions in navigating potential financial crime implications of banking CRBs, the Financial Crimes Enforcement Network (FinCen) issued guidance in 2014 that clarified how financial institutions could conduct business with CRBs and maintain compliance with their Bank Secrecy Act requirements (2014 Guidance).9 According to the 2014 Guidance, financial institutions may choose to interact with CRBs based on factors specific to each institution, including the institution’s business objectives, the evaluated risks associated with offering such services, and its ability to manage those risks effectively.

The 2014 Guidance requires those who choose to provide services to CRBs to design and implement a thorough customer due diligence review that includes, in part, analyzing the licensing of the entity, developing an understanding of the business operations of the entity, and ongoing monitoring of the entity.9 In addition, financial institutions are required to file a Suspicious Activity Report (SAR) for every transaction they process for a CRB, should they choose to accept the business.

Although the 2014 Guidance does outline a path for financial institutions to engage with CRBs, it does not change federal law and, therefore, does not eliminate the legal risk to financial institutions.10 By its very nature, the 2014 Guidance was a temporary fix, subject to changing views of different administrations, evidenced by the fact that all three of the DOJ guidance documents noted above were rescinded by then Attorney General Jeff Sessions on January 4, 2018.12 The DOJ enforcement posture could change once again in a Biden administration. Biden is on record as favoring decriminalization, and Attorney General candidate Merrick Garland has stated that if confirmed he will deprioritize enforcement of low-level cannabis crimes. Garland also believes using limited government resources to pursue prosecution of cannabis crimes states where cannabis is legal does not make sense.12

Because of the uncertainty and high risk, most banks remain unwilling to serve CRBs. Those that do serve CRBs charge exorbitant fees (fees of $750-$1,000 or more per account per month are not uncommon), pricing many smaller operators out of the financial services market.

Cash is King – Or Is It?

Cannabis operators have discovered the old adage “cash is king” is not necessarily true when it comes to the cannabis space. Bank-less CRBs are forced to utilize cash to pay business expenses, which can be particularly difficult. Utility companies, payroll companies, and taxing authorities are just some of the providers that are difficult, if not impossible, to pay in cash. For example, cannabis operators have been turned away from IRS offices when attempting to pay large federal tax obligations in cash. Likewise, cannabis operators have been unable to utilize payroll processing companies to administer payroll and benefits for their businesses because the processors won’t take cash. CRBs can’t use Amazon or other online retailers because online providers cannot accept cash.

Because dealing in cash is so difficult, CRB operators look for workarounds such as using personal credit/debit cards to purchase business equipment and supplies. This doesn’t eliminate the cash problem, however, because the credit card holder will likely have to accept cash as reimbursement. Such transactions could be considered an attempt to hide the source of the cash, which is, by definition, money laundering.

CRBs often have large sums of money onsite

Some bank-less CRBs try to skirt the system by obtaining bank accounts in the name of management companies or other entities one step removed from the actual business. While operators often choose this route in an effort to streamline business and operate out of the shadows, it again runs afoul of banking laws. Transferring cannabis related financial transactions to another entity is actually the very definition of money laundering – which, as noted above, is defined as the process used to conceal the existence or source of “illegal” funds.

In addition to the difficulties in making payments or purchasing business supplies, operating in a cash-heavy environment poses significant safety risks for cannabis operators. CRBs often have large sums of money onsite and transport large sums of cash when purchasing product or paying bills, making them a target for robbery. In 2017, there was a spate of dispensary robberies across the Phoenix Metro area, including one at Bloom Dispensary that took place during operating hours.13

Managing all that cash increases the cost of doing business as well, in the form of increased labor, insurance, and security costs. Cash must be counted and double counted, which can be time consuming for staff, not to mention the time it takes to deliver physical cash payments to hither and yon. Ironically, lack of banking significantly decreases transparency and clouds the waters of compliance, as operating strictly in cash makes it easier to manipulate reported financial results.

Potential Congressional Solutions

In recent years Congress has undertaken several efforts to pass legislation designed to address the state/federal divide on cannabis, which would likely clear the way for financial institutions to provide services to CRBs, including:

R. 1595 – Secure and Fair Enforcement Banking Act of 2019 (“SAFE Act”);

1028 & H.R. 2093 – Strengthening the Tenth Amendment Through Entrusting States Act (STATES Act); and

2227 – Marijuana Opportunity Reinvestment and Expungement Act of 2019 (MORE Act).

The climate in Washington DC, however, did not allow any of these initiatives to pass both houses of congress. Had any been sent to the White House, President Trump was unlikely to sign them into law.

The cannabis industry has new reason to believe reform is on the horizon with shift in political leadership in the White House and Senate. Newly anointed Senate Majority Leader Chuck Schumer recently committed to making federal cannabis reform a priority, and President Biden appears committed to decriminalization, reviving the hope of passage of one of these pieces of legislation.

The Changing Banking Landscape

Even though there is little in the way of formal protections for financial institutions, and with the timeline for a legislative fix unknown, an increasing number of banks are working with cannabis operators.

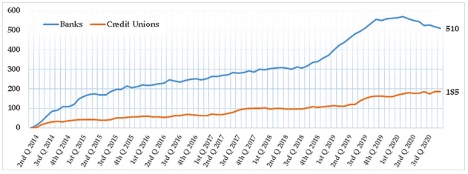

According to FinCen statistics, there were approximately 695 financial institutions actively involved with CRBs as of June 30, 2020. It is important to note that these statistics are based on SAR filings, which banks are required to file when an account or transaction is suspected of being affiliated with a cannabis business. However, some of these SARs may have been generated on genuine suspicious activity rather than on a transaction with a known cannabis customer.

Number of Depository Institutions Actively Banking Cannabis-Related Businesses in the United States (Reported in SARS)14

There are arguably more banking institutions offering services to CRBs than ever before. The challenges for CRBs are (1) finding an institution that is willing to offer services; (2) building/maintaining a compliance regime that will be acceptable to that institution; and (3) cost, given the high fees associated with these types of accounts.

How CRBs Get Accepted by Banks

The gap between CRBs’ need for banking and the financial services providers’ sparse and expensive offerings to the sector has created an opportunity for third-party firms to intervene and provide a compliance structure that will satisfy the needs of the financial institutions, making it easier for the CRB to find a bank.

These third-party firms perform extensive BSA-compliant due diligence on applicants to ensure potential customers are following FinCen guidance required to receive banking services. After the completion of due diligence, they connect the CRBs with financial institutions that are willing to do business with CRBs and provide checking/savings accounts, check writing capability, and merchant processor accounts. These firms often provide additional services such as armored car and cash vaulting services. Some of these firms also offer vendor screening, pre-approving vendors before any payments can be made.

One such firm, Safe Harbor Private Banking, started as a project implemented by the CEO of Partners Credit Union in Denver, Colorado, who set out to design a cannabis banking program that would allow Partners to do business with Colorado CRBs.15 The program was successful and has since expanded into other states who have legalized cannabis. Other operators include Dama Financial and NaturePay.

While these services offer hope for many CRBs, the downside is cost. These services perform the operations necessary to find, open, and maintain a compliant bank account; however, the costs of compliance are still high, pricing some small operators out of the market.

Is Digital Currency an Answer?

Digital currency is also making its way into the cannabis world. Digital currency, or cryptocurrency, is a medium of exchange that utilizes a decentralized ledger to record transactions, otherwise known as a blockchain. One of the largest benefits of blockchain is that it is a secure, incorruptible digital ledger used for, among other things, financial transactions.16 Blockchain technology offers CRBs a transparent and immutable audit trail for business and financial transactions. Several cannabis-specific cryptocurrencies have sprung up in the past several years, including PotCoin, CannabisCoin, and DopeCoin, to name a few.

In July 2019, Arizona approved cryptocurrency startup ALTA to offer services to the state’s medical cannabis operators.17 ALTA describes itself as a “digital payment club where cash-intensive businesses pay each other using digital tokens instead of cash.”18 ALTA members purchase digital tokens that are used to pay other members using a proprietary blockchain based system. The tokens are redeemable for US dollars at a stable rate of 1:1, and CRBs do not need a bank account to participate in the ALTA program.

ALTA proposes to pick up members’ cash and exchanges it for tokens, which are then used to pay other members for goods and services. Tokens may be redeemed for cash at any time.18 The company has been approved by the Arizona State Attorney General, and one of the first members they hope to enlist is the Arizona Department of Revenue (ADOR). Enlisting ADOR into the program would allow dispensary members to pay state taxes digitally rather than hauling large amounts of cash to ADOR offices.

Similarly, Nevada recently contracted with Multichain Ventures to supply a digital currency solution to the Nevada cannabis industry. Nevada Assembly Bill 466 requires the state create a pilot program to design a “closed loop” system like Venmo in an effort to reduce cash transactions in the cannabis sector. Like ALTA, Nevada’s proposed system will convert cash to tokens which can then be transacted between system participants.19

While both proposals are promising for Arizona and Nevada CRBs, the timeline as to when, or if, these offerings will come online is unknown. Action on cannabis reform at the federal level may render these options moot.

Looking to the Future

Although states are legalizing cannabis in one form or another in growing numbers, the fact that cannabis is still federally illegal poses a significant barrier to accessing the financial services market for CRBs. While most banks are still reluctant to offer services to this rapidly growing industry, there are more banks than ever before willing to participate in the cannabis industry. Recent changes in leadership in Washington DC offer a positive outlook for cannabis reform at the federal level.

As the “green rush” continues to envelop the country, financial services options available to CRBs are slowly growing. Many new options are now available to help CRBs find a bank, develop compliance programs, and manage the cash related problems encountered by most CRBs. However, these solutions may be out of reach for the budget-conscious small operator. Also, there are a number of cryptocurrency solutions designed specifically for CRBs; however, when, or if, these solutions will gain significant traction is still unknown.

References

Controlled Substances Act, 21 U.S.C., Subchapter I, Part B, §812.

“State Marijuana Laws”; National Conference of State Legislatures, February 19, 2021.

“Exclusive: US Retail Marijuana Sales On Pace to Rise 40% in 2020, near $37B by 2024”. Marijuana Business Daily, June 30, 2020.

Kaufman, Irving. “The Cash Connection: Organized Crime, Financial Institutions, and Money Laundering”. Interim Report to the President, October 1984.

S. Code § 1956 – Laundering of Monetary Instruments.

Rowe, Robert. “Compliance and the Cannabis Conundrum.” ABA Banking Journal, September 11, 2016.

“History of Marijuana as a Medicine – 2900 BC to Present”. ProCon.org, December 4, 2020.

Truble, Sarah and Kasai, Nathan. “The Past – and Future – of Federal Marijuana Enforcement”. org, May 12, 2017.

Sessions, Jefferson B. “Memorandum for All United States Attorneys”. January 4, 2018.

“Attorney General Nominee Garland Signals Friendlier Marijuana Stance”. Marijuana Business Daily, February 22, 2021.

Stern, Ray. “Robbers Hitting Phoenix Medical Marijuana Dispensaries: Is Bank Reform Needed?” The Phoenix New Times, April 11, 2017.

FinCen Marijuana Banking Update, June 30, 2020.

Mandelbaum, Robb. “Where Pot Entrepreneurs Go When the Banks Just Say No.” The New York Times, January 4, 2018.

Rosic, Ameer. “What is Blockchain Technology? A Step-by-Step Guide for Beginners.” com, 2016.

Emem, Mark. “Marijuana Stablecoin Asked to Play in Arizona Fintech Sandbox.” CCN.com, October 25, 2019.

http:\\Whatisalta.com\

Wagner, Michael, CFA. “Multichain Ventures Secures Public Sector Contract with Nevada to Supply Tokenized Financial Ecosystem for the Legal Cannabis Industry”, January 26, 2021.

As the legalization of cannabis in the U.S. continues to grow, stringent regulatory requirements around the country are being adopted to ensure that only safe and high-quality cannabis is sold. The U.S. cannabis testing market is estimated to see tremendous growth over the coming years. Further, the FDA has made several resources available for addressing cannabis products like CBD to ensure that consumers and stakeholders are getting safe products.

Prominent players operating in the U.S. cannabis testing market such as CannaSafe, Anresco, Collective Wellness of California, EVIO Inc., Digipath Inc., PSI Labs, SC Labs, Inc., Steep Hill, Inc. etc. are focusing on developing enhanced cannabis testing solutions and accreditation for gaining strong market presence. For example, earlier this year SC Labs developed a comprehensive hemp testing panel that is purported to meet testing standards in every state with a hemp program.

Citing another instance, in 2019, a leading cannabis resource Leafly, introduced the Leafly Certified Labs Program, under which a network of labs is independently assessed by Leafly for quality and accuracy. This program has been designed to address inconsistency in cannabis testing by ensuring that lab data comes from labs that have been confirmed to provide accurate results.

Rising adoption of high-pressure liquid chromatography (HPLC) technique

A lot of cannabis testing procedures are carried out using liquid chromatography. It is estimated to witness higher preference over the coming years. In 2020, the liquid chromatography segment recorded a valuation of USD 662.4 million. Further, liquid chromatography is a valuable alternative to gas chromatography when it comes to analysis of cannabinoids, pesticides and THC which is why this technology is often preferred for potency testing as it offers more precise analysis. Moreover, purification standards are highly controlled in liquid chromatography which helps in obtaining accurate results, which is complementing the segment growth.

Growing popularity of heavy metals testing for cannabis

Cannabis samples are liquified in strong acid in a pressurized microwave prior to evaluation for heavy metal content. Image courtesy of Digipath, Inc.

Heavy metals are known to be one of the major contaminants found in cannabis and its products apart from residual solvents, microbial organisms and pesticides. In addition, heavy metals are highly toxic in nature and on exposure can lead to poisoning and other complications. As a result, heavy metal testing for cannabis and its products is increasingly becoming popular. Several government organizations have made heavy metal testing mandatory for cannabis products. Moreover, increasing legalization of cannabis across several countries for adult use and medical purposes is likely to instigate the demand for heavy metal testing of cannabis products, thereby fostering the growth of heavy metals testing segment over the coming years. For the record, in 2020, the segment had recorded a market revenue of USD 352.5 million.

Increasing support from government bodies in the Mountain West

With increasing legalization for medical and adult use, the cannabis testing market in the Mountain West zone of the U.S. is likely to observe a tremendous growth over time. Moreover, growing support from various government bodies is playing a key role in enhancing the business space. For example, Montana’s Department of Revenue helps labs get licensed along with the state’s environmental laboratory that oversees inspections and licensing. Further, presence of a large number of cultivators of cannabis and manufacturers of cannabis-based products are also positively influencing the regional market growth. Considering the significance of these growth factors, the U.S. cannabis testing market in the Mountain West is estimated to register a substantial CAGR of 9.6% through 2027.

As sales of Delta 8 increase, hemp and cannabis industry infighting increases right along with it. Some hemp leaders say they object to Delta 8 simply because it’s intoxicating: “Hemp is nourishing….hemp is not intoxicating,” the president of the U.S. Hemp Authority President told Hemp Grower (apparently cannabinoids can only be one or the other). Others claim that Delta 8 itself is unsafe: “Very little is known about the health effects of Delta 8,” warned the media relations director for the National Cannabis Industry Association. The U.S. Cannabis Council called Delta 8’s growing popularity “a rapidly expanding crisis” in a report that includes the heading “The Health Risks of Delta-8 THC” and claims Delta 8 “presents a public health risk of potentially wider impact than the vape crisis.”

As a cannabis and hemp industry veteran and a long-time maker of numerous hemp-derived formulations (including Delta 8 products) I have to ask: who exactly is Delta 8 a crisis for, and why? I agree that we need to address the legitimate issues with Delta 8 manufacturing and create regulatory oversight that ensures consumer safety. But some Delta 8 critics may be more concerned with their own bottom line than with protecting public health. No one wants another vaping crisis, but demonizing a newly popular cannabinoid or trying to get it banned doesn’t solve the problem of an unregulated space—and it won’t end the demand for Delta 8, either.

The chemical structure of Delta 8 THC.

John Kagia of New Frontier Data points out that the Delta 8 boom is “a phenomenon that has taken the industry quite by storm”—and while that storm’s rising tide saved many hemp farmers from financial ruin, it has not lifted every boat. Some cannabis leaders consider Delta 8 an incursion into “their” market. Indeed, Delta 8 can be sold in some states where cannabis remains illegal: “Unregulated Delta 8 risks becoming a competitive threat to [cannabis companies’] existing offerings, sold in states they can’t get into,” reported Tiffany Kary at the Chicago Tribune. But the threat here for cannabis operators isn’t Delta 8: it’s Prohibition. In states where cannabis is illegal, Delta 8 (which is remarkably similar in molecular structure to its federally illegal chemical cousin Delta 9) is being purchased as an alternative. Rather than villainizing a cannabinoid, let’s address retrograde, reactionary state legislatures that refuse to listen to the will of their constituents, and outdated federal laws that equate THC with heroin.

Many see Delta 8 as a threat to the licensed cannabis industry’s profit margins, not only because it can be sold in prohibition states, but because its unregulated status makes it far easier and cheaper to make and sell. Cannabis companies have to navigate an overwhelming and burdensome maze of regulatory red tape to maintain compliance, so industry-wide frustration with the total lack of oversight for Delta 8 is both understandable and justified. But calling for statewide bans on a product that competes with yours is not the solution. That’s not how markets work. (Of all people, cannabis industry professionals should know that banning cannabinoids doesn’t make them go away.) Regulating Delta 8 manufacturers and requiring rigorous product testing are reality-based measures that will make the playing field fairer for cannabis while also safeguarding public health. In the meantime, we can strongly encourage Delta 8 consumers to seek out products made by ethical operators that are transparent about their manufacturing process and provide third-party testing results—the exact same protocol we recommend for buying CBD.

Some of the many hemp-derived products on the market today.

The safety of Delta 8 products is another legitimate concern that’s unfortunately been distorted. Some alarmist headlines seem to equate the actual cannabinoid itself with hazardous material. One East Coast CBD manufacturer issued a press release announcing “a warning for consumers and manufacturers about potentially harmful chemicals within Delta 8 THC” with the cable-newsworthy headline “Dangerous Delta 8?” Smearing Delta 8 as an inherent health menace is both misleading and unhelpful. As Rick Trojan, vice president of the board of directors of the Hemp Industries Association points out, “Cannabinoids themselves have never in the history of humanity caused a death by themselves.” Once again, the problem here isn’t the actual cannabinoid: it’s the lack of regulation that allows Delta 8 products to be produced with no oversight or testing. But given Delta 8’s widespread popularity, short-sighted bans like the ones that have been passed in 17 different states will only increase the risk to public health. Retailers nationwide sold at least $10 million worth of Delta 8 products last year. I guarantee that demand will continue, and that these bans will simply empower an illegal market full of bad actors.

Finally, I remain shocked at the contempt aimed at Delta 8 because it’s psychoactive, and at those who consume it for just “wanting a cheap high.” As with all cannabinoids, we need more clinical research into Delta 8’s properties—but the research we do have indicates that Delta 8 actually has therapeutic properties very similar to Delta 9 THC, just with less psychoactivity. Anecdotal reports indicate that Delta 8 offers many of the health benefits of Delta 9 (help with sleep problems, stress, and pain management) without THC’s less-enjoyable side effects, like paranoia. As cannabis specialist and medical doctor Peter Grinspoon told Insider, “I can’t tell you how many patients I have who say, ‘I’d love to use medical cannabis instead of opiates for pain, except it makes me anxious.’ Delta-8 might be a very good option for people like that.” Believe it or not, there are plenty of people who are using Delta 8 for its therapeutic effects—which, in a nation where 136 citizens die from opioid overdoses daily, I think should be encouraged rather than derided.

With more than 140 known cannabinoids, it makes no sense for us as an industry to brand some of them as “bad” and others as “good.” Are we going to have these tugs-of-war and calls for bans over every single cannabinoid that becomes popular? Instead of arguing amongst ourselves, we could instead focus our efforts on legalizing all of these plant compounds, studying them to determine their capabilities, and creating standardized, evidence-based regulations and testing regimens to ensure consumer safety and adult use. Delta 8 is popular because it serves a need. Consumers want it, and it’s here to stay—the sooner that we as an industry recognize those facts, the better.

In 2002, Dale Katechis revolutionized craft beer. A seemingly simple packaging decision, putting craft beer in a can, sparked an international movement and put craft beer on the map.

Before the craft beer market really gained steam, consumers associated good beer with glass bottles and larger brands selling cheap beer with cans. Through education, creative marketing and a mission to put people over profits, Dale helped the craft beer market expand massively while sticking to his roots. He also managed to convince people to drink good beer from a can.

When Dale founded Oskar Blues about twenty years ago, he didn’t just succeed in selling beer. Through collaboration and information sharing, Dale propelled craft beer as a whole and lifted all boats with a rising tide. He’s hoping to achieve similar results with his new role in the cannabis space.

Dale Katechis, Founder of Oskar Blues & recent addition to the Veritas Fine Cannabis team

Veritas Fine Cannabis, the first craft cannabis cultivator in Colorado, announced that Dale joined the company’s leadership team. Jonathan Spadafora, partner and head of marketing and sales at Veritas, told us that he’s excited about working with Dale. He says Dale is already helping them open a whole world of branding and marketing opportunities. “This is our Shark Tank moment – we’ve got someone who’s been through the fire before and will help us keep differentiating, finding new avenues and new ways to solve problems,” says Spadafora.

His colleague, Mike Leibowitz, CEO of Veritas, shares the same sentiment. “Dale maintained company culture and quality as he grew Oskar Blues into a household name,” says Leibowitz. “Maintaining our unique company culture is paramount as we work to build Veritas Fine Cannabis into the same.”

Dale’s role in the leadership team at Veritas is about sticking to his roots. Through raising industry standards in the best interest of quality products and consumers, the team at Veritas hopes to expand the brand nationally, just like Oskar Blues did, while instilling a culture of disruption and innovation without compromising quality.

We caught up with Dale to learn more about his story and what he hopes to bring to Veritas, as well as the cannabis industry at large. And yes, I had a couple of Dale’s Pale Ales (his namesake beer) later that evening.

Aaron Biros: Your success with Oskar Blues is inspiring. Taking an amazing beer like Dale’s Pale Ale and putting it in a can sounds simple to the layperson, but you launched a remarkable movement to put craft beer on the map. How do you plan to use your experience to help Veritas grow their business?

Dale Katechis: I am hoping that I can apply some of the lessons that I’ve learned through making mistakes of growing a business from the ground up. There’s obviously a lot of road blocks in cannabis and that is certainly one of the qualities of Veritas – how they’ve grown and how they had to do it in an environment that is much more challenging than the beer space.

My experience in small business development could potentially help them navigate this next renaissance of the space. I’m going to help them compete and bring the industry to a level that helps everybody win. I certainly felt that way in the craft beer movement. It was very important to us to bring the whole industry along because we were educators, we weren’t salesmen. In doing that, lifting everyone to a level where the industry benefits as a whole is a part of small business growth. To me that’s the most fulfilling part. It wasn’t just about the Oskar Blues ego at the time, it was about the craft beer scene. And what’s happening in cannabis now is very similar to what happened in the nineties with the craft beer scene.

Aaron: How did you get interested in joining the cannabis industry? What made you choose Veritas?

Dale: Most of my life, I’ve been an enjoyer of cannabis. Very recently, in the last two years, I’ve been intrigued by getting involved in the space. I’ve been shopping around for opportunities and nothing really excited me until I met Jon Spadafora and Mike Leibowitz.

It was really the two of them, the comradery and how they treat their staff that was so similar to the culture at Oskar Blues. Call it a “passion play” if you will, but this was the best opportunity to get involved with a small company and hopefully be a value add for them being in the room and sharing ideas.

Aaron: As a pioneer and leader in the craft beer space, do you notice any commonalities between the growth of the craft beer market and the legal cannabis market?

Dale: It is kind of crazy how many similarities there are. Not just the industry as a whole, but specifically the commonalities between my business, Oskar Blues, and Veritas. Overall, that’s really what allowed me to want to lean in a bit more. I wasn’t in the place where I wanted to start anything on my own. I didn’t want to be involved in fixing anything. I’ve been involved in those situations before and I’m at a point in my life that I don’t want to fix anything. Thankfully there’s nothing that needed to be fixed at Veritas. That was an exciting piece of the equation for me.

Dale takes in the view, getting up close and personal with the plants at a Veritas cultivation facility

Back to your question, how the consumer looks at cannabis versus how the consumer looks at beer in the craft beer space is very similar. There is a bit of an educational piece that’s happening where it’s almost a requirement in the cannabis industry and Veritas is leading that charge out front.

That’s what’s going to catapult Veritas and other companies if they follow suit. It’s their mentality and their philosophy of bringing the industry along as a whole, and I think it’s going to end up boding well for the consumer. The craft beer space was the same.

We had to educate people on a beer can and why we felt like a can of beer was important and exciting. The industry and the consumer associated cans of beer with large, industrial lagers and the can got a bad rap as a result. Not because it wasn’t a great package, but because they were putting bad beer in a good package. So, we had a long road of educating the consumer on the benefits of the can and I think what Veritas is doing with packaging now, how they use quality as such a fundamental pillar of their business, how they focus on the employee experience and the consumer experience sets them up for success, instead of just looking at the bottom line.

I’ve said it throughout my entire career, and at Oskar Blues, we never focused on the profits. You do the right thing for the biggest group of people moving the ball forward and the bottom line takes care of itself. Jon and Mike understand that so I don’t need to fight that battle. It’s another big similarity to the craft beer space.

Aaron: How can cannabis companies keep their craft? How can we, as an industry and as individual businesses, celebrate craft cannabis and follow in the footsteps of independent craft beer?

Dale: I believe that we’re starting to see some of that consolidation [that has been taking place in the craft beer market]. We’re at a time in the market right now where companies with such a solid foundation like Veritas don’t need to go that route to grow. I think we’ll start to see a lot more consolidation in the cannabis industry soon.

Veritas CEO Mike Leibowitz (right) showing Dale (left) a fresh harvest

Back to the point of bonding together as an industry and as a whole. Championing some of the regulatory hurdles that are coming and sticking together is crucial. One company can’t do it. There’s going to have to be some comradery in the industry among everyone trying to hold the bar up high instead of racing to the bottom. You die by a thousand cuts. I’ve lived that life in craft beer and we saw what happened 6-7 years ago when the industry overexpanded because of exponential growth. A lot of egos got in the room, and a lot of breweries spent a lot of money building out capacity and then that same year the market popped out. Everyone who didn’t have a solid foundation, got washed out of the industry.

That’s why I appreciate what Jon and Mike are doing and how they built Veritas. It’s very similar to how we built Oskar Blues. We had humble beginnings; we didn’t spend money on things outside of our core competency. We focused on quality, employee experience, morale and holding on to the culture of Oskar Blues. That’s what Jon and Mike are doing with Veritas and I think that’s really important.

In this “Flower-Side Chats” series of articles, Green interviews integrated cannabis companies and flower brands that are bringing unique business models to the industry. Particular attention is focused on how these businesses integrate innovative practices to navigate a rapidly changing landscape of regulations, supply chain and consumer demand.

Jushi Holdings Inc. (OTCMKTS: JUSHF | CSE: JUSH) is a multi-state operator with a national footprint and core markets in Illinois, Pennsylvania and Virginia, with developing markets in California, Nevada, Massachusetts and Ohio. In addition, Jushi maintains offices in Colorado, New York and Florida. In Q1 2021 they posted $42M in revenue representing 30% growth over Q4 2020 and 77% of their sales were conducted online. Jushi brands include Beyond / Hello, The Bank, The Lab, Tasteology, Sēchē, Nira CBD and Nira+ Medicinals.

We interviewed Andreas “Dre” Neumann, Chief Creative Director of Jushi Holdings. Dre joined Jushi in February 2020 after connecting to the founders through a colleague and running a large user experience research project. Prior to Jushi, Dre cut his teeth in advertising and branded entertainment. He was a startup founder at TalentHouse.com and a Partner at Idean, which he later sold to Capgemini.

Aaron Green: How did you get involved in the cannabis industry?

Andreas Neumann: I’m a guy who has been interested in many genres – I’m always looking for the next big thing. I started out in advertising and then I faded into branded entertainment when the traditional advertising wave was kind of shaky due to the digital attack of the internet with platforms like Facebook and Myspace.

I’ve also been fascinated by digital which led me to move into Silicon Valley. I had a startup called TalentHouse.com which was like LinkedIn for creative people. I learned a lot there about building a company in Silicon Valley. It was the first time I was confronted with experienced customer and user experience people. CX and UX was already kind of a thing in Silicon Valley at the time. My last company I was a partner in was a company called Idean, a Silicon Valley-based user experience company which we sold to a French company called Capgemini about four years ago.

I continue to be involved in the entertainment industry as kind of a creative outlet. I’m working with a lot of big rock bands like The Foo Fighters and Queens of the Stone Age. I just did the last Foo Fighter album. Photography is my last domain of total creativity where I can do whatever I want specifically in the rock business.

Andreas “Dre” Neumann, Chief Creative Director of Jushi Holdings Inc.

Coming to the cannabis point, I was actively looking for a partner to do a cannabis brand with The Queens of the Stone Age. I met Jushi through a very interesting coincidence. I was on the way to do a shoot in Silicon Valley with a guy called Les Claypool, who is from a famous band called Primus. I shot Les there and I was driving through Silicon Valley and remembered I had a friend nearby I should talk to. So, I called him and he was in Singapore. He called me right back (he never calls back normally) and said “You’ve got to talk to Jushi! You’ve got to talk to these guys Jim Cacioppo and Erich Mauff (two of the founders). They are starting something very exciting. They could be your partners.”

This is where the conversation started. It was my first time confronting a cannabis MSO and understanding how this works. I had just exited from my last agency and put together the best people from my previous endeavor to create a new sort of “creative collective” of UX and marketing experts. We did a test project for Jushi, a big research project on cannabis for California in retail, which was super interesting. It was a 200-page document – the first phase of user experience of the process before you build something – and through that I saw this as a big opportunity. I spoke to the founders again and came fully onboard in February 2020, just before the pandemic hit. From then on, it’s been a real amazing journey with me and the team. And it was the right moment to jump on the Jushi train as it was just about to leave the station.

Green: Can you talk about some of the geographies you are active in?

Neumann: Jushi is a multi-state operator. The most important state for Jushi is Pennsylvania. That’s where we have the most stores and we are building more stores there this year as well, very aggressively. We currently have 13 Beyond / Hello medical cannabis dispensaries in the state with many more to come, bringing an unmatched in-store experience, coupled with online reservations and in-store express pick-up.

The next important market for us is Virginia. We have a unique position there in Manassas with a cultivation facility and manufacturing and extraction facility, with the license for up to six stores. We started store number one in the facility, and we are rolling it out in HSA II. We are the only ones who can open stores in HSA II and this is straight on the border to Washington D.C. We call Virginia the “sleeping giant.” So much happened in the last year in Virginia around regulation and the industry, and now flower is finally legal.

Then we have Illinois – super interesting stores there. We have two flagship stores located straight on the border of Missouri, basically in East St. Louis. They are our biggest performers in the whole network because of the location. You have people coming over from Missouri, which is really in the beginnings of a medical market, and Illinois, which is now adult use. It was a super cool experience to see a medical market change to adult-use and be part of that change.

In other states, we recently announced the acquisition of Nature’s Remedy in Massachusetts, where we will have cultivation, processing and stores there. In Nevada, we have a grower-processor and we’re looking at opportunities in retail as well. At the moment, we have all our brands launched there. We are also continuing to build out our processing and cultivation capabilities in Ohio.

Last but not least is California. I’m based in California and the whole creative team is here. It’s a vanity market and it’s very competitive, but you’re in the capital of the world of cannabis in terms of brands and retail. California is in the future compared to the other states. So, we need to be here. It’s just like a soccer team. You must compete against good people or you’re not going to grow. So, that’s why competing here in California is key.

Green: How do you think about brand development, specifically in the cannabis CPG space?

Neumann: California is the king of brands. There are more products than brands in the cannabis industry at the moment. The products may have nice packaging, but brands aren’t really out there yet. The only states where you have “brands” as I would call them are California, Colorado and Oregon. I think we are just about to get to the place where the first rush is over and people with more experience about brands come in and build on the story of the brand. The myths, the cult, the legend of that story is important, and I think this is just about to get started.

Our brands, The Bank and The Lab, have good stories. They have been around a long time. We acquired them from a company in Colorado and we rolled them out in Nevada with a total revamp of look and feel as well as story. The Bank is celebrating this kind of roaring 20s idea. We have a lot of images, from black and white prohibition-style photos to this black-gold, very high-end, adult use tailored brand.

Vaping products from The Lab brand in Colorado

The Lab is a solid vaping brand from Colorado, and one of the 8th best-selling vape brands of all time. We revamped The Lab image to “take the lab out of the lab.” So basically, take the hairnet and the lab coat out of the vibe and add a whole new energy, with symmetry and nature in a leading role.

Tasteology, which is one of our self-made, self-created brands, was all based on customer research. In Pennsylvania, we have thousands of people we can communicate with, and we can test our brands. So, we’ve done focus groups and testing to see what sticks, and the name Tasteology came out of a huge research project with hundreds of names.

The last brand comes back to your question “Where are the brands going?” I think our brand Sēchē is the first one of our own creation and has this total lifestyle feel. It’s fine grind flower which normally might make its way to extraction. We treat it well and then we sell the raw flower, as well as a pre-roll line. It’s this kind of a young, cost effective, very affordable pre-roll and pre-ground brand, which is fabulous. And Sēchē really gets a lot of traction – flies off the shelves in Pennsylvania. It is a great product.

So, this is now the first stage where brands are created, but I think overall, there’s not many brands yet. They have to find their stories and their real purpose, I think. But California is ahead of it. And there’s some of them coming out now. So, I think there’s a new wave coming. It always goes in phases.

Green: How do you think about brand partners?

Neumann: We did the first step towards outside partnerships recently. We just partnered with Colin Hanks, Tom Hanks’ son, on his handkerchief line called Hanks Kerchiefs and we’re going to sell these in our stores. Hanks Kerchiefs has nothing to do with cannabis, but it takes our stores to a place where it’s not only cannabis products, it’s more the retail scene, the lifestyle scene. If we go into future partnerships with people, we would partner with big talent agencies to create something special. Maybe it’s limited editions, maybe it’s something more story-driven, but it doesn’t have to be there forever. I see using outside partnerships for more “drops,” as we call it. But we will see. You cannot force these collaborations. They have to come at the right time and need to be real. That’s what people feel. If it’s real you can feel it.

Green: Do you notice any differences in consumer preferences between the states you’re in and do you have to tailor your messaging differently?